Perspective on Weimob's 2024 Interim Report: Revenue Drops Again, Losses Persist, Obstacles in Tail-Cutting Survival Strategy?

08/26 2024

08/26 2024

580

580

Author: Xingxing

Source: Beiduo Finance

Recently, Weimob Group (HK:02013, hereinafter referred to as "Weimob") released its 2024 interim performance report. Since the beginning of the year, cost reduction and efficiency improvement, as well as focusing on the main business, have remained the main themes of Weimob's operations. However, while effectively slowing down the pace of losses and improving the fundamentals of business quality, the scale of the company's various businesses has declined significantly.

As the traditional SaaS business reaches its traffic ceiling, Weimob Group, once hailed as the "first SaaS stock," has had to embark on a path of transformation, seeking a way out in the emerging popular sectors. Nevertheless, with consecutive setbacks in growth, Weimob has fallen into a "crisis of trust" in the secondary market, and its share price has continued to decline.

Faced with the winter of the industry, whether Weimob Group can navigate through the cycle, find certain performance increments amidst numerous uncertainties, and thereby boost market confidence, only time will tell.

I. Unstable Revenue Growth, Profitability Not Yet Established

Public information shows that Weimob Group, founded in 2013, is a cloud-based business and marketing solutions provider dedicated to providing merchants with decentralized digital transformation SaaS products and full-link growth services to support sustainable business growth. Its products cater to various industries such as e-commerce retail, supermarkets, and fresh produce.

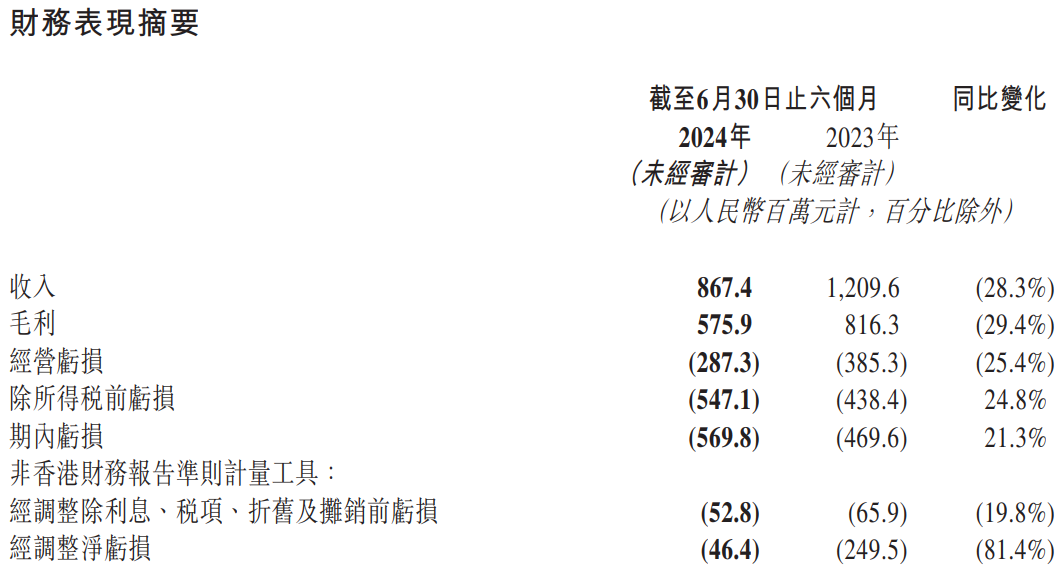

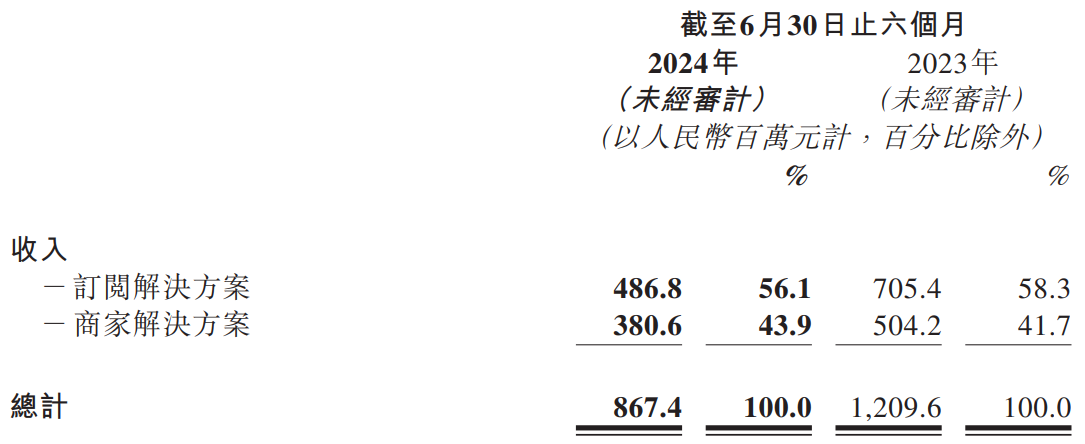

According to the financial report, Weimob Group's operating revenue for the first half of 2024 was 867 million yuan, a decrease of 28.3% compared to 1.209 billion yuan in the same period of 2023. Gross profit was 576 million yuan, down 29.4% year-on-year, and the overall gross margin also contracted by 1.1 percentage points to 66.4% compared to the same period in 2023.

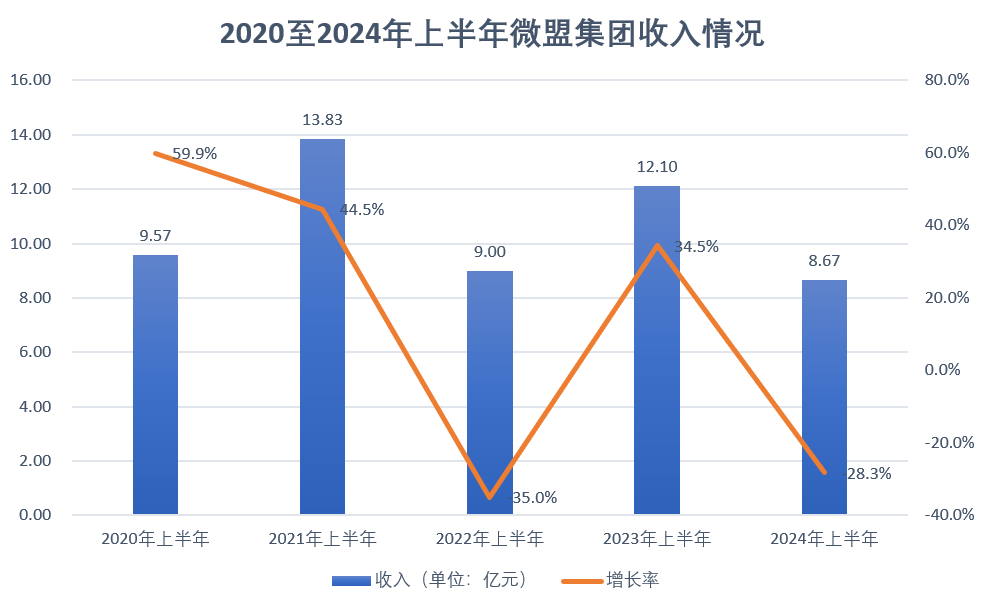

In the first half of 2023, Weimob Group's revenue increased by 34.5% to 1.21 billion yuan. In fact, Weimob's performance has been unstable in recent years, with revenues of 957 million yuan, 1.383 billion yuan, and 900 million yuan in the first half of 2020, 2021, and 2022, respectively, representing growth rates of 59.9%, 44.5%, and -35.0%, respectively.

In other words, Weimob Group's revenue in the first half of this year was even lower than four years ago. On an annual basis, after achieving a new high of 2.686 billion yuan in revenue in 2021, Weimob's revenue plummeted by 31.5% to 1.839 billion yuan in 2022. Although it rebounded by 21.1% to 2.228 billion yuan in 2023, it still failed to recover to its peak level.

It is worth noting that Weimob Group has recorded losses for several consecutive years, with net losses of 1.157 billion yuan, 783 million yuan, 1.829 billion yuan, and 758 million yuan from 2020 to 2023, respectively, amounting to cumulative losses exceeding 4.5 billion yuan over the past four years. In 2019, however, the company briefly turned a profit, achieving a net profit of 311 million yuan.

Weimob Group's operating loss in the first half of 2024 was 28.73 million yuan, a 25.4% year-on-year narrowing. Meanwhile, it recorded a net loss of 570 million yuan, an expansion of 21.3% year-on-year; the net profit margin also widened from -38.8% in the same period of 2023 to -65.7% under the condition of four consecutive years of negative values.

In contrast, Youzan (08083.HK), which operates in the same e-commerce SaaS sector as Weimob Group, achieved operational profitability in 2023. In the first half of 2024, Youzan's revenue was 686 million yuan, slightly lower than that of Weimob Group; its operating profit was approximately 2.586 million yuan, representing a year-on-year increase of 123%.

However, Weimob Group's adjusted net loss under non-HKFRS (Hong Kong Financial Reporting Standards) was 46.4 million yuan, a narrowing of 81.4% compared to 250 million yuan in the same period of 2023; the adjusted net profit margin also recovered from -20.6% in 2023 to -5.3%. The company's adjusted EBITDA also improved, narrowing by 19.8% year-on-year to 52.8 million yuan.

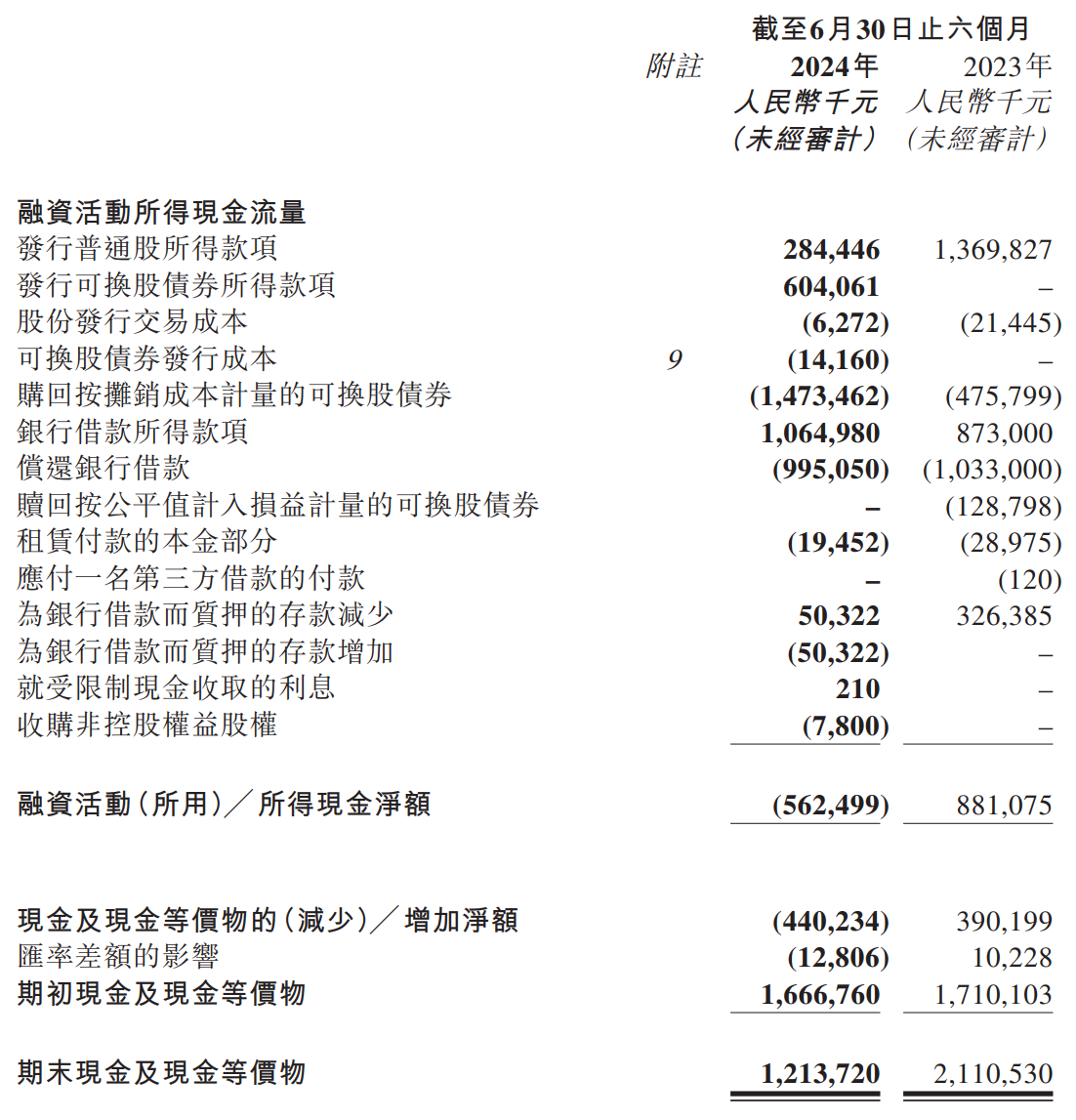

As of the end of June 2024, Weimob Group's operating cash flow was 29.498 million yuan, achieving positive cash flow for two consecutive half-year periods. However, the company's cash and cash equivalents at the end of the same period were 1.214 billion yuan, nearly halved compared to 2.111 billion yuan in the same period of 2023; total assets also decreased by 5.05% to 7.471 billion yuan.

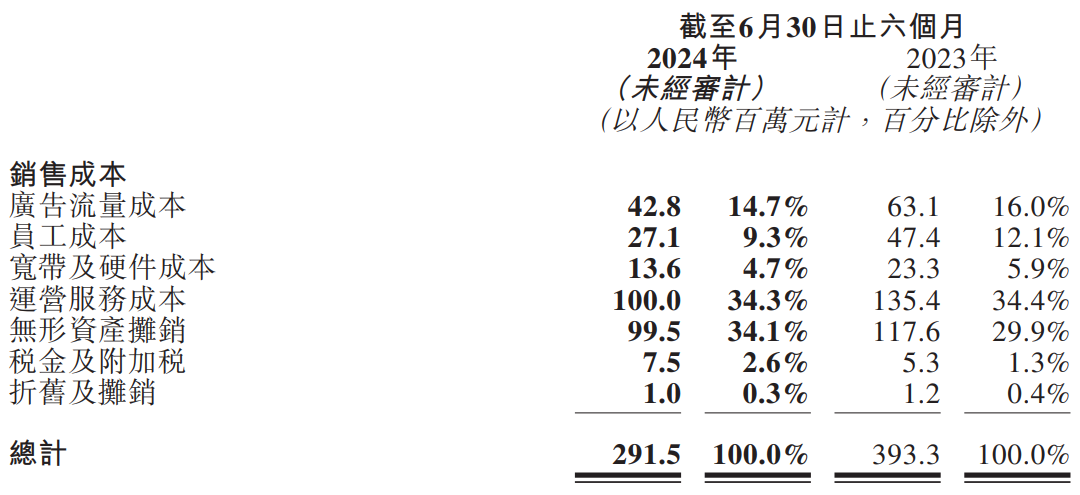

