In 2026, Mobile Phone Manufacturers Flock to the 'Safe Haven' of Foldable Phones

03/13 2026

03/13 2026

553

553

Author|Xie Jiabaoshu

Niche foldable phones are becoming the focus of smartphone manufacturers.

Image Source: Honor

On March 1 and 10, 2026, Honor held two consecutive launch events to unveil its foldable flagship, the Honor Magic V6. Equipped with a self-developed Ultimate Black Diamond screen, a 2800MPa Honor Shield Tunnel Steel hinge, and a 6850mAh battery, the device starts at 8,999 yuan. Honor CEO Li Jian stated that the Magic V6 boasts comprehensive "foldable grand slam" capabilities, earning it the title of the "King of Foldables."

OPPO has also officially announced that it will hold a product launch event on March 17 to introduce the OPPO Find N6. Featuring a next-generation titanium alloy Sky Dome hinge and Sky Dome memory glass, the device achieves a "crease-free, long-lasting flat" effect. OPPO Chief Product Officer Liu Zuohu believes that the Find N6 not only represents a significant leap in foldable technology but also delivers an exceptional user experience.

Not only Honor and OPPO are launching new foldable models. Xiaomi, vivo, and Huawei are also set to update their annual foldable flagships in the coming months. More notably, Apple, known for its "aloof" stance, will enter the foldable market this fall with the horizontally inward-folding iPhone Fold.

In fact, foldable phones are not a novel concept. As early as February 2019, Samsung introduced the Galaxy Fold, the world's first mass-produced foldable phone, marking seven years since its debut. For traditional bar-style smartphones, seven years would have been enough time for the iPhone to evolve from its first generation to the iPhone 6. However, the foldable segment has been relatively slow to gain traction, only now drawing Apple into the fray.

This raises questions: Why are smartphone manufacturers unanimously ramping up their focus on foldable products in 2026? Can foldable phones become the next big hit? What value do they hold for the smartphone industry?

01

The Smartphone Market Continues to Shrink, Leaving Manufacturers Struggling

While smartphones remain the dominant computing platform for the masses, increasing homogenization and performance excess have weakened consumer motivation to upgrade, causing the smartphone market's ceiling to steadily decline.

Image Source: IDC

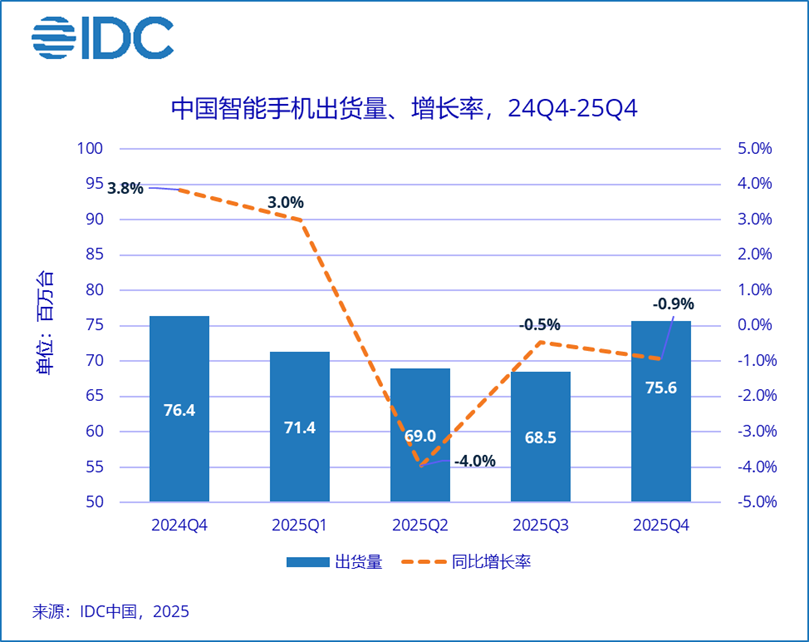

IDC data shows that from 2019 to 2025, annual smartphone shipments in China dropped from 370 million to 284 million units, with a compound annual decline rate of 4.31%. The Chinese smartphone industry has long since entered a inventory (inventory-driven) era.

