Describing February's Auto Market in a Single Word: 'Frigid'

03/06 2026

03/06 2026

435

435

Introduction | Lead

The domestic auto market in February was notably sluggish, influenced by the extended Spring Festival holiday and other contributing factors. If the market fails to rebound in March, numerous automakers will face a daunting first half of the year. Previously, during the era of booming new energy vehicle (NEV) sales, many domestic brands and new entrants capitalized on the trend. However, with the overall market and NEV sector no longer experiencing rapid growth, and foreign automakers launching a new generation of NEV models, the auto market is poised for even more intense competition.

This article is produced by Heyan Yueche Studio

Written by Zhang Dachuan

Edited by He Zi

Full text: 2886 words

Reading time: 4 minutes

If one word were to encapsulate the domestic auto market in February this year, it would be 'frigid.' However, the market's complexity defies simple categorization.

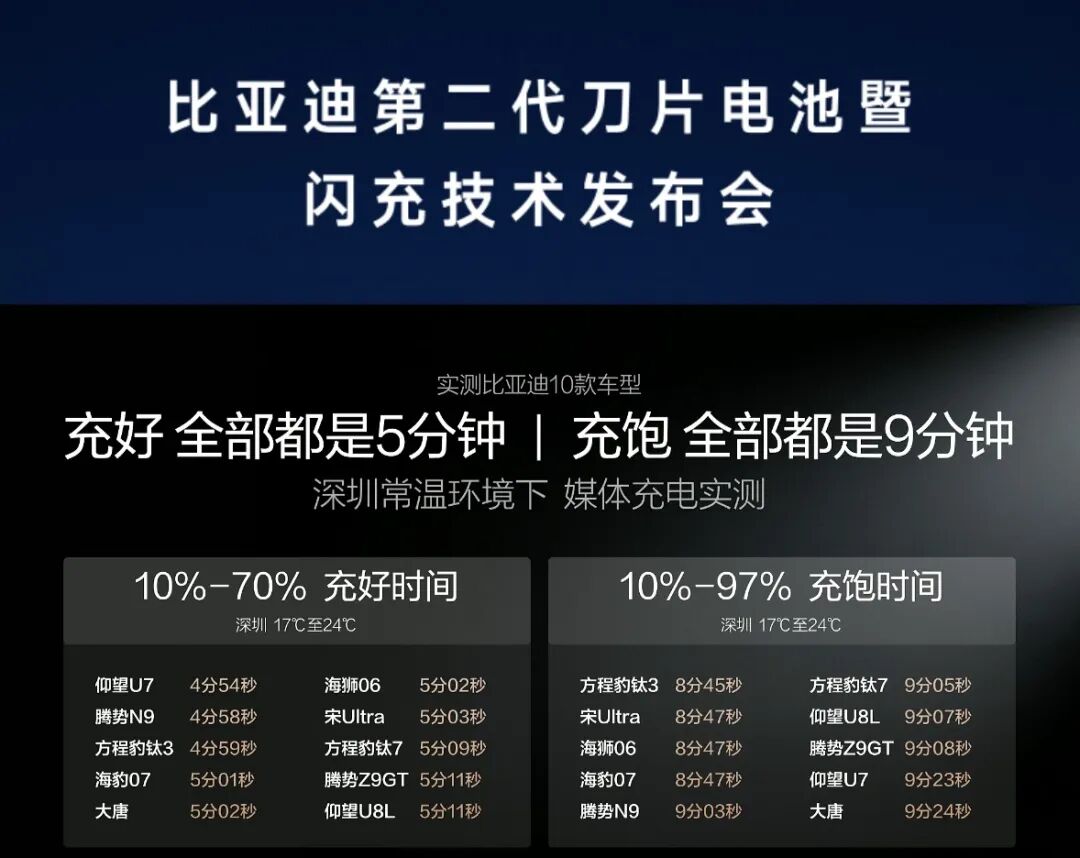

The extended Spring Festival holiday in February significantly curtailed production and sales time. Coupled with factors such as the adjustment of the NEV purchase tax policy at the beginning of the year and the anticipation of consumer spending (advanced consumption) at the end of last year, domestic automakers faced mounting pressure on sales volumes. To break free from the slump, BYD unveiled its second-generation blade battery, developed over six years, along with flash charging technology capable of charging in five minutes and reaching full capacity in nine minutes, on March 5. This move aims to address the pain points of NEVs and seek new growth avenues for electric vehicles.

△Rankings are based on sales volumes released by some automakers and do not represent the final standings.

Geely and BYD Engage in Fierce Rivalry

The competition between Geely and BYD has garnered significant attention, reminiscent of the classic rivalry between Zhou Yu and Zhu Geliang.

△Geely's sales volume surpassed BYD's for two consecutive months, claiming the top spot in domestic auto sales.

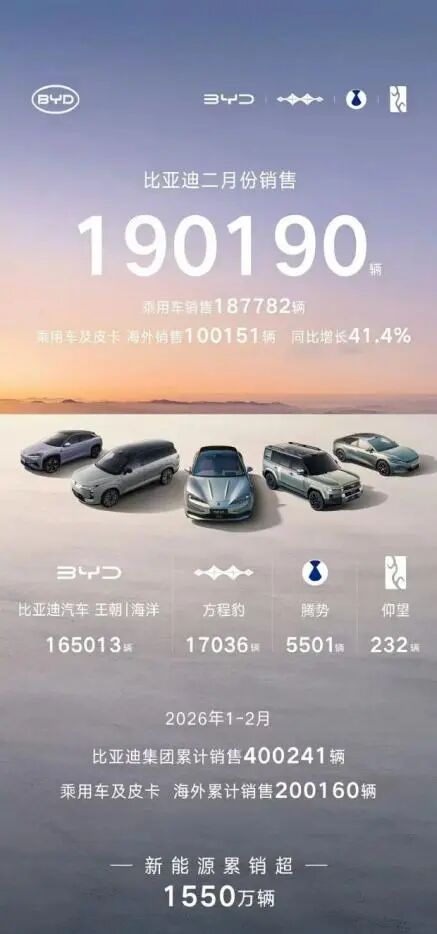

In recent years, BYD has dominated the global NEV race, leaving former independent brand leader Geely Automobile in its wake. In 2025, BYD's annual sales exceeded 4.6 million vehicles, with overseas sales surpassing 1 million, establishing it as a flagship of China's NEV sector. However, in the first two months of 2026, BYD experienced a sudden slowdown. In February, its overall sales volume declined by 35% year-on-year, with cumulative sales from January to February reaching 400,241 vehicles, a 35.80% decrease compared to the same period last year. Notably, BYD's February sales fell below 200,000 vehicles, a situation unprecedented in recent years.

In contrast, Geely's performance in the first two months of the year has bolstered its confidence in vying for the domestic auto market championship. Geely's success can be attributed to two main factors:

1. Parallel development of gasoline and NEVs. This year, the NEV purchase tax is no longer exempt but halved, with a 5% tax rate, indirectly benefiting gasoline vehicles. Geely's continuous updates to its gasoline vehicle models have given them an edge over joint-venture brand gasoline vehicles in terms of traditional components, in-vehicle connectivity, and driving assistance.

△Geely remains committed to the parallel development of gasoline and electric vehicles.

2. Collective efforts of multiple flagship models. The recent hot sales of three 9-series flagship models—Galaxy M9, Zeekr 9X, and Lynk & Co 900—have rapidly boosted Geely's market presence. In comparison, the attention garnered by multiple models under BYD, Denza, and Fangchengbao has been relatively limited.

△The hot sales of the three 9-series models have facilitated Geely's remarkable comeback.

Additionally, Geely Automobile's overseas sales volume (export sales) in February 2026 reached 60,879 vehicles, a year-on-year increase of approximately 138%. Overseas sales will be a key driver of Geely's growth in the coming period. It should be noted that Geely's overseas sales do not include the sales volumes of brands such as Volvo, Polestar, Proton (controlled by Geely), and Renault (using Geely's technology). Including these brands would undoubtedly enhance Geely's performance further.

New Force Auto Companies Face Collective Resistance

For domestic new force auto companies, 2026 promises to be even more challenging. The scenario where most automakers experienced rising sales volumes is unlikely to repeat.

Although Hongmeng Zhixing's overall sales volume reached 28,212 vehicles in February, this was the combined sales of its five brands. From an individual automaker perspective, Leapmotor had the highest sales volume among the new force auto companies. However, even so, neither company's monthly sales exceeded 30,000 vehicles. For Leapmotor, which has set an annual sales target of 1.05 million vehicles for this year, the pressure on terminal sales in the coming period will be immense. Hongmeng Zhixing, on the other hand, needs to address its unbalanced development. While Aito's performance, with a 15% year-on-year decline, can be considered average, the other four brands are significantly dimmer, especially Seres, which delivered only 945 vehicles in February and must carefully assess its issues.

△Hongmeng Zhixing's over-reliance on Aito remains unresolved.

Among the new forces, Zeekr and NIO stand out. Zeekr's sales volume has continuously increased with the launch of multiple main models. NIO, despite significant year-on-year improvement, relies heavily on the all-new ES8 model, which accounted for approximately 54.1% of its total deliveries in February (11,260 vehicles out of approximately 20,797). XiaoMI Auto's sales volume of 20,000 vehicles was primarily contributed by the YU 7 model. Looking ahead, with the launch of the all-new SU7 and multiple extended-range models, XiaoMI Auto's short-term sales prospects appear relatively optimistic.

△NIO's significant sales growth is entirely driven by the all-new ES8 model.

XPeng, which saw a nearly 50% year-on-year decline, has attracted considerable attention among mainstream new force auto companies. XPeng's previous hot sales were mainly driven by the M03 model in the MONA series. However, such models are highly susceptible to price wars. Once competitors launch lower-priced models, the M03's sales volume can easily be diverted. XPeng is now focusing on autonomous driving large models and actively cooperating with Volkswagen for research and development. These strategic directions are valid. However, XPeng must always return to its core business. Whether it can create several models like the all-new ES8, as NIO has done, will determine its future fate and direction.

△XPeng faces continuous competitive pressure.

Is the Overseas Market a Timely Lifesaver or Just Icing on the Cake?

Excluding the 100,600 overseas sales volume, BYD's domestic sales volume in February was only 89,600 vehicles. Chery's sales volume exceeded 160,000 vehicles, with export sales reaching 116,725 vehicles and domestic market sales only about 45,000 vehicles. Great Wall Motors' sales volume exceeded 70,000 vehicles, with overseas sales at 42,675 vehicles and domestic sales at 30,000 vehicles after calculation. Changan Automobile's overseas sales volume was 64,876 vehicles, corresponding to domestic sales of less than 90,000 vehicles. Geely, which performed relatively well, had an export volume of 60,897 vehicles, much lower than BYD and Chery in absolute terms and significantly lower than Great Wall and Changan in terms of sales proportion. Geely's domestic sales volume of 142,000 vehicles leads among local auto companies.

△The decline in BYD's domestic sales volume.

Since October 2025, BYD's domestic sales volume has been on a downward trend, with year-on-year declines of around 20%-30%. In January this year, the decline suddenly exceeded 50%, and in February, it exceeded 60%. For BYD, the sales alarm has sounded. To reverse its domestic market situation, BYD must either launch core technologies with generational advantages over its competitors or resort to price cuts again. However, under the policy guidance of opposing internal competition in China, the pressure to continuously lower prices is significant. Therefore, the new technologies released by BYD on March 5 will have a certain impact on its future sales volume.

△Launching new-generation technologies is crucial for BYD to re-establish itself as the leader in the domestic market.

For most domestic auto companies, 'going global' has been a buzzword in recent years. The intense internal competition in the domestic auto market has led many automakers to turn their attention to overseas markets, where competition is less intense and profit margins are relatively high. However, unfamiliar overseas markets present numerous uncertainties: different legal and regulatory requirements, business environments, labor relations due to cultural differences, the need to improve brand awareness, establish sales networks, and construct comprehensive system capabilities, etc. Every step is fraught with risks. Therefore, in the short term, overseas markets can only be icing on the cake for domestic auto companies and cannot provide timely assistance when they are in trouble.

In recent years, two crucial overseas markets, the European Union and Mexico, have successively imposed additional tariffs on complete vehicles exported by Chinese auto companies. Russia has also significantly increased the import vehicle scrappage tax rate, directly leading to an increase in the cost of Chinese exported vehicles. Therefore, while Chinese auto companies are vigorously exploring overseas markets, they must also stand firm in their home market. Chinese auto companies still have a long way to go to become truly global automakers. The idea of sweeping the globe overnight simply by relying on the advantages of NEVs is not realistic.

Comments

If sales volumes continue to remain sluggish, it is not ruled out that policies to promote automobile consumption will be successively introduced. However, the contradiction of overcapacity in the domestic auto industry remains prominent. Given that the domestic auto market cannot take another significant leap forward in size and trade barriers in overseas markets are becoming increasingly prominent, only by enduring market pain and eliminating some backward production capacity through benign competition can the auto industry return to a healthy ecosystem and allow innovative auto companies to usher in new development opportunities.

(This article is original to Heyan Yueche and may not be reproduced without authorization.)

-

![]()

The Unstoppable Rise of 'Optical Progress and Copper Decline': Sunny Optical’s Strategic Vision for the Next Decade

-

![]()

AI + Going Global in the Second Half: No Intermission for Robot Vacuum Cleaners

-

![]()

The Suffering Endured in E-commerce, Walmart Doesn't Want to Repeat in AI

-

![]()

What Does the Doubling of New Energy Vehicle Exports Mean?

-

![]()

Ghosn: 'Only I Can Save Nissan'

-

![]()

Volkswagen Lays Off 100,000 Employees, The Elephant Sits Down

-

![]()

Expanding Production Capacity! Yutong Optics Acquires Approximately 1.5 Hectares of Industrial Land in Chang'an, Dongguan

-

![]()

Why Is Nokia Making a Comeback in the AI Era?