Zhao Ming Departs, IPO Postponed, AI Phones Underperform—Can Honor Still Live Up to Its Name?

06/08 2026

06/08 2026

645

645

Summary: Huawei's Comeback, Valuation Decline, IPO Delay—Honor Faces an 'Alternative' Predicament

Recent data from Omdia indicates that Honor achieved remarkable results in overseas markets during the first quarter.

According to reports, Honor's shipments in the Middle East soared by 73% year-on-year in Q1, with its market ranking climbing to second place. In Latin America, shipments increased by 30%, securing the fourth position, while Southeast Asia witnessed a 28% year-on-year growth, with Singapore's premium market share breaking into the top three for the first time.

While Honor is making significant strides overseas, its journey towards a capital market listing has hit a snag.

As per Jiemian News, Honor failed to complete its IPO within a year of its share reform, prompting an internal employee shareholding meeting. This meeting provided a channel for employees to reduce their stakes and exit. Despite top executives asserting that 'Honor's IPO has not been terminated,' no specific timeline for listing was provided.

More than five years have elapsed since Honor's independence from Huawei, yet it has yet to make its debut on the stock market. The 'smile curve' it once enjoyed, riding on Huawei's coattails, has now transformed into a downward slope, with shipments declining for three consecutive years.

Under Li Jian's leadership, Honor bet on an AI terminal ecosystem, introducing concepts like Robot Phones and humanoid robots. However, the Magic8 series saw sluggish sales, with mid-to-low-end models accounting for over 60%, signaling a crumbling foundation in the smartphone market.

As the 'alternative dividend' fades and the AI narrative remains elusive, can Honor chart a new course for itself?

I. Declining Smartphone Business: Blame Huawei or Self-Inflicted Wounds?

In late 2020, following Huawei's sanctions, Honor was acquired and became independent through the efforts of over 30 channel partners and distributors.

In this seemingly 'lifesaving' spin-off, Honor inherited a valuable legacy: Huawei's DNA.

CEO Zhao Ming is a seasoned Huawei veteran; the core R&D team carries forward Huawei's system; product designs such as the Magic series compete with Huawei's Mate, while the number series rivals nova.

For consumers, Honor was almost synonymous with 'Huawei in a different package.'

Leveraging the 'alternative dividend' from Huawei's temporary market absence, Honor sidestepped the 'premiumization dilemma' faced by Xiaomi, OPPO, and vivo, effortlessly entering the premium market with rapid performance growth.

Official data reveals that in Q1 2021, Honor's market share in China was a mere 3%. However, IDC data shows that from 2021 to 2022, Honor's market share surged to 11.7% and 18.1%, respectively, marking a remarkable rebound.

Yet, success stemmed from Huawei, and so did failure. The borrowed momentum eventually had to wane.

In August 2023, Huawei's Mate 60 series made a comeback, reintroducing the Kirin chip. With the true protagonist back, the narrative space for alternatives was severely compressed.

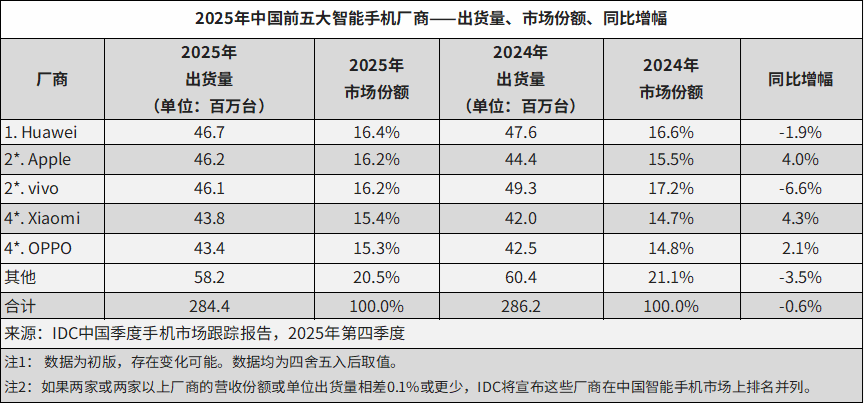

IDC data indicates that from 2023 to 2024, Honor's shipments in China fell by 10.3% and 8.1% year-on-year, ranking second and fourth, respectively. By 2025, Honor had even slipped out of the TOP 5 list.

(Source: IDC)

Counterpoint provides even more sobering figures: In 2025, Honor's domestic market share was just 13.4%, a 12.6% year-on-year drop, making it the only mainstream brand with a double-digit decline.

Huawei's return is undoubtedly the biggest external variable, but not all of Honor's problems can be attributed to 'Huawei being too strong'—that would be oversimplifying the issue. Let's delve into Honor's internal challenges.

Firstly, Honor has failed to establish independent brand recognition.

'Huawei fans' are loyal to the brand, while 'Xiaomi fans' are drawn to the ecosystem and cost-effectiveness. Consumers naturally perceive Honor as a 'downgraded Huawei,' leaving Honor users without a compelling reason to stay loyal.

Huawei, Xiaomi, OPPO, and vivo all emerged victorious from the fiercely competitive smartphone industry. Before independence, Honor was Huawei's internet-focused sub-brand, used to counter Xiaomi. Under Zhao Ming's leadership, it once pushed Lei Jun to declare 'life and death are irrelevant; if you disagree, just fight' at a product launch.

However, nearly six years after independence, Honor has yet to break free from the perception of being 'Huawei's sibling.' This is not a product issue but a strategic failure in brand building, requiring sustained marketing and PR efforts.

Secondly, Honor's product mix is unbalanced.

According to 'RD Observation' data, in 2025, products priced under 2,000 yuan accounted for 61.8% of Honor's smartphone sales. By the 20th week of 2026, the Magic8 series had sold only 1.1707 million units, far below Huawei's Mate 80 series at 6.0935 million units and ranking last among flagship models from the six major brands.

(Source: Weibo)

While 'RD Observation's data may vary due to different statistical methods, it provides a rough snapshot of Honor's product mix.

Honor's current brand premium is weak.

After independence, Honor's smartphone chips came from MediaTek and Qualcomm Snapdragon, while its system was MagicOS based on Android, leading to homogeneous competition with Xiaomi, OPPO, and vivo. With Huawei's premium flagships returning, controversies arose over Honor's 'high price, low specs,' delaying its premiumization efforts.

Thirdly, Honor's channel-dominated shareholder structure cannot support long-term vision.

Honor's independence was essentially a collective rescue by channel partners.

Initially, over 30 channel partners and distributors stood behind Honor's acquirers. By the end of 2024, Honor completed its joint-stock reform. According to Tianyancha APP, Honor Group still has 25 investors, including Shenzhen State-Owned Assets, China Mobile, China Telecom, BOE, and dozens of channel partners.

(Source: Tianyancha)

Channel partners naturally prioritize rapid turnover and profit maximization. They care about 'how much profit this phone generates,' not 'how much this brand will be worth in five years.'

However, the benefit of aligning with channel partners was that Honor could quickly expand offline stores using their resources in its early independence phase and push channel partners to stock more products to inflate sales, similar to the 'inventory backlog' in the liquor industry.

But with Huawei's return, higher premium capabilities, and declining Honor smartphone sales, the returns for channel partners have diminished, forcing them to bear inventory pressure from Honor, making 'defection' inevitable.

Thus, blaming Huawei for Honor's predicament seems more like self-consolation. Honor's dilemma is 30% timing (Huawei's return) and 70% human factors (hollow branding, low-end product mix, strategic indecision).

II. IPO 'Delayed'—Can the AI Narrative Gain Traction?

In terms of valuation, Honor has shrunk from around $40 billion (260 billion yuan) at independence to 170 billion yuan as assessed by Hurun Research Institute, a 34.62% drop in less than five years.

Behind this decline lies shared anxiety among multi-tier shareholders: Shenzhen State-Owned Assets, over 30 distributors, China Mobile, China Telecom, BOE... Every investor desires returns, yet Honor's performance increasingly lacks confidence.

The leadership change reflects this anxiety.

In November 2023, Wu Hui, backed by Shenzhen State-Owned Assets, became chairman, with the primary task of pushing for a listing. In January 2025, Zhao Ming stepped down as CEO, replaced by former Huawei executive Li Jian.

Zhao Ming was undoubtedly Honor's 'soul figure.' During his leadership, Honor had already attempted to address challenges from Huawei's return.

In product strategy, the number series targeted the female market; the GT series was defined as 'young people's first gaming phone'; the Magic series focused on AI.

At the Magic 7 launch, the 'YoYo Smart Agent' achieved 'one-sentence automatic task execution,' and Honor treated 2,000 attendees to coffee. AI phones predated Doubao phones, and 'treating to coffee' predated Qianwen.

Arguably, Zhao Ming laid the foundation for Honor's AI phones.

After Li Jian's arrival, AI became part of a larger 'ecosystem' play.

At MWC 2025 in March 2025, Li Jian announced the 'Alpha Strategy,' declaring Honor's transition from a smartphone maker to a global leading AI terminal ecosystem company, with plans to invest $10 billion over five years in three phases: building smartphones, constructing a smart ecosystem, and co-creating a smart world.

A year later, at MWC, Honor went further, proposing the Augmented Human Intelligence concept and showcasing phase achievements like the Robot Phone and embodied AI humanoid robots.

From an imagination standpoint, the embodied AI track is indeed enticing. Data from 36Kr Research shows that from 2018 to 2025, China's embodied AI market grew from 213.3 billion yuan to 915 billion yuan, with a CAGR of 23.27%, expected to reach 1.32 trillion yuan by 2027.

Capital markets are generous with imagination for such narratives, providing storytelling material for Honor's IPO.

At the product level, the Robot Phone features a micro 4DoF gimbal system, capable of 180-degree tracking and performing actions like 'nodding' or 'backflips' via voice commands. Honor CEO Li Jian stated, 'A phone shouldn't just be a boring black block with a touchscreen.'

