Q2 Mobile Phone Market: Huawei, Samsung, and Apple Shine Amid Industry Struggles for OPPO, Xiaomi, and vivo

07/17 2026

07/17 2026

403

403

AI Drives Memory Demand, Splitting Mobile Phone Industry

Author|Qingyun

Editor|Xiaobai

Illustrations|AI Generated

Produced by|Qiangdiao Next

While AI has not yet become the primary incentive for most users to upgrade their smartphones, it has significantly impacted the cost structures of mobile phone manufacturers.

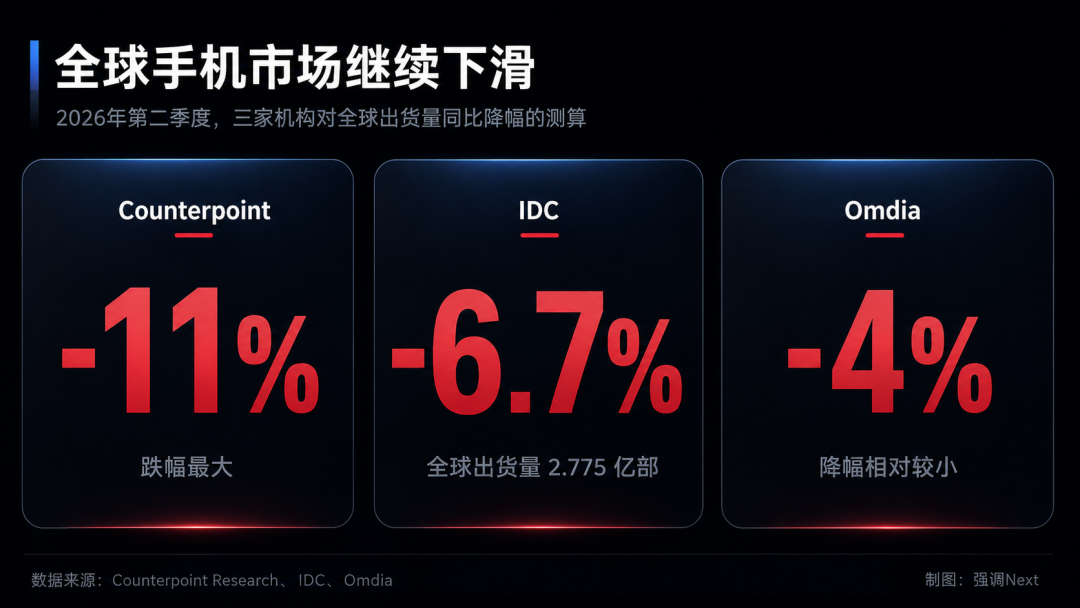

In mid-July, leading market research firms Counterpoint, IDC, and Omdia sequentially released their Q2 2026 data. Despite using different statistical methods, all three reported declines in global shipments, with figures at 11%, 6.7%, and 4%, respectively. According to IDC, global smartphone shipments in Q2 reached 277.5 million units. Counterpoint, however, noted that this was the lowest Q2 shipment volume since 2013.

The overall market decline is not surprising; what stands out is the pattern of this decline.

