85% Less Profit: Where Did the Ideal Earnings Go?

03/17 2026

03/17 2026

605

605

2025 marked a year of stalling momentum for Li Auto.

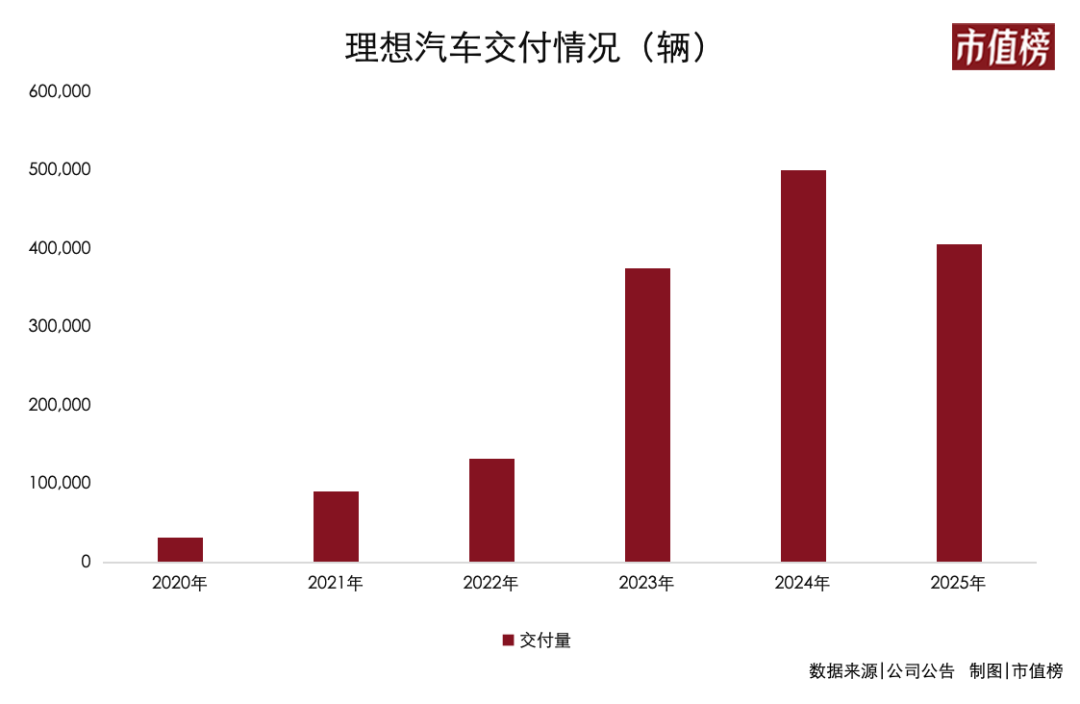

In terms of sales volume, Li Auto delivered 406,000 vehicles throughout 2025, down 18.8% year-on-year, achieving only 63.5% of its annual sales target of 640,000 units. This former leader among new energy vehicle (NEV) startups fell to fifth place in sales among NEV manufacturers and was the only one to experience a year-on-year decline.

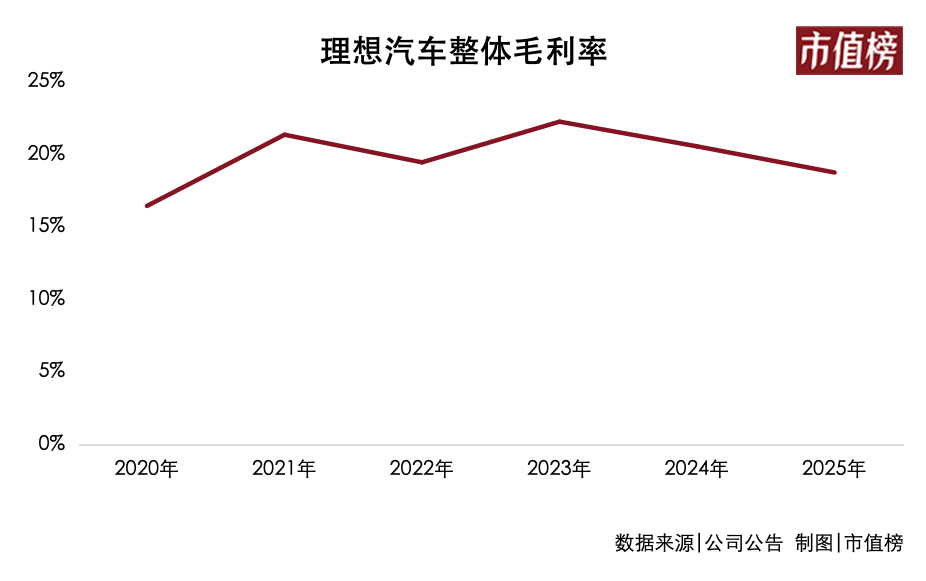

Due to a drop in average selling prices, Li Auto's revenue fell by 22.3% to RMB 112.3 billion in 2025, a larger decline than the drop in delivery volume.

