Latest Release! XPENG Motors Unveils a 'Game-Changing' Moment

03/23 2026

03/23 2026

419

419

Written by | Guanchejun

XPENG Motors is now in the black!

On March 20, 2026, XPENG Motors released its financial results for the fourth quarter and full year of 2025, announcing a net profit of RMB 380 million for Q4—marking its first-ever profitable quarter. Congratulations are in order!

He Xiaopeng hailed 2025 as a 'historic turning point.' Given the financial data, this claim has some substance. In 2025, XPENG's annual deliveries soared by 125.9%, revenue jumped by 87.7%, and net losses contracted. The fourth quarter saw the company earn RMB 380 million in profit for the first time.

However, there are significant nuances behind these figures.

01

Let's delve into profitability first.

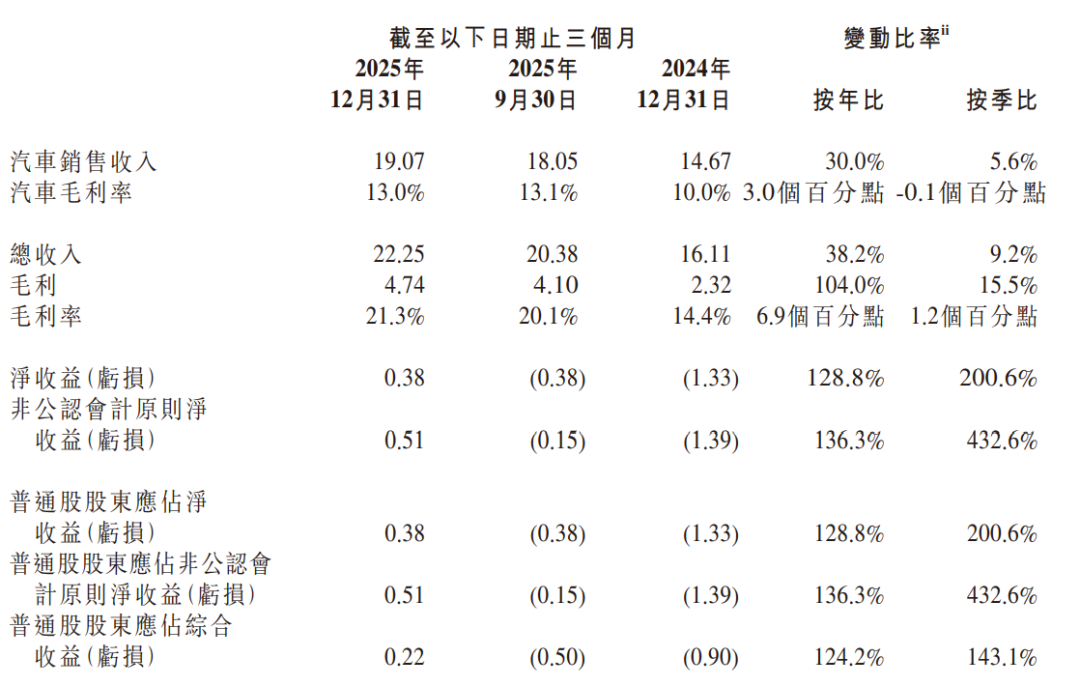

In Q4 2025, XPENG's automotive gross margin stood at 13.0%, a slight dip from Q3's 13.1%. This suggests that vehicle sales alone were not significantly more profitable.

So, where did the profit come from? Primarily from two key areas.

Firstly, service revenue. In Q4 2025, XPENG generated RMB 3.18 billion in service revenue, a 122% year-on-year surge. According to the financial report, this was largely due to technology R&D services provided to a major automaker (Volkswagen). This business segment boasted an impressive 70.8% profit margin.

Secondly, government subsidies. During this period, XPENG recorded RMB 840 million in 'other income,' a 327% year-on-year spike. Excluding this amount, XPENG's operating profit for the quarter would still be in the red.

Now, let's shift our focus to the full year of 2025.

