Merz's Visit to China Sends Strongest Signal: Only by Embracing China Can German Automakers Secure a Future!

03/02 2026

03/02 2026

420

420

Layoffs, factory closures, and plummeting exports—as the German automotive industry at home experiences a harsh winter, German Chancellor Friedrich Merz has led a “German Industrial Dream Team” composed of the heads of three major automakers aboard a special plane to China.

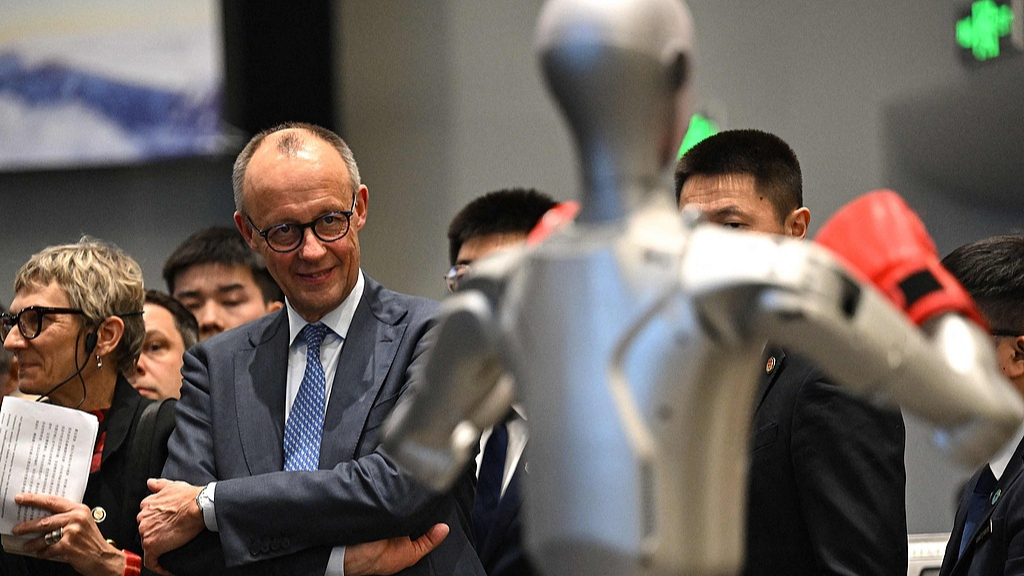

On the afternoon of February 26, German Chancellor Friedrich Merz concluded his first official visit to China since taking office. This delegation, comprising around 30 representatives from the German business community, was hailed by some German media as one of the “most luxurious lineups” accompanying a German chancellor to China in recent years.

As the crown jewel of German industry, the automotive sector's moves undoubtedly hold the key to interpreting the true intent of this visit. Oliver Blume, Chairman of the Board of Management of Volkswagen Group, Oliver Zipse, Chairman of the Board of Management of BMW Group, and Ola Källenius, Chairman of the Board of Management of Mercedes-Benz Group, all accompanied Merz. The Germans are no longer talking about the outdated notion of “trading market access for technology.” Because everyone knows that if they fail in the battle for new energy and intelligence in the Chinese market, the German automotive industry will suffer unbearable consequences.

