Can Geely Shake BYD's Dominance with Its Aggressive Pursuit?

03/19 2026

03/19 2026

478

478

Geely Automobile released its Q4 2025 report during the Hong Kong Stock Exchange's midday session on March 18, 2026 (Beijing Time). Key highlights include:

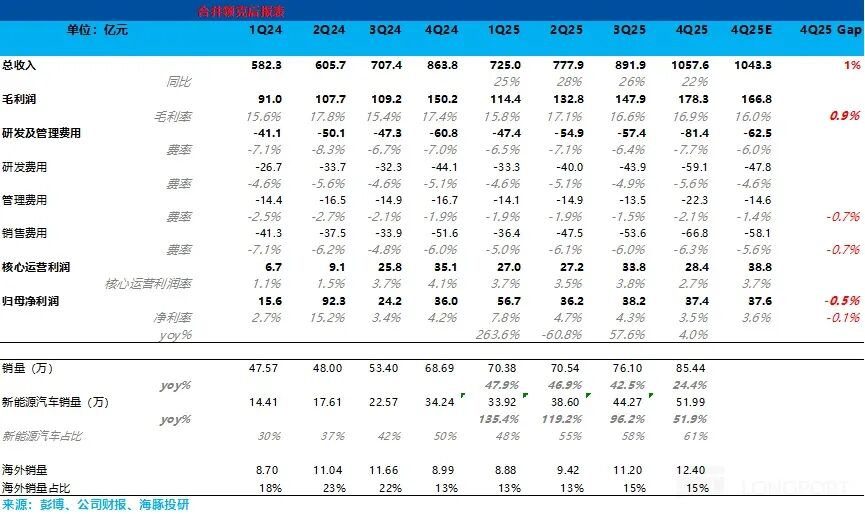

1. Revenue slightly exceeded market expectations: Total revenue reached RMB 105.7 billion, up 22% YoY, slightly surpassing the expected RMB 104.3 billion. This was primarily driven by an improved average selling price (ASP) due to a high-end product mix, indicating solid progress in premium strategy.

2. Per-vehicle revenue continued to rise quarter-on-quarter due to premiumization: ASP reached RMB 124,000, up RMB 7,000 QoQ, mainly fueled by Zeekr's premium surge:

Zeekr's Q4 sales soared 52% QoQ to 53,000 units, accounting for 9.4% of total sales (up 2.5 percentage points QoQ).

Growth was driven by high-end models like the Zeekr 9X (priced at RMB 465,900-599,900) and the refreshed Zeekr 001. The Zeekr 9X alone sold 21,400 units in Q4 at an average price of RMB 538,000, boosting overall ASP.

3. Gross margin rebounded quarter-on-quarter: Overall gross margin hit 16.9%, up 0.9 percentage points QoQ, due to:

a. High-end model volume growth and profitability recovery: Hot sales of high-margin models like the Zeekr 9X (estimated gross margin >40%) and reduced promotions for Lynk & Co's ICE vehicles restored margins. Premium models like the Galaxy M9 also contributed to margin expansion.

b. Economies of scale: Q4 vehicle sales rose 12.3% QoQ to 854,000 units, diluting fixed depreciation and amortization costs.

4. Sharp rise in operating expenses squeezed profits: Core operating profit margin declined QoQ as three major expenses surged:

Despite improved revenue and gross profit, Geely's operating expenses (R&D, sales, administration) jumped significantly, pushing core operating profit well below expectations.

R&D expenses rose RMB 1.5 billion QoQ to RMB 5.9 billion, mainly for next-gen premium models (e.g., Zeekr 8X, future flagships) and intelligentization (urban NOA, smart cockpits, chips). Higher R&D expense ratios and one-time adjustments (e.g., intelligent driving team integration) also impacted profits.

Sales expenses increased RMB 1.3 billion QoQ to RMB 6.7 billion, primarily for premium brand marketing (promoting Zeekr 9X) and accelerated domestic/overseas channel expansion (paving the way for 640,000-700,000 export targets in 2026).