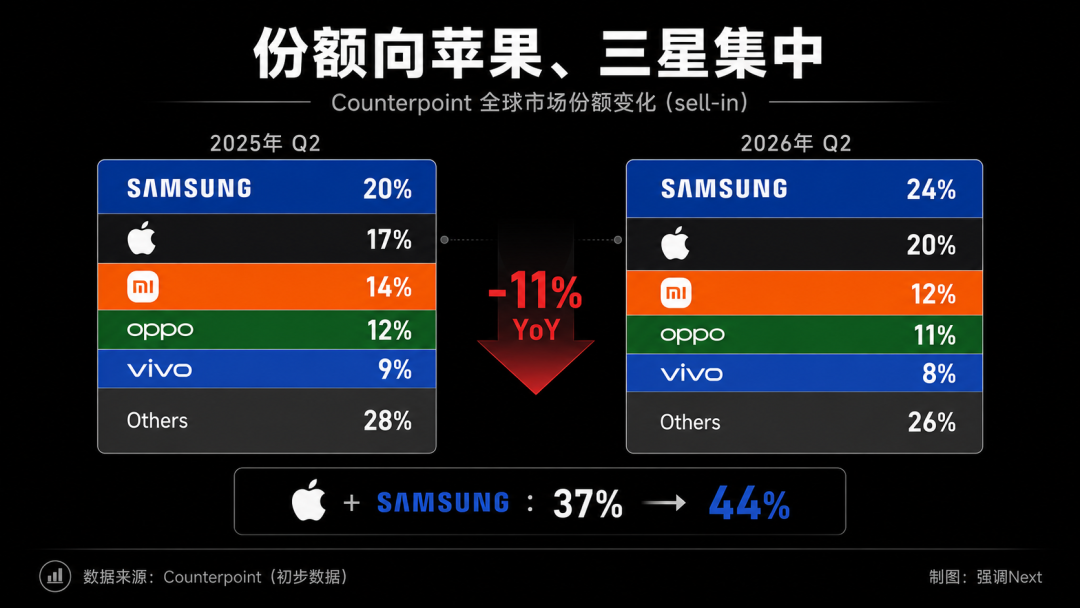

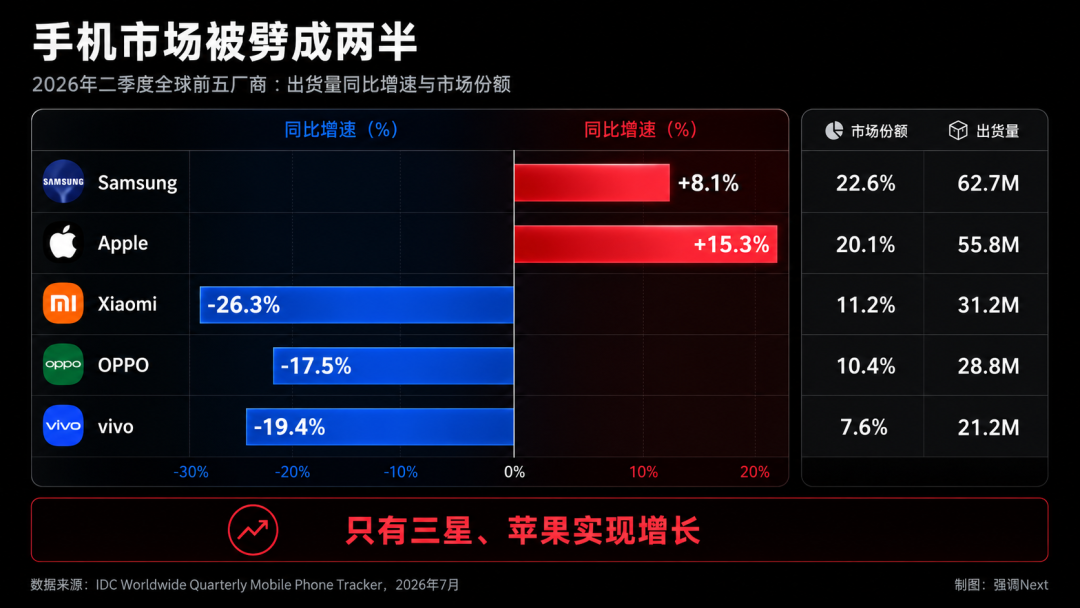

Among the top five global manufacturers as per IDC, only Samsung and Apple achieved positive growth. Xiaomi, OPPO, and vivo experienced shipment declines of 26.3%, 17.5%, and 19.4%, respectively. Huawei, though not in the top five globally, achieved a 20.9% year-over-year growth and secured the top spot in the Chinese market.

A clear divide has emerged: companies with scale, robust supply chain relationships, and premium product structures are expanding their advantages, while brands reliant on mid-to-low-end volume sales are being rapidly dragged down by rising costs.

01. Memory Market Divides Industry into Two Camps

The starting point of this industry adjustment lies in the memory sector.

The rapid expansion of AI data centers has led companies like Samsung Electronics, SK Hynix, and Micron to allocate more resources to HBM and server storage. This shift has pressured the supply of DRAM and NAND used in mobile phones, causing procurement prices to rise continuously.