From a profitability perspective, affected by the MEGA recall in the third quarter, Li Auto's 11-quarter streak of profitability came to an end. While there was a slight recovery in the fourth quarter, the full-year net profit of RMB 1.14 billion represented an 85.8% year-on-year decline.

2025 was also a year of deep adjustments for Li Auto, leaving its mark on both operations and the capital markets.

In the NEV sector, the advantages of extended-range models were increasingly matched by other automakers, while battery electric vehicle (BEV) models faced challenges ranging from poor market performance to recalls due to coolant corrosion resistance issues and production bottlenecks. Meanwhile, Li Auto chose to expand its technological boundaries by fully transitioning to embodied AI, a field requiring longer cycles and greater investment.

On the capital markets front, Li Auto's stock price fell for half of 2025.

Before the financial results were released, rumors circulated in the market that "Li Xiang was considering repurchasing some of Li Auto's Hong Kong-listed shares."

Since its Hong Kong listing in 2022, Li Auto had never conducted a share repurchase, nor had Li Xiang ever increased his stake in the company. If this move were to materialize, it would mark the company's first-ever share repurchase.

At this juncture, the significance of the term "repurchase" is self-evident. So, has Li Auto passed through its toughest period?

I. Has the Darkest Hour Passed?

After experiencing recalls and losses in the third quarter, with one-time disruptions subsiding, Li Auto's financial and operational data appeared to improve.

In the fourth quarter, Li Auto's revenue increased by 5.2% quarter-on-quarter to RMB 28.78 billion, with the overall gross margin rebounding by 1.5 percentage points to 17.8%, including a 1.3 percentage point increase in vehicle gross margin to 16.8%. Net profit turned positive at RMB 20.2 million, compared to a Q3 loss of RMB 624 million.

These figures suggest a slight rebound from being pressed to the bottom, like a spring.

However, the situation is not as optimistic as it appears on the surface.

Excluding the impact of the recall, Li Auto's vehicle gross margin in Q3 would have been 19.8%. By comparison, the Q4 vehicle gross margin of 16.8% actually represents a significant decline.

In Q4, Li Auto incurred an actual operating loss of RMB 443 million, with the net profit figure remaining positive primarily due to financial interest and other gains.

Why did the gross margin decline?

On one hand, the i6 is not a profitable model, yet its sales proportion increased in the fourth quarter. Priced at RMB 249,800, the i6 could actually be purchased for as low as RMB 239,800 after discounts.

Reports indicate that before the transition to dual suppliers was completed, the i6's gross margin would remain below 15%. In Q4, i6 production ramp-up was slow, with deliveries repeatedly delayed. Recently, Li Auto announced that production bottlenecks had finally eased, with 17,000 and 16,000 units delivered in January and February, respectively, and monthly production capacity expected to reach 20,000 units in March. However, before this, the path to reducing costs and improving gross margins through economies of scale was challenging.

On the other hand, to counter competition, Li Auto offered significant discounts in the fourth quarter, particularly on the L series, but still could not prevent a 60% year-on-year decline in L series sales.

In other words, in 2025, Li Auto faced a situation where high-margin models were hard to sell, while volume models were unprofitable.

Based on current information, the downward trend in gross margins is expected to continue into 2026.

Li Auto expects Q1 deliveries to be between 85,000 and 90,000 units, down 3.1% to 8.5% year-on-year, with total revenue projected at RMB 20.4 billion to RMB 21.6 billion, a 16.7% to 21.3% year-on-year decline.

According to Bloomberg consensus estimates, the market had previously forecast revenue of RMB 24.01 billion. The delivery guidance largely aligns with market expectations, but the revenue guidance falls short by RMB 2-3 billion.

Calculating based on average selling price, the Q4 average selling price was approximately RMB 250,000, while the Q1 2026 average selling price is expected to further decline to RMB 222,000. This implies greater reliance on low-priced models like the i6 to drive sales, while the L series remains under significant pressure.

Recent price increases in upstream raw materials such as lithium batteries and memory chips will also pressure gross margin recovery in 2026. Research reports indicate that Li Auto expects a full-year vehicle gross margin of 15% in 2026. Based on this, Citi and Bank of America both believe Li Auto risks posting a loss in 2026.

At the earnings call, Li Xiang stated that in 2026, the number of new models launched in the mid-to-high-end market above RMB 200,000 would exceed the total of the previous few years, while overall market growth would be limited.

Under such intensified competition, Li Auto's sales target for 2026 is to achieve over 20% growth, reaching 487,000 units, meaning average monthly sales of 44,000-45,000 units over the remaining nine months.

How to layout products in 2026 becomes the top priority for achieving this goal.

II. Internal Friction and Correction: Returning to Extended-Range, Betting on i9

Product cannibalization was the most visible form of internal friction for Li Auto in 2025.

For example, the lower-priced L6 offered features like refrigerators and screens, while the i8 intentionally reduced configurations to maintain the RMB 320,000 price range. The L series also failed to create a 1+1>2 effect, even experiencing customer diversion .

The root of this situation traces back to the organizational restructuring in 2024.

After the MEGA's underperformance, Li Auto split its product lines into three independent vertical teams. The first product line covered models above RMB 400,000 (MEGA/L9), the second covered models between RMB 300,000-400,000 (L8/L7/i8), and the third covered models below RMB 300,000 (L6/i6).

While products at different price points aimed to precisely target market segments, the downside was internal competition and resource contention. Coupled with various versions like Max Pro Ultra across models, product positioning became unclear, increasing consumer decision difficulty.

Li Auto recognized this issue and adjusted its strategy to enhance the luxury feel of flagship models, creating clearer distinctions in positioning, product strength, and pricing to minimize internal competition between BEV and extended-range models at similar price points.

In December 2025, Li Auto announced the merger of its first and second product lines, with Tang Jing, former president of the first product line, taking unified control, ending this year-and-a-half-long "product line experiment."

The practical corrections will be reflected in the 2026 product rhythm.

A key move is returning to extended-range technology. 36 krypton Pro reported that internally, it was judged that the core market for future extended-range models would primarily be above RMB 400,000.

In 2026, the L series will undergo a major refresh, streamlining SKUs and eliminating numerous versions. All models will come standard with 5C ultra-fast charging, eliminating the pain point of "compromised entry-level experience."

Compared to current models, the new extended-range core changes include: battery capacity exceeding 70 kWh, pure electric range exceeding 400 km, self-developed third-generation range extender enabling "seamless power generation," and the debut of the self-developed Mach 100 chip.

The new L9, launching in the first half of 2026, is seen as key to Li Auto's breakthrough. Success with the L9 would revitalize the product lineup below it.

However, challenges cannot be ignored.

In terms of volume, the development and popularize (popularization) of ultra-fast charging technology are eroding the overall market share of extended-range models. CPCA data shows that extended-range vehicles' share in NEV wholesale structure declined for several consecutive months in the second half of 2025.

Structurally, competition is intensifying. In terms of configurations, "refrigerator, TV, sofa" features have been replicated. In terms of batteries, starting in 2025, more automakers are pushing large-battery extended-range models as a transitional solution into mainstream price segments. In terms of intelligent driving, the AITO M9, with Huawei's ADS intelligent driving system, continues to squeeze the market.

Whether the L9's refresh can break through in this "fierce competition" remains a significant unknown.

BEV efforts are concentrated on the i9. The flagship BEV SUV, the Li Auto i9, will launch in the second half of 2026, forming a "extended-range + BEV" dual flagship lineup with the extended-range flagship L9 Livis.

The ideal rhythm is: first stabilize the base with the refreshed extended-range flagship L9 and Livis version in Q2, then have the i9 impact (impact) the high-end BEV market in the second half.

If the L9 and i9 achieve great success, Li Auto will thoroughly (completely) pass through its darkest hour, elevating its product strength and brand momentum while accelerating gross margin recovery.

However, when extended-range vehicles achieve over 400 km of pure electric range and support 5C ultra-fast charging, the experience boundary between them and BEVs may blur. Whether "dual flagships" become another form of internal friction will be validated by consumer choices after the new models launch.

