Direct Satellite Connection to Smartphones: Despite Its Infancy, It Shows Promising Growth

04/28 2026

04/28 2026

616

616

Recently, analysts from Ookla, a renowned network testing and data analysis firm, published an article highlighting that while D2D (Device-to-Device) satellite terminals are still in their nascent stages of development, they have already exhibited steady growth. D2D is swiftly transitioning from experimental validation to large-scale commercial deployment, bolstering support for a broader range of terminal connections and diverse scenarios, poised to become a standard feature in mobile communications.

D2D: Paving the Way for Large-Scale Development

D2D technology facilitates direct connections between satellites and smartphones. Given the immense distance—thousands of kilometers—between satellites and Earth, coupled with their high-speed orbits, achieving stable communication poses significant challenges. In contrast, traditional mobile signal base stations are stationary and located just a few hundred meters to kilometers away from mobile users.

Over the past few years, leading industry players have been propelling the D2D market forward. Apple pioneered this market by leveraging Globalstar's satellites and spectrum, introducing satellite communication capabilities for the iPhone 14 in 2022. This innovation enabled every iPhone 14 to send and receive text messages via satellites.

Apple is not alone in this endeavor; SpaceX's Starlink Mobile, Skylo, and other providers have also announced the launch of commercial D2D services in select countries worldwide. This month, Amazon revealed its acquisition of Globalstar as part of its Amazon Leo satellite internet project, aiming to offer D2D services to global mobile network operators. Although most of these services currently support text messaging and lightweight data services, D2D network performance is expected to continually improve as providers deploy more satellites and expand spectrum resources.

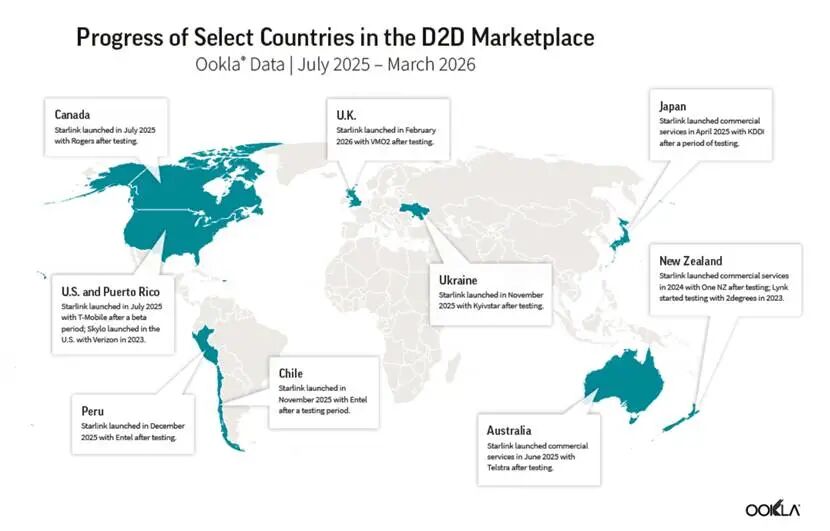

As a leading testing provider, Ookla has extensively utilized its testing tools. By analyzing data from Android smartphones and satellite registration data from Starlink, Skylo, and Lynk, Ookla has mapped out the progress of the D2D market. For instance, D2D connections from July 2025 to March 2026 are illustrated as follows:

Ookla's data reveals a 24.5% increase in global D2D connections following the launch of Starlink's D2D services in multiple countries, despite still relatively low monthly usage. The United States leads in connection numbers, accounting for 45.9% of global users, followed by Australia at 18.1%, Chile at 10%, and Canada at 9.8%. Notably, these countries all have significant rural, regional, or inland areas outside ground network coverage, making D2D services more practically valuable. Data indicates that independent D2D users in New Zealand, Chile, and Peru constitute over 1% of cellular users.

However, since D2D is still in its early commercial stages and costs remain high, users are highly price-sensitive. Data suggests that some users' willingness to pay for D2D services is diminishing. Ookla notes that despite overall global growth, D2D connection numbers in the United States and Canada have recently declined, likely due to T-Mobile in the U.S. and Rogers in Canada beginning to charge some users. Both T-Mobile and Rogers have ended their free trial periods, bundling Starlink D2D only into premium plans; other users must pay separately, with monthly fees around $10, and users of other carriers are charged at the same rate for the service.

The D2D market is undergoing dynamic changes. For example, AST SpaceMobile has committed to entering the field by launching 45 to 60 satellites by the end of 2026, most of which will offer data speeds of up to 120 Mbps. While it remains uncertain how these capabilities will impact the actual customer experience, AST SpaceMobile's partners, such as AT&T, have pledged to provide a comprehensive broadband connectivity suite, including voice, data, and text messaging.

Similarly, Amazon Leo has committed to deploying its own D2D satellite constellation by 2028 while retaining the Globalstar constellation for Apple. Amazon claims that the Leo D2D system will offer higher spectrum utilization and efficiency than traditional direct-to-cell systems, implying faster speeds and better performance.

Another satellite operator, Lynk, announced its merger with Omnispace in late 2025, combining its "space base station" technology with Omnispace's extensive satellite spectrum assets.

Meanwhile, SpaceX's Starlink Mobile has announced plans to launch second-generation D2D satellites, with a constellation size double that of the current D2D constellation. These new D2D satellites will support spectrum purchased by SpaceX from EchoStar and feature improved antennas and other technologies. Starlink states that this will "enable full 5G cellular connectivity, with an experience comparable to existing terrestrial services." Of course, the launch of Starlink's V2 D2D satellite constellation depends on SpaceX's larger Starship rocket, which is still undergoing testing.

The Mobile Communications Ecosystem: Fueling Further D2D Adoption

Currently, the D2D market remains relatively small. According to a February report by the Global Mobile Suppliers Association (GSA), D2D services are already operational in 15 countries. Presently, 61 countries and regions are planning, evaluating, testing, or have launched satellite-to-smartphone partnerships. According to GSA statistics, Starlink leads in this area with 59 partnerships, followed by AST SpaceMobile with 28.

The GSA report does not encompass the Chinese market, where D2D has also made significant strides. China Unicom and China Telecom have obtained licenses to provide point-to-point services via the Tiantong satellite system. Meanwhile, China Mobile, leveraging the Beidou satellite system, plans to integrate with emerging satellite constellations to further expand its point-to-point capabilities.

The expansion of D2D technology coverage holds significant implications for cellular network operators, particularly those seeking to understand customer behavior outside traditional terrestrial network coverage. AT&T has suggested that the widespread adoption of satellite-driven broadband connectivity could alleviate the need for additional base stations in rural areas, potentially impacting the long-term business of base station operators. Starlink has committed that its V2 constellation for D2D services will enable mobile network operators to "reduce investment in terrestrial networks while achieving seamless service in remote areas." Ultimately, a cost-benefit analysis may determine whether it is more cost-effective to build base stations or rely on D2D service providers to cover rural and outdoor areas.

However, the existing mobile communications ecosystem is not merely being disrupted by satellite communications; instead, it is actively embracing satellite communications, which, to a certain extent, will become a core force driving the development of satellite communications, particularly the widespread adoption of D2D.

Market research firm Omdia recently released the "Smartphone Satellite Direct Connection Market Forecast" report, providing insights into the global development of smartphone satellite direct connection services. The report projects that by 2030, the number of global monthly active D2D users will reach 411 million, with related revenue reaching $11.99 billion. Between 2026 and 2030, the compound annual growth rates for users and revenue in this field are expected to reach as high as 80.1% and 49.4%, respectively, demonstrating robust development momentum.

Omdia predicts that satellite direct connections to smartphones based on cellular network standards (4G/5G) will dominate the market. By 2030, such devices will account for over 95% of the total global monthly active users. Their core advantage lies in eliminating the need for dedicated terminal devices, allowing users to access satellite communication networks directly through existing smartphones. This technological path is gaining widespread support across all segments of the industry chain.

Omdia experts believe that as satellite constellations expand and coverage continues to grow, more communication service providers will leverage satellite D2D capabilities to offer ubiquitous connectivity. In the future, direct satellite connection services for smartphones will become a common additional feature in mobile plans, providing coverage in areas lacking terrestrial networks. In the long term, satellite-based broadband will help operators improve network connectivity in rural areas and support universal service goals.

The role of the operator-led mobile communications ecosystem in satellite communications, particularly D2D, is concentrated in the advancement of the 3GPP's NTN (Non-Terrestrial Network) standards, which have become the technological foundation for the entire D2D industry. 3GPP Release 17 incorporated satellites and high-altitude platforms into the 5G standard system for the first time, providing core technical specifications for ground devices to connect directly to satellites. Currently, 3GPP NR-NTN (5G devices connecting to the 5G core network via satellites) has evolved from a conceptual technology into a mature, commercially viable solution.

Looking ahead, 6G will become the first mobile communication system to natively integrate NTN technology. The industry consensus is that D2D will not replace terrestrial communications but will serve as a "sky extension layer" for mobile communications, providing on-demand services to all mobile users.

-

![]()

ByteDance, DJI, and Xiaohongshu Secure Top Three Positions Among China’s Fastest-Growing Unicorns

-

Tesla's in-car voice system in China is finally learning to 'understand human language'

-

![]()

Foreigners Are Amazed: Chinese Electric Vehicle Drive Systems Unveil Innovative 'Poses'

-

![]()

700,000 Brothers and the Future of Robots: Behind JD.com's 'Nirvana Plan'

-

![]()

Zhipu's Trillion-Dollar Valuation: A New Chapter for China's AI

-

![]()

Is Laifen, a 'Dyson Alternative' on the Rise, Now Ensnared by the 'Alternative Curse'?

-

![]()

Beyond Patents: Insta360 and DJI Compete in Retail

-

![]()

Piercing Through Industry Chaos: The Curtain Rises on Compliance for Autonomous Driving