February Sales Plunge for Emerging Automakers: Is the Era of Booming Growth Over?

03/04 2026

03/04 2026

504

504

They say the toughest times come when warmth returns but the cold still lingers, and for emerging automakers, the tension is palpable.

My high school physics teacher once used an analogy to describe our class's exam scores after a mock test: 'A student's score is like a ball placed high up. When it is suddenly released and falls freely, by the time it hits the ground and we discuss it again, due to air resistance, it can never bounce back to its original height and will eventually come to rest.'

Little did we know that this analogy would aptly describe the sales of emerging automakers more than a decade later.

After experiencing a general decline in sales in January, February saw an even steeper drop. Overall, among the emerging automakers, including Aito, no brand sold more than 30,000 units in a month, with many selling less than 20,000, once again teetering on the edge of the 10,000-unit survival threshold. Several brands even dared not disclose their sales figures.

They say the toughest times come when warmth returns but the cold still lingers, and for emerging automakers, the tension is palpable. Although the automotive market performed poorly this February due to the Spring Festival holiday, adjustments to new energy vehicle purchase tax policies, and the reduction of 'national subsidies' in some cities.

What is concerning is that the market may never fully recover.

The Battle Among the Top Three: A Shifting Landscape

If we consider monthly sales of 20,000 units as the threshold for the 'first tier' of emerging automakers, then in February, at least five brands stood at this gateway. However, upon closer inspection, the internal rankings have undergone subtle yet significant changes.

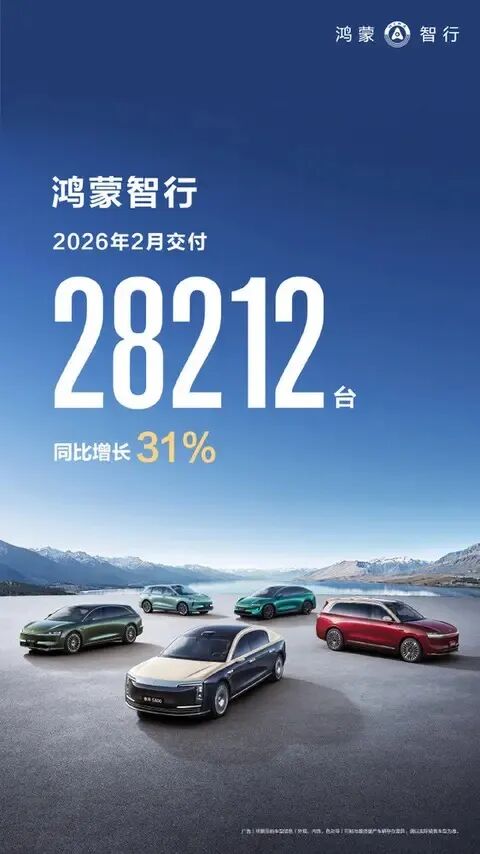

In terms of total sales, Aito remains the undisputed leader. Even with a halving of sales, it maintained its leading position with 28,212 units, a year-on-year surge of 31.1%, and cumulative sales of 86,000 units from January to February.

This figure is undoubtedly a victory for the 'Huawei + automaker' deep empowerment model. The scale and efficiency of Aito's 'group army operations' are unattainable for solo brands.

However, it is worth noting that among Aito's 'Five Realms,' only the Aito brand truly stands out, with a single-brand sales volume reaching 17,984 units. As the absolute mainstay of Aito, the decline in February was mainly due to product transitions. The clearance of old M5/M7 models is nearing completion, while the highly anticipated M6 has yet to be officially delivered. Although the cumulative sales of 58,000 units from January to February are not bad, the success of the M6 is crucial for Aito to regain its peak.

Among the other brands, Exa cannot support high sales volumes due to its positioning as a million-dollar flagship. Sales data released by Chery Automobile shows that Luxeed sold only 945 units in February, a year-on-year decline of 90.6%. Xiangjie and Shangjie have also remained lukewarm and failed to explode in sales.

It can only be said that Huawei is not a 'cure-all,' and there is still much room for future growth for Aito.

Following Aito, Leapmotor fell short by just over 100 units, nearly surpassing it again. As the 'defender' of ultimate cost-effectiveness, Leapmotor sold 28,067 units in February this year, a year-on-year increase of 10.99% and only a slight month-on-month decline of 12.45%, making it one of the less affected brands.

While competitors saw their sales 'halved' due to the Spring Festival factor, Leapmotor managed to control its month-on-month decline reasonably well. This is attributed to the impenetrable wall it has built in the 100,000-150,000 yuan market with its B-platform models. From the C-series to the B-series, Leapmotor has proven with its 'full-stack self-research + extreme cost control' that there is significant potential in the mass-market.

Li Auto, once the 'leader of the emerging automakers,' had a somewhat lackluster performance in February, selling 26,421 units, almost flat year-on-year and down 4.51% month-on-month. However, in cross-comparison, Li Auto's performance can be considered stable.

Since last year, facing the strong impact from Aito and the sudden rise of various large SUVs, the aging of the L-series products and the intense competition in the extended-range track have put unprecedented pressure on Li Auto. The release of the all-new L9 this year may help Li Auto stage a comeback.

Xiaomi's Halved Sales: Strategic Retreat or Bottleneck?

Xiaomi has never released accurate sales data, only announcing monthly delivery volumes rather than order volumes for each month.

Following this logic, Xiaomi's monthly delivery volume is solely related to its production capacity, and it should have been the least affected in February due to this objective factor. However, Xiaomi's delivery volume also plummeted, albeit exceeding 20,000 units, with a month-on-month collapse of 48.7% and a year-on-year decline of 15.7%.

Lei Jun explained that February was a period of proactive strategic contraction for Xiaomi. With the discontinuation of the first-generation SU7, the factory is fully dedicated to paving the way for the new-generation SU7 and YU7 SUV, leading to a 'precipitous' drop in delivery volume. This is not a bad thing but rather a buildup of strength for the launch of the new SU7 in April.

For Xiaomi, the current 'halving' is for future 'doubling.'

That being said, a simple product transition can cause sales to fluctuate wildly. This raises the question: How much of those seemingly impressive monthly delivery figures are genuine market demand, and how much are 'number games' that automakers can manipulate?

Under the pressure of an annual target of 550,000 units, how to quickly stabilize sales amid product transitions has become an urgent issue for Xiaomi.

In contrast, Zeekr Automobile emerged as the only brand to achieve growth amid this sales collapse. In February this year, Zeekr delivered 23,867 new vehicles, a year-on-year surge of 70% and a slight month-on-month increase of 0.06%.

Against the backdrop of an overall cooling pure electric market, Zeekr is one of the few brands to achieve 'year-on-year and month-on-month double growth.' The '9 Series' luxury products, such as the 9X and 009, contributed the main increment, with the 9X, priced at over 500,000 yuan, selling over 10,000 units per month, a rare feat in Chinese automotive industry history. Zeekr has proven with its strength that as long as the product is strong enough, the high-end pure electric market is not a dead end.

NIO, another representative of high-end luxury, also performed reasonably well in February, barely crossing the 20,000-unit monthly sales threshold. It delivered 20,797 new vehicles in February, a year-on-year increase of 57.6% and a month-on-month decline of 23.49%.

The nearly 60% year-on-year increase indicates that NIO's 'battery swap + service' system is regaining market recognition. Notably, the all-new ES8 delivered over 11,000 units in a single month, accounting for half of the brand's total sales.

This flagship model, once considered 'acclaimed but not popular,' has now become NIO's sharpest weapon.

A Tale of Two Extremes: Some Plummet, Some Soar

If the first tier is a battle among gods, then the second-tier brands are experiencing vastly different fates.

The first to slide from the first tier to the second tier is Xpeng. After the launch of the new MONA model, Xpeng saw a period of improvement and even enjoyed a stint at the top.

However, the hype around robots only garnered some applause, flying cars have yet to commercialize, and VLA is imminent but still unable to enhance product strength. Xpeng has found itself in an awkward position.

In February this year, sales fell to 15,256 units, a year-on-year decline of 49.9% and a month-on-month decline of 23.8%. Excluding some state-owned enterprise emerging automakers, this marks Xpeng's second consecutive month at the bottom of the top-tier list. Sales of the X9 failed to meet expectations, the dividends from the P7+ are gradually fading, and new models have yet to take over.

If the VLA in mid-March still fails to help Xpeng reverse its fortunes, its once-celebrated technological edge will truly be gone, and it will have to return to the muddy waters of low-price competition.

Additionally, Voyah delivered 8,358 units, a slight year-on-year increase but a significant month-on-month decline of 20%. Its sales poster only dared to show the cumulative sales from January to February, giving an impression of abundance.

Moreover, emerging automakers incubated by state-owned enterprises, such as Avatr and IM Motors, did not even release posters amid the cold winter, hoping to see improvements in March.

Overall, '20,000 units' has become the survival threshold for emerging automakers, a core indicator of their ability to withstand risks. Leapmotor, Li Auto, Zeekr, NIO, and Xiaomi have all crossed this hurdle, putting immense pressure on the pursuers behind them.

The past days of relying solely on 'fridges, TVs, and sofas' are no longer sufficient to win over consumers. Intelligent driving experience, energy replenishment systems, and cost control—these comprehensive capabilities are the keys to future success and are currently giving some brands a competitive edge in the market.

2026 is truly a year of major product launches, with the comprehensive renewal of Li Auto's L-series, the launch of the refreshed Xiaomi SU7, the delivery of Aito's M6, and the debut of Zeekr's 8X... Almost all the top players have saved their 'ace cards' for the second quarter and beyond.

For automakers, the real knockout phase may have just begun. Who will weather the storm, and who will fade away? Let's wait and see.

Note: Some images are sourced from the internet. If there is any infringement, please contact us for removal.

-END-

-

![]()

Can Leapmotor's New C-Series Take the Lead in Its Family Lineup?

-

![]()

Multimodal AI Model Revolutionizes Audio-Visual Perception in Steelmaking Safety: Hikvision and Nanjing Iron and Steel Forge New Pathways

-

![]()

Can Chinese Automakers Pose Such Fierce Competition? Mercedes-Benz Cancels Year-End Bonuses for 90,000 Staff, Volkswagen to Lay Off 100,000 Employees...

-

![]()

Anhui and Zhejiang Vie for the Crown in New Energy Vehicle Dominance: Who Will Prevail?

-

![]()

Tmall 618 Rankings Unveil Trends Transforming the Home Appliance Industry

-

![]()

This Week in Home Appliances: Overseas Boom! Midea, TCL, Dreame Break Through; Casarte, Fotile, Gree, Hisense, Ronshen Lay Foundations

-

![]()

Aiming to Be the Alphard of the Electric Era! After D99's Launch, Leapmotor Will Release All-New Technologies to Pave the Way for a High-End Brand | Mirrormedia Pro

-

![]()

Over 5,200 Orders Placed on First Day: Can the Qijing GT7, Priced from 209,900 Yuan, Compete with the Z7 and SU7? | Mingjing Pro