III. Challenges of Transitioning to Embodied AI

It must be acknowledged that Li Auto's transition to BEVs was relatively late and fraught with difficulties.

This made Li Auto realize that if products remain at the "electric vehicle" level, competition will devolve into parameter wars; if only focusing on "smart terminals," it risks repeating the feature redundancy seen in smartphones.

Li Xiang's solution is to transform vehicles into embodied AI products in the physical world. Li Auto is firm (firmly) moving toward a full transition to embodied AI.

Around embodied AI, Li Auto has initiated multi-dimensional restructuring, including products (not elaborated here), sales systems, and R&D systems.

In terms of sales systems, the "Store Partner Program" will officially launch in March 2026, delegating pricing power to store managers who will be fully responsible for operational results. The evaluation mechanism will expand from single sales volume metrics to overall store performance, introducing a profit-sharing mechanism.

In terms of R&D systems, in January, Li Auto restructured its R&D team, abandoning traditional departmental divisions by software and hardware functions. Instead, it reorganized R&D into four major segments: visceral systems, brain systems, software ontology (ontology), and hardware ontology , along with three teams: foundation model team, software ontology team, and hardware ontology team.

This new logic reorganize (reorganization) is described by Li Xiang as "organizing in the way of creating digital and silicon-based humans."

Li Auto internally reflected that it had previously overemphasized R&D efficiency ratios, meaning R&D budgets were cut when revenue declined, creating a vicious cycle. Now, this metric is being de-emphasized to free R&D investment from rigid constraints.

This was evident in Q4: despite revenue and marketing/administrative expense contractions, Li Auto's R&D spending increased by 25.3% year-on-year. Full-year R&D investment reached RMB 11.3 billion, with half allocated to AI, including chips, models, and operating systems.

However, transformation does not happen overnight.

First, route changes have triggered personnel changes, with personnel turbulence and transformation growing pains contributing to the current situation.

From July 2025, when Jia Peng, head of intelligent driving technology R&D, went on sick leave and the departure of the end-to-end "three musketeers," to the January 2026 R&D system restructuring, multiple core leaders exited, including Lang Xianpeng (head of intelligent driving), Han Ling (head of intelligent driving products), Qin Dong (head of SoC in the chip department), and Chen Wei (head of foundation models).

Describing the short-term effects of this adjustment, Li Xiang said, "Everyone has noticed that work efficiency has improved recently. Intelligent driving model training frequency increased from bi-weekly to daily iterations." Li Xiang also revealed that many post-90s and post-95s have taken over core positions.

Second, external competition will not pause.

In automotive, intelligent driving is the ultimate test of automakers' AI capabilities and a key factor influencing consumer decisions in the second half of the NEV era.

Both Li Auto and XPENG have chosen the VLA route. Judging by release timing and demonstration effects, XPENG's recently launched second-generation VLA has demonstrated T0-tier capabilities, suggesting Li Auto may be a step behind. Beyond VLA, other approaches like Huawei's bet on world models are also advancing rapidly.

In embodied AI, Li Auto's AI glasses will compete with those from Qianwen, Kuake, Xiaomi, etc. Regarding robots, some industry insiders believe that if Li Auto starts from scratch, it may take two years to reach the level publicly demonstrated by XPENG IRON last year.

Third, while reusable hardware and software between automotive and AI will increase, fighting a "turnaround battle" for extended-range models and an "uphill battle" for BEVs while engaging in multi-front warfare will inevitably disperse (disperse) attention and resources.

This means Li Auto must catch up while safeguarding its extended-range base and expanding its BEV presence, leaving little room for error.

-

![]()

The Unstoppable Rise of 'Optical Progress and Copper Decline': Sunny Optical’s Strategic Vision for the Next Decade

-

![]()

AI + Going Global in the Second Half: No Intermission for Robot Vacuum Cleaners

-

![]()

The Suffering Endured in E-commerce, Walmart Doesn't Want to Repeat in AI

-

![]()

What Does the Doubling of New Energy Vehicle Exports Mean?

-

![]()

Ghosn: 'Only I Can Save Nissan'

-

![]()

Volkswagen Lays Off 100,000 Employees, The Elephant Sits Down

-

![]()

Expanding Production Capacity! Yutong Optics Acquires Approximately 1.5 Hectares of Industrial Land in Chang'an, Dongguan

-

![]()

Why Is Nokia Making a Comeback in the AI Era?