IDC reported that mobile phone memory costs in Q2 had risen nearly 300% compared to a year ago, accounting for over 65% of the material costs in some low-end models. Omdia's data also indicated that the average prices of DRAM and NAND rose by more than 80% quarter-over-quarter in Q1 2026.

This has led to an unbalanced cost structure.

In a smartphone priced around 1,000 yuan, there is room to compress costs for the screen, chip, imaging, and battery, but memory is difficult to significantly reduce. Reducing configurations would immediately impact system smoothness and lifespan; maintaining configurations means the original pricing can no longer cover costs.

Manufacturers are left with few options: raise prices, reduce low-end models, or shift resources to the more profitable mid-to-high-end market. Omdia predicts that the global average selling price of smartphones will rise from $467 to $565 in 2026, a 21% increase. Shipments, however, may decline by 12.2% during the same period. The mobile phone industry is transitioning from competing on volume to competing on the ability to raise prices.

Samsung and Apple were the first to benefit from these changes.

IDC data showed that Samsung's Q2 shipments reached 62.7 million units, up 8.1% year-over-year, with its market share rising to 22.6%. Apple's shipments were 55.8 million units, up 15.3% year-over-year, with its share reaching 20.1%, the highest Q2 level in the company's history.

Samsung's advantage stems from its scale and supply certainty. As one of the world's largest mobile phone manufacturers and a major memory chip supplier, Samsung enjoys supply stability, strong bargaining power, and group risk resistance far superior to those of most Android manufacturers, even though its mobile business procures memory according to market mechanisms.

Apple, on the other hand, relies on its premium product structure to absorb costs. A $100 increase in memory prices might eliminate profits for a $1,000 phone, but on an iPhone priced at several thousand or even over ten thousand yuan, the cost proportion is much lower. Apple also secured some supply in advance and kept iPhone prices stable while competitors generally raised prices, prompting some consumers to upgrade early.

This advantage has a time limit. Omdia has noted that Apple raised prices for some other hardware products at the end of Q2. Whether the iPhone will follow suit will be a key variable in the second half of the year.

02. Huawei Seizes a Counter-Cyclical Opportunity

In a quarter where Android manufacturers generally faced pressure, Huawei took a different path.

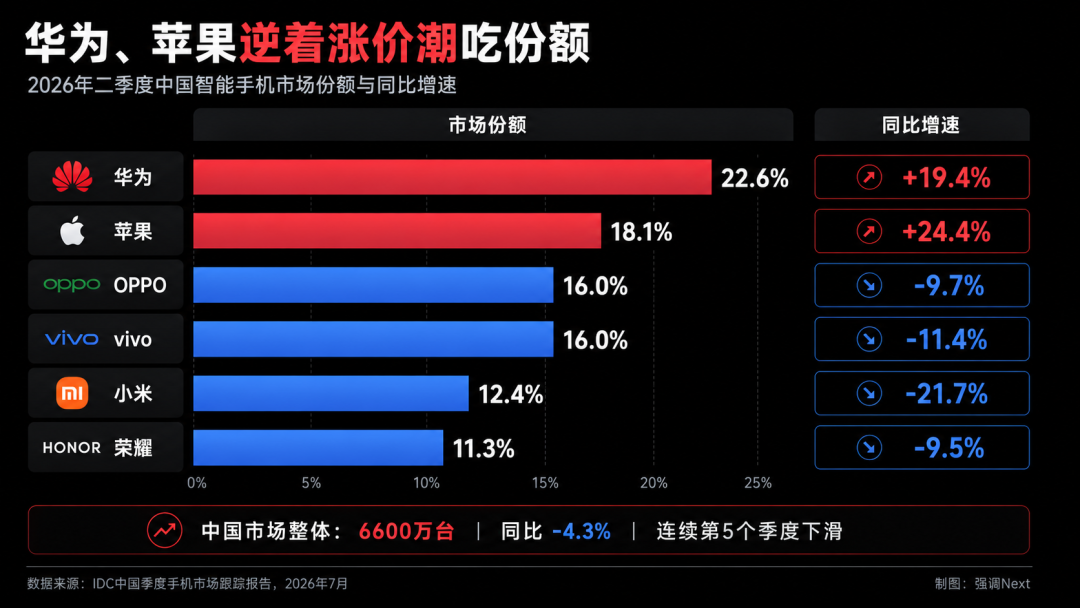

IDC data showed that Huawei's global mobile phone shipments in Q2 grew by 20.9% year-over-year. In the Chinese market, Huawei's shipments grew by 19.4%, with its share reaching 22.6%, ranking first; Apple grew by 24.4%, ranking second. Xiaomi, OPPO, vivo, and Honor all saw declines.