Given the shrinking market dividends, many smartphone manufacturers have resorted to intense competition over underlying specifications to maintain their influence, leading to a decline in performance.

Image Source: Xiaomi's Q3 2025 Financial Report

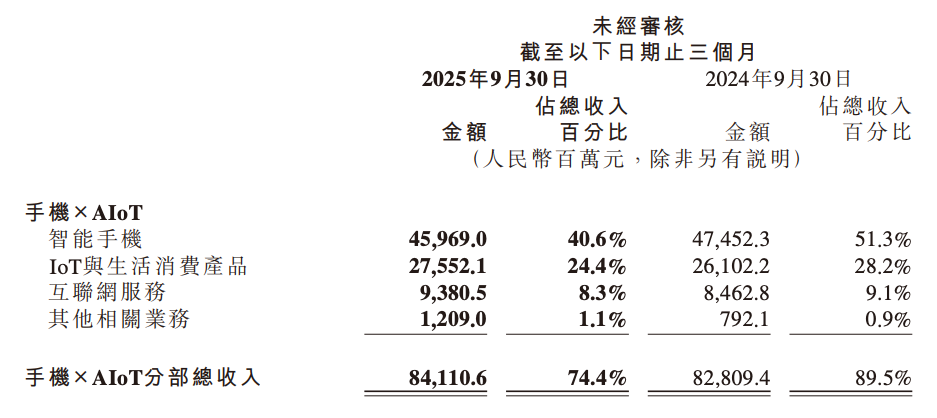

For example, Xiaomi's Q3 2025 financial report revealed that smartphone shipments reached 43.3 million units, up 0.5% year-on-year. However, the average selling price of Xiaomi phones fell 3.6% year-on-year to 1,062.8 yuan, while the gross margin declined by 0.6 percentage points to 11.1%. Due to the inability of shipment growth to offset price declines, Xiaomi's smartphone revenue for the quarter was 46 billion yuan, down 3.1% year-on-year.

Admittedly, not all manufacturers have fallen into negative growth amid the declining smartphone shipment scale. Apple, for instance, demonstrated strong growth during the downturn with its iPhone 17 series, released in September 2025.

Image Source: IDC

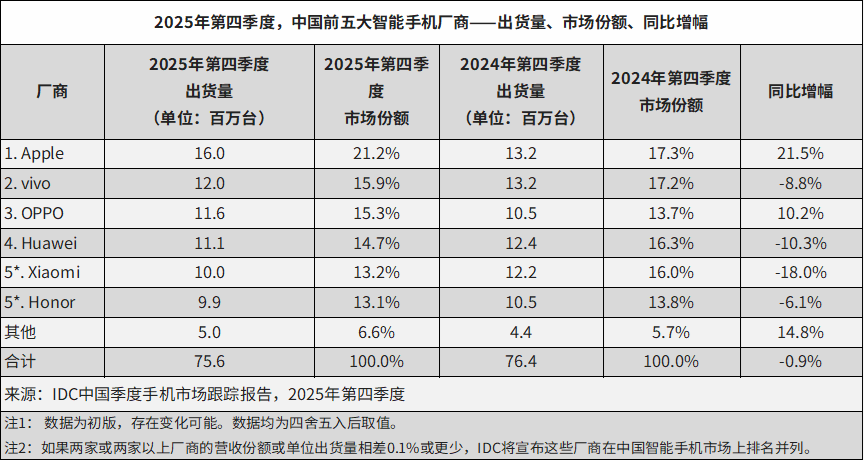

IDC data shows that in Q4 2025, Apple shipped 16 million smartphones in the Chinese market, ranking first with a 21.5% year-on-year increase. Data from digital blogger "RD Observation" revealed that as of the 9th week of 2026, iPhone 17 series sales in China reached 23.8397 million units, far outpacing Android flagships.

However, it should be noted that the iPhone 17 series' impressive sales largely stem from Apple's significant upgrades. The standard iPhone 17 no longer adheres to "entry-level" specifications but features a second-generation Ceramic Shield front cover, an LTPO display supporting ProMotion and full-screen AOD, with a peak brightness of 3,000 nits.

By enhancing underlying specifications, Apple has gained some breathing room, but this also indicates that, under increasing market downturn pressure, Apple has lost its competitive dominance and must resort to passive "intensification" to maintain product competitiveness.

Image Source: Apple

As Li Nan, former vice president of Meizu Technology, remarked, "The iPhone 17 series' current success is mainly due to a surprise attack. However, if the Android camp responds aggressively, even if the 17 loses, the 18 or 19 will eventually be defeated." As Android manufacturers launch counterattacks, Apple must still confront the challenge of a steadily declining smartphone market ceiling.

Amid growing anxiety among smartphone manufacturers due to intensified competition, the emerging foldable phone segment offers a new outlet for the industry. IDC data shows that from 2021 to 2025, annual foldable phone shipments in China grew from 1.5 million to 10.01 million units, with a compound annual growth rate of 60.7%.

While foldable phone shipments remain relatively small, the segment's growth potential provides a rare incremental space for smartphone manufacturers stuck in a inventory (inventory-driven) competition. By entering the foldable phone market, manufacturers can reshape their growth logic through form factor innovation, balancing the downward pressure of a shrinking overall market.

02

Soaring Memory Prices Make Foldables a 'Safe Haven'

The primary reason smartphone manufacturers are intensifying their focus on foldable products in 2026 is, of course, the shrinking overall smartphone market. A more direct factor is that, amid rising memory prices, foldable phones—with their stronger pricing power—have become a "safe haven" for manufacturers to hedge against cost pressures.

Image Source: Counterpoint Research

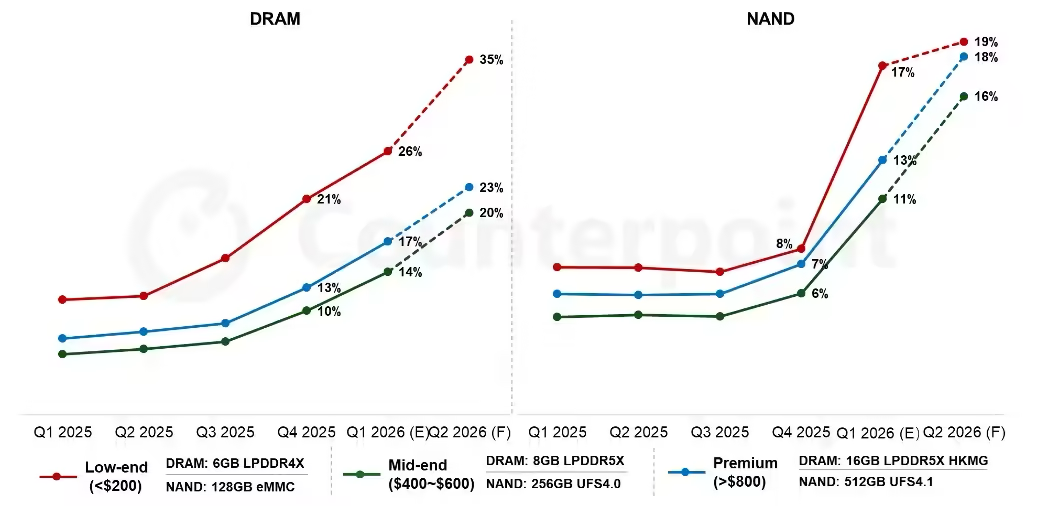

Since the second half of 2025, memory prices have surged due to explosive demand for AI computing power. Counterpoint Research's report reveals that in Q1 2026, mobile memory prices continued to rise sharply, with DRAM prices increasing by over 50% quarter-on-quarter and NAND Flash prices by over 90%.