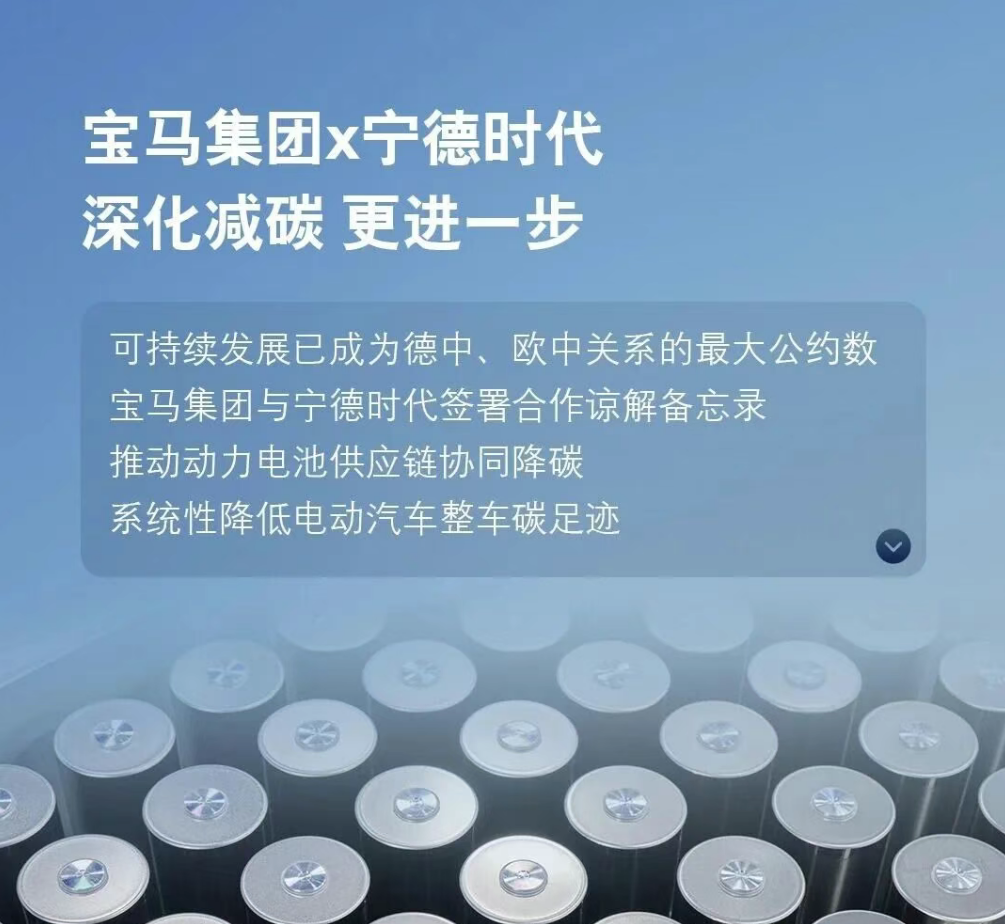

From Merz personally testing Mercedes-Benz's urban intelligent driving system, co-developed with Momenta, and exclaiming “amazing,” to his urgent trip to Hangzhou to inspect Unitree Robotics, the “Spring Festival Gala star”; from BMW signing a power battery (power battery) carbon reduction agreement with CATL to Mercedes-Benz deepening its AI cooperation with ByteDance, these series of moves send a clear signal—the Germans must humble themselves and integrate their century-old automotive logic into China's reshaping industrial chain and innovation ecosystem.

“Success in China is essential for success in other markets.”

To understand the strategic significance of Merz's visit, one must first recognize the structural crisis the German automotive industry is facing.

Data from the China Automobile Dealers Association shows that German brands sold a cumulative 3.645 million new vehicles in China in 2025, a nearly 10% year-on-year decline; in January 2026, this downward trend continued, with a further 7.6% drop. In stark contrast, the penetration rate of new energy vehicles from Chinese domestic brands has surpassed 50%, with BYD's monthly sales exceeding the combined total of all Volkswagen China models.

However, paradoxically, the centrality of the Chinese market remains unshakable—Volkswagen Group's sales in China account for about 30% of its global total, BMW's 25.4%, and Mercedes-Benz's 26.5%. This means that the Germans' “Achilles' heel” has never been so clearly exposed to China.

Market pressure is not new; what truly warrants attention is the fundamental reversal of power dynamics. In the past, the paradigm of Sino-German automotive cooperation was “market access for technology,” where Germany provided platforms, engines, and chassis tuning, while China offered joint venture partners, distribution channels, and labor. Today, China is no longer just “the world's largest single market” but has emerged as an innovation hub and global strategic center for electrification and intelligence.

“For Volkswagen Group, Germany, and even the entire European industrial sector, China is not just a sales market but also a source of innovation, a technology partner, and a major pillar of the global value creation system.” This statement by Ralf Brandstätter encapsulates the collective awakening of the German automotive industry.

This shift in positioning, from “market” to “innovation hub,” is driven by reality. Against the backdrop of the rapid rise of Chinese domestic automotive brands, the leading edge of German automakers in electrification and intelligence is being gradually eroded. A deeper challenge lies in the fact that the pace and direction of technological iteration are now defined by the Chinese market. Blume's assertion that “only by succeeding in China can one succeed in other markets” is the most concise summary of this reality.

Thus, Merz's visit must secure an entry ticket—or a lifeline—for the core lifeblood of German industry to integrate into China's new ecosystem.

How to Secure an Entry Ticket to China's Future Market?

The Germans have finally realized that instead of stubbornly going it alone, they should humble themselves and fully embrace China's industrial chain.

They are seeking a “survival formula” for themselves: German luxury brands + Chinese batteries + Chinese intelligent driving + Chinese AI = an entry ticket to China's future market. Merz's visit has set three core directions for the development of German automakers in China, each directly addressing the key issue of “adaptation.”

First, accelerate electrification and deeply localize production capacity and supply chains. BMW continues to invest in its Shenyang base, with total investments exceeding 120 billion yuan; Mercedes-Benz plans to jointly invest over 14 billion yuan in China with its partners; Volkswagen has established its largest overseas R&D and production center in Hefei, shortening vehicle development cycles by about 30%—meaning future models developed specifically for the Chinese market will no longer need to wait for lengthy approvals from Germany.

