Insightful Analysis on Cars: New Energy Penetration Rate Expected to Exceed 60% in October

11/04 2025

11/04 2025

611

611

TEAM

Layout: Chen Yujie

Image: Sourced from the internet; removal upon receipt of an infringement claim.

Produced by: Qiancheng Shuzhi (Performance Marketing Intelligence Agency)

Introduction

Several brands have achieved record-breaking sales, with the leading effect in the automotive market becoming highly pronounced.

What does it signify when the new energy retail penetration rate in China's October automotive market approaches the 60% mark?

According to data from the China Passenger Car Association, the retail sales volume of narrowly defined passenger cars in October is estimated to be around 2.2 million units. Despite a slight 2% month-on-month decline, new energy retail sales are expected to surge to 1.32 million units, with the penetration rate potentially breaking through the 60% barrier for the first time, setting a new benchmark.

The primary driving force behind this rapid surge remains the impending 'Sword of Damocles' – the clear expectation of a phase-out of new energy vehicle purchase tax subsidies by 2026. This has not only sparked a 'last-chance' buying spree among consumers but also signaled the countdown for automakers to give it their all. Over a dozen automakers, including Xiaomi, NIO, Zeekr, Changan, and Lynk & Co, have successively launched cross-year purchase tax subsidy guarantees, with the main objective of securing orders in advance and avoiding a potential 'demand cliff' after the policy phase-out.

This 'Silver October' performance report not only marks the completion of the market leadership transition but also reveals that the industry is grappling with the dilemma of 'rising sales but declining profits.' As the penetration rate nears 60%, the pressing issue for China's automotive market has shifted from 'whether we can sell cars' to 'whether we can maintain profitability in a competitive consumption environment.'

Conglomerates: Achieving 'Elephant-like Agility' Through Systemic Strength

Under clear policy expectations and survival pressures, conglomerates have demonstrated what it means to 'dominate with systems.' With their massive scale, comprehensive resources, and rapid transformation speed, they prove that large entities can not only pivot but also accelerate.

'New Energy Transformation' and 'Globalization' are precisely the two engines propelling these giants forward.

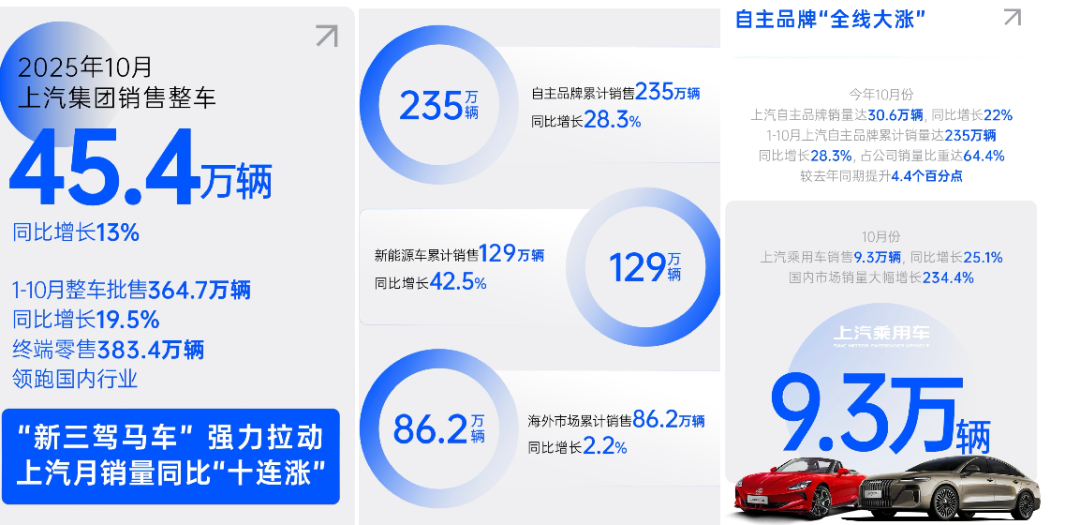

SAIC Motor maintained its industry-leading position with 454,000 units sold, achieving 'ten consecutive months of growth' in monthly sales. Its growth foundation has successfully expanded from past joint venture strongholds to three new fronts: self-owned brands, new energy, and overseas markets. From January to October, SAIC's self-owned brand sales accounted for over 60%, reaching 2.35 million units; new energy vehicles totaled 1.29 million units, with overseas contributions at 862,000 units.

BYD set a new annual record with 441,700 units sold, continuously deepening its market dominance. More importantly, it has shifted its growth engines: overseas sales reached 83,524 units in October, soaring 155.5% year-on-year, marking its successful establishment of a 'domestic + overseas' dual-drive model.

Geely Auto surpassed the 300,000-unit monthly sales mark for the first time, with its multi-brand strategy yielding significant results. The Geely Galaxy brand achieved its 'annual sales of one million' target in just 10 months with 127,476 units sold, becoming the cornerstone in the mass market. Meanwhile, Zeekr (21,423 units) and Lynk & Co (40,213 units) have taken up the mantles of high-end pure electric and global advancement, respectively. Notably, the current annual sales target achievement rate has reached 83%, making the 3 million-unit target virtually attainable.

Chery Group's 281,000 units sold represent a classic example of 'boosting domestic sales through overseas expansion' – with exports accounting for a substantial 45% (126,000 units). This deep 'overseas' moat provides it with more leeway in the fierce domestic market competition.

BAIC Group sold 160,000 complete vehicles in October. Its BAIC New Energy (Arcfox/Xiangjie) achieved a remarkable '10,000+ in August, 20,000+ in September, 30,000+ in October' triple jump. Among them, the Xiangjie S9, in collaboration with Huawei, has firmly established itself in the luxury market above 300,000 yuan. This indicates that the empowerment of tech giants is a shortcut for traditional automakers to achieve brand elevation, but the depth and sustainability of their cooperation remain long-term questions they need to address.

Great Wall Motor, based on 143,000 units sold, achieved 57,158 units in overseas sales, growing in tandem with new energy sales. Its unique 'boxy' product series (Haval Menglong/Tank, etc.) not only contributed 46% of sales but also became its distinctive business card for global market impact.

The Transformation of Traditional Central State-Owned Enterprises: Seeking a New Balance Between 'Stability' and 'Progress'

FAW Group sold 305,000 complete vehicles in October, with the Hongqi brand exceeding 45,000 units sold in a single month and new energy product sales growing 66.3% year-on-year. Meanwhile, FAW-Volkswagen just reached the milestone of the 30 millionth vehicle produced, and FAW Toyota's products are also accelerating their refresh, demonstrating the product resilience of the joint venture sector.

Changan Auto's total sales volume of 278,000 units included 119,000 new energy units. The matrix formed by the Shenlan, Avita, and Qiyuan brands has achieved precise positioning in different market segments.

Dongfeng Group adopted more flexible organizational and product strategies to open up new opportunities. E-π Tech achieved 31,107 units sold in October, and Voyah delivered 17,218 units, jointly becoming important pillars for the group's electrification transformation.

New Forces: From Survival Races to Positioning Battles

As conglomerates fully leverage their systemic strength, the internal dynamics of the new force camp are also quietly evolving. The market landscape has shifted from a 'who can survive' survival race to a 'who can secure a top-tier position' positioning battle, with the competitive dimension upgrading from a single product strength to a comprehensive system capability contest involving brand, scale, technology, and operations.

Among the leading camp, Leapmotor and HiMo have taken two distinct yet equally successful paths.

Leapmotor continued to lead the new force camp with 70,289 units delivered, its core weapon being extreme cost control capabilities brought by full-domain self-research, successfully penetrating the most mainstream consumer market and earning the title of 'Volkswagen of the electric vehicle world.' Meanwhile, HiMo delivered 68,216 units across its entire lineup, setting a new record for the 'fastest one million deliveries' among new forces while achieving an average transaction price as high as 390,000 yuan, a price band even surpassing traditional luxury brands BBA. Strong tech brand empowerment has proven capable of rapidly scaling high-end models in the Chinese market.

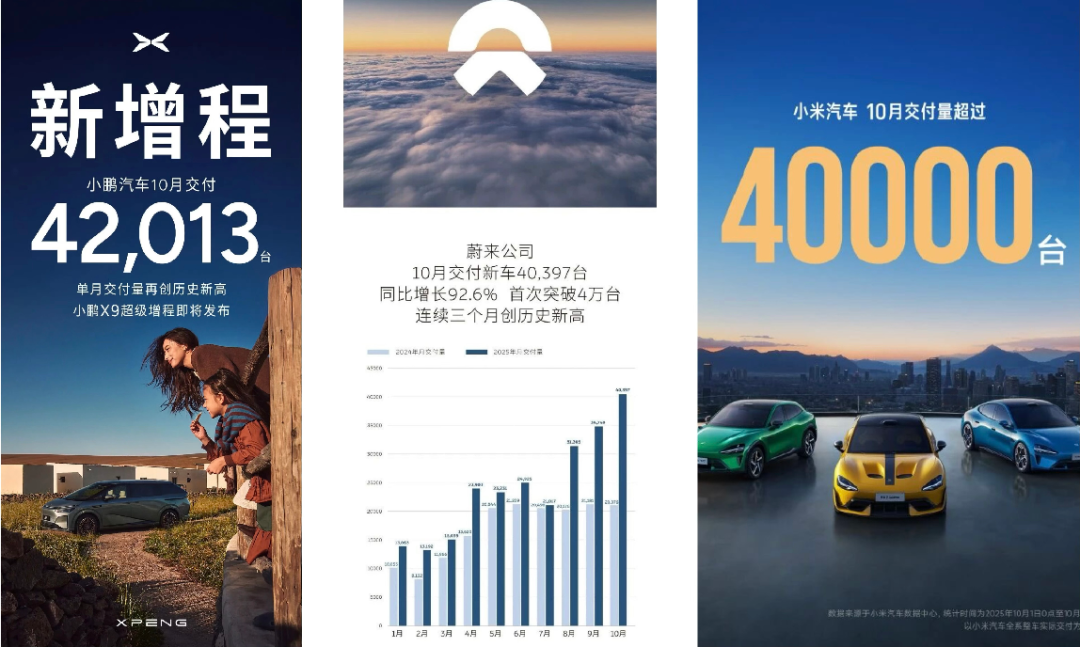

In the chasing camp, XPeng, NIO, and Xiaomi have all surpassed the 40,000-unit threshold but face different challenges.

XPeng's 42,013 units reflect the stability of its tech label (intelligent driving), but it faces direct competition from tech companies like Huawei and Xiaomi. NIO broke through the 40,000-unit mark for the first time, with the largest contributor being the 17,342 units delivered by the Ledo brand, marking the initial success of its multi-brand strategy and opening the channel to the mass market. Meanwhile, Xiaomi, while maintaining a momentum of over 40,000 units, is simultaneously experiencing the 'heat' of production capacity ramp-up and the 'chill' of public opinion controversies.

In contrast, Li Auto's 31,767 units and its month-on-month decline highlight the growing pains of its transition from a range-extended leader to a pure electric track. Li Auto i6's over 70,000 orders are undoubtedly a strong boost, but the most urgent task now is to convert these orders into actual deliveries and repair the damaged brand image after the MEGA controversy.

Sharp Car Talk

The October sales rankings are not just a performance report but also a map of power distribution in the future market.

Conglomerates, leveraging their systemic advantages and global layouts, have regained the right to define the game rules. New forces are seeking their survival philosophies within the ranks. All players, driven by both policies and markets, are making their final sprint for the upcoming fully marketized competition.

Scale, brand, technology, and globalization – the key exam points for victory are clear. A Chinese automotive market thoroughly dominated by new energy has arrived, and its main theme is shifting from previous collective sprints to a prolonged consumption war that tests endurance and comprehensive strength.

-

![]()

ByteDance, DJI, and Xiaohongshu Secure Top Three Positions Among China’s Fastest-Growing Unicorns

-

Tesla's in-car voice system in China is finally learning to 'understand human language'

-

![]()

Foreigners Are Amazed: Chinese Electric Vehicle Drive Systems Unveil Innovative 'Poses'

-

![]()

700,000 Brothers and the Future of Robots: Behind JD.com's 'Nirvana Plan'

-

![]()

Zhipu's Trillion-Dollar Valuation: A New Chapter for China's AI

-

![]()

Is Laifen, a 'Dyson Alternative' on the Rise, Now Ensnared by the 'Alternative Curse'?

-

![]()

Beyond Patents: Insta360 and DJI Compete in Retail

-

![]()

Piercing Through Industry Chaos: The Curtain Rises on Compliance for Autonomous Driving