Wei Jianjun Says 'There is a Huge Gap Between Chinese Automobiles and Those from Europe, the US, Japan, and South Korea'. Where Does the Gap Lie?

03/04 2026

03/04 2026

446

446

Lead-in

Introduction

It's good not to be overly self-congratulatory.

In the past few years, the rise of Chinese automobiles has been rapid enough to be recorded in the annals of the global automotive industry. From production and sales volumes exceeding 30 million units for the first time, to export volumes surpassing Japan to claim the top spot globally, and then to the penetration rate of new energy vehicles exceeding 50%, the Chinese automotive industry has made significant progress in electrification, intelligence, exports, and industrial chains, becoming an important force in the global automotive market.

Especially in the new energy sector, China has achieved 'overtaking on a different track.' In 2025, the production of new energy vehicles exceeded 16 million units, with monthly sales accounting for more than half. For every three new energy vehicles sold globally, two come from China.

Leading automakers such as BYD, Great Wall, and Geely have ventured overseas, establishing a foothold in European, Southeast Asian, and South American markets. BYD's overseas sales surged by 145% year-on-year, Great Wall established production bases in multiple overseas countries, and SAIC sold well in several European countries. Chinese automobiles are transitioning from 'product exports' to 'brand exports.' Chinese brand vehicles are ubiquitous, and consumer recognition of domestically produced cars has shifted from 'cost-effectiveness' to technology, quality, and intelligence.

At one point, voices claiming 'Chinese automobiles are fully leading' and 'overtaking on a different track is a foregone conclusion' were loud, as if we had completely surpassed veteran automakers from Europe, the US, Japan, and South Korea and become the leaders of the global automotive industry.

Amidst this celebration, Wei Jianjun, Chairman of Great Wall Motors, poured 'cold water' on Chinese automobiles recently. He stated, 'Our Chinese automobiles, including Great Wall, still have a huge gap compared to those excellent companies... Veteran enterprises have a deep foundation in car manufacturing. The road to car manufacturing is long, and we still need to learn diligently, humbly, and solidly.'

Admittedly, these words may be disappointing to many, but it's good not to be overly self-congratulatory. Although Chinese automobiles have made significant progress and have an increasingly influential voice in the global automotive industry, when we deeply analyze the comparison between Chinese automobiles and some veteran powerhouses from Europe, the US, Japan, and South Korea, there are indeed many areas worth learning from.

This gap is not a shortcoming in a single dimension but a systemic gap spanning technology, brand, and details. This gap is temporarily masked by the dividends of new energy and short-term sales but cannot be truly ignored.

01 The Gap Still Exists, and the Chase is On

If we list what Chinese automobiles need to learn from veteran automakers, technology remains an item that cannot be ignored. Currently, the lead of Chinese automobiles is concentrated in the new tracks of new energy and intelligent connectivity, but there are still gaps in traditional core technologies and engineering systems.

Especially, European and American automakers, with a century of precipitation, possess mature technological reserves and a comprehensive R&D system in traditional powertrain fields such as engines and transmissions. Even in the transition to new energy, their mechanical engineering expertise has not been lost.

Take the 'heart' of a vehicle—the engine—as an example. The industry holds an annual 'Ward's 10 Best Engines' competition, where brands such as Volkswagen, Dax, BMW, Nissan, Honda, Mazda, General Motors, and Cadillac consistently rank among the top ten, with few Chinese engines making the list. In the most recent 2024 competition, only BYD's 2.0T extended-range hybrid + Easy Four-Wheel Drive power system was nominated.

Take chassis tuning as another example. Most Chinese automakers rely on foreign engineers or directly borrow from mature platforms, lacking a core methodology for independent R&D. Many domestically produced cars appear fully configured but fail to achieve the stable quality of veteran automakers. Behind this gap lies decades of repeated trial and error and accumulated engineering experience, which cannot be compensate (replaced by simply stacking parameters in the short term).

At the same time, due to different competitive rhythms in various markets, the intense competition and rapid iteration in the Chinese market may lead to insufficient validation cycles. According to the industrial thinking of mature automakers, a model often undergoes five to seven years of validation, covering extreme conditions such as high temperatures, severe cold, high speeds, and rough roads. However, domestic new energy models, influenced by market competition and capital pressure, must be replaced every two to three years, and many potential issues 'hit the road before they have a chance to surface.'

Beyond vehicle manufacturing, in the battery sector, although the Chinese market has achieved leadership in production capacity and installation volume, it still lags in certain core material systems and industrialization experience. For example, LG maintains a first-mover advantage in specific technological routes (such as NCMA). In the underlying algorithms of intelligent driving, our strengths lie in scenario-based applications, but we still rely on foreign suppliers for core capabilities such as chip design and algorithm iteration. This 'application-heavy, R&D-light' status makes our lead somewhat 'fragile.'

