Rivian: Farewell to the Era of Subsidies, Can the R2 Model Lead a Turnaround?

02/25 2026

02/25 2026

572

572

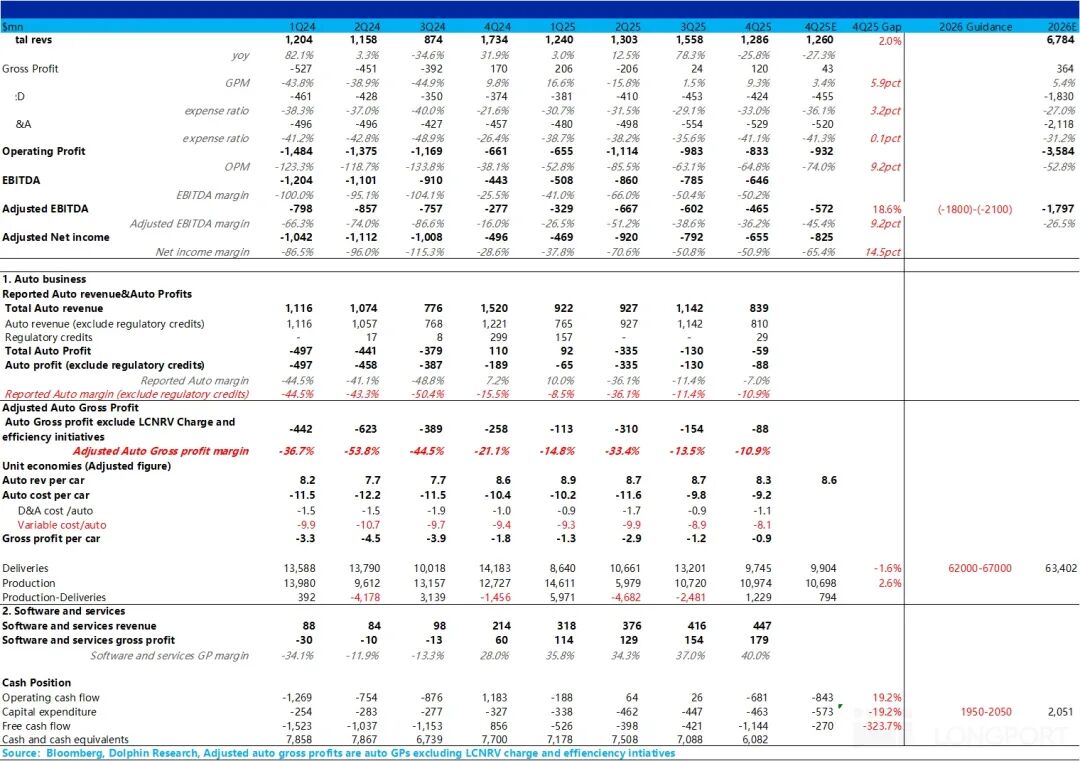

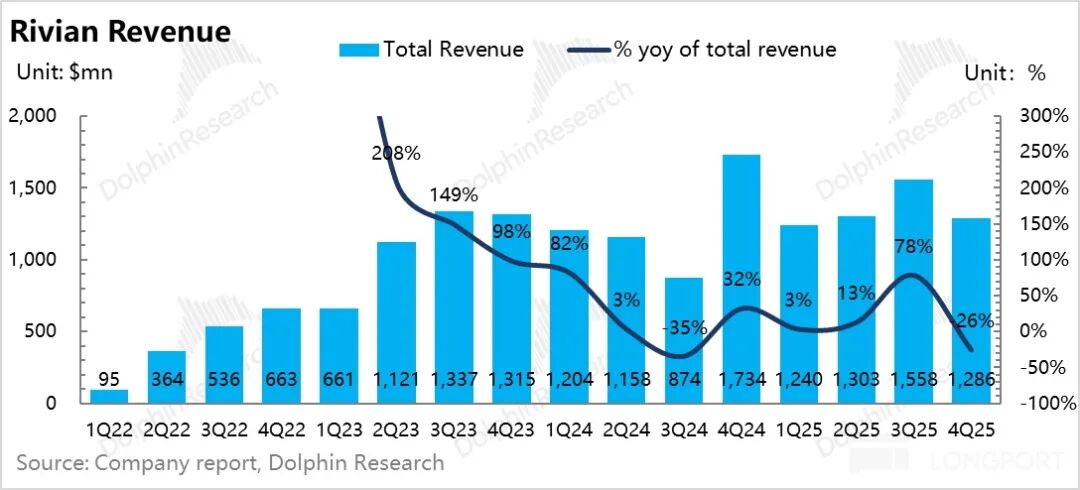

Revenue slightly exceeded expectations: Total revenue for the quarter was $1.29 billion, slightly higher than the market consensus of $1.26 billion, despite a slowdown in vehicle sales. Vehicle sales revenue (including carbon credits) was $840 million, down 26.5% QoQ, primarily due to the phase-out of IRA subsidies in Q4, which led to a 26% QoQ decline in sales volume to 9,700 units, and a $4,000 QoQ drop in average selling price (ASP) to $83,000, driven by a higher mix of lower-priced EDV models and increased promotional discounts.