Image Source: OPPO

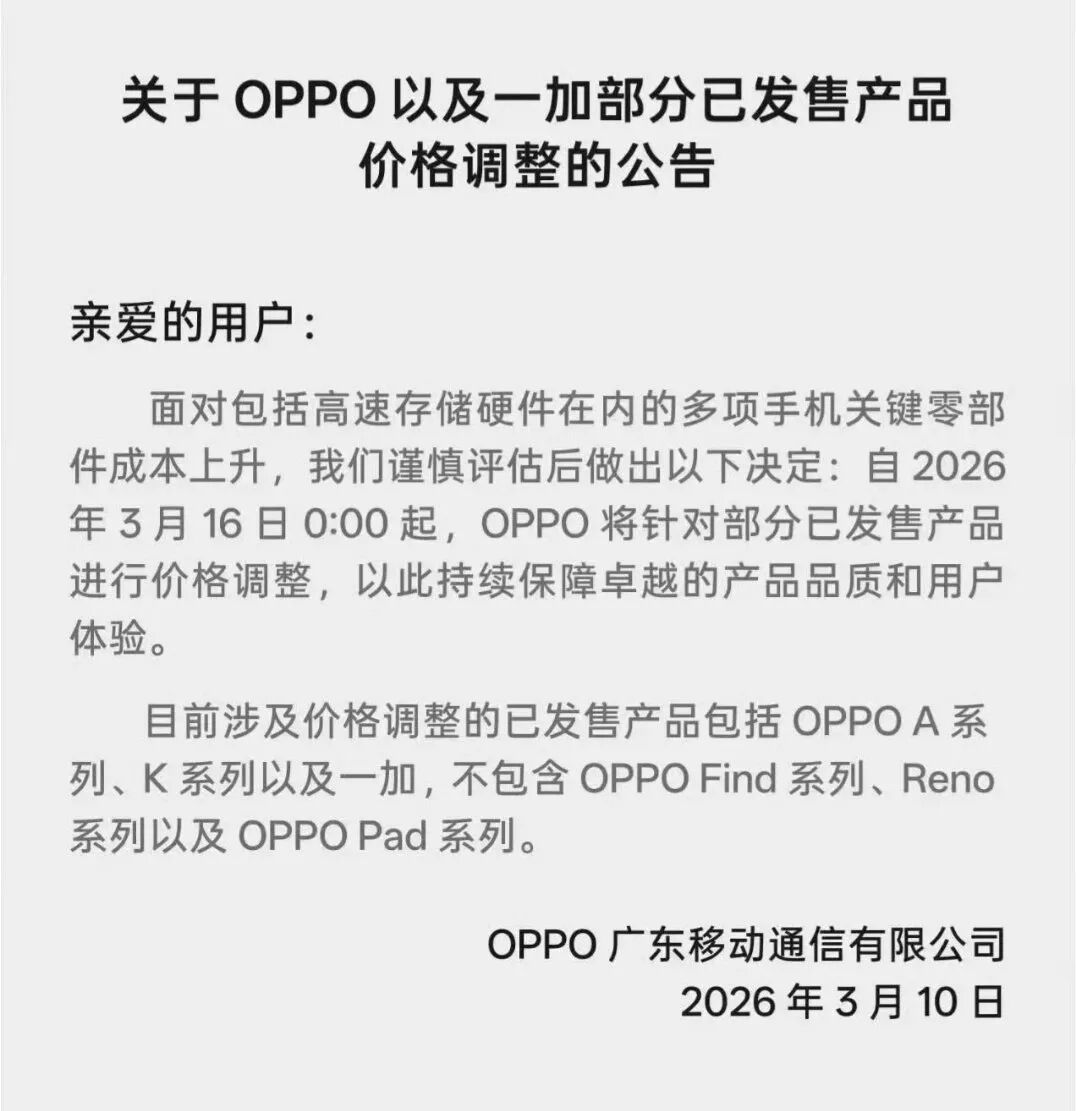

Under these circumstances, smartphone manufacturers have had to pass cost pressures onto consumers. On March 10, 2026, OPPO announced that, due to rising costs of key smartphone components, including high-speed storage hardware, prices for some already-released products, such as the OPPO A series, K series, and certain OnePlus models, would be adjusted starting March 16.

