Revenue Surges to 3.76 Billion as Horizon Ramps Up Future Investments

03/20 2026

03/20 2026

613

613

Mid-to-High-End Chip Shipments Soar Fivefold

Author|Wang Lei

Editor|Qin Zhangyong

Horizon’s financial results clearly reflect a strategy of "high investment for growth."

In 2025, Horizon made significant strides in the mid-to-high-end intelligent driving assistance market. Shipments of its Journey series chips surpassed 4 million units, marking a 39% year-on-year increase and leading the industry in scalable delivery capabilities. Mid-to-high-end chip shipments reached 1.8 million units, nearly five times the volume recorded in the same period of 2024, with their share of total shipments rising to 48%.

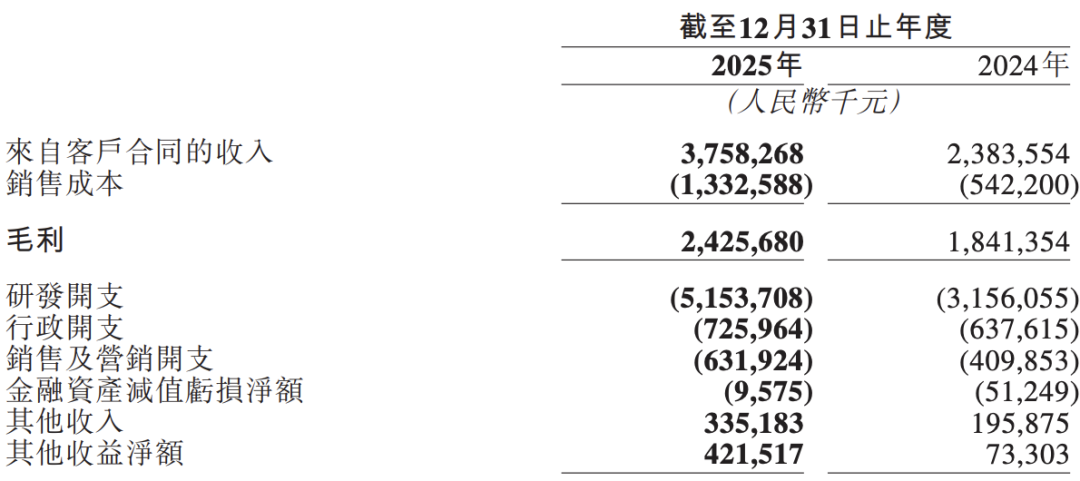

The focus on higher-priced products paid off, driving both revenue and gross margins. Full-year revenue soared to 3.76 billion yuan, up 57.7% year-on-year, while gross profit reached 2.43 billion yuan, maintaining a gross margin of 64.5%.

However, profits swung from a surplus of 2.347 billion yuan in 2024 to a deficit of 10.469 billion yuan in 2025, a shift the company attributed to a substantial increase in R&D investment.

Indeed, in this long-term, high-stakes sector, only relentless investment can pave the way for a prosperous future.

During the earnings call, Horizon's founder and CEO, Yu Kai, expressed confidence, stating that future growth curves would be steeper than previously anticipated. By 2026, Horizon aims to achieve a 60% increase in automotive revenue, ship 400,000 HSD units, and launch China's first cabin-driving integrated full-vehicle AI chip.

01

R&D Investment Takes the Spotlight

In 2025, Horizon's operating loss stood at just 3.338 billion yuan, indicating that significant "non-operating losses" occurred outside its core operations, causing the final loss to far exceed operating losses.

The primary factor impacting profit performance was the "three expenses"—selling, general, and administrative expenses—with high-intensity R&D investment being the core driver. Financial data reveals that Horizon invested 5.154 billion yuan in R&D in 2025, up 63.3% year-on-year, accounting for 137.1% of revenue—far outstripping its revenue scale.

Yu Kai acknowledged during the earnings call that the profit decline was primarily due to the further increased R&D investment in 2025.

