Is the EU in a State of 'Panic' Over Chinese Automobiles?

12/19 2025

12/19 2025

586

586

Are Chinese Automobiles Making a Significant Impact in Europe?

EU Reverses Policy on Banning Sales of New Fuel-Powered Vehicles

Chinese automobiles are no longer peripheral players in the European market; they have firmly established themselves in the mainstream competitive landscape, compelling the EU to make substantial adjustments to its automotive industry policies.

According to reports from foreign media, by the end of this year, the volume of vehicles imported by the EU from China is projected to surpass its exports to China for the first time. For the EU, this signifies a trade 'deficit' in the China-EU automotive sector. For Europe, which has long stood at the pinnacle of the global automotive industry, boasting technological exports and trade surpluses, this shift is undeniably an 'industrial earthquake.'

Image Source: Official Website of the European Commission

Under mounting pressure, on December 16 (local time), the European Commission officially announced the withdrawal of its planned policy to entirely ban the sale of new fuel-powered vehicles starting in 2035, opting instead for a more adaptable emission reduction strategy. According to the new proposal, automakers are required to reduce the average CO2 emissions of new vehicles by 90% compared to the 2021 baseline by 2035.

Image Source: CheBaiHui Research Institute

Data from the CheBaiHui Research Institute indicates that Europe has emerged as China's primary export market for automobiles. 'The European automotive industry cannot thrive without the Chinese automotive sector, particularly in the era of intelligence,' stated Zhang Yongwei, Chairman of CheBaiHui, in an interview with China Newsweek. 'Automobiles are a cornerstone of Europe's economy. During the globalization of Chinese automobiles, it is imperative to achieve a mutually beneficial outcome with the EU. In the realms of electrification and intelligence, the EU has demonstrated a strong willingness to collaborate, and we should seize this opportunity.'

China-EU Automobiles: The Transition from Offensive to Defensive

As the birthplace of the automotive industry, Europe has traditionally been an exporter of automotive products and technologies, supplying advanced goods and know-how worldwide and maintaining a trade 'surplus.'

Just three years ago, in 2022, Europe still enjoyed a €15 billion surplus in automotive exports to China. However, by 2025, the tables have turned. Foreign media reported that the China-EU automotive trade would experience a trade deficit for the first time in 2025, with EU automotive imports to China expected to exceed exports by €2.3 billion (approximately RMB 19.09 billion).

Behind these figures lies a reshuffling of the global automotive industry amidst the new energy revolution. While European traditional automotive giants continue to refine internal combustion engine technologies and hesitate in transitioning to new energy, Chinese automakers have keenly seized historical opportunities. With policy support, capital investment, technological innovation, and market cultivation, the Chinese new energy vehicle industry has achieved remarkable development.

The choice of Laurent Combette, a senior executive at a French electronics company, is highly illustrative. He opted for BYD, a Chinese brand, for his new company vehicle, stating, 'I cannot find a comparable model at the same price point.' He added, 'This BYD plug-in hybrid model has a range of 870 kilometers and is priced at €44,500. In terms of both appearance and range, it is more competitive in its class.'

Zhang Yongwei directly pointed out that accurately understanding the needs of young consumer groups is one of the core strengths of Chinese automakers. 'Smart vehicles have not only won over young Chinese consumers but are also gaining traction among young Europeans, laying a solid market foundation for Chinese automobiles going global.'

The influence extends beyond complete vehicle exports. German automakers such as Volkswagen, BMW, and Mercedes-Benz are increasingly sourcing Chinese components or partnering with Chinese smart solution providers. The reasons are twofold: firstly, Chinese component companies have narrowed the quality gap with German enterprises through industrial upgrading; secondly, the intelligent and electrified solutions from Chinese companies offer technological and cost advantages that are hard for European automakers to ignore.

From complete vehicles to components, the Chinese automotive industry is making significant inroads into the European market.

EU Policy Shift

The EU's substantial adjustment to its automotive emission reduction policy was not made on a whim. Tracing the evolution of the policy, it is evident to see the struggles and compromises of the European automotive industry.

In 2021, the European Commission initially proposed the radical goal of entirely banning the sale of new fuel-powered vehicles by 2035, attempting to use policy to drive the automotive industry towards electrification, causing a global stir in the automotive sector. In February 2023, the European Parliament passed the zero-emission agreement with 340 votes in favor, 279 against, and 21 abstentions, clarifying that new vehicles sold in 2035 must achieve zero emissions. In March of the same year, under pressure from traditional automotive powerhouses like Germany and Italy, the EU made its first compromise by passing an amendment to create an exemption for internal combustion engine vehicles using synthetic fuels.

Now, the latest proposal announced by the European Commission is far more lenient than market expectations: unlike the previous rule that only exempted synthetic fuel vehicles, this time the core requirement has been relaxed from '100% zero emissions' to 'reducing new vehicle emissions by 90% compared to the 2021 baseline.' The remaining 10% emission gap can be offset by using low-carbon steel produced in the EU, synthetic fuels, or non-food biofuels. This means that plug-in hybrids, extended-range hybrids, hybrid electric vehicles, and even traditional fuel-powered vehicles can remain in the market after 2035 through various emission reduction measures, effectively abandoning the ban on fuel engine technologies.

In fact, European automakers such as Volkswagen Group and Stellantis have previously expressed concerns about weak demand for electric vehicles. They have called on the EU to relax carbon emission targets and reduce fines for automakers that fail to meet them. The European Automobile Manufacturers Association has described the current moment as a 'critical juncture' for the European automotive industry.

William Todts, Executive Director of the clean transport advocacy group Transport & Environment (T&E), stated that the EU is delaying while China is accelerating: 'Relying on internal combustion engines will not restore European automakers to greatness.'

Breaking the Deadlock and Achieving Win-Win Collaboration

Faced with the strong rise of Chinese automobile brands in the European market, European local companies are intensifying their defensive measures to maintain market positions.

Recently, French automaker Renault and American automotive giant Ford announced plans to jointly develop mid-to-low-end electric vehicles for the European market, aiming to reduce development costs. Meanwhile, the French Automotive Suppliers Industry Liaison Committee (CLIFA) has publicly called for higher-threshold localization policies, proposing stringent standards such as increasing the localization rate of complete vehicles to 80% and the local content of components to no less than 70%, aiming to weaken the market competitiveness of Chinese automobiles through policy barriers.

Europe has stringent global requirements for data protection, particularly the GDPR (General Data Protection Regulation). Additionally, regulations on cybersecurity (such as the NIS2 Directive) and future potential AI legislation (AI Act) impose specific requirements on connected vehicle data processing.

Zhang Yongwei revealed that leading domestic intelligent driving companies have launched multiple compliant solutions, 'neither sacrificing intelligent driving functionality nor failing to meet standards due to compliance issues. I believe this is a gradual process. However, it is not an insurmountable obstacle.'

It is worth noting that the EU's Carbon Border Adjustment Mechanism (CBAM) will officially take effect in 2026. At that time, vehicles exported to the EU will need to fully declare lifecycle carbon emission data, and from 2030, taxes will be levied based on emission levels. Based on the 2024 export scale, annual taxes could exceed RMB 370 billion.

Changes in the industrial environment are also intensifying competitive pressures. With the global demand for energy storage batteries recovering, battery prices may rebound in 2026, posing a significant constraint on profit growth for new energy vehicle companies highly dependent on battery cost advantages.

Additionally, brand and service shortcomings remain one of the factors restricting the global expansion of some Chinese automobiles. Currently, some automakers are still stuck in the stage of 'trading price for volume' in product exports, with insufficient overseas after-sales service network coverage and lagging localization of service systems. Brand recognition and premium pricing capabilities still lag behind those of traditional European automakers. The transition from 'cost-effectiveness exports' to 'technology and brand value exports' still requires lengthy market cultivation and reputation accumulation.

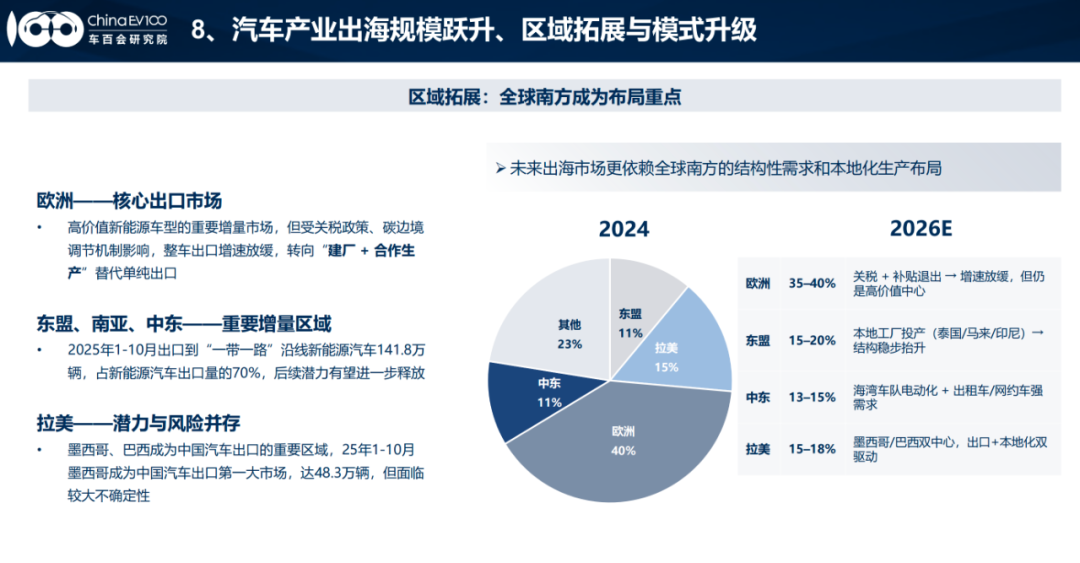

Data from the CheBaiHui Research Institute shows that Europe is an important incremental market for high-value new energy vehicle models. However, affected by tariff policies and the carbon border adjustment mechanism, the growth rate of complete vehicle exports has slowed, shifting toward 'factory construction + cooperative production' as an alternative to pure exports.

Zhang Yongwei believes that the automotive industry is a pillar of the EU, relating to employment, livelihoods, and economic foundations. In his view, on the one hand, we should continue to export more electric and intelligent products to the European market to meet local consumers' demand for high-quality new energy vehicles; on the other hand, it is even more crucial to consider how to achieve mutual benefit and win-win collaboration between the Chinese and European automotive industries in the context of globalization.

Image Source: CheBaiHui Research Institute

Despite numerous challenges, the industry still has sufficient long-term growth confidence. Zhang Yongwei predicts that in the future, China's automobile export volume is expected to exceed 10 million units, with new energy vehicles dominating. Those automakers that can maintain a firm footing in their domestic market positions while building technological, brand, and service barriers in global competition will ultimately stand firm and achieve sustainable development in this wave of global automotive industry transformation.

-

![]()

Enflame Tech's IPO Journey: Navigating Over 5.9 Billion Yuan in Losses and Soaring Debt in Q1 This Year

-

![]()

Trillion-Yuan Giant Li Shufu 'Streamlines': Could Levc Be the Casualty?

-

![]()

AI Competes for Electricity and Generates Power in the Gobi Desert

-

![]()

The First Batch of Victims of the AI Bubble: Programmers

-

![]()

ByteDance, DJI, and Xiaohongshu Secure Top Three Positions Among China’s Fastest-Growing Unicorns

-

Tesla's in-car voice system in China is finally learning to 'understand human language'

-

![]()

Foreigners Are Amazed: Chinese Electric Vehicle Drive Systems Unveil Innovative 'Poses'

-

![]()

700,000 Brothers and the Future of Robots: Behind JD.com's 'Nirvana Plan'