The embodied AI product 'Lightning' won first place in the 2026 Beijing Yizhuang Humanoid Robot Half Marathon on April 19, 2026, breaking the human half-marathon world record with a time of 50 minutes and 26 seconds.

However, the $10 billion R&D investment, compared to the current $23.5 billion (170 billion yuan) valuation, will inevitably drag down Honor's financial performance.

The capital market's high valuation of Honor still depends on tangible results from its AI ecosystem.

Yet, Honor's AI narrative faces an awkward reality—a lack of transitional products.

The Magic 7 and Magic 8 series, as AI flagships, have performed poorly in the market.

As mentioned earlier, the Magic8 series sold only 1.1707 million units, far below Huawei's Mate 80 series and Xiaomi's number series during the same period. This indicates that consumers are not yet buying into the 'AI phone' concept.

Most of Honor's sales come from models under 2,000 yuan, whose users are highly insensitive to AI features and lack motivation to upgrade.

This relates to the current lack of 'intelligence' in AI phones.

As a smartphone maker, Honor must not only ensure user experience but also consider developer rights.

The Magic 8 did not rely on crude simulated clicking like 'Doubao phones' but used a system-level MCP architecture for 'one-sentence automatic task execution.' However, not all third-party developers are motivated to adapt to the MCP interface.

Thus, current AI phones cannot smoothly achieve 'one-sentence automatic task execution,' with efficiency often lower than manual operation.

As for the Robot Phone, while impressive, its commercial prospects are questionable.

Multiple industry insiders point out significant doubts about its durability and repair costs.

Fitting a 4DoF gimbal system into a phone's limited internal space will inevitably raise motherboard integration and battery design costs. The extending 'head' design and precision transmission shaft face risks of drops or impacts, with mechanical failures likely requiring disassembly at the level of scrapping the entire device for repairs.

More critically, the Robot Phone's main selling point—autonomous filming—is not a market necessity.

Professional creators already rely on dedicated gimbals and charging equipment for mature workflows, while average users prioritize portability and grip. The product may end up in a dilemma of 'being insufficient for professionals and too bulky for average users.'

From an industry perspective, humanoid robot shipments are far from sufficient to become a second growth curve for manufacturers.

IDC data shows that global humanoid robot shipments in 2025 totaled under 18,000 units, with sales around $440 million. Honor would need at least 3-5 more years to achieve scalable commercial returns in this track.

More challenging is Honor's weak technological barriers.

In December 2025, ByteDance and ZTE launched the 'Doubao phone' nubia M153, allowing users to execute cross-app tasks with one sentence. Honor product line president Fang Fei admitted that Doubao phone's technical logic 'highly aligns' with Honor's AI direction.

In April 2026, reports emerged that Honor was in talks with ByteDance to jointly develop a new generation of 'Doubao phones.'

The same applies to embodied AI. The half-marathon champion result reflects specific capabilities in specific scenarios; industry competition still hinges on scene application capabilities after technological leadership.

No matter how bright the future of AI may be, it cannot fill the current pits.

In Q1 2026, Xiaomi shipped 33.8 million smartphones, down 19.14% year-on-year; its smartphone business gross margin was 10.1%, down 2.3 percentage points year-on-year.

As a top-five brand, Xiaomi faces such cost pressures, meaning Honor's situation is even more dire. With rising storage chip prices, price cuts by Apple, and Huawei's strong return, smartphone makers are undergoing a brutal shakeout.

Conclusion:

From the moment Honor became independent from Huawei, its goal has been simple: survive, then soar.

In six years of independence, Honor did fly—from a 3% trough to an 18.1% peak, a 'smile curve' worth documenting.

But now, the curve is trending downward, with no inflection point in sight.

The core issue boils down to three words: not exciting.

Smartphone business: No brand loyalty, forced into mid-to-low-end price wars, easily outmatched by Huawei;

IPO narrative: Valuation shrinkage, employee share withdrawals, shareholder anxiety—the capital market has already voted;

At the MWC, Li Jian remarked, "There's no rainbow without rain." However, capital markets are not swayed by mere catchphrases.

What Honor urgently requires at present is not an elaborate blueprint for an "AI terminal ecosystem," but rather the fortitude to develop genuinely distinctive products that consumers are willing to pay for in the current market landscape.

Securing a stable foundation for its smartphone business is the sole avenue to afford Honor the time necessary to substantiate its AI narrative. For the AI story to hold water, it must initially demonstrate that it is not a mere figment of imagination.

Otherwise, the instant the flywheel loses momentum, Honor will find itself on the brink of another "descent."

Disclaimer:

Kindly be informed: This analysis is predicated on publicly available information (financial reports, announcements, etc.). The author makes no assurances regarding the adequacy or timeliness of these information sources. The stock market is fraught with risks; capital may be forfeited. Exercise utmost caution when making investment decisions! All opinions expressed in this article are strictly the author's personal commentary and should never be construed as advice for buying or selling. Investors are obligated to conduct independent research and make judicious decisions based on their individual circumstances, assuming all associated risks.

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle