Is the Start of the 15th Five-Year Plan Period the Most Opportune Time for the Automotive Industry?

03/10 2026

03/10 2026

460

460

Introduction

This year, recommendations and strategies concerning the automotive sector have shifted from broad, overarching themes to highly specific actions, marking a notable departure from previous approaches.

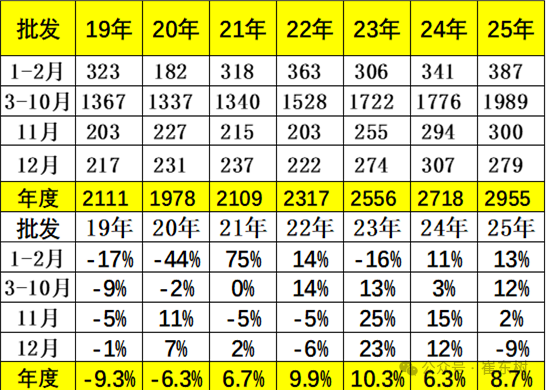

As the first natural week of March draws to a close, many are surprised to find that only three weeks remain until the end of the first quarter of 2026. Reflecting on the Chinese automotive market in January and February, the specter of declining sales has cast a shadow over all professionals in the field.

The challenge of catching up on sales targets over the next three quarters looms large. It is widely acknowledged that sales in the Chinese automotive market during January and February fell short of expectations. Consequently, the industry generally predicts a less-than-optimistic outlook for overall annual sales. For automakers, the question remains: Will March continue to be a sluggish period? Can they achieve their yearly targets?

A closer look at the data from various automakers reveals that, at any given stage, whether during peak or trough periods, there are always leaders in the pack. This is an inevitable outcome of market competition and the natural law of survival of the fittest. Thus, regardless of overall market conditions, the brands that endure are those that meet market demands.

Moreover, and more significantly, with the convening of this year's Two Sessions and the release of the work report, we have witnessed the relevant departments' emphasis on the automotive industry. This includes concerted efforts to address "involutionary" competition, support for major consumer expenditures such as automobiles and home appliances, a focus on high-quality automotive exports, intelligent technological advancements, and more. This year's recommendations and strategies regarding automobiles have delved into highly specific details, a departure from previous broad concepts. Particularly noteworthy is the emphasis on transitioning from scale expansion to quality and efficiency transformation. It is evident that the Chinese automotive industry is poised for a significant transformation this year.

This transformation not only benefits consumers but also reshapes the automotive industry. It is crucial to recognize that the Chinese automotive industry has been able to surpass foreign brands in just a few decades of development, largely due to its once-relentless pursuit of growth. Now, to become a global automotive powerhouse, it must inevitably enter a new phase characterized by higher quality.

01 Is March a Turning Point?

The start of the Chinese automotive market in 2026 indeed carries elements of both unpredictability and inevitability. Factors such as the expiration of year-end promotional policies from the previous year and the timing of the Spring Festival holiday have led consumers to adopt a wait-and-see attitude, which is understandable. This policy vacuum, compounded by the absence of a spring auto show season, has left the automotive industry feeling the chill of a delayed spring in terms of sales performance.

However, a review of OEM sales in January and February reveals that there have not been significant changes in the rankings among automotive groups or brands. Any changes that have occurred are merely positional swaps. Notably, strong automakers such as Geely, Chery, Xiaomi, HiMo, and Leapmotor have maintained solid sales growth.

This indicates that truly capable automakers often stand out in a downturn. A calm sea does not produce skilled sailors; in times of prosperity, everyone can stay ahead. Only in adverse conditions do automakers with scalable operational capabilities truly meet market demands.

Thus, even during what is considered a slow season, leading brands demonstrate resilience. They simply absorb market share from other brands, while those experiencing declines should feel increased pressure. If they cannot transform this pressure into motivation, elimination is only a matter of time.

Therefore, many in a declining market like to use the phrase: "Squatting deep is for a better jump." This aptly reflects the current state of the domestic automotive industry. The decline in January and February is not a loss of momentum but rather a squatting deep. Having navigated through such a challenging phase, the road ahead will be much smoother.

Moreover, as time returns to normal, macro, industrial, corporate, and consumer levels will also experience normal market cycle operations. Since late last year, various regions across the country have begun implementing trade-in subsidies and local consumption promotion policies, coupled with higher-level incentives, bringing automotive consumption back into the public eye.

In fact, promoting automotive consumption is not just a national-level intention. In this major commodity market, various automakers, as participants, are also giving it their all. According to relevant statistics, more than 15 new cars, including facelifts and all-new models, are set to launch in March, marking the arrival of a new round of new car dividends.

Another aspect is the flexibility of automakers' own promotions. Previously, we only knew about price reductions. Now, promotional tactics are diverse, with the most recently discussed being financial schemes such as 5-7 years of interest-free or low-interest financing, which will, to a certain extent, usher in a new era of consumption attitudes and meet the precise needs of the automotive market.

In addition to new cars and new promotional policies, companies such as XPeng, BYD, and Huawei have initiated a series of technology launches after the Spring Festival holiday. Breakthroughs in technology have led to the inclusion of affordable models, which will undoubtedly stimulate consumer willingness. The entry of a new wave of consumers will coincide with the introduction of these high-end yet affordable technology models into the market.

It is important to note that regardless of whether the auto market rises or falls this year, the total sales volume of Chinese automobiles will remain between 25-30 million units. Therefore, the issue is not about discussing what the automotive industry should do but rather which automaker has the capability to secure a larger share. This is the core of automotive industry development and the result of high-quality development.

So, will March be a turning point? Will the automotive industry recover in March? With the current pace of new car launches, technological announcements, coupled with relevant promotional and stimulative policies, even if March's auto market sales yield predictable and unpredictable results, they will pave the way for the entire year.

02 Is It Time for the Value War?

In recent years, various industries have been plagued by intense competition and a lack of innovation, a phenomenon known as "involution." The automotive industry, catering to both B-end and C-end consumers, is no exception. Coupled with the fact that automobiles are major commodities, professionals in the automotive industry feel this even more acutely. In recent years, there have been statements opposing involution, but it was only this year that it was officially included in the government work report.

Furthermore, it was written as "in-depth efforts to address involutionary competition," indicating that everyone is aware of the approximate total annual sales volume of the Chinese auto market, making it difficult to achieve new peaks. This is determined by the fundamental market conditions. Additionally, after years of involution in the automotive industry, price wars have ultimately prevailed, becoming the biggest drawback damaging the industry.

It is important to note that the profit margin of the Chinese automotive industry has dropped to a historical low of 4.1% in 2025. Automakers are not profitable in manufacturing and selling cars, upstream supply chains are not profitable, downstream auto dealerships are facing closures, and consumers are repeatedly disappointed by new car launches, leading to a severe lack of consumer confidence.

Therefore, we have recently seen a counter-trend news item: Chery has become the first automaker to raise prices this year. This individual case is sufficient to show that a significant number of automakers can no longer withstand sustained price wars. Price wars only lead to low-level industry development and fail to provide effective stimulation.

Thus, some automaker leaders have also raised their hands in agreement not to engage in price wars but instead to focus on technological wars, quality wars, service wars, and brand wars, hoping to enter the profit zone. However, when it comes down to it, whether it is a price war or the so-called value war, a key point is whether automakers have cost advantages and technological strength.

If automakers lack both, they cannot afford to engage in either price wars or value wars. Ultimately, Chinese automakers will face a process of survival of the fittest. There is no need to sympathize with the automakers that are eliminated; the winners are what the industry and consumers need the most.

This is why, in the past, relevant authorities could allow the Chinese automotive industry to grow rapidly. However, once the market share of domestic brands surpasses that of foreign brands, a new round of competition, as seen this year, will be implemented. Domestically, domestic brands must rise. The purpose of the upcoming value war is to go global and allow domestic brands to be seen by consumers worldwide.

In November last year, the Ministry of Commerce and three other ministries and commissions issued the "Notice on Further Strengthening the Management of Used Car Exports," which strictly controls the export of new cars under the guise of used cars starting from January 1, 2026, and promotes the establishment of overseas after-sales service networks, sending a clear signal of shifting from a "quantity-oriented" to a "quality-oriented" approach in overseas expansion.

There are also traces to follow behind this. In 2025, Chinese automobile exports exceeded 7 million units, ranking first globally for three consecutive years. However, behind this scale leap, issues such as high compliance costs, lack of overseas services, and disorderly competition have emerged. More often than not, this is a result of learning from history; scale expansion cannot be detached from quality control, which would undermine the industry's long-term competitiveness.

In fact, with the advent of the era of reverse joint ventures, Chinese automobile exports have also encountered the most opportune moment. When national-level top-level designs take the lead in building bridges and paving the way, they still provide a convenient gateway for competitive automakers, marking the best moment for Chinese automobiles to showcase a brand-new image.

Therefore, the critical time point of 2026, as the beginning of the 15th Five-Year Plan period, marks a turning point for the automotive industry from scale expansion to quality development. Chinese automobiles are no longer a market characterized by rapid but uncontrolled growth but have embarked on a path of meticulous cultivation. This is beneficial for both domestic and foreign brands.

Editor-in-Chief: Yang Jing Editor: He Zhengrong

THE END

-

![]()

The Unstoppable Rise of 'Optical Progress and Copper Decline': Sunny Optical’s Strategic Vision for the Next Decade

-

![]()

AI + Going Global in the Second Half: No Intermission for Robot Vacuum Cleaners

-

![]()

The Suffering Endured in E-commerce, Walmart Doesn't Want to Repeat in AI

-

![]()

What Does the Doubling of New Energy Vehicle Exports Mean?

-

![]()

Ghosn: 'Only I Can Save Nissan'

-

![]()

Volkswagen Lays Off 100,000 Employees, The Elephant Sits Down

-

![]()

Expanding Production Capacity! Yutong Optics Acquires Approximately 1.5 Hectares of Industrial Land in Chang'an, Dongguan

-

![]()

Why Is Nokia Making a Comeback in the AI Era?