The 2026 Auto Market: Headed for a Downturn?丨Outlook and Trends ①

02/25 2026

02/25 2026

645

645

Lead-in

Introduction

The Chinese auto market in 2026 is poised for a survival battle, characterized by an inevitable decline!

This article is an excerpt from 'Outlook and Trends 2026': In mature markets such as the US, Europe, and Japan, fluctuations in car sales are commonplace. Only in China is there a strong reluctance to accept the notion of decline—official forecasts often lean towards optimism, as if acknowledging a downturn would undermine the industry's development. However, the market trends in 2026 are brutally dismantling this 'avoidance of decline' mindset.

On January 3, 2026, The Wall Street Journal featured a front-page headline, 'Tesla Overtaken by BYD,' drawing global attention to the Chinese automotive market. Yet, a more in-depth article on BYD on page B9 that same day unveiled a harsher reality: the Chinese auto market in 2026 is destined for a survival battle, marked by an inevitable decline!

Both domestic official institutions and foreign authoritative research organizations have laid a solid foundation for the possibility of a market downturn in 2026. The most optimistic forecast from the China Passenger Car Association (CPCA) cautiously projects a mere 1% growth for the auto market in 2026, while the most pessimistic prediction suggests a 7% decline. The majority of forecasts indicate a negative growth range, with declines between 3% and 5%.

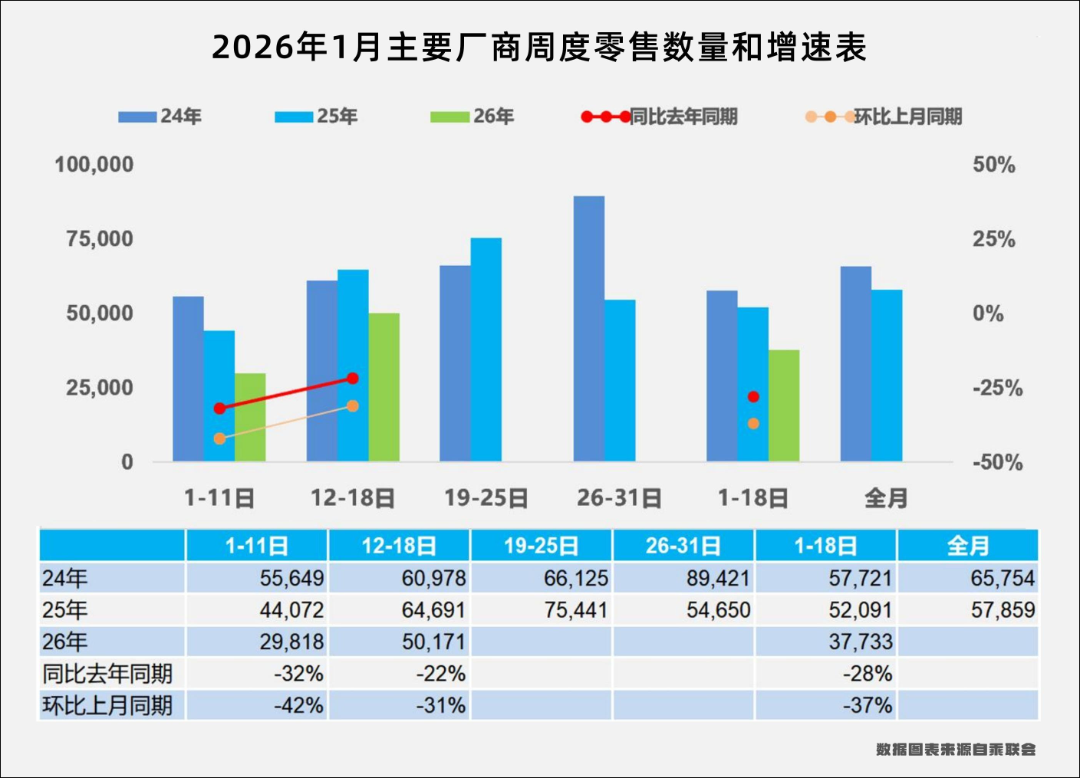

January's data strongly supports this consensus: from January 1-18, retail sales of passenger vehicles nationwide reached 679,000 units, a 28% year-on-year decrease compared to the same period last January and a 37% month-on-month decline. The rollback of policies has been described by some as 'the failure of the last painkiller.' Two key subsidy policy adjustments are impacting this year's auto market: the New Energy Vehicle (NEV) purchase tax exemption has been reduced to a 50% reduction; and the trade-in subsidy has shifted from a fixed amount to a percentage of the vehicle price, with a cap.

This means that NEV models priced below 100,000 yuan, which benefited the most last year, will face significant impacts. Conversely, NEV models in the 150,000-200,000 yuan price range, benefiting from the 50% purchase tax reduction and trade-in subsidies, will emerge as the biggest winners under the new policies in 2026. The policy shift is eroding the fundamental logic that has fueled two consecutive years of rapid growth in the Chinese auto market.

To compound the issue, in 2026, weak consumer confidence, coupled with significant asset depreciation, has led to a shrinking middle class. From 2024 to 2025, the income curve for this group began to decline, with housing market depreciation and investment setbacks halving car-buying budgets. Families that once had budgets ranging from 200,000 to 500,000 yuan have been forced to downgrade their consumption.

Consequently, the most pessimistic forecasts come from research institutions with foreign ties. Morgan Stanley predicts a 5% decline in domestic wholesale auto sales in 2026, with domestic retail sales potentially shrinking by as much as 7%. The most concerning aspect is that after the start of the year, traditionally a peak season for auto sales, Morgan Stanley analysts expect sales to plummet by 30-35% quarter-on-quarter, far exceeding the market's general expectation of 20-25%. The primary reasons are the premature withdrawal of local subsidies, which has suppressed consumer demand, and manufacturers' reluctance to provide their own subsidies to offset the potential increase in purchase taxes in 2026.

Domestic institutions' forecasts remain relatively optimistic, as always. The CPCA predicts that domestic passenger vehicle retail sales will reach approximately 24 million units in 2026, a 1% year-on-year increase; NEV retail sales will reach about 14.6 million units, a 13% increase, with a penetration rate of 61%. The China Association of Automobile Manufacturers (CAAM) released a forecast on January 14, projecting total auto sales of 34.75 million units this year, a slight 1% year-on-year increase, including 30.25 million passenger vehicles (including exports), a slight 0.5% year-on-year increase.

Auto Magazine is not entirely pessimistic about the overall market: Given domestic consumption trends, passenger vehicles may remain relatively weak, but commercial vehicles are expected to continue the growth seen in the fourth quarter of last year, with overseas exports remaining a strong pillar for the Chinese auto industry.

Looking ahead to the 2026 auto market, three key phrases emerge: 'the first quarter determines the whole year,' 'slowing growth in penetration rate,' and 'joint ventures' major counterattack':

—Whoever can first stabilize after the significant decline in the first quarter will gain the advantage for the entire year;

—The growth rate of NEV penetration will slow due to subsidy rollbacks, declining oil prices, and setbacks in the low-priced pure electric market, marking the lowest growth in five years;

—Joint venture NEVs will enter the 2.0 era, with increased supply, and joint ventures will hit bottom in market share this year.

Auto Magazine forecasts: For the full year of 2026, domestic passenger vehicle retail sales will decline from last year's 23.74 million units to around 22.5-22.7 million units, a drop of about 5%; including commercial vehicles, domestic auto retail sales will decline from last year's 27.3 million units to 26-26.5 million units, a drop of 3%-4%; domestic NEV passenger vehicle retail sales will continue to grow from last year's 12.8 million units to 14.5-15 million units, up 12%-15% year-on-year. Auto exports are expected to grow from last year's 7.04 million units to around 8 million units in 2026, continuing to serve as a stabilizing force for Chinese autos!

The full-year sales trend in 2026 is expected to be low at the beginning, high in the middle, and flat at the end;

—The first quarter is expected to see a 20-25% decline, influenced by the subsidy rollback and the pace of local subsidy implementation. January is expected to see a 25% decline, February a 30% year-on-year decline due to the Spring Festival, with a gradual recovery starting in March;

—The second quarter will see a gradual market improvement and return to growth as promotional efforts intensify and new subsidy policies are implemented across regions;

—The third quarter will struggle to maintain high growth on last year's high base, with an expected modest growth of around 5%;

—The fourth quarter carries significant uncertainty, with a high probability of maintaining 0% growth.

Additionally, the NEV penetration rate for passenger vehicles will increase from 53.9% in 2025 to around 58% in 2026, with the previously rapid annual growth of around 8% slowing to below 5%. This year, controversial new regulations on intelligent driving, transformations in the automotive distribution sector, and industry consolidation led by leading companies, which emerged in 2025, will come to fruition in 2026.

——This article is excerpted from 'Outlook and Trends 2026'

Editor-in-Chief: Cao Jiadong Editor: He Zengrong

THE END

-

![]()

Depreciation Rate on Par with Mobile Phones: Just 40% Value Retention After Three Years—Why Do Battery Electric Vehicles Lose Their Worth?

-

![]()

Clearing Bugatti Stock Worth 7 Billion: Why is Porsche 'Cutting Ties'?

-

![]()

Don’t Dismiss Huawei’s Potential in Sedans Just Because the Shangjie Hasn’t Hit It Big Yet

-

![]()

Unsold Cars in China Find Success Overseas

-

![]()

Ghosn: Only I Can Save Nissan, Shareholders Beg Me to Return

-

![]()

Expanding Automobile Consumption: It's Time to Address the High Cost of Electric Vehicle Repairs

-

![]()

Luna Ultra Entangled in 'National Subsidy Fraud' Controversy, Insta360 Pushed to the Brink by DJI

-

![]()

People have long suffered from splash ads. Will the 'temporarily disappeared' traffic behemoth make a comeback?