Under heavy expense pressure, core operating profit fell 16% QoQ to RMB 2.84 billion, well below the expected RMB 3.88 billion. Core operating profit margin dropped 0.9 percentage points QoQ to 2.7%, and per-vehicle core operating profit fell RMB 1,100 to RMB 3,300.

5. Net profit attributable to parent barely met expectations due to JV income contributions: Against squeezed operating profits, Q4 net profit attributable to parent reached RMB 3.74 billion, up 4% YoY. Per-vehicle net profit fell to RMB 4,400 from RMB 5,000 QoQ. Final net profit barely met expectations, largely thanks to a RMB 780 million surge in share of JV profits to ~RMB 520 million QoQ.

Overall, Geely's Q4 results show that its premium strategy drove revenue and gross margin surprises, but soaring operating expenses heavily eroded current profits.

In terms of sales volume, Geely maintained steady progress. Despite raising its 2025 sales target from 2.71 million to 3 million units earlier, the company achieved 3.02 million units for the full year, exceeding the revised target.

Critically, Geely's new energy transition accelerated in Q4. NEV sales hit 520,000 units, up 17.4% QoQ, with penetration rising from 58% in Q3 to 61%, marking the company's entry into a "NEV-led" growth phase.

Breakdown by brand:

a. Galaxy Series: NEV sales rose 29% QoQ to 190,000 units, driven by new models like the Galaxy M9, Xingyao 6, Galaxy A7, and Xingjian 7, validating Galaxy's "head-to-head" strategy against BYD.

b. Lynk & Co: NEV sales grew 24% QoQ to 79,000 units, accounting for 72% of total brand sales—a rapid transition led by hot models like the Lynk & Co 10, 08, and 07.

c. Zeekr: Led with 52% QoQ growth (53,000 units), driven by the Zeekr 9X and 001. Zeekr's premiumization (especially the 9X's blockbuster sales) further lifted ASP and vehicle gross margin.

Zeekr's 2025 NEV sales reached 1.688 million units, up 90% YoY, far exceeding the revised 2025 target of 1.5 million units (113% completion rate).

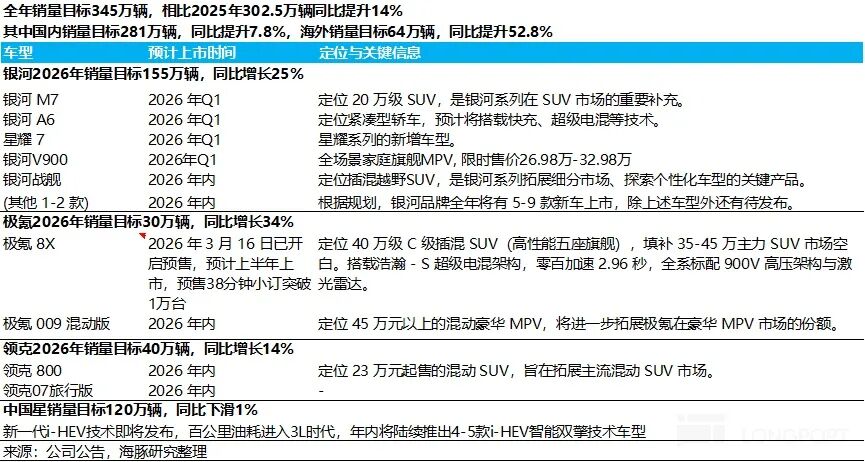

Looking ahead to 2026:

① Strong product cycle continues, with overseas growth as key driver

Geely set a 2026 total sales target of 3.45 million units (+14% YoY), characterized by "NEV-led growth and overseas expansion."

NEV sales are targeted at 2.22 million units (+32% YoY), with penetration rising 8.5 percentage points YoY to 64%. ICE vehicle sales are projected at 1.23 million units (-8% YoY).

Brand-specific plans include nearly 10 new models in 2026 to achieve targets:

Geely Galaxy: As the sales mainstay, targets 1.52 million NEV sales (+23% YoY), leveraging new models like the M7 and Xingyao 7 to consolidate the mainstream market.

Zeekr: Targets 300,000 sales (+34% YoY), driven by the pre-sold Zeekr 8X and sustained 9X volume. Premiumization remains key to profit growth.

The Zeekr 8X, launching in April, boasts superior handling, luxury, and comfort. Zeekr's proactive operational adjustments and brand upscaling will further solidify its high-end market position. As integration effects materialize, Zeekr's premiumization will drive significant profit elasticity.

Lynk & Co: Targets 400,000 sales (+14% YoY), driven by NEV transition (penetration now >72%) and new models like the Lynk & Co 800.

② Overseas markets explode, delivering high profit elasticity:

Regionally, Geely expects 2026 overseas sales to surge 53% YoY to ~640,000 units. Exports reached 121,000 units in Jan-Feb 2026 (+129% YoY), annualizing to 730,000 units—indicating high target achievability.

Overseas growth will be driven by NEV exports and channel expansion: NEVs are expected to account for 45-50% of overseas sales (~290,000-320,000 units), with the overseas channel network expanding to over 2,200 outlets.

Overseas markets are key to profit improvement: In 2025, overseas ASP (RMB 176,500) was 1.7x domestic levels, with gross margins ~10 percentage points higher and per-vehicle net profit nearing RMB 10,000. As overseas sales rise to 18.6% of the total in 2026, their high-profit nature will significantly boost overall profits.

③ Cost savings from "One Geely" integration:

Following Zeekr's privatization in late 2025, the "One Geely" strategy entered full implementation, expected to yield substantial synergies in 2026.

Integration of R&D, procurement, manufacturing, and management platforms will lower overall operating costs. As synergies fully materialize in 2026, sales, administrative, and R&D expense ratios are expected to stabilize or decline, alleviating profit pressure from high 2025 Q4 investments.

A detailed value analysis is available in the same name article under the "Insights - Deep Dive (Research)" section of the Longbridge App.

- END -

// Reprint Authorization

This article is an original work by Dolphin Research. Reproduction requires authorization.

// Disclaimer and General Disclosure

This report is for general reference only, intended for users of Dolphin Research and its affiliates for browsing and data reference. It does not consider any individual's specific investment objectives, product preferences, risk tolerance, financial status, or unique needs. Investors must consult independent professional advisors before making investment decisions based on this report. Any investment decisions made using or referencing this report's content or information are at the user's own risk. Dolphin Research shall not be liable for any direct or indirect consequences arising from the use of this report's data. The information and data herein are based on publicly available sources and are for reference only. Dolphin Research strives but does not guarantee the reliability, accuracy, or completeness of such information.

The views and analysis methods expressed in this report are personal opinions of the relevant contributors and do not represent the stance of Dolphin Research or its affiliates.

This report is produced by Dolphin Research, with copyright reserved solely by Dolphin Research. No institution or individual may, without prior written consent from Dolphin Research, (i) reproduce, copy, duplicate, reprint, forward, or create any form of copies or replicas in any manner, and/or (ii) directly or indirectly redistribute or transfer to any unauthorized parties. Dolphin Research reserves all related rights.

-

![]()

The Unstoppable Rise of 'Optical Progress and Copper Decline': Sunny Optical’s Strategic Vision for the Next Decade

-

![]()

AI + Going Global in the Second Half: No Intermission for Robot Vacuum Cleaners

-

![]()

The Suffering Endured in E-commerce, Walmart Doesn't Want to Repeat in AI

-

![]()

What Does the Doubling of New Energy Vehicle Exports Mean?

-

![]()

Ghosn: 'Only I Can Save Nissan'

-

![]()

Volkswagen Lays Off 100,000 Employees, The Elephant Sits Down

-

![]()

Expanding Production Capacity! Yutong Optics Acquires Approximately 1.5 Hectares of Industrial Land in Chang'an, Dongguan

-

![]()

Why Is Nokia Making a Comeback in the AI Era?