Additionally, the gap in brand heritage is also a difficult hurdle for Chinese automobiles to overcome.

Since its inception, the automobile has never been a mere industrial product but also a carrier of brand culture and value. Traditional veteran automakers, with a century of accumulation, have formed unique brand genes and user perceptions.

For example, Mercedes-Benz represents luxury, BMW represents sportiness, Toyota represents reliability, and Volkswagen represents rigor. These labels are deeply rooted in the hearts of global consumers. Such brand premium is not built through short-term marketing or hit products but through the trust accumulated by generations of consumers over long-term use. In contrast, Chinese automotive brands, on the whole, still lack the exploration and precipitate (accumulation) of brand culture.

This gap is directly reflected in pricing power and tolerance for mistakes: the same quality flaw is called an 'isolated incident' for luxury brands but labeled a 'common problem' for domestic brands; the same configuration trade-off is interpreted as an 'engineering orientation' for luxury brands but accused of 'reducing configurations to fleece consumers' for domestic brands.

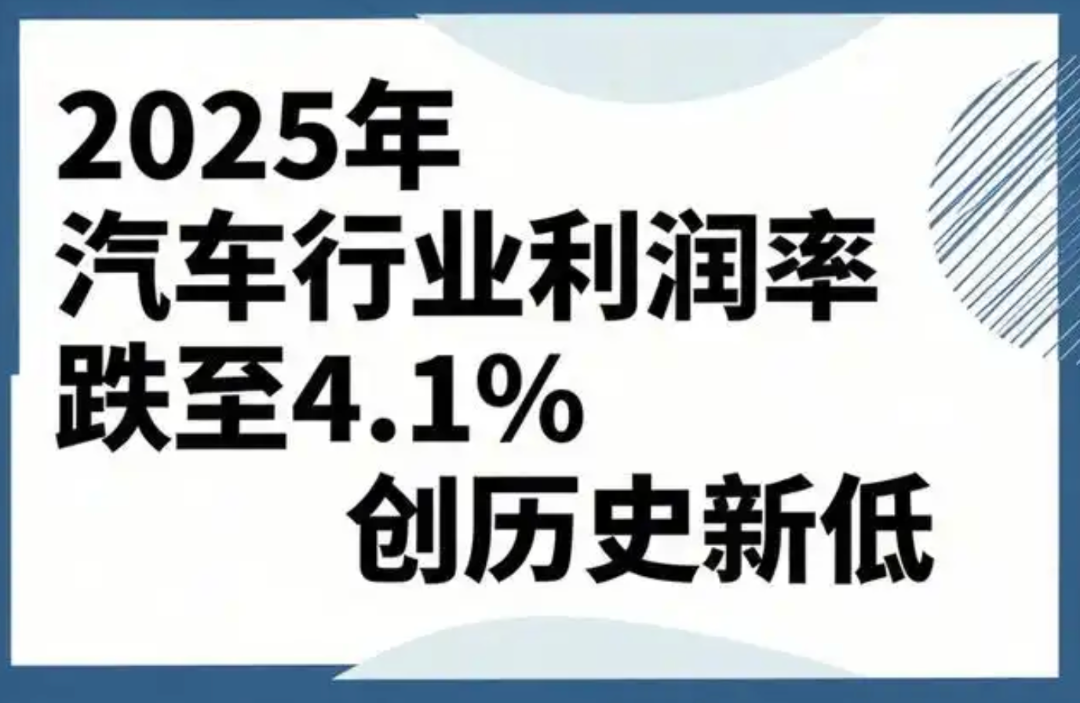

When it comes to one of the core pain points of Chinese automotive development, profit undoubtedly (undoubtedly) amplifies this pain.

In recent years, a saying has circulated in the industry: 'We work hard all year to sell 30 million vehicles, yet the profit is still less than Toyota's 10 million vehicles.'

Data shows that in fiscal year 2025, Toyota's net profit reached 4.765 trillion yen, equivalent to RMB 237.7 billion. This is nearly three times the combined profit of 18 listed Chinese passenger vehicle enterprises in 2024. Among these 18 Chinese enterprises, although 13 achieved profitability, their combined net profit was only RMB 122.677 billion; once the five loss-making enterprises are included, the total profit would decrease by another RMB 33.2 billion.

In other words, the entire Chinese listed automotive industry earns less in a year than half of Toyota's profit. During the same period, the profit margin of the domestic automotive industry was 4.1%.

Furthermore, in terms of attention to detail in car manufacturing, global supply chain layout, after-sales service systems, and user operations, Chinese automakers also differ from veteran automakers. The latter, with years of globalization, possess stable supply chain systems and comprehensive after-sales service networks, enabling them to respond quickly to global market changes. In contrast, most of the supply chains of Chinese automakers are concentrated domestically, and their overseas supply chain layouts are still imperfect. Once faced with risks such as geopolitical tensions and trade barriers, they may encounter supply chain disruptions.

02 Acknowledge the Gap, and the Future is Promising

Of course, we cannot deny the progress Chinese automobiles have made in recent years just because gaps exist.

In fact, amidst the global automotive industry's transition to electrification and intelligence, Chinese automobiles have seized historical opportunities, achieving leapfrog development from 'catching up' to 'running alongside' and even 'leading' in some areas. This achievement deserves our pride and recognition.

Over the past five years, the charging efficiency of power batteries in China has increased more than fourfold, and motor and electronic control systems have reached global leading levels. BYD's Blade Battery and CATL's ternary lithium batteries not only dominate the global market but also achieve significant breakthroughs in safety and energy density.

In the field of vehicle manufacturing, Chinese automakers were the first to launch pure electric exclusive platforms, such as BYD's e-platform, Great Wall's Lemon Hybrid Platform, and Geely's SEA Grand Architecture, significantly improving overall vehicle performance and space utilization. In 2025, the production and sales of new energy vehicles in China both exceeded 16 million units, becoming an important force in the global new energy vehicle market.

Additionally, compared with veteran automakers, Chinese automakers better understand consumer needs and faster (more quickly) integrate technologies such as artificial intelligence, big data, and the Internet of Things into automotive products, creating intelligent experiences that better fit user scenarios. Currently, the penetration rate of Level 2 assisted driving among Chinese brands continues to rise, and Level 3 autonomous driving is about to experience rapid development.

At the same time, guided by national policies and through corporate efforts, China has built the world's most complete and resilient new energy vehicle industrial chain, from upstream lithium and cobalt mines to midstream batteries, motors, and electronic controls, and then to downstream vehicle manufacturing and after-sales services, forming a closed-loop industrial chain. This not only reduces production costs but also ensures supply chain stability.

Currently, more than 10 Chinese auto parts enterprises have made it to the 2025 Global Auto Parts Suppliers Top 100 list, covering areas such as batteries, motors, and intelligent cockpits, breaking the monopoly of foreign auto parts enterprises. This perfect (well-established) supply chain system is difficult for European, American, Japanese, and South Korean automakers to replicate in the short term and is an important support for Chinese automobiles to iterate quickly and seize market share.

In 2025, the sales volume of Chinese brand passenger vehicles reached nearly 21 million units, with a market share of nearly 70%, an increase of about 30 percentage points from the end of the '13th Five-Year Plan' period, changing the market landscape dominated by joint-venture vehicles. In terms of overseas expansion, Chinese automotive exports covered more than 200 countries and regions, with export volumes reaching 8.32 million units in 2025, a year-on-year increase of 30%. BYD and Geely ranked among the top ten global automakers in sales volume.

Moreover, more and more Chinese automakers have recognized the importance of core technologies, increasing R&D investment in core areas such as batteries, chips, and algorithms, establishing independent R&D systems, cultivating core technical teams, and holding numerous patents in areas such as batteries, motors, and electronic controls, achieving self-developed and controllable (independent and controllable) core technologies.

This emphasis on R&D is the foundation for the long-term development of Chinese automobiles and the key to narrowing the gap with veteran automakers.

In other words, we acknowledge the gap but do not underestimate ourselves; we recognize our achievements but do not become complacent. This is the core meaning of Wei Jianjun's remarks and the clarity that the Chinese automotive industry needs most.

In today's increasingly competitive global automotive industry, leading in sales is only temporary. Only by acknowledging the gap and facing problems head-on can we achieve progress. Currently, Chinese automobiles are at a critical juncture of transformation, facing both historical opportunities brought by new energy and intelligence and challenges of shortcomings in technology and brand. Indulging in the notion of 'fully leading' and avoiding the gap will only lead to elimination by the market; only by staying sober and facing the gap can we develop healthily amidst fierce competition.

Editor-in-Chief: Du Yuxin Editor: He Zengrong

THE END

-

![]()

The Unstoppable Rise of 'Optical Progress and Copper Decline': Sunny Optical’s Strategic Vision for the Next Decade

-

![]()

AI + Going Global in the Second Half: No Intermission for Robot Vacuum Cleaners

-

![]()

The Suffering Endured in E-commerce, Walmart Doesn't Want to Repeat in AI

-

![]()

What Does the Doubling of New Energy Vehicle Exports Mean?

-

![]()

Ghosn: 'Only I Can Save Nissan'

-

![]()

Volkswagen Lays Off 100,000 Employees, The Elephant Sits Down

-

![]()

Expanding Production Capacity! Yutong Optics Acquires Approximately 1.5 Hectares of Industrial Land in Chang'an, Dongguan

-

![]()

Why Is Nokia Making a Comeback in the AI Era?