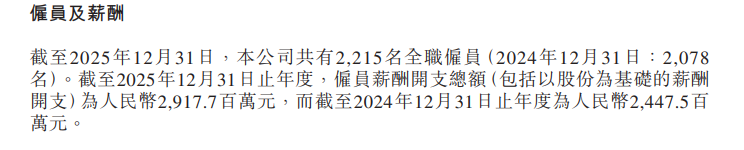

R&D spending was concentrated in three areas: cloud service training costs, tape-out fees for the new-generation BPU architecture "Riemann," and equity compensation for R&D personnel. Financial data shows that R&D personnel accounted for over 70% of the workforce.

Notably, despite its losses, Horizon continued to boost employee salaries, paying 2.918 billion yuan to 2,215 employees in 2025—more than its net loss for the year. Per capita compensation reached 1.32 million yuan, up 12% from 1.18 million yuan in 2024.

In fact, this scenario of "R&D investment exceeding current revenue" is not uncommon among early-stage tech companies. Horizon needs to reinvest all earnings into future growth.

Beyond R&D, Horizon's 2025 administrative expenses were 726 million yuan, up 13.9% year-on-year, while sales and marketing expenses reached 632 million yuan, up 54.2% year-on-year—both significant proportions relative to its revenue scale.

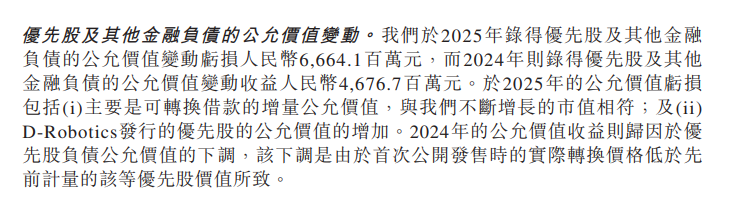

Additionally, capital market factors played a role. In 2025, Horizon recorded a "fair value change in preferred shares and other financial liabilities" loss of 6.664 billion yuan, compared to a 4.677 billion yuan gain in the same item in 2024. The fluctuation between these two items alone exceeded 10 billion yuan.

Horizon explained in its financials that this large fluctuation had two main causes. First, Horizon's convertible loans, classified as financial liabilities, saw their fair value rise alongside the company's growing market cap, though this involved no actual cash outflow. Second, subsidiary Digua Robotics also issued preferred shares, whose fair value increased.

Thus, this fluctuation did not involve actual cash outflows nor reflected operational performance.

In other words, these two sources of loss do not indicate operational issues at Horizon. On the contrary, "we are not afraid of high R&D investment," Yu Kai said, believing sustained R&D will refine Horizon's AI foundation model, build deep competitive moats, and ultimately bring L4/L5 autonomous driving to millions of households.

Horizon's confidence in "burning money" for the future may also be reflected in its cash flow. As of late 2025, Horizon held approximately 20.2 billion yuan in cash and cash equivalents, up 31.3% from 15.371 billion yuan at the end of 2024.

02

Significant Optimization in Revenue Structure

Compared to losses, changes in revenue structure send a clear signal.

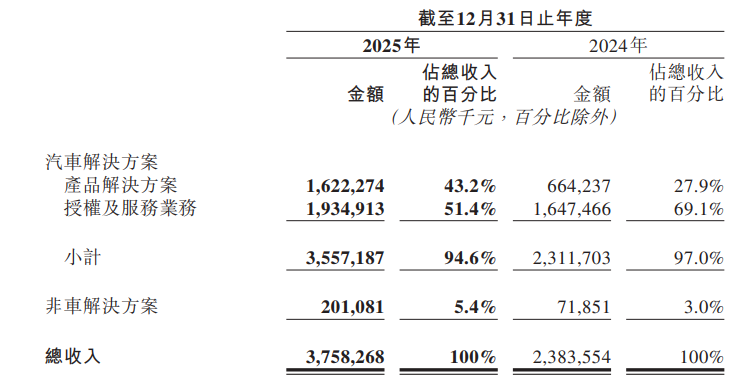

Horizon's revenue primarily comes from two segments: product solutions and licensing and services.

Revenue from automotive products and solutions reached 1.62 billion yuan, up 144.2% year-on-year, with its share of total revenue rising from 28% in 2024 to 43%. Financial data attributes this to strong shipment growth and a significant increase in per-unit value. Meanwhile, licensing and services revenue grew 17.4% year-on-year to 1.94 billion yuan, with its share declining from 69.1% to 51.4%.

In contrast, the former had a gross margin of 34.5%, while the latter reached 94.5%.

Nevertheless, their closing shares indicate that Horizon no longer relies solely on licensing "admission fees" but has truly sold large volumes of hardware and integrated hardware-software solutions. Compared to licensing revenue, product solutions represent tangible business breakthroughs with stronger risk resilience.

"This reflects the structural optimization of revenue sources after mid-to-high-end intelligent driving assistance solutions entered mass production," Yu Kai said.

Financial data shows total shipments of Horizon's Journey series chips reached 4.01 million units in 2025, up 38.8% year-on-year. Mid-to-high-end chips supporting functions like highway NOA and urban NOA reached 1.8 million units, nearly five times the volume recorded in the same period of 2024 and accounting for 45% of total shipments.

This means that for every 10 chips Horizon sells, 4.5 power high-end intelligent driving, with mid-to-high-end chips contributing over 80% to total product and solutions revenue.

In the basic ADAS market, Horizon also retained its championship with a 47.7% share, with over 95% of NOA-capable chip shipments delivered through ecosystem partners.

In terms of coverage breadth, Horizon added over 110 new vehicle models, covering mainstream domestic and joint-venture automakers. Its HSD solutions have been designated for over 20 models. Yu Kai added, "This is just a snapshot from late last year. Horizon will see explosive growth in HSD solution designations this year."

During the earnings call, Yu Kai revealed that Horizon's HSD has become a key factor influencing end consumers' vehicle purchase decisions. In 2025 models debuting HSD, top-tier variants featuring HSD as a core configuration accounted for 83% of sales.

"We are confident of achieving around 60% growth in 2026."

This confidence stems from three points. First, in terms of shipments, Horizon secured designations for hundreds of new models in 2025, mostly mid-to-high-end, with mass production starting in 2026. Shipments are expected to grow around 35% from 4 million units in 2025.

Second, regarding shipment structure, Yu Kai said 45% of Horizon's 2025 shipments were AD chips, with 55% being ADAS chips. However, AD chips will account for over 55% of 2026 shipments.

Optimization of chip shipment structure will drive up product unit prices. AD chip prices far exceed ADAS products, and AD chips' high growth will also positively impact pricing.

Yu Kai noted that while Horizon's chip ASP (average selling price) rose over 75% last year, it remains below 60 USD—still relatively low. However, ASP levels have 50% room to grow to match current highway NOA product prices and tenfold room to match urban NOA product prices.

Thus, product price increases will contribute even more to revenue growth than shipment volumes in the coming years.

It is foreseeable that with high-end intelligent driving becoming indispensable for next-gen vehicle models, Horizon's leap from "growth" to "domination" may not be far off.

-

![]()

The Unstoppable Rise of 'Optical Progress and Copper Decline': Sunny Optical’s Strategic Vision for the Next Decade

-

![]()

AI + Going Global in the Second Half: No Intermission for Robot Vacuum Cleaners

-

![]()

The Suffering Endured in E-commerce, Walmart Doesn't Want to Repeat in AI

-

![]()

What Does the Doubling of New Energy Vehicle Exports Mean?

-

![]()

Ghosn: 'Only I Can Save Nissan'

-

![]()

Volkswagen Lays Off 100,000 Employees, The Elephant Sits Down

-

![]()

Expanding Production Capacity! Yutong Optics Acquires Approximately 1.5 Hectares of Industrial Land in Chang'an, Dongguan

-

![]()

Why Is Nokia Making a Comeback in the AI Era?