Leapmotor: Can This Overseas-Bound 'Game-Changer' Really Lead New Forces with One Million Sales?

03/17 2026

03/17 2026

596

596

Leapmotor (09863.HK) released its Q4 2025 financial results after the close of Hong Kong trading on March 16 (Beijing Time). The report continued to show strong performance, reflecting Leapmotor's consistent and stable operational capabilities. Key highlights include:

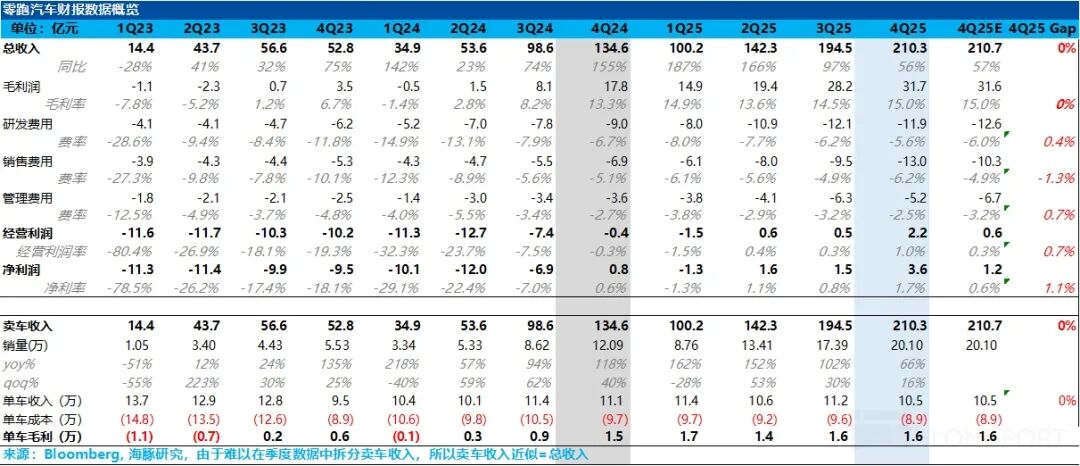

1. Revenue largely met expectations, though average selling price (ASP) declined quarter-over-quarter due to model mix shifts and promotions: This quarter's revenue reached RMB 21 billion, up 56% year-over-year and roughly in line with market expectations. However, ASP continued to decline quarter-over-quarter, primarily because Leapmotor intensified promotional efforts in Q4 and its model mix continued to shift toward lower-priced vehicles. The B-series and T-series models, which are more affordable, accounted for a rising share of sales.

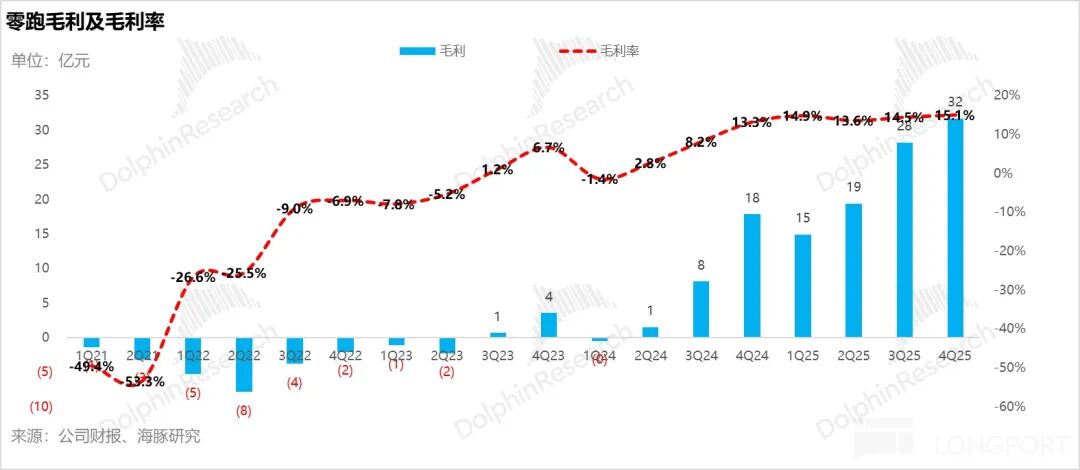

2. Gross margin improved quarter-over-quarter: Management previously guided that Q4 gross margin would remain flat quarter-over-quarter, as increased promotional efforts offset the positive impact of scale effects. However, gross margin actually rose slightly by 0.5 percentage points to 15%.

Dolphin Research attributes this primarily to: a) Leapmotor's consistent cost-reduction capabilities (through platformization and in-house R&D and production of components); b) the realization of scale effects; and c) the positive impact of other revenue streams on gross margin in Q4 (e.g., carbon credit revenue likely doubled quarter-over-quarter due to accelerated overseas expansion).

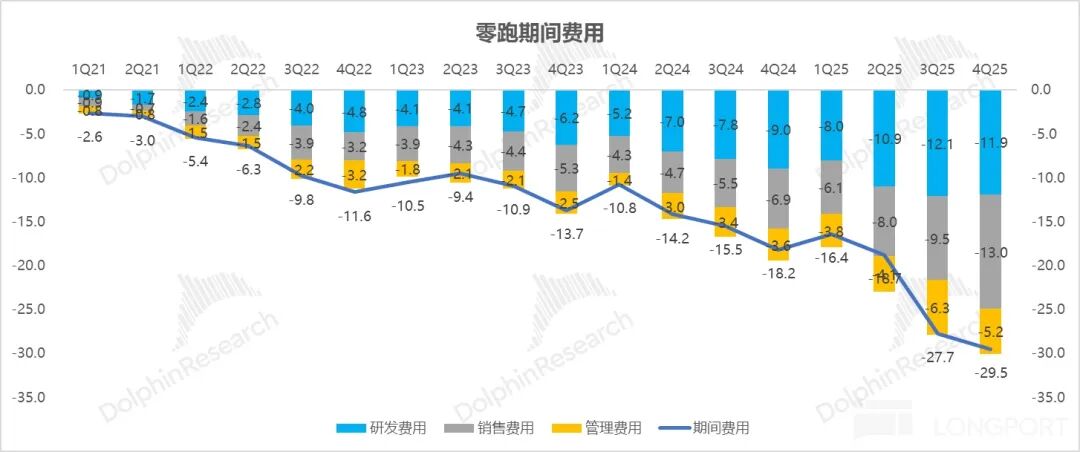

3. Sales expenses increased, while R&D and administrative costs were controlled: In Q4, Leapmotor's sales expenses reached RMB 1.3 billion, a significant quarter-over-quarter increase (up RMB 350 million), mainly due to higher advertising spending and expanded sales networks. However, R&D and administrative expenses were well-controlled and even decreased slightly quarter-over-quarter. Despite ongoing R&D investments in intelligence, deepening in-house component development, and new model launches (D/A-series), R&D expenses fell by RMB 20 million quarter-over-quarter to RMB 1.19 billion, reflecting high R&D efficiency.

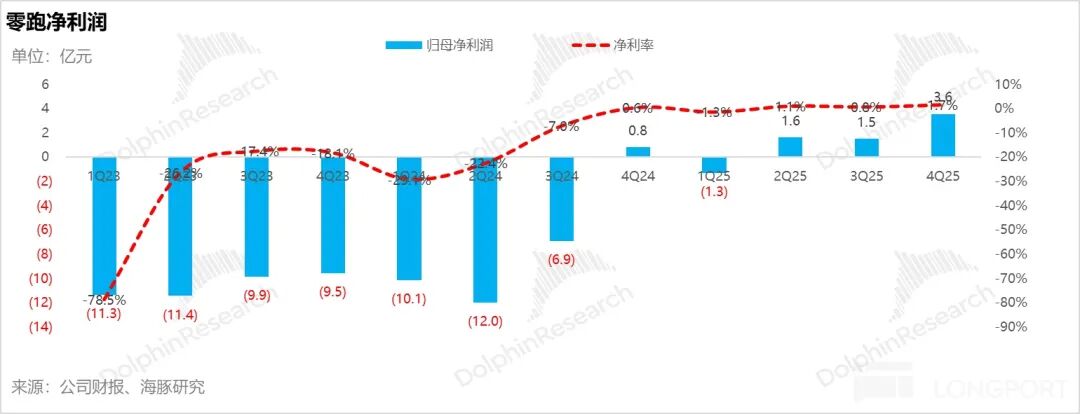

4. Operating and net profits continued to rise quarter-over-quarter: Operating profit reached RMB 220 million, up RMB 170 million quarter-over-quarter. Despite increased sales expenses, reasonable control of R&D and administrative costs, along with improving gross margin, leverage effects from higher sales volume, and increased investment income from joint ventures, drove net profit to RMB 360 million, exceeding market expectations by RMB 120 million.

Dolphin Research's View:

Overall, Leapmotor delivered a solid Q4 performance that met expectations. Although management had previously guided for flat quarter-over-quarter gross margin due to intensified promotions, the actual margin improvement reflects Leapmotor's strong cost-control capabilities and the growing contribution of carbon credit revenue from accelerated overseas expansion.

More importantly than Q4 results, however, is the market's outlook for Leapmotor in 2026:

① Q1 2026 margin pressure to persist due to model mix shifts and promotions:

In Q1, Leapmotor's sales for January-February reached only 60,000 units (average monthly sales of 30,000 units), a sharp decline from Q4 2025's average of 67,000 units per month and only a 19% year-over-year increase. Key factors include:

a) Dealer inventory reductions ahead of the Q1 2026 launch of the 'A10' SUV;

b) Demand being pulled forward into Q4 2025 ahead of the implementation of a new 5% vehicle purchase tax policy for new energy vehicles (NEVs) in Q1 2026; and

c) Reduced government trade-in subsidies. The revised 2026 subsidy program shifted from a flat subsidy across price tiers (as in 2025) to a proportional subsidy, reducing support for mid-to-low-end models priced below RMB 150,000.

Additionally, while the new trade-in policy took effect on January 1, 2026, local government subsidy rollouts varied (e.g., Hubei on January 15, Jilin on January 17), causing some potential buyers to delay purchases. In response, the company increased promotional efforts and offered purchase tax support policies to boost Q1 sales.

The rising share of low-priced models like the T03 in Leapmotor's mix (increasing from 11% in Q4 to 27% in January-February 2026) will further depress ASPs. Combined with weakening scale effects from lower sales volume, Dolphin Research expects margin pressure to persist in Q1.

However, the growing share of overseas sales (24,000 units in January-February 2026, accounting for 40% of total sales, up from 14.6% in Q4 2025) could partially offset margin declines.

② Looking beyond Q1's seasonal slowdown to the full year 2026:

Leapmotor plans to launch four new models and two facelifts in 2026, further enriching its product lineup:

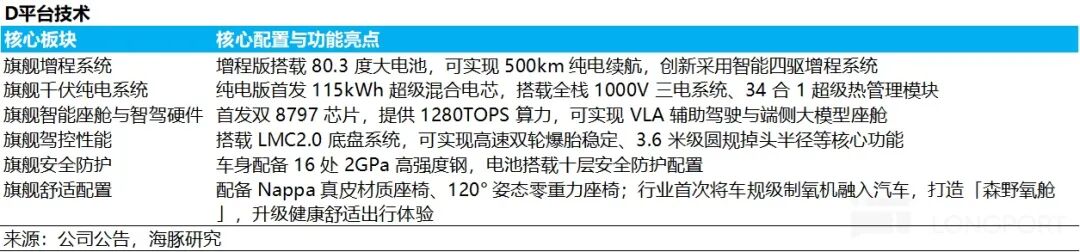

a) Premium D-series (models priced above RMB 200,000): This platform is key to Leapmotor's brand upscaling and model mix improvement, featuring six core technologies such as large-battery extended-range systems, 1000V high-voltage platforms, and 1280TOPS high-computing-power autonomous driving chips. The first model, the full-size 'D19' SUV, will launch in April 2026, followed by the large 'D99' MPV.

b) Volume-focused A-series: The compact 'A10' SUV (launching in March) and small 'A05' hatchback will target the RMB 100,000 price segment, driving sales expansion.

c) B-series facelifts: Annual updates for the B01 and B10 models are expected in Q2 2026.

Management has set a 2026 sales target of one million units (100,000-150,000 overseas, 850,000-900,000 domestic). If achieved, net profit could reach RMB 5 billion (net margin of nearly 5%).

The market's main concerns about Leapmotor center on whether it can achieve near-doubling of sales volume, with three key worries:

a) Tightening policy environment: The restoration of a 5% NEV purchase tax in 2026 and the shift to proportional trade-in subsidies (reducing effective support for models under RMB 150,000) may suppress overall demand, particularly impacting Leapmotor's core price segment.

b) Worsening competition: Leapmotor's key battleground (RMB 100,000-200,000) will see new model launches from Geely, Great Wall, XPeng, and others in 2026, intensifying market competition into a 'zero-sum game' as marginal benefits from NEV substitution and domestic brand substitution weaken.

c) Extremely high growth base: Jumping from ~600,000 units in 2025 to 1-1.1 million in 2026 requires near-doubling sales (68%-84% year-over-year growth), a daunting task against the backdrop of slowing overall NEV industry growth (estimated at 5%-15% year-over-year).

Dolphin Research believes that despite these challenges, Leapmotor has structural advantages that could drive outperformance:

a) Strong overseas expansion determinism among new forces:

Leapmotor stands out among new forces for its high certainty in overseas expansion, supported by its channel and brand strength through partnership with Stellantis. The company continued to rapidly expand its overseas sales network in Q4, reaching ~900 outlets by the end of 2025 (nearly 90% in Europe). The B-platform and A-platform models are well-suited to European demand for affordable small cars, enhancing overseas expansion certainty.

Synchronized capacity deployment: A European CKD plant is scheduled to start production in October 2026 (initial production of B10), with a matching battery pack plant set to begin mass production in July 2026. The Malaysia KD plant is progressing smoothly, and expansion in South America using Stellantis' existing facilities is under evaluation. This complete 'channels + capacity + supply chain' localization system lays a solid foundation for achieving the 2026 overseas sales target of 100,000-150,000 units.

Leapmotor has already sold 24,000 overseas units in January-February 2026, completing 16%-24% of its full-year target, suggesting the 100,000-150,000 goal is well within reach.

b) Vertical integration-driven cost control advantages amid rising industry costs:

Leapmotor currently achieves in-house R&D and production for components accounting for 65% of total vehicle costs, with deep control over core systems (excluding battery cells), intelligent driving, and smart cockpits.

The company aims to increase its self-sufficiency ratio to 80% by 2026 and plans to bring battery cells in-house, further reducing reliance on external suppliers and strengthening cost control. This deep vertical integration capability enables sustain cost reductions and the launch of high-cost-performance models, providing an edge amid rising industry costs.

c) Recognition of carbon credit revenue:

Due to the 2025-2027 European carbon emissions regulatory window, Leapmotor's EV sales in Europe generate carbon credit revenue (agreement signed in June 2025). This revenue is essentially pure profit (similar to Tesla's model), boosting Leapmotor's revenue and gross margin (transaction cap of RMB 1.5 billion).

d) Potential for technology licensing revenue:

Leapmotor's current technology licensing primarily involves collaboration with FAW. If Leapmotor can expand this model to license its electronic architecture to other automakers, technology licensing revenue could become a recurring income stream. *For more detailed analysis, see the same name article in the 'Insights - Deep Dive (Research)' section of the Longbridge App.

Here's a detailed analysis:

1. Q4 gross margin rose slightly quarter-over-quarter

Leapmotor's Q4 results drew significant investor attention to automotive business gross margin, as vehicle sales volume had already been disclosed. Management previously guided for flat quarter-over-quarter gross margin in Q4, as intensified promotions would offset scale effect benefits.

However, actual Q4 gross margin reached 15%, up 0.5 percentage points quarter-over-quarter and slightly above management guidance. This was primarily due to the company's sustained strong cost-reduction capabilities and increased recognition of high-margin carbon credit revenue from strong overseas sales in Q4 (estimated RMB 500+ million vs. RMB 250 million in Q3).

PS: Leapmotor's revenue consists mainly of ① automotive revenue and ② service and other sales revenue, but the company does not disclose these segments quarterly. Thus, Dolphin Research analyzes based on total revenue.

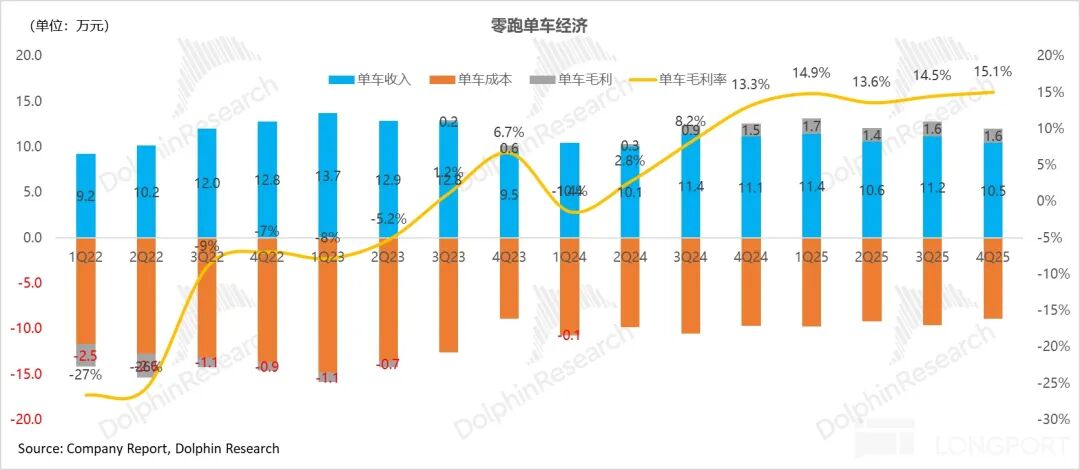

From a per-vehicle economics perspective (including service and other revenue):

a) ASP declined quarter-over-quarter to RMB 105,000:

Q4 ASP fell by RMB 7,000 quarter-over-quarter to RMB 105,000. Despite higher carbon credit revenue recognition this quarter, actual vehicle ASPs continued to decline, primarily due to model mix shifts and promotional discounts.

① Increased promotional discounts:

In Q4, local government subsidies in many regions declined earlier than expected. As 2025 national subsidies provided a flat amount, the subsidy proportion was relatively higher for low-priced models, making their market more sensitive to subsidy reductions.

To address demand pressure, Leapmotor increased terminal promotions for its older C-series and T-series models. It also offered competitive purchase subsidies for the newly launched Lafa 5, with direct cash discounts pulling down the average ASP.

② Continued model mix shifts toward lower-priced vehicles:

In Q4, the higher-priced C-series accounted for 49% of sales, down 7 percentage points quarter-over-quarter, while the lower-priced B-series and T-series rose by 5.3 and 1.8 percentage points to 40% and 11%, respectively. This mix shift depressed ASPs.

③ Rising overseas sales share boosted carbon credit revenue:

Overseas sales reached 29,000 units in Q4, accounting for 14.6% of total sales (up 4.6 percentage points quarter-over-quarter). The strong overseas sales growth increased recognition of high-margin carbon credit revenue (estimated RMB 500+ million in Q4 vs. RMB 250 million in Q3).

While exported models typically command higher pricing (due to fewer domestic promotions), Leapmotor's Q4 export mix still focused on low-priced T03 models (47% share), diluting their price-lifting effect. The increased carbon credit revenue failed to fully offset the downward pressure from the domestic sales mix shift.

b) Actual per-vehicle cost fell to RMB 89,000, with scale effects driving cost reductions:

Actual per-vehicle production costs declined by RMB 7,000 quarter-over-quarter to RMB 89,000. The main cost-reduction drivers included:

a. Leapmotor continued its explosive sales growth, with a 16% month-over-month increase to 200,000 units, driving down the fixed cost per vehicle.

b. Leapmotor still maintains strong cost-reduction capabilities: With a parts commonality rate of nearly 88%, along with advantages in high self-developed components and vertical integration, Leapmotor continues to achieve scaled production and consistently lower unit costs.

c) Actual gross profit per vehicle stood at RMB 16,000, remaining largely flat quarter-over-quarter.

In Q4, the actual gross profit per vehicle remained at RMB 16,000, largely flat quarter-over-quarter. Although the average selling price continued to decline, Leapmotor's sustained cost reductions drove a slight 0.5 percentage point quarter-over-quarter increase in gross margin to 15%.

II. Sales expenses surged, while R&D and administrative costs remained restrained.

In R&D, Leapmotor persists with full-domain self-development, while on the sales front, it continues to expand its dealer network in preparation for increased sales volumes of B-platform and A-platform models. Sales expenses rose significantly quarter-over-quarter this period, but R&D and administrative costs were reduced. Details are as follows:

1) R&D expenditure: Focused on intelligence, vertical integration, and new model development.

In Q4, Leapmotor's R&D expenses reached RMB 1.19 billion, down RMB 20 million quarter-over-quarter and below market expectations of RMB 1.26 billion. Despite a slight contraction in absolute investment, the company maintains high R&D efficiency, primarily focusing on new model development, deepening its self-developed system, intelligence advancements, and platform capability building:

a. New model development: In Q4, the company officially launched its flagship "D Platform," representing its highest technological level, and showcased six core technological benchmarks, including: extended-range versions with large batteries, 1000V high-voltage platforms, and 1280TOPS high-computing-power intelligent driving chips. This platform is key to Leapmotor's brand positioning upgrade and model mix improvement. The first model based on this platform, the full-size SUV "D19," will launch in April 2026, followed by the large MPV "D99."

b. Self-developed components and vertical integration advantages: Currently, Leapmotor's self-developed components cover 65% of the vehicle's cost structure, achieving deep control over core powertrain systems (excluding battery cells), intelligent driving, and smart cockpits.

As planned, the company aims to increase its self-developed and self-supplied proportion to 80% by 2026 and plans to include battery cells in its self-developed system. This will further reduce reliance on external suppliers, enhance cost control capabilities, and the deep vertical integration capability is also why cost reductions continue to exceed market expectations.

c. In intelligence, Leapmotor is firmly committed to the end-to-end large model technology route and is exploring cutting-edge directions such as VLA (Vision-Language-Action). Previously, Leapmotor planned to achieve end-to-end-based urban NOA (combined assisted driving) capabilities by the end of 2025. Currently, its main models have achieved urban memory navigation (vehicles remembering fixed routes) and highway NOA, still striving to catch up in intelligence progress. Leapmotor aims to complete the development of its intelligent driving base model by the end of 2026, reaching industry-leading levels in intelligent driving capabilities.

d. Platform-based and standardized design: Leapmotor features a highly standardized battery platform design, with far fewer battery pack SKUs than competitors, reducing supply chain and production costs.

Leapmotor's self-developed Leap 3.5 architecture (A/B/C/D platforms) achieves an 88% commonality rate for core components. This not only shortens the new model development cycle by 25% compared to the previous generation and reduces overall vehicle R&D investment by 40% but also continuously lowers unit costs through scaled procurement and production of components.

2) Sales expenses: The significant quarter-over-quarter increase was primarily due to increased advertising efforts and simultaneous expansion of the sales network.

Leapmotor's Q4 sales expenses reached RMB 1.30 billion, significantly exceeding market expectations of RMB 1.03 billion and increasing by RMB 350 million quarter-over-quarter from Q3. The Exceeding expectations growth in expenses primarily stemmed from the company's efforts to support its aggressive global sales targets for 2026, including simultaneous domestic channel expansion, overseas network layout, and brand marketing investments.

a. Domestic channels: Accelerated expansion into lower-tier cities to pave the way for "volume models." The company is advancing its domestic sales network construction at a faster-than-expected pace, primarily penetrating fourth- and fifth-tier cities.

In Q4, the domestic retail network net increased by approximately 84 stores, accelerating from the 60-store net increase in Q3. By the end of 2025, the total number of domestic sales outlets had reached 950, largely meeting the annual target set by management.

As planned, the company aims to expand its sales network to over 1,500 outlets by 2026, implying the addition of approximately 550 new outlets and continuing to accelerate expansion (255 new outlets added in 2025).

This round of channel expansion and rapid growth primarily aims to pre-establish extensive sales and service touchpoints for entry-level B-series models and the A-series models set to target the RMB 100,000 price segment in 2026, serving as a pre-investment to support the goal of achieving one million domestic sales in 2026.

b. Overseas layout: Focused on Europe, with simultaneous capacity and channel rollouts.

Channel expansion: By the end of 2025, Leapmotor's overseas sales outlets reached 900, with over 800 in Europe, over 50 in Asia-Pacific, and over 30 in South America. Europe remains Leapmotor's primary battleground for overseas expansion.

Capacity preparation: The company has completed site selection for its European Completely Knocked Down (CKD) assembly plant, with production scheduled to begin in October 2026 (B10 to be launched first, with B05 expected to start trial production in June 2026 and official production in 2027). Meanwhile, the Malaysian Knocked Down (KD) assembly plant is progressing smoothly, and the possibility of building a new plant in South America using existing facilities of partner Stellantis is being evaluated.

The battery plants supporting B10 and B05 have also completed site selection and are currently undergoing factory renovations, with trial production of the first battery pack scheduled for April 2026 and official mass production starting in July.

Leapmotor also expects its overseas sales target for 2026 to be 100,000-150,000 units, with 70%-80% expected to come from the European market. The product positioning of the B-platform and the upcoming A-platform models aligns highly with the European market's demand for cost-effective, compact electric vehicles, further enhancing the certainty of its overseas sales growth.

The joint venture, Leapmotor International, achieved annual profitability in 2025, generating approximately RMB 670 million in investment returns for the company.

Operating profit reached RMB 220 million this quarter, continuing to rise by RMB 170 million quarter-over-quarter. Although sales expense investments are still increasing, R&D and administrative costs are reasonably controlled. Additionally, the leverage effect from increased sales volumes and higher investment returns from the joint venture contributed to a net profit of RMB 360 million, exceeding market expectations by RMB 120 million.

- END -

// Reprint Authorization

This article is an original work by Dolphin Research. Reprinting is prohibited without authorization.

// Disclaimer and General Disclosure

This report is for general comprehensive data purposes only, intended for general reading and data reference by users of Dolphin Research and its affiliated institutions. It does not consider the specific investment objectives, investment product preferences, risk tolerance, financial status, or special needs of any individual receiving this report. Investors must consult with independent professional advisors before making investment decisions based on this report. Any person making investment decisions using or referring to the content or information in this report assumes all risks. Dolphin Research shall not be liable for any direct or indirect responsibilities or losses that may arise from using the data contained in this report. The information and data in this report are based on publicly available sources and are for reference purposes only. Dolphin Research strives to ensure but does not guarantee the reliability, accuracy, and completeness of the information and data.

The information or viewpoints mentioned in this report shall not, under any jurisdiction, be considered or construed as an offer to sell securities or an invitation to buy or sell securities, nor shall they constitute recommendations, solicitations, or endorsements of relevant securities or related financial instruments. The information, tools, and data in this report are not intended for or to be distributed to jurisdictions where distribution, publication, provision, or use of such information, tools, and data contradicts applicable laws or regulations or requires Dolphin Research and/or its subsidiaries or affiliated companies to comply with any registration or licensing requirements in such jurisdictions, nor to citizens or residents of such jurisdictions.

This report reflects only the personal viewpoints, insights, and analytical methods of the relevant creators and does not represent the stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, with copyright solely owned by Dolphin Research. No institution or individual may, without the prior written consent of Dolphin Research, (i) make, copy, reproduce, duplicate, forward, or create any form of copies or reproductions in any manner, and/or (ii) directly or indirectly redistribute or transfer to other unauthorized persons. Dolphin Research reserves all related rights.

-

![]()

The Unstoppable Rise of 'Optical Progress and Copper Decline': Sunny Optical’s Strategic Vision for the Next Decade

-

![]()

AI + Going Global in the Second Half: No Intermission for Robot Vacuum Cleaners

-

![]()

The Suffering Endured in E-commerce, Walmart Doesn't Want to Repeat in AI

-

![]()

What Does the Doubling of New Energy Vehicle Exports Mean?

-

![]()

Ghosn: 'Only I Can Save Nissan'

-

![]()

Volkswagen Lays Off 100,000 Employees, The Elephant Sits Down

-

![]()

Expanding Production Capacity! Yutong Optics Acquires Approximately 1.5 Hectares of Industrial Land in Chang'an, Dongguan

-

![]()

Why Is Nokia Making a Comeback in the AI Era?