To balance soaring upstream component costs, some manufacturers have even chosen to "reverse course." On March 11, prominent digital blogger "Digital Chat Station" revealed, "They're out of options—mid-range and low-end new models are now testing 90Hz waterdrop screens." Notably, mid-range and low-end models have already adopted 120Hz punch-hole screens, while 90Hz waterdrop screens were mainstream around 2019. This significant regression reflects smartphone manufacturers' helpless (helplessness) and compromise.

Given that consumer motivation to upgrade has long weakened, surging memory costs triggering smartphone price hikes and specification cuts will further suppress replacement demand.

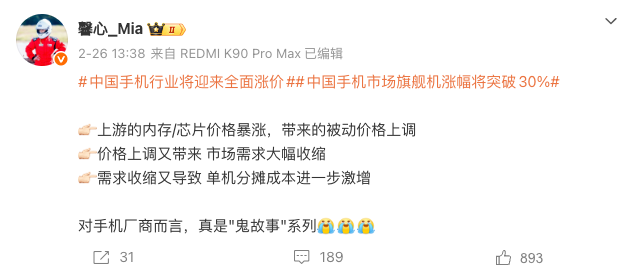

Image Source: Hu Xinxin

On February 26, 2026, REDMI Product Manager Hu Xinxin posted on social media that soaring upstream memory and chip prices had forced phone prices to rise passively. This price increase led to a significant contraction in demand, which, in turn, caused per-unit cost allocation to surge further. "For phone manufacturers, it's truly a 'horror story' series."

Image Source: TrendForce

In February 2026, TrendForce's research data showed that under baseline forecasts, global smartphone production in 2026 is expected to reach 1.135 billion units, down 10% year-on-year. Under pessimistic forecasts, production could drop to 1.061 billion units, a 15% year-on-year decline.

Against this backdrop, smartphone manufacturers are ramping up foldable phones not only because the segment maintains positive growth but also because foldables' high prices can significantly offset memory price increases.

On February 28, 2026, the National Development and Reform Commission's Price Monitoring Center released a notice titled "Storage Chip Prices Continue to Rise and Pass Down to Downstream." As of January, DRAM and NAND flash memory prices had reached their highest levels since data became available in 2016. The average contract price for DRAM (DDR4 8Gb 1G*8) was $11.5, up about 83% from September 2025. The average contract price for NAND flash memory (128Gb 16G*8 MLC) was $9.5, nearly 1.5 times higher than in September 2025.

A simple linear calculation shows that from September 2025 to January 2026, the storage cost of a 12GB+256GB phone rose from about $136 (approximately 936.07 yuan) to about $290 (approximately 1,996.04 yuan), a net increase of about 1,059.97 yuan.

It should be noted that this calculation model is relatively rough and does not account for factors such as shipment scale or manufacturers' bargaining power, so it does not represent actual terminal costs. However, considering that most phones now use LPDDR5+UFS storage combinations, which are more expensive than DDR4+MLC, the actual cost pressure on manufacturers may be even greater than the above figures suggest.

For mid-range and low-end models, which already have low selling prices, directly passing memory cost increases onto the market could easily trigger consumer resistance.

Take a phone originally priced at 2,000 yuan with a 12GB+256GB configuration as an example. If the price is raised by about 1,000 yuan in line with memory price increases, the total price would reach 3,000 yuan, a 50% increase. Such a dramatic hike would be unacceptable to price-sensitive mid-range and low-end phone users.

In contrast, due to higher research and development costs and significant differentiation, foldable phones often sell for tens of thousands of yuan, allowing them to handle memory price increases more calmly.

Image Source: Honor

Take the Honor Magic V6 as an example. Its 16GB+512GB and 16GB+1TB versions are priced at 10,999 yuan and 11,999 yuan, respectively, representing increases of 1,000 yuan or 10% and 9.09% compared to the previous generation.

While the absolute price increase is the same, the Magic V6's higher base price "dilutes" the 1,000 yuan increase into a single-digit percentage rise, making consumers far less sensitive to the price change than they would be with mid-range or low-end phones.