More critically, supply chains are being “bound to China.” CATL, Eve Energy, Envision AESC—the Germans are aggressively partnering with Chinese battery giants. On February 25, BMW deepened its cooperation with CATL, focusing on battery passports and carbon footprint accounting, to fully resolve the “logistical” issues of electrification.

Second, pivot entirely to intelligent driving and use “Chinese solutions” to address core weaknesses. This was evident in Merz's itinerary.

On February 26, Merz personally experienced Mercedes-Benz's urban intelligent driving system, co-developed with Momenta. His “amazing” remark reflected the German leadership's Clear cognition (clear-eyed recognition) of their technological shortcomings.

Thus, we see: BMW integrating with HarmonyOS and partnering with Baidu Apollo; Audi deeply collaborating with Huawei's ADS. This means German luxury cars will achieve a “German luxury feel + Chinese intelligent experience” combination, swiftly regaining discourse power (voice) in the high-end intelligent electric vehicle market.

Third, reinvent manufacturing through robotics and smart manufacturing. Merz's dedicated visit to Unitree Robotics was a highly symbolic moment. In a Hangzhou showroom, the chancellor watched a quadruped robot perform various complex maneuvers, his eyes reflecting both surprise and anxiety. Germany possesses top-tier industrial manufacturing heritage, while China leads in robotics and flexible production capabilities. Their combination will comprehensively upgrade German factories in China. In the future, Chinese smart equipment will massively enter Volkswagen, BMW, and Mercedes-Benz production lines, achieving a milestone “Chinese smart manufacturing for German cars.”

Merz's visit has pointed the way forward for the German automotive industry, but for it to truly adapt to China's industrial chain and market logic, a painful identity reconfiguration is necessary—from a lofty “technology exporter” to a deeply embedded “ecosystem participant” in China's innovation ecosystem.

This means acknowledging that in the realm of intelligence, Chinese companies have become the teachers. In the future, they must use China's brains to drive Germany's body.

Rapid Adaptation: Products Must Be Localized

The second level of change German automakers need in China is in product definition logic.

In the past, German arrogance stemmed from the fact that slightly modified global models could sell well in China. Today, this logic has completely collapsed. Chinese consumers no longer settle for “downgraded international models”; they demand products designed specifically for them, tailored to Chinese scenarios.

Thus, thorough localization of products is fundamental. They must move R&D cores to China, letting Chinese teams—who best understand the local market—define the next generation of products.

In electrification, products must be customized for the Chinese market with long range and ultra-fast charging. Chinese consumers' range anxiety and demand for fast charging far exceed those in European and U.S. markets. In Norway, consumers accept 300 km of range; in China, that would be a “deal-breaker.” German cars must develop models with larger battery capacities and higher charging power for Chinese users' travel scenarios. Volkswagen's ID. series has extended its range from 400 km to 700 km, Mercedes' EQE introduces battery optimization schemes for China, and Audi's PPE platform models will come standard with 800V high-voltage fast charging—all changes forced by the Chinese market.

In intelligence, they must meet Chinese users' extreme pursuit of a “smartphone-like experience.” Chinese consumers' demands for smart cockpits now rival those for luxury cars. Smooth interactions, rich applications, and precise voice control are all “make-or-break” features. German cars must elevate their smart experience to “smartphone-grade”—hence BMW's integration with HarmonyOS and Audi's deep customization of Huawei's cockpit.

In physical space, they must continuously lengthen, upgrade, and enhance comfort. “Lengthening” was pioneered by FAW-Audi in 1999 and remains a fundamental strategy for German cars in China. The all-new Audi Q5L and BMW X5 LWB versions all prove a simple truth: Chinese consumers' demands for rear-seat space and comfort will never be satisfied. German cars must keep upgrading in this dimension, taking “China-exclusive” to the extreme.

Among these changes, FAW-Volkswagen and FAW-Audi, participating as “national teams,” play crucial roles as “ballast stones” and “pioneers.” In 2025, FAW-Volkswagen once again claimed the “double championships” of top-selling joint venture automaker and top-selling fuel vehicle brand, with annual vehicle sales of 1.5871 million units. This foundational advantage underpins German brands' transformation in China.

2026 marks the 35th anniversary of FAW-Volkswagen's founding. The company has outlined three strategies—“stabilize the foundation, strengthen electrification and intelligence, and pioneer new frontiers”—to navigate the changes, planning to launch 13 all-new models throughout the year. Its Audi brand has been particularly aggressive and pioneering. In January 2026, the all-new Audi Q5L was officially released, fully integrating Huawei's ADS intelligent driving assistance system with a dual-lidar scheme and visual fusion perception architecture. This is not only the result of six years of joint tuning by Audi and Huawei teams but also demonstrates how joint ventures can act as bridges to deeply fuse German engineering with Chinese technology, rapidly producing “adapted products” for the Chinese market. This ability to evolve from “localization” to “Sinicization” is precisely what German giants urgently need.

Win-Win and Pressure: Who Benefits? Who Faces Pressure?

For China's automotive market and industry, this new wave of German development brings not just a simple return of brands but deep-level win-win outcomes and pressure for adaptation.

The win-win aspect manifests in two areas: consumers and the industrial chain.

On one hand, with the Intensive advertising ( dense launch) of new models like the Audi A6L e-tron and ID.AURA, along with localized cost reductions for PPE platform models, consumers will gain access to vehicles combining German handling, luxury heritage, and local intelligent experiences at more affordable prices. The luxury pure electric market will see a true “supply explosion,” resolving consumers' past dilemma of choosing between “traditional luxury without intelligence” and “intelligent new forces without luxury.”

On the other hand, the Vehicle Engineering (vehicle engineering), chassis tuning, brand operations, and global quality management experience brought by German brands will continue to empower China's industrial chain. From signing China's first luxury car technology transfer contract in 1988 to pioneering “lengthening” in 1999, and now fully embracing China's intelligent ecosystem, FAW-Audi has not only nurtured world-class suppliers like Fuyao Glass through “full-value-chain localization” but also deeply collaborated with Chinese tech giants like Huawei and CATL in the smart electric era. This collaboration is systemic and profound, far beyond simple order placements.

The pressure for adaptation manifests in two dimensions: technology export and competitive landscape.

China's technology exports in intelligent driving, batteries, and robotics are now being Reverse output (reverse exported) through the German global system. For example, CATL's batteries enter Europe with BMW, Momenta's algorithms go global with Mercedes, and Huawei's intelligent driving solutions are exported overseas with Audi. This signifies that China's automotive industry is moving from “product exports” to “technology exports” and “standard exports,” perhaps reaching a height unseen in the past 40 years.

Meanwhile, the full awakening of German brands is also pressuring Chinese domestic brands to accelerate their evolution. When Mercedes boasts “German chassis + Momenta” and Audi achieves “PPE platform + Huawei ADS,” Chinese brands' early advantages in intelligence will face severe challenges. This competitive pressure is precisely the best catalyst for sustained industrial progress.

Kanche Shuo (Car Talk)

Merz's plane has returned, but the real test has just begun. The German automotive industry must complete this “survival adaptation” in China, as it is not just a business choice but a survival necessity. One statistic suffices: The annual profits China generates for Volkswagen could sustain one-third of Germany's domestic factories. Losing the Chinese market would mean German cars losing their entry ticket to global competition for the next decade—not just in sales but in technological discourse power and standard-setting.

Thus, the Germans must gamble. They are betting that when “German craftsmanship” and “Chinese solutions” deeply fuse, a new breed of vehicle will emerge—one combining German handling quality with Chinese intelligent experiences, the brand premium of a century-old luxury marque with the agile iteration of local innovation. This could win back Chinese consumers, especially the “swing voters” torn between new forces and traditional luxury brands.

But they must also face a harsh reality: Chinese consumers' loyalty is eroding. Gen Z buyers no longer worship BBA's halos; they are more willing to pay for “black technology” from new forces. This means German cars must not just win back the market but an entire generation.

This is a war with no retreat. If we win, the German automotive industry can continue to thrive for another thirty years; if we lose, Wolfsburg, Stuttgart, and Munich will become Europe's Detroit.

For the Chinese automotive industry, this represents both a win-win situation and a forced transformation; it is both an embrace and a game of strategy. When the Germans use China's brain to drive Germany's body, and when Chinese technology, paired with German brands, sets sail for the global market, a new world order in the automotive industry is taking shape.

Operated by | Su Hongying

Produced by | Kanche China

-

![]()

AI Predicting the World Cup? It’s Time to Stop Insulting AI

-

![]()

iPhone 18 Pro Memory Costs Soar Threefold! Apple Seeks Trump Administration Approval for CXMT Memory Chips

-

![]()

AI Tutoring: A Crack in the Intense Competition of East Asia

-

![]()

Weekly Stock Review | Li Bin Sounds Alarm on 'Toughest' Year, Casting a Shadow Over Lei Jun's Noodle Moment

-

![]()

Car Manufacturing Paused, Yet Dreame’s Automotive Dream Marches On

-

![]()

Can the Brand-New Hongqi H7 Forge Its Own Identity in the Hybrid Vehicle Market?

-

![]()

Challenges in Redeeming Certificates for New Cars: Mercedes-Benz Dealership Group Grapples with Operational Hurdles Once Again

-

![]()

Porsche Returns to Volkswagen, Ending the 'Electric Ferrari' Story