Weimob Group explained in its financial report that the decline in revenue was mainly due to its adherence to cost reduction and efficiency improvement, as well as focusing on its core business, by proactively downsizing non-core and low-quality businesses, reducing business scale, and cutting costs and expenses. Specifically, Weimob's total cost of sales decreased by 25.9% from 393 million yuan in the first half of 2023 to 291 million yuan.

Among these, the reduction in staff costs was particularly significant, with a near-halving from 47.4 million yuan to 27.1 million yuan. Behind this was Weimob Group's continuous layoff measures. As of the end of June 2024, Weimob Group had 3,952 full-time employees, nearly one-third fewer than the 5,704 employees at the end of the same period in 2023.

Previously, rumors had circulated that Weimob Group would disband its Wuhan subsidiary. Although Weimob responded that there was no such occurrence of disbanding the Wuhan company, only a change in business model with the introduction of the "Super Partner Plan," the internal turmoil still cast doubt on the sustainability of Weimob's business model.

Beiduo Finance found that various expenses of Weimob Group in the first half of the year also showed varying degrees of "slimming down." Its selling and distribution expenses, general and administrative expenses, and research and development expenses were 565 million yuan, 287 million yuan, and 234 million yuan, respectively, representing year-on-year decreases of 33.0%, 24.5%, and 26.8%.