Software and services revenue remained strong at $450 million, up $30 million QoQ, largely due to high-margin technology licensing revenue from the joint venture with Volkswagen.

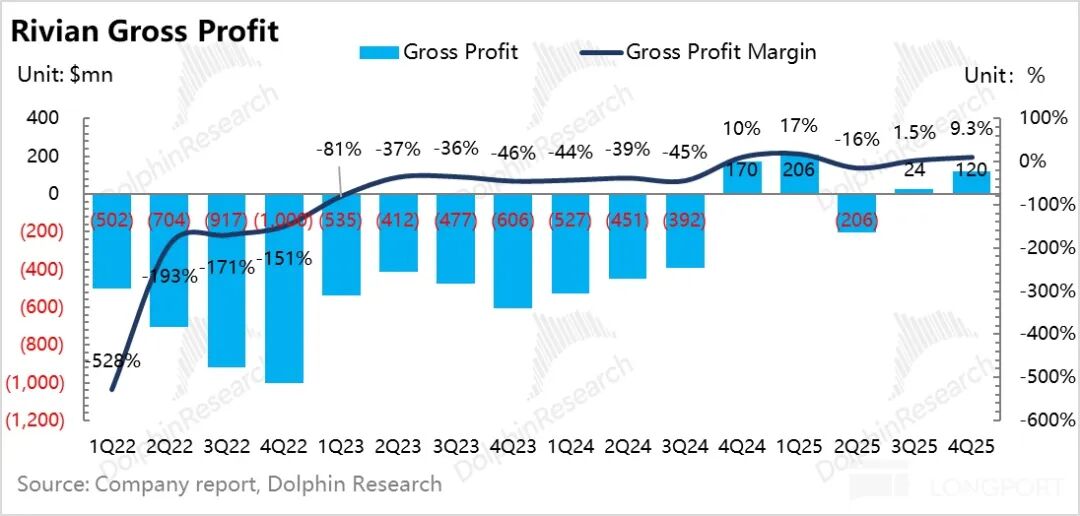

Gross margin continued to improve QoQ: More impressively, gross margin expanded by 7.8 percentage points QoQ to 9.3%, significantly exceeding market expectations of 3.4%. Both vehicle sales and services gross margins improved QoQ, with the services segment still benefiting from high-margin technology licensing revenue from the Volkswagen JV.

Vehicle gross margin continued to rise: Q4 vehicle gross margin was -7%, up 4.4 percentage points QoQ, or -11% excluding carbon credits, driven by lower per-unit variable costs (due to Rivian's ongoing cost reductions, weakened tariff impacts, and higher-margin EDV sales), offsetting the effects of lower ASPs and higher per-unit depreciation costs.