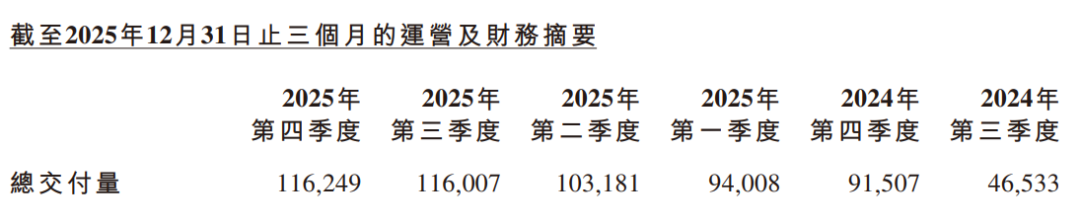

In 2025, XPENG delivered a total of 429,445 vehicles, a 125.9% year-on-year increase from 190,068 units in 2024. Quarterly delivery data reveals a consistent upward trend throughout 2025, with 94,008 units in Q1, 103,181 units in Q2, 116,007 units in Q3, and 116,249 units in Q4.

Notably, XPENG's Q4 deliveries increased by just 0.2% sequentially from Q3 and by 27% year-on-year from Q4 2024's 91,507 units. While growth remained positive, it had slowed considerably compared to the full-year growth rate of 125.9%, indicating that Q4 growth had hit a bottleneck.

More concerningly, XPENG's delivery performance in early 2026 has been lackluster: 20,011 units in January and 15,256 units in February, totaling just 35,267 units for the first two months.

XPENG's delivery forecast for Q1 2026 is 61,000–66,000 units. To meet this target, March deliveries would need to reach 25,733–30,733 units, representing a 29.79%–35.11% year-on-year decline compared to Q1 2025.

To bolster delivery growth, XPENG expanded its offline channels and charging infrastructure in 2025. By the end of 2025, XPENG had 721 physical stores spanning 255 cities and a self-operated charging network of 3,159 stations, including 2,108 ultra-fast charging stations.

02

XPENG's revenue structure also underwent notable changes in 2025.

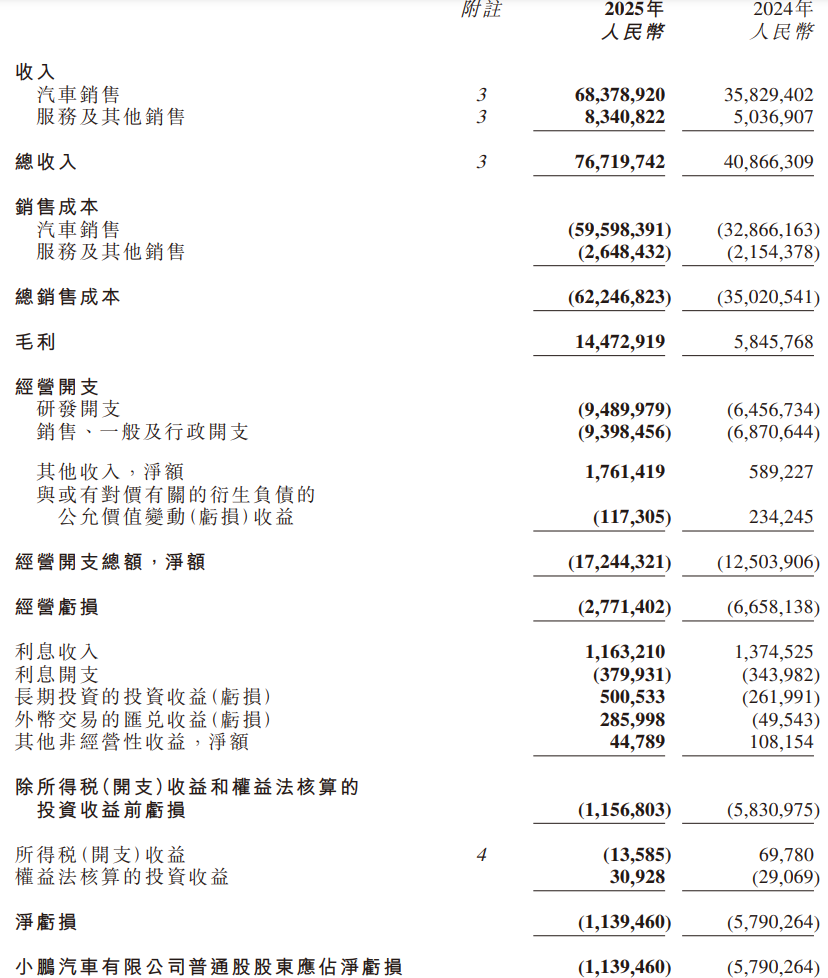

Annual automotive sales revenue reached RMB 68.38 billion, a 90.8% year-on-year increase from RMB 35.83 billion in 2024, slightly trailing the 125.9% growth in annual deliveries.

Service and other revenue totaled RMB 8.34 billion for the year, a 65.6% year-on-year rise.

This growth was propelled by three main factors: firstly, technology R&D services provided to other automakers; secondly, sales of parts and accessories, which naturally increased with cumulative vehicle sales; and thirdly, revenue growth from carbon credit trading, benefiting from the NEV industry's carbon credit trading mechanism.

Crucially, the profit margin for service and other revenue far outstripped that of automotive sales. In 2025, this segment achieved a 68.2% profit margin, compared to just 12.8% for automotive gross margin.

The expansion of this high-margin business directly boosted XPENG's overall gross margin. In 2025, XPENG's consolidated gross margin was 18.9%, up 4.6 percentage points from 14.3% in 2024.

In 2025, XPENG's net loss narrowed to RMB 1.14 billion, an 80.3% year-on-year reduction from RMB 5.79 billion in 2024.

The primary driver of this improvement was a 58.4% year-on-year reduction in operating losses, which fell to RMB 2.77 billion from RMB 6.66 billion in 2024.

As of the end of 2025, XPENG held RMB 47.66 billion in cash, an increase from the previous year.

In terms of R&D, XPENG invested RMB 9.49 billion in 2025, up by over RMB 3 billion from RMB 6.46 billion in 2024. He Xiaopeng emphasized in the financial report that this cash would be channeled into 'physical AI' R&D, including L4 autonomous driving, second-generation VLA architecture, and mass production of humanoid robots—a bold vision.

03

In summary, from Guanchejun's perspective, Q4 profitability marks a significant milestone for XPENG after years of toil, demonstrating the company's ability to mend its finances amid fierce competition.

However, akin to NIO's situation, the sustainability of this profitability remains uncertain. After all, the bulk of the profits came from technology licensing and government subsidies, rather than the core automotive business.

Moreover, the NEV market in 2026 is poised to become even more competitive, as evidenced by XPENG's declining delivery expectations for Q1. If volume growth stagnates, sustained profitability will remain elusive.

He Xiaopeng's reference to a 'historic turning point' may hold true in terms of technological narrative. But from a financial and operational standpoint, the real turning point has yet to materialize—it will arrive when XPENG achieves profitability in its core automotive business.

Thus, XPENG's Q1 2026 performance will be pivotal. Let's wait and see how things pan out.

All charts in this article, unless otherwise cited, are sourced from publicly disclosed information. We acknowledge and appreciate these sources! The views expressed herein are for reference only and do not constitute investment advice.

This article is original content from Leverage Auto Insights. Unauthorized reproduction is prohibited. For reprints, please obtain authorization and credit the original source and author at the beginning of the article. Thank you!

-

![]()

The Unstoppable Rise of 'Optical Progress and Copper Decline': Sunny Optical’s Strategic Vision for the Next Decade

-

![]()

AI + Going Global in the Second Half: No Intermission for Robot Vacuum Cleaners

-

![]()

The Suffering Endured in E-commerce, Walmart Doesn't Want to Repeat in AI

-

![]()

What Does the Doubling of New Energy Vehicle Exports Mean?

-

![]()

Ghosn: 'Only I Can Save Nissan'

-

![]()

Volkswagen Lays Off 100,000 Employees, The Elephant Sits Down

-

![]()

Expanding Production Capacity! Yutong Optics Acquires Approximately 1.5 Hectares of Industrial Land in Chang'an, Dongguan

-

![]()

Why Is Nokia Making a Comeback in the AI Era?