03

Behind the 'Niche' Status, Foldables Serve as a 'Testing Ground' for New Technologies

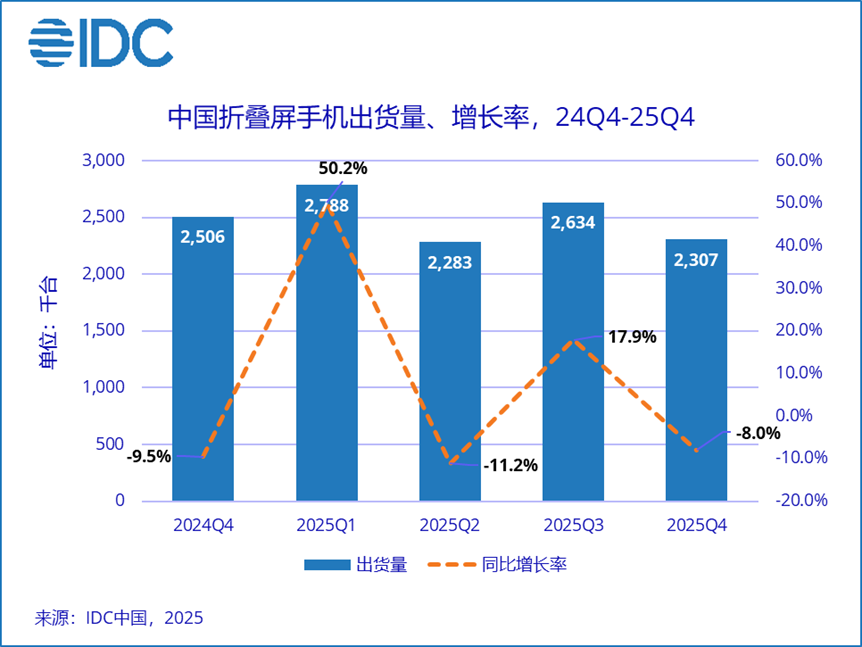

Over the past few years, China's foldable phone market has grown in scale, but due to high selling prices, the segment's shipment growth rate has been declining. IDC data shows that from 2022 to 2025, year-on-year shipment growth rates for foldable phones in China were 118%, 114.5%, 30.8%, and 9.2%, respectively.

Image Source: IDC

As major manufacturers ramp up their foldable product lines, Sigmaintell predicts that in 2026, foldable phone shipments in China will reach 12-13 million units, up 20-30% year-on-year, showing renewed growth momentum. However, compared to the triple-digit growth rates of the early days, overall growth momentum has clearly slowed.

Compared to the overall smartphone market, the market share of foldable phones remains quite limited. According to IDC data, China's foldable phone shipments will reach 10.01 million units in 2025, accounting for just 3.52% of the total smartphone market.

However, it is important to note that the limited market influence of foldable phones does not mean that the efforts of smartphone manufacturers have become a "niche game." On the contrary, the technological "spillover" effects demonstrated by foldable phones are having a profound impact on the advancement of the smartphone industry.

Image Source: OPPO

Due to the higher engineering complexity of foldable phones, smartphone manufacturers have invested heavily in R&D over the past few years to create products with a comprehensive experience that rivals traditional bar-shaped phones. For example, on March 11, Liu Zuohu revealed that since 2018, OPPO has invested over RMB 3 billion in R&D for foldable phones, with its number of related patents ranking among the top 3 globally.

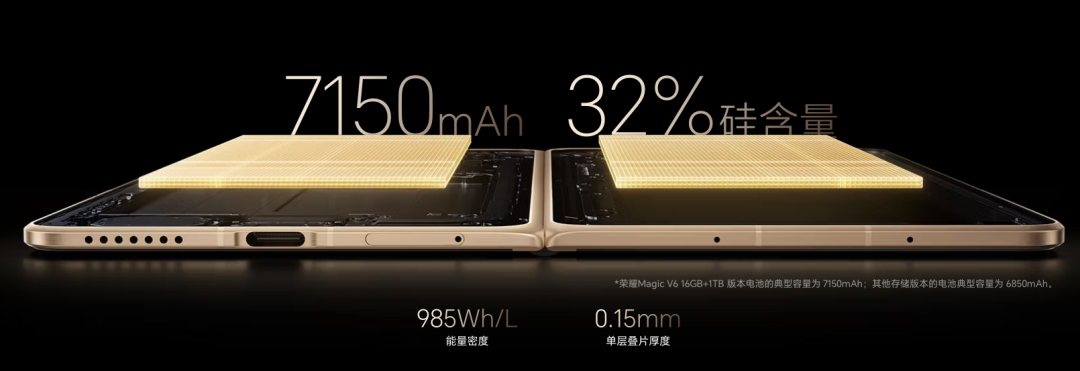

From a product perspective, as foldable phones mature, they are increasingly "feeding back" into traditional bar-shaped phones. Taking Honor as an example, to enhance the battery life of its foldable phones, it has actively developed Qinghai Lake batteries since 2023, aiming to improve anode energy density through the high gravimetric capacity characteristics of silicon materials.

Image Source: Honor

The Honor Magic V, launched in January 2022, was equipped with a 4,750mAh battery. Four years later, the Honor Magic V6 (16GB+1TB version) debuted with a new Qinghai Lake blade battery, featuring a silicon content increased to 32%, a single-layer stack thickness of just 0.15mm, an energy density of 985Wh/L, and a capacity of up to 7,150mAh.

Driven by the Magic V series, products such as the Honor 500, X60, and MagicPad 3 Pro have all adopted Qinghai Lake batteries. Honor has even created a dedicated "power bank" phone, the Honor Power2. Official data shows that the Honor Power2 is equipped with a 10,080mAh Qinghai Lake battery, capable of continuous screen-on usage for 20.3 hours.

Exploring the technological direction of making foldable phones thinner and lighter, the smartphone industry has also seen the emergence of ultra-thin products such as the Huawei Mate 70 Air, Honor Magic8 Pro Air, and iPhone Air.

Image Source: Apple

Although Apple's foldable product has not yet been launched, the iPhone Air is seen as a technological preview of a foldable iPhone. The product's explorations in ultra-thin design, internal structure optimization, and eSIM technology are largely paving the way for the future iPhone Fold.

In summary, the collective focus of smartphone manufacturers on foldable phones in 2026 is not a blind competition but an inevitable result triggered by changes in the market environment. Faced with the dual pressures of market downturns and rising costs, manufacturers naturally need to allocate more resources to the emerging high-end segment of foldable phones to escape internal competition and open up growth opportunities.

It is undeniable that, limited by price and form factor, foldable phones are unlikely to quickly become mainstream products. However, from an industry evolution perspective, the technological "spillover" value of these products cannot be ignored. Whether it is ultra-thin structural design, hinge technology, or key technologies such as batteries and screen materials, they often debut on foldable phones before gradually trickling down to mainstream bar-shaped phones, thereby elevating the overall smartphone experience to new heights.

Looking back on the smartphone industry in 2026 years later, the role of foldable phones may not only be as a high-end product line but also as a crucial "safe haven." Amid industry cycle fluctuations caused by rising memory prices, they provide manufacturers with new growth opportunities and buy valuable buffer space for the smartphone industry to navigate through downturns.

-

![]()

ByteDance, DJI, and Xiaohongshu Secure Top Three Positions Among China’s Fastest-Growing Unicorns

-

Tesla's in-car voice system in China is finally learning to 'understand human language'

-

![]()

Foreigners Are Amazed: Chinese Electric Vehicle Drive Systems Unveil Innovative 'Poses'

-

![]()

700,000 Brothers and the Future of Robots: Behind JD.com's 'Nirvana Plan'

-

![]()

Zhipu's Trillion-Dollar Valuation: A New Chapter for China's AI

-

![]()

Is Laifen, a 'Dyson Alternative' on the Rise, Now Ensnared by the 'Alternative Curse'?

-

![]()

Beyond Patents: Insta360 and DJI Compete in Retail

-

![]()

Piercing Through Industry Chaos: The Curtain Rises on Compliance for Autonomous Driving