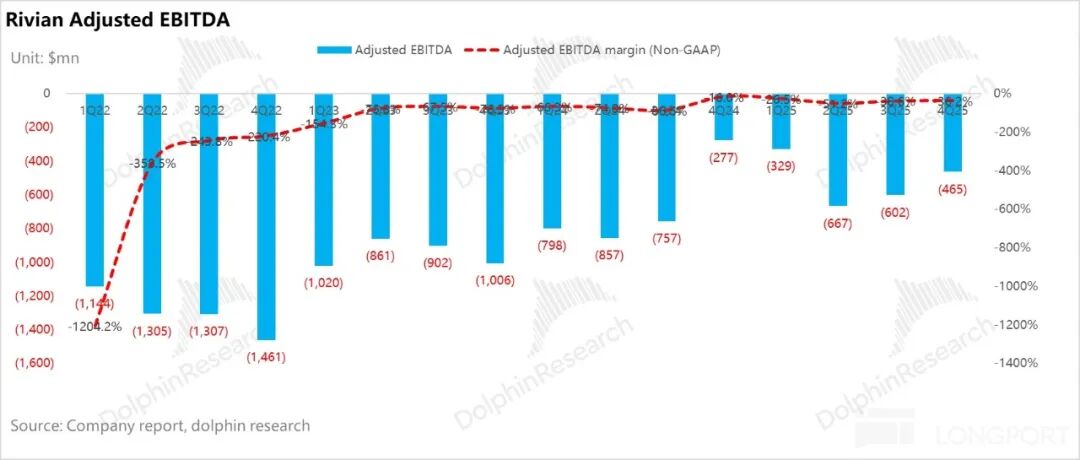

Adjusted EBITDA and net profit beat expectations: With revenue exceeding forecasts, gross margin improving QoQ, and well-controlled operating expenses, adjusted EBITDA and net profit both surpassed expectations. Adjusted EBITDA was -$470 million, up $140 million QoQ despite lower sales, better than the market consensus of -$570 million.

Dolphin Research's Overall View:

Overall, Rivian delivered a strong performance against low expectations. Affected by the IRA subsidy phase-out in the U.S. market, Q4 sales across the industry (including Tesla) were sluggish, and Rivian was no exception, hitting a sales trough.

However, Rivian outperformed market expectations in both revenue and profitability, with sequential improvements in gross and net margins, demonstrating relatively strong cost control amid headwinds.

Beyond the results, market attention is focused on Rivian's 2026 guidance, as the affordable R2 model is set to enter mass production and launch in 2026:

① Vehicle sales guidance of 62,000–67,000 units: Up 47%–60% YoY from 42,000 units in 2025, primarily driven by the R2's production and launch in 2026.

Rivian expects Q1 2026 deliveries to be around 9,000–11,000 units, rising to 22,000–23,000 units per quarter in H2 2026 as R2 production ramps up. The R2's initial production will start with a single shift, switching to dual shifts by year-end.

Dolphin Research estimates that if R1 sales decline 7% YoY due to subsidy impacts, the implied R2 sales guidance is ~21,000–27,000 units, significantly higher than the ~10,000 units previously forecast by major banks.

Banks were previously bearish because the R2's H1 2026 deliveries will still use second-gen hardware, while third-gen hardware with Rivian's self-developed 800 TOPS RAP1 chip and advanced sensors (including LiDAR) will only be available by year-end. Combined with subsidy-induced demand suppression, the market had expected Rivian's 2026 total sales to reach just 47,000–50,000 units.

Rivian's above-consensus sales guidance alleviates some market concerns.

② Adjusted EBITDA guidance of -$1.8 billion to -$2.1 billion (vs. -$2.06 billion in 2025): Below market expectations of -$1.8 billion, mainly due to prolonged R2 production ramp-up throughout 2026 and increased R&D investment in autonomous driving, diluting the profit improvement from sales growth.

However, Rivian previously guided for R2's gross margin to turn positive by Q4 2026, driven by BOM cost reductions from joint procurement with Volkswagen and higher sales volume lowering per-unit depreciation costs.

Rivian expects software and services revenue to grow 60% YoY to $2.5 billion (with the Volkswagen JV contributing ~half), at an overall gross margin of 35%, providing crucial support for Rivian's overall gross margin stability during the R2 ramp-up phase.

③ Capital expenditure guidance of $1.95–$2.05 billion: Higher than $1.7 billion in 2025, primarily due to construction of the Georgia factory (for R2 expansion and R3 production).

④ Autonomous driving progress: Rivian's self-developed RAP 1 chip (800 TOPS) has been unveiled. Point-to-point (P2P) autonomous driving will launch in H2 2026, while "hands-off + eyes-off" driving is expected in 2027. Rivian is closely following Tesla's AI and AD strategy, maintaining its scarcity value in the U.S. market.

⑤ Cash flow: As of late 2025, Rivian held ~$6.1 billion in cash and cash equivalents. With an expected $2 billion injection from Volkswagen in 2026, $500 million in 2027, and ongoing U.S. Department of Energy loan negotiations, current funds are sufficient to support operations for the next 2–3 years, with no short-term liquidity risks.

The R2's progress is on track, and the above-consensus sales guidance reflects management's confidence in the new model. Successful R2 ramp-up will be the core driver of Rivian's stock price.

A more detailed valuation analysis is available in the same name article under the "Insights - Deep Dive (Research)" section of the Longbridge App.

Below is a detailed analysis:

I. Vehicle sales decline, but performance improves sequentially

1. Gross margin continues to rise QoQ

Despite the IRA subsidy phase-out impacting Rivian's Q4 vehicle sales, which declined QoQ, gross margin surprisingly improved further.

