Insta360's Revenue Growth Without Profit Increase: Why 'Doing Everything' Became the Biggest Strategic Trap?

05/29 2026

05/29 2026

618

618

Insta360 (688775) delivered a "contradictory" report card in 2025.

Full-year revenue reached RMB 9.741 billion, up 74.76% year-on-year, nearly doubling; R&D investment hit RMB 1.53 billion, nearly doubling year-on-year, exceeding the combined total of the previous three years. However, net profit attributable to the parent company fell to RMB 929 million, down 6.62% year-on-year. By the first quarter of 2026, this contradiction intensified: revenue reached RMB 2.481 billion, up 83.11% year-on-year, but net profit attributable to the parent company plummeted to just RMB 84.62 million, down 52.02% year-on-year; core net profit excluding non-recurring items dropped by 61.27%.

Revenue growth far outpaced profit growth, establishing a trend of 'selling more but earning less.'

This report card raises a core question: When a company's revenue surges at double the pace while profits shrink at an accelerating rate, how much 'quality' remains in its growth? The answer lies in Insta360's category expansion strategy pursued in recent years.

I. From Panoramic Cameras to a Limited Ceiling

Insta360's story began as a classic niche market player.

Defined by its role as a market creator, the company was founded in 2015 and rose to prominence with panoramic cameras, once becoming synonymous with the category.

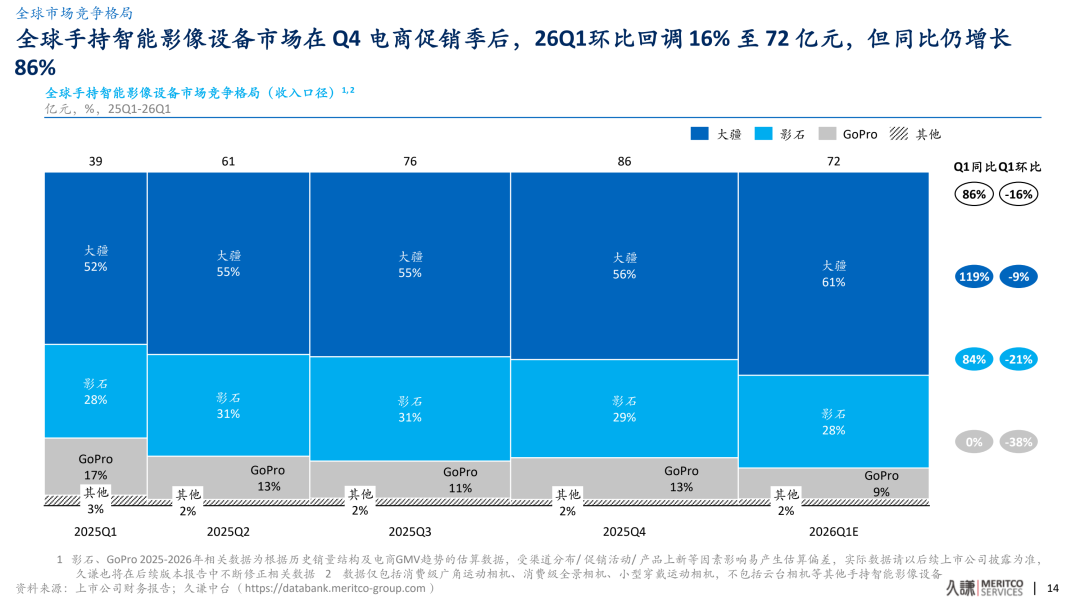

However, the size of the panoramic camera market itself imposes a natural limit on growth. Data shows that the global market for handheld smart imaging devices was worth approximately RMB 36.5 billion in 2023, offering limited expansion potential compared to trillion-dollar markets like smartphones. More critically, according to a May 2026 industry research report by Jiuqian, top brands already occupy 61% of the overall handheld smart imaging device market, with Insta360 maintaining its second-place position. The continuously improve (continuously rising) industry concentration means shrinking space for latecomers.

Driven by a desire for larger markets, Insta360 embarked on a multi-year category expansion journey. Since launching action cameras in 2019, its product lineup has broadened annually: thumb cameras (officially launched in 2023), gimbal cameras, wireless lavalier microphones, and drones and AI hardware collaborations under development. Founder Liu Jingkang's vision of a 'photography robot' in his shareholder letter elevates this expansion logic to a higher narrative level.

Here lies a critical strategic question: Category expansion itself is not the issue; the problem lies in whether the direction, pace, and resource allocation of expansion align with the company's inherent capabilities.

II. The First Cost of Multi-Front Warfare: The Income Statement Speaks

The most direct signal comes from the structural dispersion of R&D investment.

In 2025, Insta360 invested RMB 1.53 billion in R&D, up 96.95% year-on-year; in the first quarter of 2026, it invested another RMB 465 million, up 101% year-on-year. Viewed in isolation, this shows a company willing to spend on technology. However, when these investments are spread across at least seven or eight directions—panoramic cameras, action cameras, thumb cameras, gimbal cameras, drones, lavalier microphones, AI chips, and photography robots—the actual R&D intensity per category warrants re-examination.

A simple estimate: Distributing RMB 1.53 billion in total R&D across seven or eight product lines averages less than RMB 200 million per line. For comparison, GoPro's 2025 R&D expenses were approximately $85 million (about RMB 600 million), all concentrated in action cameras. In terms of R&D density per category, Insta360's investment per line falls far short of focused competitors. More notably, a significant portion of Insta360's R&D spending flows into frontier areas like AI chips and embodied intelligence, which remain in the investment phase without clear commercialization paths—these 'future investments' continuously consume current profits, with no timeline provided in annual reports for when they will translate into revenue.

R&D investment follows a 'critical mass' concept: Below a certain threshold in a technical direction, breakthrough outputs are difficult to achieve; only above the threshold can qualitative changes occur. Distributing RMB 1.53 billion in total R&D across seven or eight lines, averaging less than RMB 200 million per line—in fields like imaging chips and AI algorithms requiring sustained high-intensity investment—raises questions about whether this level of dispersed investment can support long-term technological competitiveness against single-category deep cultivator (deep divers). From a patent structure perspective, Insta360's 2025 annual report shows 1,120 total patents, with only 261 invention patents and 859 utility model and design patents combined (about 76.7%). Utility model and design patents have far lower technical barriers than invention patents—the gap between 'many patents' and 'strong core technology' indirectly evidences diluted R&D resources from multi-front operations.

The deterioration of the income statement is more intuitive (intuitive). In 2025, Insta360's overall gross margin fell to 45.7%, down 6.5 percentage points year-on-year, with consumer-grade smart imaging devices at just 45%, down 7 percentage points. The annual report attributed the margin decline to rising storage component prices and intensified market competition. Correspondingly, facing price competition, Insta360 reduced the price of its flagship X5 product by several hundred yuan—volume growth through price cuts boosted revenue but further eroded profit margins.

Price-for-volume trading itself is not the issue—many tech companies follow this path during expansion. The problem lies in Insta360's overly extended product lineup, where the loss of pricing power is not isolated to a single category but systemic. Panoramic cameras need price cuts to defend market share, action cameras need low pricing to gain market entry, and thumb cameras rely on cost-effectiveness against smartphone imaging—the trend of 'selling more but earning less' occurs not just in one product line but across all three main categories. This means Insta360 has hardly any (hardly any) product line capable of 'raising prices against the trend,' a concerning signal for a consumer goods company.

The scissors gap (scissors gap) of over 80 percentage points between revenue growth (75%) and profit growth (-6.6%) reveals a simple logic: When growth relies more on price cuts and category expansion than product premiums and efficiency gains, profit quality declines as scale expands.

III. The Second Cost: From 'First Mover' to 'Latecomer'

Category expansion has positioned Insta360 as a vastly different competitor under the same brand.

In panoramic cameras, Insta360 is the first mover. But in action cameras, thumb cameras, and other new categories, it has become a latecomer—and latecomers face a core dilemma: requiring higher R&D and marketing costs to pry market share from established players, with returns not necessarily proportional.

How 'expensive' is this dilemma? In 2025, Insta360's selling expenses reached RMB 1.679 billion, up 103.31% year-on-year, with the selling expense ratio rising from about 14.8% in 2024 to 17.23%. This RMB 1.679 billion in selling expenses was not spent on panoramic cameras—a 'defensive' category already synonymous with the brand, not requiring massive market education—but on persuading consumers that 'action cameras don't have to be GoPro' and 'thumb cameras are better than smartphones for Vlogs.' Latecomers inherently face higher customer acquisition costs: new categories lack user mindshare, so every market share gain must be 'purchased' with marketing investment. When selling expense growth (103.31%) far outpaces gross profit growth, the marginal return per additional unit sold may turn negative—this is not growth but burning money for scale.

The relationship between thumb cameras and smartphone cameras is not competitive but overlapping. Over the past five years, flagship smartphones have achieved qualitative leaps in imaging systems: multi-camera setups, computational photography, and AI algorithms have pushed daily shooting quality and convenience to extremely high levels. When smartphones can already produce cinematic portrait modes and 4K HDR videos, why would consumers spend hundreds or thousands more on a thumb camera with a single function and Not necessarily stronger (not necessarily better) image quality?

In contrast, action cameras have irreplaceable value due to rigid demands like extreme waterproofing, stabilization, and durability. However, the 'portable recording' positioning of thumb cameras heavily overlaps with smartphones' core usage scenarios. Insta360's 2025 GO Ultra, equipped with a 5nm AI chip and supporting 4K lossless zoom, attempts to differentiate through image quality and AI features. But AI imaging is precisely where smartphone makers invest most heavily—Apple, Huawei, and Samsung's AI photography algorithm iteration speeds are unmatched by a camera company.

When a category's core selling point is 'slightly more portable than a smartphone,' its moat is destined to be shallow. If category expansion targets battlefields being covered by mainstream technological trends, no amount of product design can alter the fate of obsolescence.

IV. The Third Cost: Continuous Dilution of Brand Perception

Another hidden cost of category expansion is the blurring of brand perception—a cost not directly reflected in financial statements short-term but potentially the most far-reaching long-term impact. The essence of a brand is to 'reduce consumers' choice costs': you don't need to compare specs because you know GoPro means action cameras and Sony means mirrorless cameras. When Insta360 spreads its product lineup across seven or eight directions, every new product launch dilutes the answer to 'What does Insta360 stand for?' This is not brand extension—brand extension requires a solidified core category first. Without a second category establishing equally unshakable cognitive barriers, each additional product line does not 'expand brand boundaries' but 'disperses brand equity.'

What does Insta360 represent in consumers' minds? For early users, it was synonymous with 'panoramic cameras.' But today, it is simultaneously an action camera brand, thumb camera brand, gimbal camera brand, and soon a drone brand and microphone brand. A classic warning in positioning theory states: When a brand does everything, it may represent nothing.

In contrast, although GoPro's revenue has contracted to about $652 million and camera shipments to about 2 million units in recent years, the mental anchor of 'action cameras = GoPro' remains clear—a consequence of this single-category strong association is that even during scale contraction, GoPro's 2025 gross margin remained above 33%. While lower than Insta360's consumer-grade product margin (45%), considering GoPro's revenue scale is just a fraction of Insta360's consumer business, its per-unit brand premium has not collapsed due to scale shrinkage. What about Insta360? A 'fun panoramic camera'? A 'small thing you can stick on yourself for Vlogs'? A 'cheap alternative'? The dispersion of user perceptions most directly results in the brand losing pricing power—when consumers cannot articulate what your brand stands for, their purchasing decisions devolve into pure spec comparisons and price shopping. And in the race to the bottom on specs, there will always be cheaper latecomers.

V. Greater Risk: All-Around Offensives Trigger Omnidirectional Competition

Another consequence of category expansion is that the more fields Insta360 enters, the more diverse and formidable its competitors become.

