The Ultimate Showdown in Handheld Smart Imaging: DJI's Ecosystem Moat and Insta360's Risk of Falling Behind

05/25 2026

05/25 2026

730

730

As the consumer electronics industry generally languished in an "involutionary" stock game (inventory competition), the handheld smart imaging market staged an astonishing counter-trend surge in 2025.

As the consumer electronics industry generally languished in an "involutionary" stock game (inventory competition), the handheld smart imaging market staged an astonishing counter-trend surge in 2025.

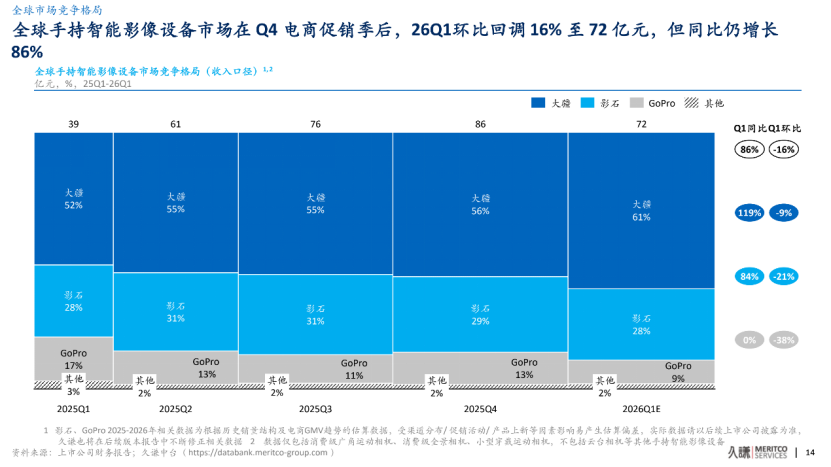

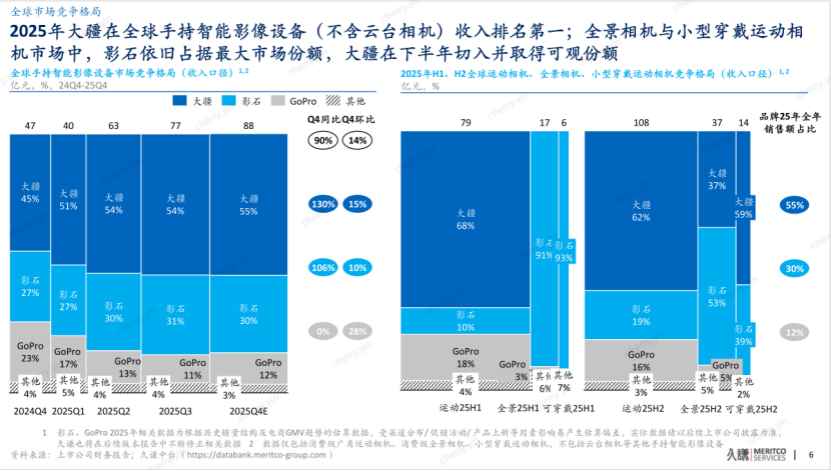

According to the latest report released by the authoritative institution Qianzhan Consulting, driven by intensive technological iterations and rich product offerings from leading brands, the global handheld smart imaging market (including action cameras, panoramic cameras, and small wearable cameras) experienced explosive growth in 2025, with year-on-year revenue growth reaching a staggering 96%. Amidst this activated blue ocean, a highly dominant giant emerged—DJI.

With a 55% global market share, DJI not only left its former pioneer GoPro (12%) far behind but also absolutely suppressed the track (track) star Insta360 (30%). By the first quarter of 2026, the latest data from Qianzhan Consulting showed DJI's share further rising to 61%, while Insta360's dropped to 28%, widening the gap from 25 to 33 percentage points and intensifying the industry's polarization.

As competition shifted from single hardware parameter comparisons to a comprehensive "technology + ecosystem" battle, this spectacle of "supply innovation activating demand" was essentially an uneven dimensional reduction strike. DJI's ability to "dominate from entry" stemmed from its escape from traditional traps of "parameter stacking" and "minor scenario innovations," instead reshaping industry rules from the industrial chain (supply chain)'s uppermost level—customizing underlying hardware and setting accessory ecosystem standards.

01 DJI's Core Strengths: Triple Barriers of Technology, Products, and Supply Chain

1. Supply-Side Foundational Innovation: Redefining Industry Technical Standards

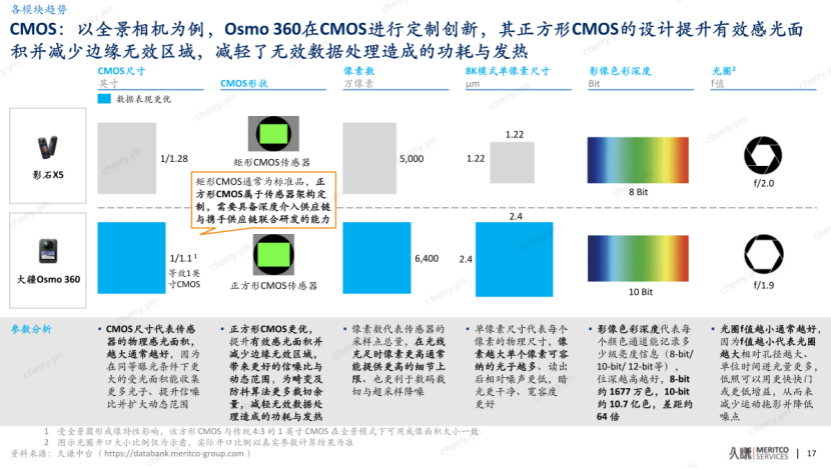

Qianzhan's 2025 report clearly stated that the market's 2025 explosion was fundamentally a victory of supply-side innovation, with DJI's core advantage deriving from its customized R&D capabilities deep in the upstream supply chain. Unlike the industry's prevalent standardized solutions, DJI pioneered square CMOS sensors in consumer imaging devices. Despite high customization costs and technical integration risks, this design perfectly aligned with users' "shoot first, frame later" habits, supporting free cropping across platforms without quality loss—a classic case of differentiated competition.

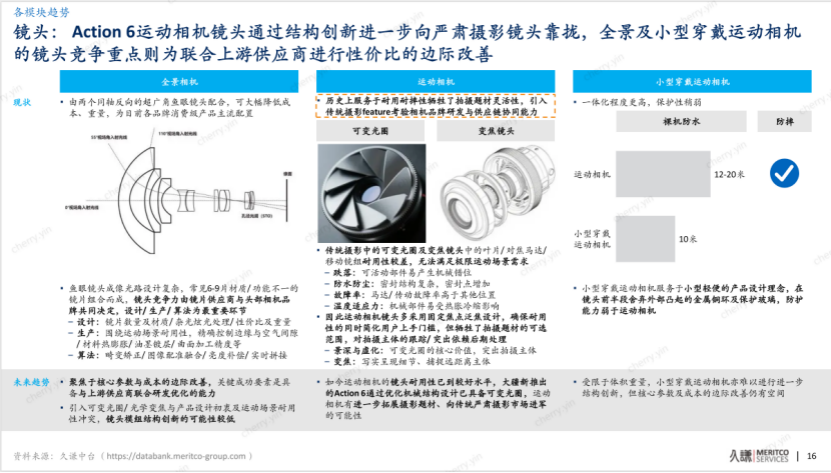

In 2025, DJI's Action 6 introduced variable aperture technology to action cameras for the first time, breaking the category (category)'s long-standing reliance on fixed apertures for durability and expanding usage scenarios from extreme recording to serious photography, directly pushing category boundaries outward.

This foundational innovation capability stemmed from DJI's decade-plus technological accumulation. Its three-axis gimbal stabilization technology, refined in drones, created the pocket gimbal camera category when adapted to handheld devices. The Pocket series, through five iterations, continuously set industry experience standards with features like 1-inch sensors, SmartFollow 7.0 algorithms, and beauty tuning.

2. All-Scenario Product Matrix: Flawless User Coverage

DJI's product strategy long transcended single-category competition, forming a complete matrix covering all handheld imaging scenarios. In the action camera segment (70% market capacity), Action 5 Pro was China's best-selling model throughout 2025, solidifying its base. In July 2025, DJI entered the panoramic camera market with Osmo 360, priced at 2,999 yuan to directly compete with Insta360 X5 (3,798 yuan), rapidly attracting early adopters and expanding the panoramic camera market to 37.1% domestic share by Q3 2025. In September, its first wearable camera, Osmo Nano, sold for just 1,698 yuan after subsidies—nearly 600 yuan cheaper than Insta360's comparable GO Ultra—and quickly became the small wearable camera market leader. Combined with the continuously iteration (iterated) Pocket series gimbal cameras (topping Japan's video camera sales charts for 20 consecutive months with 34.1% share in June 2025), DJI achieved full-scenario coverage of "handheld Vlog + sports recording + panoramic creation + wearable shooting," ensuring users found solutions for any shooting need within its ecosystem.

In contrast, Insta360's product line remained concentrated in panoramic and thumb cameras, with far lower shares in core segments like action and gimbal cameras. This product matrix weakness directly reduced its risk resistance.

3. Accessory Ecosystem Barrier: The Core Lever for User Retention

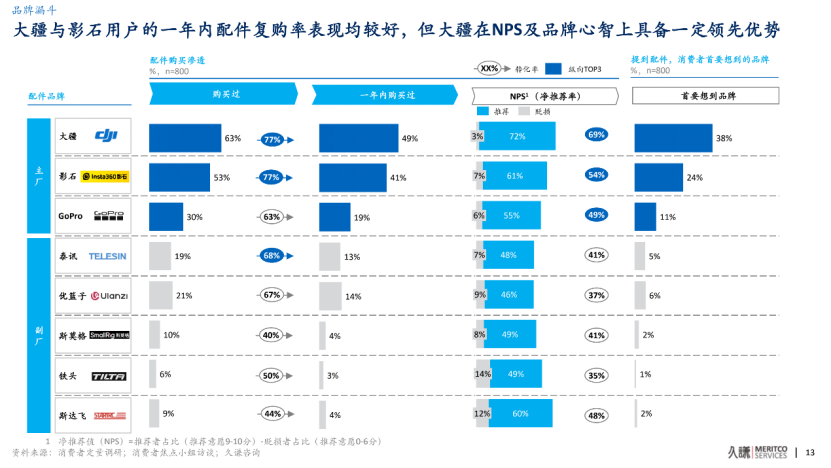

Qianzhan Consulting's 2026 accessory ecosystem report revealed DJI's another core strength: user retention through accessory ecosystems. Surveys showed 93% of handheld imaging users purchased accessories, with 17-20% choosing the same brand for future host (host device) purchases due to existing accessory systems.

DJI's accessory system was built around "efficient connectivity + continuous reuse." Magnetic quick-release designs replaced traditional screws, reducing scenario-switching time by over 70%. Contact-based linkage technology enabled power, control, and data transmission between accessories and hosts, transforming microphones and grips from standalone peripherals into host function extensions. Most critically, multi-generation compatibility allowed core accessories like extension rods and grips to work across multiple camera generations, eliminating redundant accessory costs during upgrades and significantly boosting brand loyalty during device replacements.

Qianzhan data showed DJI's accessory Net Promoter Score (NPS) reached 69%, with 38% of consumers mentioning it as their first-choice brand—both industry-leading figures. In contrast, despite Insta360's industry-leading accessory richness, its multi-product-line strategy resulted in extremely weak cross-series compatibility. Thumb camera, panoramic camera, and action camera accessories were incompatible, forcing users to abandon existing accessories when switching models.

4. Risk Resistance: The Natural Buffer for Market Leaders

Facing storage chip price hikes driven by global AI demand, Qianzhan's 2025 report noted DJI's high-price product lines, inventory buffers from high shipment volumes, and stable product launch rhythms collectively formed a moat against cost risks.

While Insta360's 2025 revenue grew over 90% year-on-year, its net profit declined due to raw material price fluctuations and strategic investment increases. DJI, leveraging scale advantages and supply chain bargaining power, maintained stable profitability. During the industry's seasonal Q1 2026 downturn, DJI's revenue share rose 5 percentage points sequentially and 9 percentage points year-on-year, while Insta360's dipped slightly by 1 percentage point. This head concentration effect intensified, further squeezing profit margins for second-tier players.

02 Insta360's Breakout Dilemma: Losing Ground in Core Segments and Ecosystem Weaknesses

1. Rapid Depletion of Founding Advantages

Insta360 initially built its global leadership in panoramic cameras, holding 91% of the global market share in H1 2025 according to Qianzhan data. However, DJI's rapid entry eroded this advantage. After DJI launched Osmo 360 in July 2025, Insta360 was forced to cut X5's price by 500 yuan and later introduced X4 Air at 2,399 yuan in response. Yet Qianzhan data showed Insta360's panoramic camera share dropped to 53% in H2 2025 while DJI's rose to 37%, confirming DJI's catch-up momentum. This trend was even more pronounced in the small wearable action camera market.

More critically, while panoramic cameras contributed minimally to DJI's overall business (merely an ecosystem supplement (supplement)), they accounted for over 60% of Insta360's revenue. DJI's price wars directly impacted Insta360's core profit source.

2. Uncertainty of the Second Growth Curve

Facing DJI's all-out offensive, Insta360 chose a highly challenging path—entering the drone market. In July 2025, it announced its first drone, the "Antigravity A1." The strategic intent was clear: sustain high valuations through a "second growth curve" while constraining DJI in its core market.

However, the challenges were immense. DJI held over 70% of the consumer drone market share, with the world's most complete drone patent portfolio and maturest supply chain. More notably, DJI began striking back—on March 26, 2026, it officially launched the DJI Avata 360, its first 8K panoramic flagship drone. If Insta360's Antigravity A1 was a pioneer in the "panoramic drone" category, DJI's Avata 360 represented a classic "top student's dimensional reduction strike."

As the drone industry's overlord (hegemon) for two decades, DJI didn't build a "new wheel" from scratch but directly integrated mature technology stacks into a panoramic camera. Once DJI completes vertical integration in drones, Insta360's "second curve" risks being blocked outright.

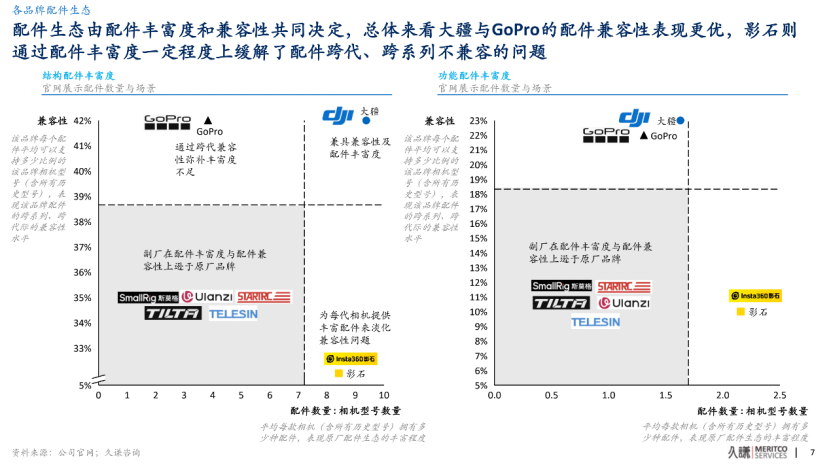

3. Long-Term Risks from Accessory Ecosystem Weaknesses

Insta360's accessory system featured high richness but low compatibility. With multiple product lines like thumb and panoramic cameras, it needed highly segmented accessories for different hosts, resulting in greater accessory variety. However, this came at the cost of weak cross-series compatibility.

Qianzhan Consulting's research noted that accessory compatibility issues primarily arose from cross-series adaptation rather than within-series upgrades. For example, adapting action camera accessories to small wearable cameras often faced limitations from body size, port location, and mounting method differences. Insta360's strategy essentially used "richer scenario-specific accessory offerings" to partially compensate for cross-series adaptation difficulties, but this increased user switching costs over time—original accessories often became unusable when upgrading hosts.

Insta360's "hardware-software integration" accessory strategy essentially used scenario-based solutions to compensate (compensate for) hardware compatibility gaps. However, this "high richness, low compatibility" approach faced significant retention risks during user upgrade cycles.

03 Final Projection: Industry Oligopolization

The handheld smart imaging industry stands at a critical crossroads. Market growth potential remains vast, but the competitive landscape is rapidly polarizing, with resources and users concentrating toward leading brands.

DJI, driven by its dual-wheel model of "hardcore technology + ecosystem closure," is constructing a nearly insurmountable competitive barrier. Its supply-side structural innovations, multi-generation accessory compatibility and locking effects, full-category scale advantages, and strategic deterrence through patents and supply chain control have put Insta360 at multiple disadvantages.

While Insta360 maintains an unshakable position in panoramic cameras, its "revenue growth without profit growth" financial pressure, accessory system compatibility weaknesses, and high-risk drone market entry strategy are accumulating systemic risks. In the foreseeable future, unless it finds sufficient differentiated competition space and significantly improves profitability, Insta360 will struggle to avoid shrinking market share and widening gaps with DJI.

As technological innovation shifts from "feature stacking" to "foundational restructuring," and competition extends from "single-product battles" to "ecosystem duels," only enterprises truly controlling technological discourse and ecosystem dominance will ultimately prevail in this transformation.

- END -

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle