New 13-Year Low! Global Smartphone Shipments to Plunge 13.9% by 2026: Huawei Bucks the Trend with Growth

06/02 2026

06/02 2026

554

554

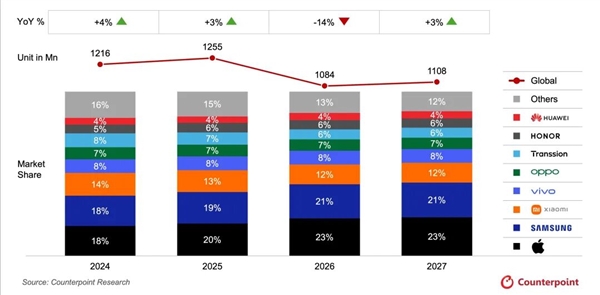

Kuaikeji, June 2: According to Counterpoint's latest May report, global smartphone shipments are forecast to drop sharply by 13.9% year-on-year in 2026, falling to approximately 1.08 billion units—marking a new annual low since 2013. The decline has widened from the 12.4% forecast in February.

The primary driver of this downturn is tight memory supply, as foundries shift wafer capacity to AI-related HBM and server DRAM, causing severe shortages in mobile memory.

LPDDR4/5 prices are expected to roughly triple in Q2 2026 compared to Q4 2025, with LPDDR4 supply shrinking by over 40%. Supply constraints may persist until the second half of 2027.

In terms of pricing, wholesale smartphone prices rose 14% year-on-year in Q1 2026 and are expected to continue climbing.

The entry-level market (below $150) faces the greatest pressure, with some regions effectively exiting this segment. Low-end OEMs and emerging markets are particularly hard hit.

Brand performance is sharply divided: Apple and Samsung are less affected, with Samsung projected to decline only 4% annually.

Huawei is the only Chinese brand expected to see shipment growth.

Xiaomi is projected to decline 28% annually, while Transsion is expected to drop 32%—among the steepest declines among leading vendors.

The report notes that market shifts will accelerate industry consolidation, benefiting the secondhand and refurbished phone markets, which are expected to grow 13% in 2026.

With supply recovery, demand release, and advancements in 6G and AI-native devices, the market is poised for a rebound by 2028.

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle