"Backup Chip" Powers On: Huawei Phones Anticipated to See Further Price Cuts

05/29 2026

05/29 2026

558

558

Source | YuanSight

Over the past few decades of semiconductor industry development, Moore's Law has been the cornerstone of technological advancement. By continuously reducing the geometric dimensions of transistors, chip performance has been consistently enhanced, and the cost per unit of computing power has gradually decreased. This has underpinned decades of iterative upgrades in end-user products such as smartphones and consumer electronics.

However, as the industry progresses into the advanced process node phase, challenges such as physical limitations, escalating complexity in photolithography processes, and rising manufacturing costs have begun to surface. The deceleration and impending plateau of Moore's Law have emerged as a common hurdle for the global semiconductor industry.

Faced with this industry bottleneck, leading global companies have embarked on diverse development paths.

On May 25, at the 2026 International Circuit Systems Symposium, He Tingbo, a board member of Huawei and President of its Semiconductor Business Department, introduced "Tao's (τ) Law." He stated that Huawei's "logical folding" technology has propelled semiconductor development forward, adhering to Tao's Law.

Simultaneously, He Tingbo disclosed that the Kirin smartphone chip, set to make its debut this autumn, will be the first to incorporate logical folding technology. By 2031, semiconductors designed in accordance with Tao's Law are projected to achieve processing capabilities equivalent to 1.4nm.

Notably, 1.4nm represents the next frontier in semiconductor technology, which giants like TSMC and Samsung Electronics are striving to mass-produce. This logical reconfiguration holds the potential to enable China's semiconductor industry to seize opportunities to surpass competitors through alternative routes.

01 Surpassing Through Alternative Routes

Seven years ago, amidst shifts in the international landscape, Huawei found itself in a predicament with "no chips available," disrupting its high-end flagship models. At that juncture, HiSilicon, which Huawei had considered a "backup chip," was elevated to primary status, and the development of the HarmonyOS system was expedited. Subsequently, under external constraints, Huawei embarked on self-developed innovation to address its shortcomings.

In recent years, the smartphone industry's chip technology has neared the limits of process node advancements, making it challenging to significantly enhance performance solely through DUV multiple exposure. Concurrently, the demand for smartphones in areas like AI continues to surge. Moreover, with restrictions on EUV lithography, architectural innovation has become Huawei's strategy to "surpass through alternative routes" in its chip business.

Under this trend, Huawei has integrated three-dimensional stacking and logical folding technologies into its smartphone main chips, overcoming the current technological impasses faced by the domestic chip industry.

Data reveals that, based on Tao's Law, Huawei has mass-produced 381 chip models over the past six years, spanning communications, AI, and automotive sectors.

For China's semiconductor industry, the significance of Tao's Law lies in its innovative resolution to the bottleneck in chip competition.

According to reports from the Economic Information Daily, citing industry insiders, Tao's (τ) Law is poised to significantly bolster confidence in the domestic chip industry and foster the development of the entire industrial chain. In the short term, it will directly stimulate the growth of domestic semiconductor materials, manufacturing, packaging, and testing companies upstream and downstream. In the long term, it offers a new viable path for domestic chip design companies to circumvent risks associated with advanced process restrictions and break through technological barriers.

However, whether this new technological path can become mainstream remains to be validated by the industrial chain and the market over the long haul.

The aforementioned industry insider noted that this new evolutionary path still confronts numerous challenges. This technological system hinges on Huawei's sustained high-intensity R&D investment and technological accumulation, making it difficult for most industry players to swiftly replicate. The journey towards a new upgrade in the semiconductor industry is arduous.

02 Reducing Smartphone Costs

Specifically for the smartphone business, smartphones are highly integrated consumer electronics products, with chips serving as their core control components and constituting a substantial portion of the overall material costs. For instance, in high-end flagship models, the cost of the main chip typically accounts for 25% to 35% of the total BOM cost.

In essence, fluctuations in chip costs directly impact the total hardware cost of the entire device, thereby influencing product pricing strategies.

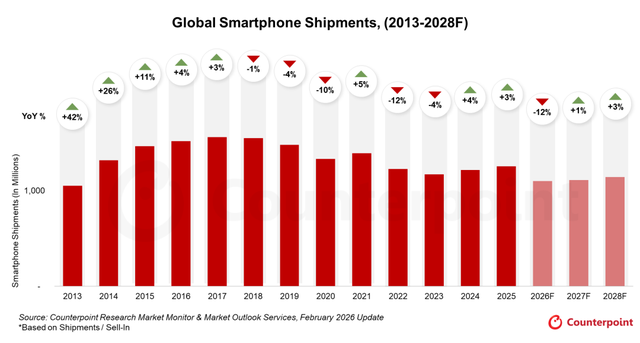

From last year to the present, the global smartphone industry has grappled with immense cost pressures. Data from Counterpoint Research indicates that in the second quarter of 2026, the price of mobile-grade LPDDR4/5 will soar to nearly three times the level of the third quarter of 2025. The scarcity of memory chips, rapid inflation in component prices, and the structural fragility of low-end OEM manufacturers will not only depress data for 2026 but also prolong the downturn into 2027.

Counterpoint Research anticipates a significant downturn in the smartphone market in 2026, with shipments projected to decline by 12.4% year-on-year.

Image Source: Counterpoint Research

Furthermore, as product homogenization intensifies, smartphone manufacturers' relentless pursuit of refining configurations such as imaging and battery life has also driven up production costs.

Against this backdrop, breakthroughs in chip technology have become paramount.

In the current market, high-end smartphones equipped with 3nm and 4nm advanced process flagship chips generally incur high procurement costs for their main chips. When combined with supporting hardware such as large batteries, liquid cooling systems, high-specification screens, and high-end imaging modules, the total material cost of the entire device remains elevated.

This hardware cost compels smartphone manufacturers to position their products solely in the high-price range, with high-end smartphones maintaining a premium for an extended period.

With the implementation of Huawei's three-dimensional stacked chips, the procurement cost of its smartphone main chips is expected to decrease. Coupled with cost reductions in batteries and thermal management components due to power optimization, the overall material cost of a flagship smartphone can be reduced to a certain extent.

After the hardware cost decreases, manufacturers gain greater flexibility. They can either opt to maintain the original price and increase per-unit profit or lower the terminal price and enhance product cost-effectiveness to capture market share.

03 A New Landscape for Smartphones

In March of this year, Huawei Terminal CEO He Gang officially announced the full resurgence of the company's smartphone business, which is also attributed to its continuous breakthroughs in semiconductor technology and autonomous control over production capacity.

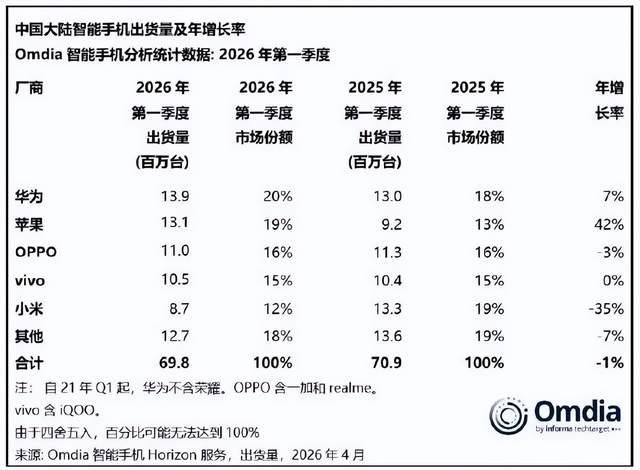

According to data from Omdia, Huawei led the Chinese smartphone market in the first quarter of 2026 with 13.9 million shipments and a 20% market share.

Image Source: Omdia

In the smartphone sector, in terms of global market share and shipments, Huawei ranked second in the industry in 2019 and third in 2020. However, this ranking slipped below sixth after 2021.

Additionally, Omdia's data reveals that Huawei's global market share for tablets was 7% in 2025, indicating a trend of continuous recovery.

According to media reports, Huawei's overseas operating revenue reached approximately 248.7 billion yuan in 2025, marking a 9% year-on-year increase and recovering to about 70% of its historical peak.

Currently, the significance of semiconductor technology breakthroughs for Huawei's smartphone business is multifaceted.

On the product front, the Kirin chip will propel the performance of Huawei's Mate and P series flagships to rival Apple's A series and Snapdragon products. If logical folding technology is extended to mid-range and low-end models, the experience of related products is also expected to improve.

On the market front, as Huawei's technological barriers heighten, this differentiated competitiveness can also drive Huawei to challenge Apple and Samsung's dominance in the high-end market.

From the latter half of last year to the present, Huawei has successively adjusted the pricing of multiple smartphone products. At the end of last year, it announced price reductions for the Mate 80 series, with the starting price of the standard version lowered by 800 yuan and the Pro version by 500 yuan. The Huawei Pura 90 series, released in April this year, maintained the same pricing for the standard version as the previous generation, while the 12GB+256GB and 12GB+512GB versions of the Pro version were reduced by 1000 yuan compared to the previous generation.

The ability to drive product price reductions amidst current cost pressures stems from Huawei's relentless efforts in recent years to promote the self-development of smartphone operating systems and chip technologies. Simultaneously, its high-end models constitute a significant proportion, providing ample room to absorb cost increases from upstream suppliers.

From technological breakthroughs to market resurgence and flexible pricing adjustments, Huawei continues to chart its path to recovery. With the support of semiconductor and terminal technology autonomy, the smartphone industry landscape may also witness new transformations.

Some images are sourced from the internet. Please inform us for removal if there is any infringement.

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle