The Automotive Market's 'New Darling' Has Made Its Debut

03/17 2026

03/17 2026

584

584

Regional Disparities

Hainan leads the pack in terms of the highest proportion of new energy vehicles. Surprisingly, the runner-up isn't Beijing, Shanghai, Guangzhou, Shenzhen, or the regions typically associated with high vehicle ownership—Jiangsu and Zhejiang. When it comes to C-class vehicles, Beijing takes the crown, followed by Shanghai, with the third-place finisher being quite unexpected.

China's vast expanse, varied topography, along with the influences of climate, economic conditions, consumption levels, licensing policies, and the development of the local automotive industry, have all contributed to significant differences in automobile consumption preferences across different provinces and cities.

The old stereotype of Beijing being dominated by Mercedes-Benz, BMW, and Audi, Northeast and Shandong preferring Volkswagen, and Jiangsu and Zhejiang favoring luxury cars is fading into a distant memory. According to national automobile consumption landscape statistics from a third-party platform, in addition to Beijing's continued love affair with traditional luxury cars like the Audi A6L and Mercedes-Benz GLC, models such as the Model Y, Qin PLUS, and Xiaomi SU7 have emerged as the 'new darlings'.

In regions like Tianjin, Inner Mongolia, and Heilongjiang, the BYD Qin PLUS enjoys a clear advantage. In areas including Shanxi, Hebei, Anhui, Jiangxi, Shandong, Henan, Hubei, Guangxi, and Yunnan, cost-effective compact cars are the mainstream choice, with models like the Hongguang MINI EV, Seagull, Xingyuan, and Geely Panda leading the sales charts. In economically developed regions such as Guangdong, Zhejiang, Jiangsu, and Shanghai, the Model Y and Xiaomi SU7 rank among the top three in sales.

A recent report from the China Passenger Car Association (CPCA) highlights that economic development, diversified domestic demand, and export expansion have reshaped the regional automotive market structure.

For instance, driven by 'two new' subsidies, A00-class vehicles have performed exceptionally well in North and Northeast China, while A0-class electric vehicles have witnessed robust growth in most regions. Policy subsidies have primarily benefited economical electric vehicles, reflecting the core principle of policy fairness. Therefore, encouraging the development of small and micro electric vehicles through subsidies holds great significance for the widespread adoption of electric vehicles.

Meanwhile, due to the relatively high new energy subsidies in the national 'two new' subsidies for 2025, the entry-level sedan market has experienced a rebound. In flat regions such as Shandong, Henan, and Hebei, pure electric sedans have developed relatively strongly, with mid-to-low-end products becoming the mainstream.

A more pronounced trend is the continuous increase in the market share of Chinese brands across all provinces, with once-dominant joint-venture and luxury brands gradually taking on a supporting role. From the current landscape, the era of a single model dominating the market is over, and China's automotive market has begun to embrace 'regional differentiation'. Additionally, trends such as strong SUV demand in the central and western regions, increased adoption of pure electric vehicles in the north, and the accelerated replacement of joint ventures by domestic brands are becoming increasingly apparent.

Significant Shifts in Powertrain Structure

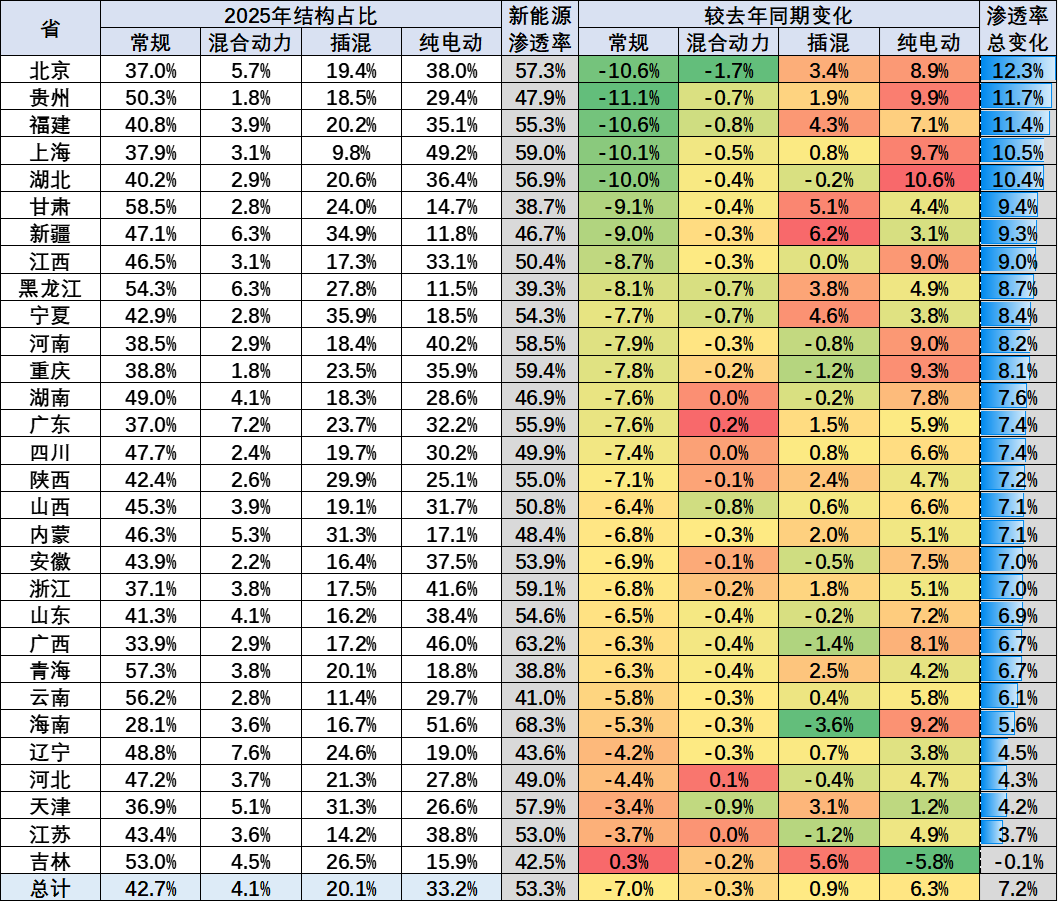

The regional pattern of 'plug-in hybrids complementing the north and pure electrics leading the south' underwent some notable changes in 2025. According to a CPCA report, although plug-in hybrids continued to perform well in 2025, pure electric models demonstrated overwhelming growth in most provinces and cities.

Image Source: China Passenger Car Association

From January to July 2025, plug-in hybrid growth remained relatively robust in the north and northwest, with Jilin Province witnessing a 5.7% year-on-year increase in market share, Heilongjiang 5.4%, Liaoning 2.4%, and Beijing 3.0%. In provinces such as Ningxia, Xinjiang, Qinghai, and Gansu, plug-in hybrid market share increased by 7.7%, 7.6%, 5.1%, and 6.4%, respectively.

Subsequently, plug-in hybrid growth slowed significantly in many regions. In 2025, Beijing, Jilin, Heilongjiang, and Liaoning saw plug-in hybrid market share increase by 3.4%, 5.6%, 3.8%, and 0.7%, respectively, while Ningxia, Xinjiang, Qinghai, and Gansu saw increases of 4.6%, 6.2%, 2.5%, and 5.1%, respectively.

In contrast, for pure electric vehicles, only four regions saw market share increase by more than 9% from January to July 2025, but by the end of 2025, seven regions had witnessed such growth, with many regions showing increases.

According to CPCA analysis, this is largely attributable to subsidy policies encouraging adoption. With an aging population, a shrinking construction industry, and a high-end shift in export industries, there has been a noticeable回流 of northern migrant workers, while consumption among institutional and civil servant sectors has remained relatively strong. This aligns with national 'trade-in' and 'scrappage update' subsidies favoring mid-to-low-end products, making high-cost-performance A00-class small cars and A0-class electric vehicles particularly appealing to budget-conscious car buyers.

With advancements in battery technology and a collective price drop in pure electric vehicles, the advantage of plug-in hybrid models replacing fuel vehicles due to cold northern weather has been increasingly diminished.

According to CPCA data from 30 regions, in 2025, only Jilin Province saw a year-on-year decline in pure electric vehicle market share, while ten regions saw declines in plug-in hybrid market share. From January to July 2025, only Hainan and Jiangsu saw plug-in hybrid market share decline.

The noticeable increase in pure electric vehicle market share has also driven changes in new energy vehicle penetration rates. In eastern plain regions, especially in the south, new energy vehicles now account for over 50% of the market, with Sichuan and Hebei approaching 50%.

Notably, Hainan and Guangxi have the highest new energy vehicle market shares at 68.3% and 63.2%, respectively. Shandong, Jiangsu, Hubei, and Ningxia all exceed 50%, while Beijing, Shanghai, Zhejiang, Henan, and Tianjin are close to 60%.

Consumption Patterns Embrace Rationality

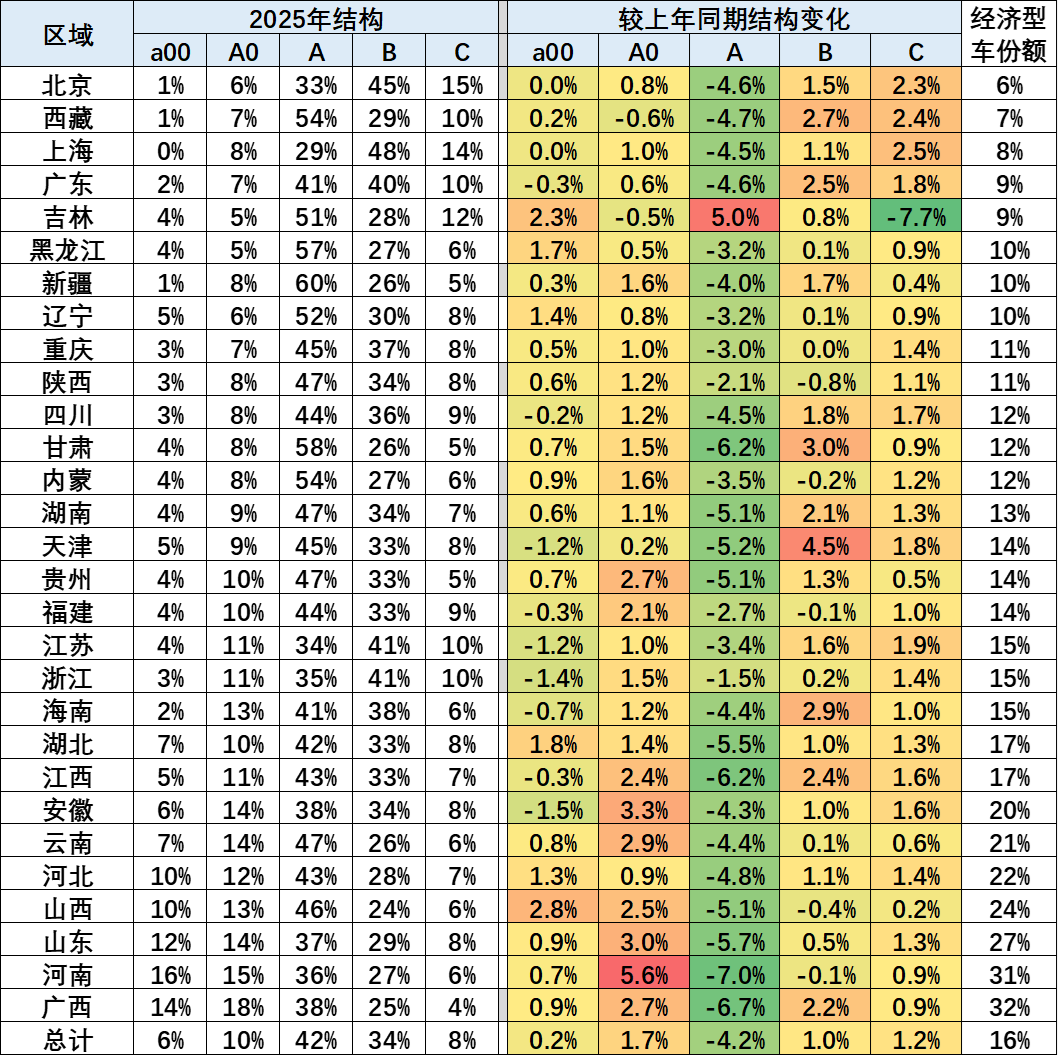

From a model structure perspective, the implementation of 'two new' subsidy policies in most regions has had the most significant impact on economical vehicles.

A00-class models have witnessed notable growth in Jilin, Hubei, and Shanxi provinces, while A0-class models have gained more market share in Guizhou, Fujian, Jiangxi, Anhui, Yunnan, Shanxi, Shandong, Henan, and Guangxi. Henan Province saw the largest increase, with A0-class market share rising 5.6% year-on-year.

Image Source: China Passenger Car Association

For A-class vehicles, except for Jilin Province, which saw a 5.0% year-on-year increase in market share, other regions experienced varying degrees of decline. Henan saw the largest drop at 7.0%, while Guangxi, Gansu, and Jiangxi all saw declines exceeding 6%. For B-class vehicles, Tianjin saw the strongest growth at 4.5%, followed by Gansu at 3.0%, with Tibet, Guangdong, Hunan, Hainan, Jiangxi, and Guangxi all seeing year-on-year increases exceeding 2%.

Another notable change in Jilin Province is the trend of C-class vehicles. Unlike the growth trend of A-class vehicles, Jilin is the only region where C-class vehicle market share declined, dropping by 7.7%. Other regions, except for Beijing, Tibet, and Shanghai, which saw increases exceeding 2%, experienced varying degrees of slight growth. Nevertheless, Jilin's C-class vehicles still rank in the top three with a 12% market share, behind Beijing's 15% and Shanghai's 14%.

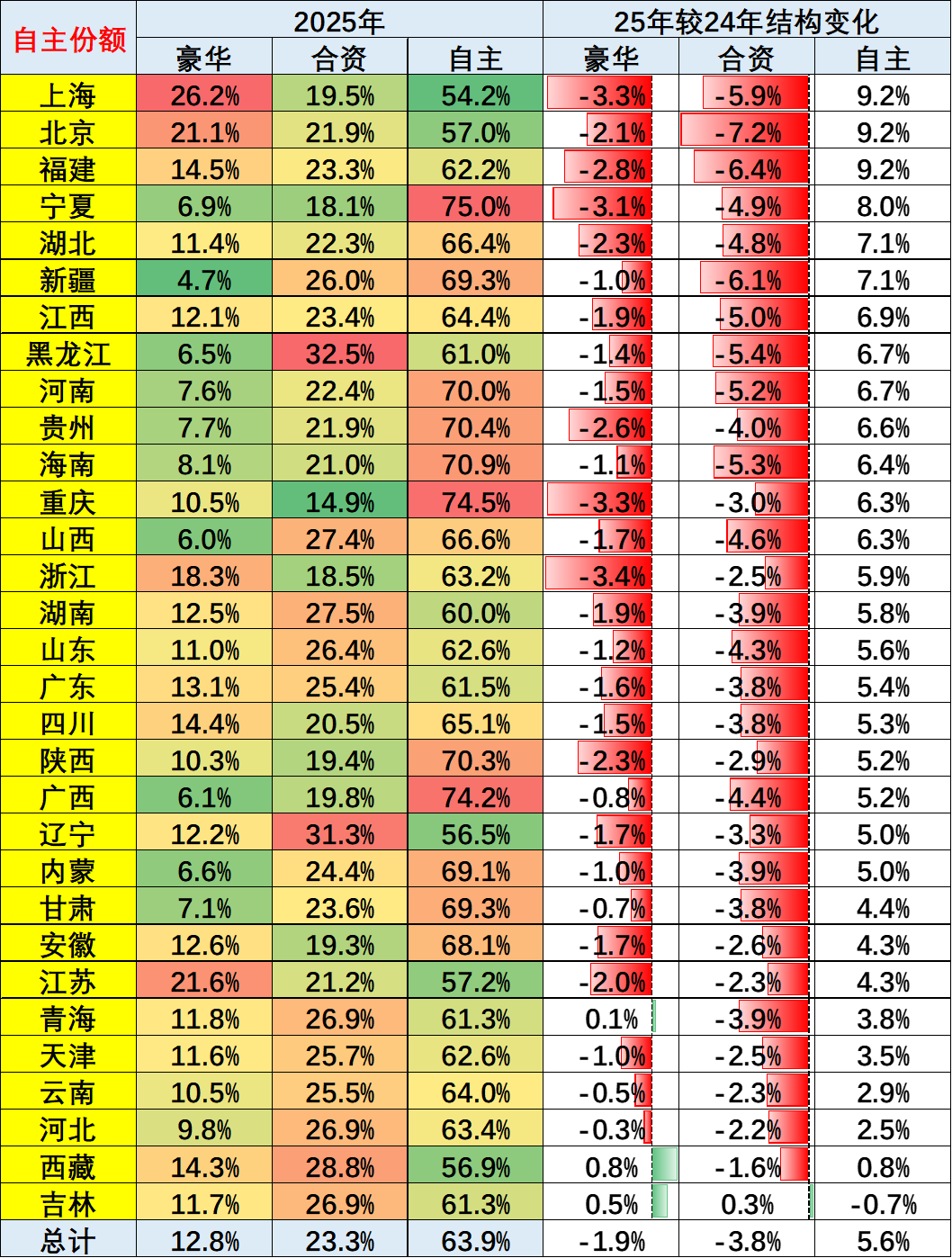

Additionally, in 2025, Jilin Province's market shares for luxury, joint-venture, and Chinese brands were 11.7%, 26.9%, and 61.3%, respectively. Luxury and joint-venture brands saw slight increases of 0.5% and 0.3%, respectively, while Chinese brands experienced a 0.7% year-on-year decline, making Jilin the only region where Chinese brand market share fell.

Regions with relatively high luxury brand market shares, such as Beijing (21.1%) and Jiangsu (21.6%), saw declines exceeding 2%. Zhejiang (18.3%), Chongqing (10.5%), and Shanghai (26.3%) saw the largest drops, all exceeding 3%. For joint-venture brands, Jilin was the only region with positive market share growth. Currently, only Heilongjiang and Liaoning have joint-venture brands accounting for over 30% of the model structure.

Image Source: China Passenger Car Association

For Chinese brands, except for Beijing, Shanghai, Tibet, Liaoning, and Jiangsu, other regions have market shares exceeding 60%, with Ningxia, Chongqing, and Guangxi having the highest shares at 75%, 74.5%, and 74.2%, respectively.

According to CPCA analysis, Shanghai and Beijing have relatively high luxury car market shares. In 2025, with the rapid development of Chinese brands, luxury brand market share declined significantly, while joint-venture brand share fell below luxury brand share in major cities in the Yangtze River Delta, demonstrating the clear substitution effect of Chinese brands on joint-venture brands.

For the automotive industry, this pattern of 'regional differentiation + graduated new energy penetration' is the result of market self-regulation, with distinct regional characteristics reflecting the diversity of the Chinese market. Moreover, it is evident from the data that as Chinese brands continue to develop and the market matures, consumption patterns have embraced rationality.

This article is original content from China Automotive News. Sharing is welcome, but media outlets must credit the author and source before reprinting. Any media or self-media creating video or audio content based on this article is strictly prohibited, and violators will be held legally responsible.

-

![]()

The Unstoppable Rise of 'Optical Progress and Copper Decline': Sunny Optical’s Strategic Vision for the Next Decade

-

![]()

AI + Going Global in the Second Half: No Intermission for Robot Vacuum Cleaners

-

![]()

The Suffering Endured in E-commerce, Walmart Doesn't Want to Repeat in AI

-

![]()

What Does the Doubling of New Energy Vehicle Exports Mean?

-

![]()

Ghosn: 'Only I Can Save Nissan'

-

![]()

Volkswagen Lays Off 100,000 Employees, The Elephant Sits Down

-

![]()

Expanding Production Capacity! Yutong Optics Acquires Approximately 1.5 Hectares of Industrial Land in Chang'an, Dongguan

-

![]()

Why Is Nokia Making a Comeback in the AI Era?