Admittedly, cost reduction and revenue enhancement can help Weimob Group optimize asset quality and reduce losses to a certain extent, but it also significantly drags down revenue scale. By business segment, the company's subscription solutions revenue declined by 31.0% year-on-year to 487 million yuan in the first half of 2024; merchant solutions revenue also fell by 24.5% to 381 million yuan.

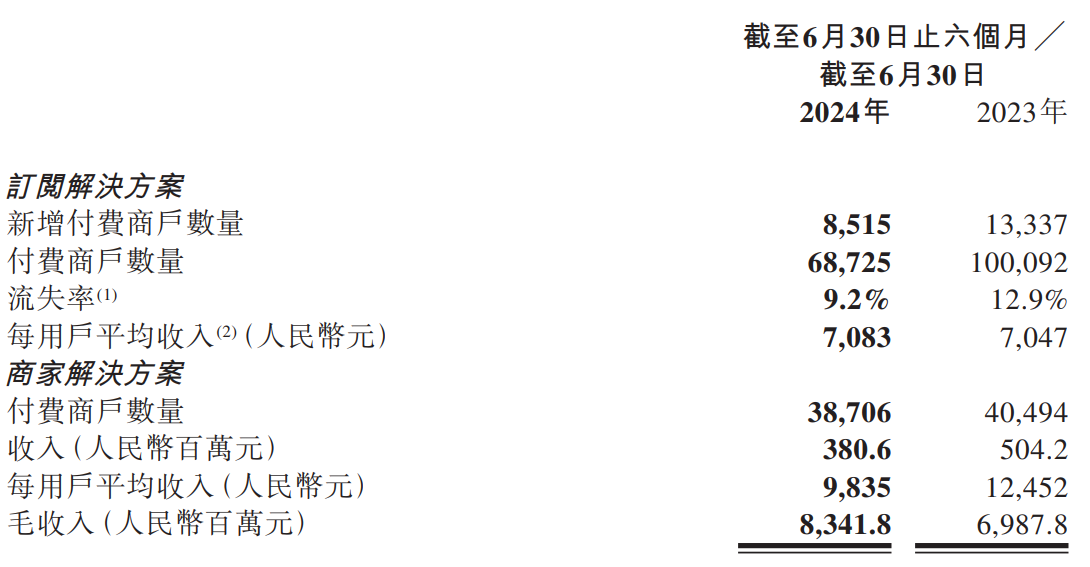

Moreover, the number of paying merchants for Weimob's subscription solutions decreased to 68,700, a drop of 31.3%; while the number of new paying merchants in the first half of the year was only 8,515, far from covering the number of lost users. The number of paying merchants for the company's merchant solutions also fell to 38,700, a decrease of 1,788 year-on-year.

In the key business areas of smart retail and other large customer segments developed by Weimob Group, the average revenue per user in the first half of the year was 7,083 yuan, an increase of only 0.5% year-on-year; revenue from smart retail was 304 million yuan, representing an endogenous growth of 3.1% year-on-year, but the actual scale of the business declined by 2.6% year-on-year.

It is foreseeable that while focusing on core businesses and optimizing organizational structure can alleviate Weimob Group's cost pressure to a certain extent, both the sudden decline in operating revenue and the continuous reduction in the number of paying users are questioning the long-term feasibility of Weimob's cost reduction and efficiency improvement strategy.

III. Diversified Layout Fails to Boost Market Confidence

In fact, as major platforms represented by WeChat have successively established closed-loop ecosystems, the SaaS membership system is no longer the only way for small and medium-sized enterprises to convert public domain traffic, and the e-commerce SaaS service business has entered a "recession." Facing a challenging market environment, proactive change has become the only option for Weimob.

In May 2023, Weimob Group launched Weimob WAI to expand "AI+SaaS" service touchpoints. It is reported that Weimob WAI is currently applied to more than ten large models, meeting enterprises' needs for online store opening, content marketing, private domain operation, and covering various marketing scenarios such as home decoration, finance, education, and tourism.

While betting on the hot AI concept in recent years, Weimob Group has also targeted the short video sector, strategically investing in Shanghai Banfan Information Technology Co., Ltd. (hereinafter referred to as "Banfan Technology") in March this year; it also signed a contract with Google CPP, becoming a Tier 1 agent in China and an official partner of Apple Ads.

At this stage, Weimob Group can be described as "going wherever there is heat." However, regardless of the capital consumption of the preliminary preparations for the new sector layout, the market's confidence in Weimob has long been lost without a proven business model, independent operation, and self-sustaining capability.

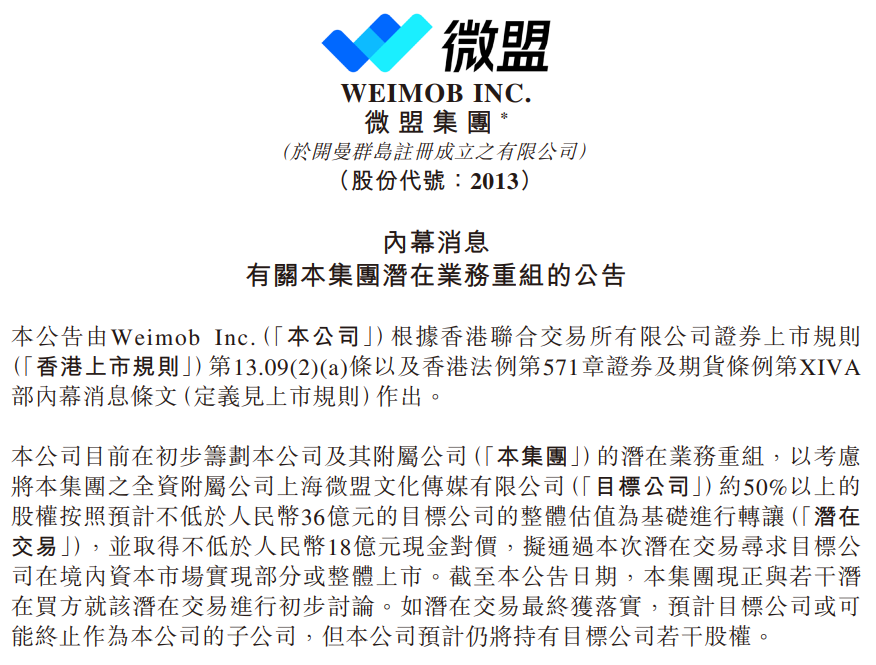

On January 16, Weimob Group announced its plan to transfer more than 50% of the equity of Shanghai Weimob Culture Media Co., Ltd. (hereinafter referred to as "Shanghai Weimob"), based on an estimated overall valuation of the target company of not less than 3.6 billion yuan, seeking to achieve partial or full listing of Shanghai Weimob in the domestic capital market.

Weimob Group believes that this move can reduce the impact of Weimob's marketing working capital on its cash flow and facilitate financing for Shanghai Weimob as an independent entity, with a strategic significance akin to "sacrificing pawns to protect the king." However, the market did not buy into this plan, and the company's share price plunged significantly the day after the announcement was made, closing at 1.98 Hong Kong dollars per share, down 11.61%.

Ultimately, Weimob reluctantly announced the termination of the potential transaction plan, citing "a series of constructive feedback received from shareholders regarding the potential transaction." The Weimob Board of Directors also announced that it would choose an appropriate time to repurchase Weimob shares, and the management team, led by CEO Sun Taoyong, would increase their shareholdings, attempting to boost market confidence.

However, the reality is that on the day following the release of Weimob's interim report, its share price fell by more than 10%. As of the close on August 23, 2024, Weimob Group was trading at 1.13 Hong Kong dollars per share, with a total market value of only 3.477 billion Hong Kong dollars. The former glory has vanished, and the market and investors have left little opportunity for Weimob now.

-

![]()

Internet Valuation Logic Shifts: From Scale Narrative to Profit Accountability

-

VOYAH Struggles to Find Its Niche in the Competitive Auto Market

-

![]()

Maxwell Technologies Gains Indirect Stake in Precision Optics via New Venture

-

![]()

Raising 1.8 Billion! This Domestic Optical Inspection 'Little Giant' is Going Public

-

China's AI 'Normandy Moment': The Explicit and Implicit Threads of BATL

-

![]()

Starting at 4999 Yuan! Nubia RedMagic Gaming Tablet 5 Pro Review: Impressive Performance, But Hefty Price Tag

-

![]()

ByteDance Initiates First Major Management Reform

-

![]()

AI is Quietly Destroying a Trillion-Dollar Industry