Huawei's core strategy this round is straightforward: maintain stable pricing, with some new models even actively reducing prices.

The starting price of the Mate 80 standard version is 4,699 yuan, 800 yuan lower than the previous generation. After the supply of Kirin chips improved, the shortage issues that constrained Huawei in previous years eased, and the company also extended its HarmonyOS to more price segments. Counterpoint data showed that HarmonyOS's market share in China's smartphone operating system market reached 19% in Q1 2026, again surpassing iOS.

While competitors raised prices, Huawei used stable pricing and a more complete product lineup to gain share. While competitors cut low-end products, Huawei continued to explore the mass market.

This is a strategic trade-off. Huawei sacrificed some short-term pricing power in exchange for channel recovery, HarmonyOS installation volume, and user reengagement. As long as supply can keep up, this window may persist for some time.

03. Xiaomi, Honor, OPPO, and vivo Face Unique Challenges

The memory crisis has impacted other Chinese mobile phone manufacturers similarly, but the problems exposed vary.

Xiaomi faces the simultaneous contraction of its mobile phone business and investment in new businesses.

In Q1 2026, Xiaomi's mobile phone revenue declined by 12.5% year-over-year to 44.3 billion yuan, with shipments falling by 19.2% to 33.8 million units. Mobile phone gross margin dropped from 12.4% to 10.1%. During the same period, revenue from Xiaomi's smart electric vehicles, AI, and other innovative businesses grew by 6.9% to 19.9 billion yuan, while group R&D expenses increased by 33.4% to 9 billion yuan.

This set of data describes Xiaomi's situation more accurately than the notion of "smartphones subsidizing electric vehicles."

Investment in electric vehicles, AI, and robotics must continue, while the mobile phone business is losing both volume and profitability. Xiaomi can neither stop investing in new businesses nor abandon mobile phones, which still contribute nearly half of the group's revenue. Rising memory prices further compress maneuvering space, forcing the company to cut inefficient products and organizational costs, concentrating mobile phone resources on more profitable models.

Honor faces more pressure from the capital markets.

IDC data showed that Honor's market share in China in Q2 was 11.3%, with shipments declining by 9.5% year-over-year. The company has completed its joint-stock reform and initiated IPO counseling in June 2025, but the original counseling timeline did not proceed as planned. Honor explicitly denied the termination of its IPO in May this year while opening an employee equity exit channel but did not announce a new listing timeline.

The publicly available information is insufficient to prove that rising memory prices directly hindered Honor's IPO. However, with the overall contraction of the mobile phone industry and profitability under cost pressure, the capital markets will inevitably focus more on Honor's sustained profitability in its mobile phone business and when investments in AI terminals and humanoid robots will generate revenue.

OPPO's challenge is managing internal brand cannibalization.

OPPO's global market share in Q2 was approximately 11%. In the Chinese market, its shipments declined by 9.7% year-over-year.

Compared to Xiaomi, OPPO's decline is not as significant. However, the resource overlap left by years of multi-brand expansion has become a burden OPPO urgently needs to shed.

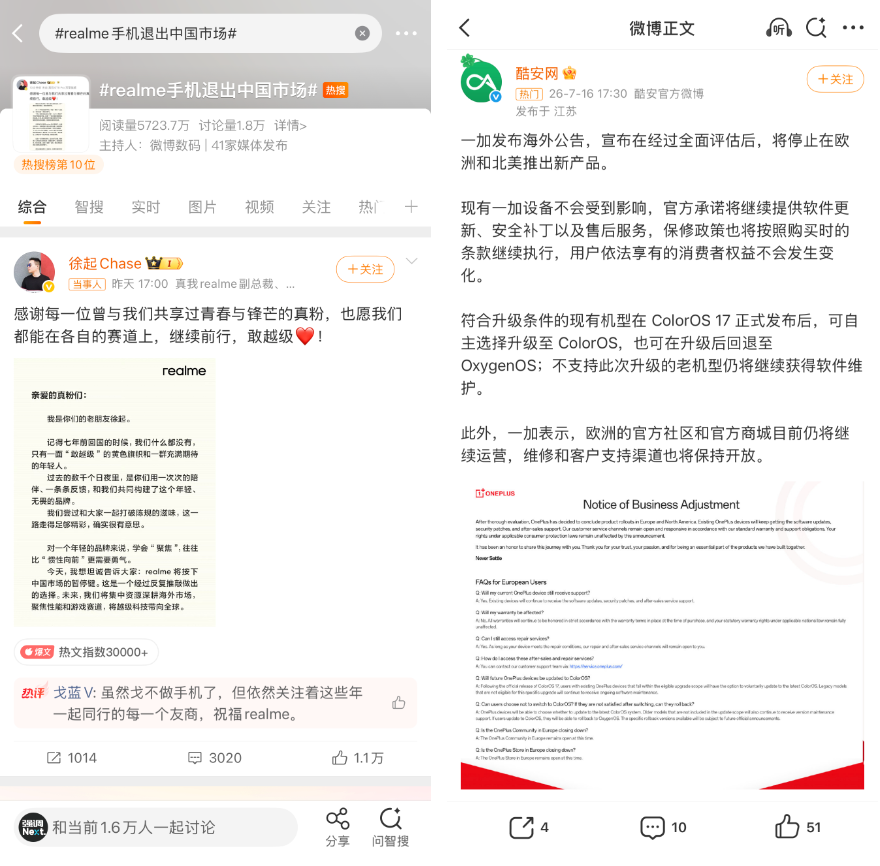

Recently, OPPO finally announced that realme would exit the Chinese market and OnePlus would exit the European and North American markets, confirming previous foreign media rumors. As recently as January this year, realme had just rejoined the OPPO system.

When the market was growing, multi-brand strategies helped OPPO cover more price segments and channels. As the market shifted to inventory competition, the problems reversed, and multi-brand strategies led to internal cannibalization.

OPPO, OnePlus, and realme have long had overlapping positions in the 2,000 to 4,000 yuan price range, all emphasizing performance, fast charging, and young users, while sharing supply chains, systems, and some R&D capabilities. On the surface, the three brands compete for the market together, but in reality, they also compete for similar users, marketing budgets, and channel resources.

This round of rising memory costs and compressed profits on low-end models has undoubtedly amplified the impact of this issue.

However, retrenchment can only save costs, not solve growth problems. Whether OnePlus can capture OPPO's online share depends on its ability to differentiate from the main brand. Otherwise, with fewer brands, sales may not recover. What OPPO truly lacks is a sufficiently clear brand differentiation and strategic focus: why the main brand deserves to be priced higher and how OnePlus can capture young users from Xiaomi, Honor, and iQOO.

vivo's choice is closer to actively pursuing the high-end market.

IDC data showed that vivo's global shipments in Q2 declined by 19.4% year-over-year. In March, vivo and iQOO already raised prices for some products. Meanwhile, vivo continued to strengthen its flagship imaging capabilities, with the X300 Ultra starting at 6,999 yuan in China and reaching up to 11,999 yuan for the highest configuration and photography package. The Indian version was priced at 159,999 rupees.

Stacking imaging features does increase costs, but for vivo, it is also a way to shift cost pressures upward. Mid-to-low-end models struggle to pass on increased memory costs to users, while high-end imaging flagships can establish higher prices through lenses, sensors, and brand positioning.

This path is not without risks, but it aligns with the changes happening across the industry. The less profitable the low-end market becomes, the more manufacturers need to create new reasons to buy high-end products. However, it remains uncertain whether the vivo brand can support these price points.

04. The Second Half Will Be the True Stress Test

The Q2 figures do not yet fully reflect the cost impact.

IDC pointed out that the low-cost memory inventory some manufacturers had stockpiled earlier is still providing a buffer. As inventory is depleted, cost pressures will further transmit to shipments and retail prices in the second half of the year. IDC predicts that the year-over-year decline in the Chinese smartphone market in the second half of 2026 may widen to around 20%.

For the full year, IDC expects global smartphone shipments to decline by 13.9% to 1.09 billion units. Omdia predicts a 12.2% decline. Both agencies believe that memory supply and demand are unlikely to recover significantly before 2027, and a meaningful market rebound may not occur until 2028.

This crisis is redefining the core capabilities of mobile phone manufacturers.

Supply chain management is no longer just about early stockpiling and lowering procurement prices but also about securing long-term access to critical components. Premiumization is no longer just about upgrading materials and imaging parameters but about whether users are willing to pay higher prices for the brand and experience.

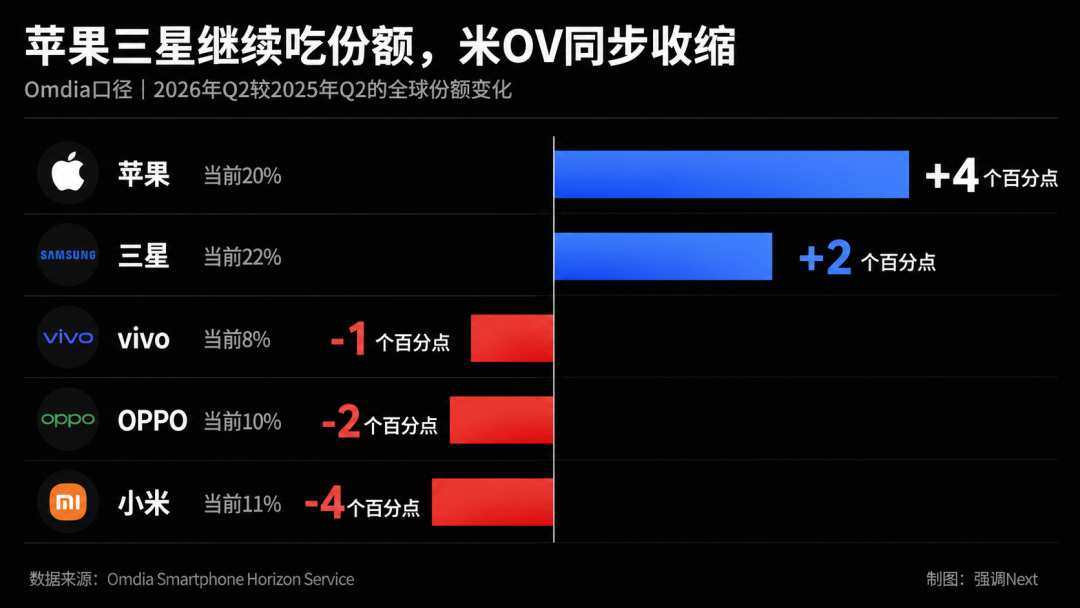

Samsung, Apple, and Huawei are temporarily in a favorable position. Xiaomi, OPPO, vivo, and Honor still have room for adjustment, but the old methods of relying on low-priced volume sales, a flood of models, and frequent specification upgrades are no longer sustainable.

More interestingly, this crisis was triggered by the expansion of AI infrastructure, and the next growth answer proposed by mobile phone manufacturers is also AI.

AI first took away mobile phones' memory. Next, on-device models and intelligent agents must prove they can bring users' upgrade demand back. Otherwise, AI phones will merely become more expensive devices without a corresponding increase in purchase justification.

- END -

-

The Moment to Evaluate Montage Technology Has Arrived

-

![]()

StepOn Has Solved the Monetization Challenge of Large Models with Just a Smartphone

-

![]()

Is a Camera the New AI Safety Guardian? Hikvision Introduces Active Vision Operation Monitoring Gun-Ball Camera at WAIC 2026

-

The Second Half of AI: Cost-Effectiveness Takes Center Stage

-

![]()

Location, Concentration, and Trajectory Tracking: Hikvision’s TDLAS Gas Cloud Imaging Telemetry System Debuts at WAIC 2026

-

The 'AI Study Tour' Under the Original Equipment Manufacturer Model is Set to Create a New Wave of Internet-Famous Science and Innovation Cities

-

![]()

Now, There's a 'Basis' to Curb 'Price Wars': Future Reports of Automakers Setting Low Prices Will Be Probed Under New Rules

-

![]()

WAIC 2026: Farewell to Parameter Races, Full-Chain AI Commercialization