Q4 gross margin was 9.3%, up 7.8 percentage points QoQ, significantly exceeding market expectations of 3.4%. Both vehicle sales and services gross margins improved QoQ:

① Vehicle gross margin still rising: Automotive gross margin expanded 4.4 percentage points QoQ to -7%, mainly due to $29 million in carbon credit revenue recognized in Q4 (none in Q3).

Excluding this impact, true vehicle gross margin was -11%, up 2.5 percentage points QoQ, driven by lower per-unit variable costs, offsetting the negative effects of lower ASPs and higher per-unit depreciation costs.

② Software and services gross margin also impressive: This segment's gross margin rose 3 percentage points QoQ to 40% (from 37% in Q3), primarily due to high-margin technology licensing revenue from the Volkswagen JV ($270 million in Q4, 60% of total software and services revenue), along with margin improvements in used car sales, vehicle maintenance, and other services.

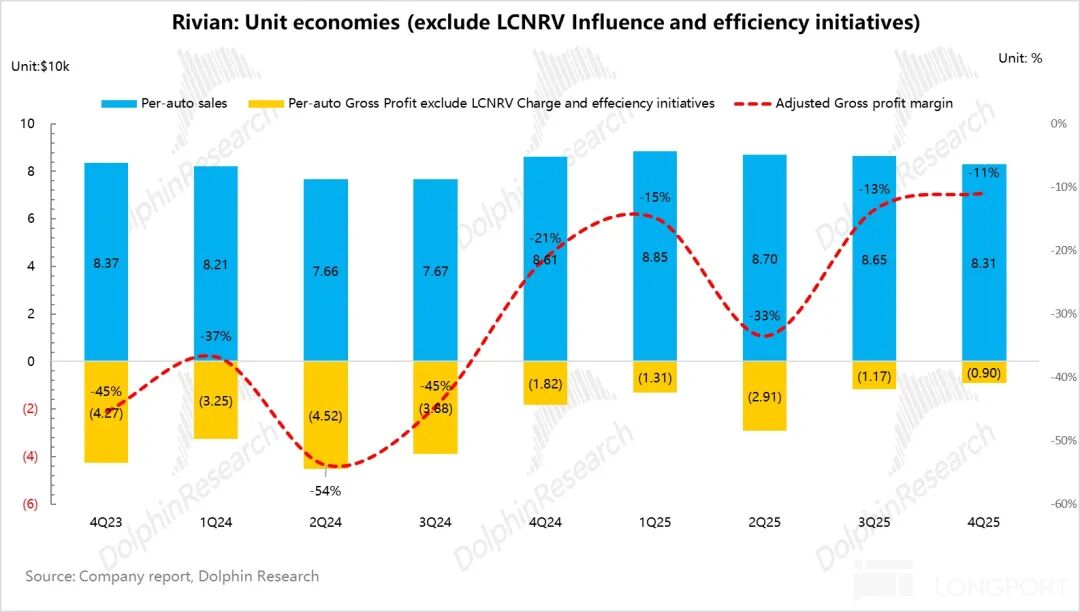

2. Lower per-unit costs drive above-expectation automotive gross margin

Analyzing Rivian's true automotive gross margin is complex due to various accounting adjustments (inventory LCNRV write-back, one-time costs, etc.).

Excluding carbon credits and inventory impairments, true automotive gross margin in Q4 was -10.9%, up 2.5 percentage points QoQ from -13.5% in Q3, marking the best quarterly performance despite the sales trough.

Key per-unit economics:

1) ASP: Declined QoQ due to higher EDV mix and increased discounts

Q4 ASP was $83,000, down ~$4,000 QoQ, likely due to a higher mix of lower-priced EDV vans and increased promotional discounts (e.g., $5,000–$6,500 lease rebates, 0% financing for 5 years on 2025 R1 inventory, and rates as low as 0.99%–1.99% on new Tri-motor or Dual-motor versions).

2) Per-unit cost: Down $6,000 QoQ, driving gross margin improvement

a. Per-unit depreciation cost up $2,000 QoQ due to lower sales volume

Q4 per-unit depreciation cost rose $2,000 QoQ to $11,000, as Rivian's Q4 sales declined 26% QoQ to 9,700 units due to the IRA subsidy phase-out, reducing scale effects.

b. Per-unit variable cost down $8,000 QoQ due to weaker tariff impacts and ongoing cost reductions

Q4 per-unit variable cost fell $8,000 QoQ to $81,000, primarily due to:

① Rivian expects the extension of U.S. Section 232 tariff offsets (3.75% of MSRP) to 2030 and expanded part categories under the 232 program to benefit its vertically integrated model (self-manufactured parts), reducing tariff impacts to hundreds of dollars per unit (vs. ~$2,000 in Q3). Subsidies likely offset tariff costs in Q4, with further benefits ahead for the R2.

② Higher mix of low-cost, high-margin EDV models also contributed to variable cost reductions.

③ Lower raw material costs: Declining lithium prices and joint procurement with Volkswagen further reduced material costs.

c. Per-unit gross profit improved QoQ due to cost reductions

Q4 per-unit gross profit rose $2,600 QoQ to -$9,000, with true automotive gross margin improving 2.5 percentage points QoQ to -10.9%.

3. Overall revenue slightly exceeds expectations

Total revenue was $1.29 billion, slightly above the $1.26 billion consensus despite weak vehicle sales:

① Vehicle sales revenue (including carbon credits) was $840 million, down 26.5% QoQ, due to the IRA subsidy phase-out reducing Q4 sales volume 26% QoQ to 9,700 units, and ASP declining $4,000 QoQ to $83,000 due to higher EDV mix and increased discounts.

② Software and services revenue remained strong at $450 million, up $30 million QoQ, driven by high-margin technology licensing revenue from the Volkswagen JV ($270 million in Q4, 60% of total), along with growth in used car sales and vehicle maintenance services.

4. Adjusted EBITDA and net profit beat expectations

Adjusted EBITDA was -$470 million, up $140 million QoQ despite lower sales, better than the -$570 million consensus, driven by gross margin expansion and well-controlled operating expenses:

Q4 R&D expenses rose slightly due to R2 prototype development, AD training, and cloud services, but overall remained controlled, down $30 million QoQ to -$420 million. SG&A expenses also declined $30 million QoQ to -$530 million, despite ongoing channel and team expansion.

The adjusted net profit was -660 million, which was also higher than the expected -830 million. This was also due to a significant quarter-over-quarter increase in gross profit margin and a decline in the three expenses.

- END -

// Reprint Authorization

This article is an original work by Dolphin Research. Reprinting requires authorization.

// Disclaimer and General Disclosure Notice

This report is intended solely for general comprehensive data purposes, designed for general reading and data reference by users of Dolphin Research and its affiliated institutions. It does not take into account the specific investment objectives, investment product preferences, risk tolerance, financial situation, or special needs of any individual receiving this report. Investors must consult with independent professional advisors before making investment decisions based on this report. Any person making investment decisions using or referring to the content or information mentioned in this report does so at their own risk. Dolphin Research shall not be liable for any direct or indirect responsibilities or losses that may arise from the use of the data contained in this report. The information and data contained in this report are based on publicly available sources and are for reference purposes only. Dolphin Research strives to ensure, but does not guarantee, the reliability, accuracy, and completeness of the relevant information and data.

The information mentioned or the views expressed in this report shall not, under any jurisdiction, be considered or construed as an offer to sell securities or an invitation to buy or sell securities, nor shall they constitute advice, solicitation, or recommendation regarding securities or related financial instruments. The information, tools, and materials contained in this report are not intended for distribution to, or use by, any person or resident in any jurisdiction where such distribution, publication, provision, or use would conflict with applicable laws or regulations or would subject Dolphin Research and/or its affiliates or associated companies to any registration or licensing requirements in that jurisdiction.

This report merely reflects the personal views, insights, and analytical methods of the relevant creators and does not represent the stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, and the copyright is solely owned by Dolphin Research. Without the prior written consent of Dolphin Research, no institution or individual shall (i) make, copy, reproduce, duplicate, forward, or create any form of copies or reproductions in any manner, and/or (ii) directly or indirectly redistribute or transfer them to other unauthorized persons. Dolphin Research reserves all related rights.

-

![]()

Depreciation Rate on Par with Mobile Phones: Just 40% Value Retention After Three Years—Why Do Battery Electric Vehicles Lose Their Worth?

-

![]()

Clearing Bugatti Stock Worth 7 Billion: Why is Porsche 'Cutting Ties'?

-

![]()

Don’t Dismiss Huawei’s Potential in Sedans Just Because the Shangjie Hasn’t Hit It Big Yet

-

![]()

Unsold Cars in China Find Success Overseas

-

![]()

Ghosn: Only I Can Save Nissan, Shareholders Beg Me to Return

-

![]()

Expanding Automobile Consumption: It's Time to Address the High Cost of Electric Vehicle Repairs

-

![]()

Luna Ultra Entangled in 'National Subsidy Fraud' Controversy, Insta360 Pushed to the Brink by DJI

-

![]()

People have long suffered from splash ads. Will the 'temporarily disappeared' traffic behemoth make a comeback?