This is not simply a problem of 'intensified competition.' The key issue is that Insta360's chosen categories happen to be strategic highlands for smartphone makers. Gimbal cameras, AI imaging, and portable shooting—these categories are highly homologous with smartphone imaging technologies. Smartphone makers entering these fields do not start from zero: imaging algorithms transfer directly from smartphone product lines, supply chains leverage the bargaining power of mobile systems, and channels reuse tens of thousands of offline stores and proprietary e-commerce platforms. Insta360 faces not just 'a few more rivals' but competitors with structural advantages in technological reserves, supply chain efficiency, and channel coverage—and these competitors' marginal costs for entering new categories are far lower than Insta360's.

The entry paths of smartphone makers warrant caution. According to industry media reports, OPPO, vivo, and Honor have sequentially launched gimbal camera products, entering categories Insta360 has targeted. But the real concern is not these products themselves—smartphone makers' gimbal cameras remain small in volume—but the underlying logic: smartphone brands are upgrading imaging capabilities from 'mobile phone auxiliary function (ancillary functions)' to 'independent hardware categories.' Huawei and Xiaomi have already entered action cameras and smart cameras, while Apple's Vision Pro and spatial video strategy are redefining the boundaries of 'shooting.' When smartphone makers operate imaging hardware as independent categories, their ecosystem barriers—account systems, cloud storage, device interconnection—built on hundreds of millions of users are difficult for single-category companies to counter. Insta360 must compete not just on products but on ecosystem stickiness with these players.

The greater risk is that rivals are not only competing in Insta360's new battlefields but also pressuring its core stronghold. According to a May 2026 industry research report by Jiuqian, top brands already occupy 61% of the overall handheld smart imaging device market, with Insta360 maintaining second place. Panoramic cameras—Insta360's founding category and global market leader with 67.2% share—are facing unprecedented competitive intensity. History provides a clear reference: GoPro once held over 80% global market share in action cameras in 2014, but when competitors entered with equivalent performance and lower prices, its share plummeted within five years. Insta360's 67.2% panoramic camera share seems secure, but if 'defending panoramic cameras' requires continuous price cuts and 'expanding new categories' requires sustained burning of cash, with both lines simultaneously draining cash flow, how long can the financials hold?

Insta360's current predicament can be summarized as: Profit margins are shrinking in old battlefields, investments are escalating in new ones, financial conditions are deteriorating in both directions, and time is on the side of rivals.

Conclusion: The Window for Strategic Choices May Be Tighter Than Imagined

Insta360's growth anxiety is real and reasonable. Panoramic cameras, while strong, operate in a limited niche market; action cameras and thumb cameras, while larger, face competitive landscapes and category risks that cannot be ignored; AI hardware and drones represent even greater resource commitments and stronger rivals.

However, the solution may lie not in 'doing more' but in 'doing deeper.' A company with nearly RMB 10 billion in revenue, simultaneously managing seven or eight product lines, three self-developed chips, AI large models, and embodied intelligence collaborations, while profits are accelerating their decline—with net profit attributable to the parent company plummeting to just RMB 84.62 million in the first quarter of 2026, less than one-tenth of 2025's full-year RMB 929 million—raises legitimate market questions: On each specific battlefield, does Insta360 possess the resource reserves to engage in long-term warfare with rivals several times its size? If this trend of 'revenue growth without profit increase' continues, can Insta360's cash flow sustain until any of its multiple product lines achieves a profitable breakthrough?

From 'doing everything' to 'excelling in everything,' what lies in between is not just time and investment, but a difficult decision regarding strategic trade-offs. The growth rate of sales expenses (103.31%) is nearly 30% higher than that of revenue growth (74.76%). When the net profit attributable to the parent company in the first quarter is less than 85 million while R&D and sales are still aggressively increasing, the time window for Insta360 to make a choice may be shorter than market expectations. After all, there can be multiple paths to growth—but only one path to profit: products that are truly recognized by consumers and for which they are willing to pay a premium.

Disclaimer: This article is based on the company's legally disclosed content and publicly available information for commentary, but the author does not guarantee the completeness or timeliness of this information.

Note: The stock market involves risks; enter with caution. This article does not constitute investment advice. Investors must make their own judgments regarding whether to invest.

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle