Xiaomi SU7 Says Farewell to Long Waiting Lists: How Will Other Automakers Compete?

03/23 2026

03/23 2026

457

457

After the "Removal" of Purchase Tax Incentives, Automakers Are Collectively Sent to the ICU

With Xiaomi's Production Capacity "Overflowing," How Will Other EV Automakers Survive?

On March 19, Xiaomi Auto officially launched the new-generation SU7 "Revamped Edition." The standard version is priced at 219,900 yuan, the Pro version at 249,900 yuan, and the Max version at 303,900 yuan.

However, what draws even more attention than the price is the hype surrounding Xiaomi and CEO Lei Jun.

Compared to the unprecedented frenzy when the first-generation SU7 debuted, dominating online discussions and electrifying both the automotive and tech circles, this launch has been markedly subdued in the public sphere. Gone are the days of overwhelming online excitement and trending discussions; everything now seems too calm.

Accompanying the decline in hype is the remarkably swift delivery speed. Xiaomi Auto officially stated that the "nearly ready" new-generation SU7 can be delivered in just 1 to 5 weeks after locking in the order.

It's worth noting that during the peak of the initial SU7's release, wait times for delivery could stretch up to half a year or even over eight months. This once spawned a secondary market resale industry where orders were transferred at a premium. The rapid shift from "hard-to-find cars with long waits" to "possible delivery within a week" reflects more than just a single company's ramp-up in production capacity.

This raises a starkly realistic and brutal question: When even Xiaomi, with its inherent star power, has moved away from the frenzy of blind orders and nearly entered a state of "ready cars waiting for customers," how are other automakers at the table faring? As the tide of hype recedes, what stifling market quagmires and survival dilemmas are domestic automakers truly facing?

01

BYD's Sales "Halved," AITO "Disappears"

If one word were to describe the new energy vehicle market at the start of 2026, it would undoubtedly be "brutal."

Normally, automakers love to highlight impressive metrics in their sales reports, boasting about "year-over-year surges." However, when we examine the most authentic passenger vehicle sales data for February, it reveals a retreat across the board, whether for pure electric, plug-in hybrid, or extended-range models.

According to statistics, China's new energy passenger vehicle sales totaled 429,000 units in February, down 34% year-over-year and 24% month-over-month.

Breaking it down by energy type, pure electric vehicle sales reached 261,000 units, down 37% year-over-year and 24% month-over-month. Plug-in hybrid sales stood at 121,000 units, down 32% year-over-year and 20% month-over-month. Extended-range vehicle sales were 47,000 units, down 17% year-over-year and 30% month-over-month.

Over the past two years, everyone has been saying that new energy vehicles replacing fuel-powered ones is inevitable. However, as soon as purchase tax incentives were reduced, the "true colors" of various new energy vehicles were exposed.

This industry-wide sales decline has hit hardest those sales giants that rely on large sales volumes, such as BYD.

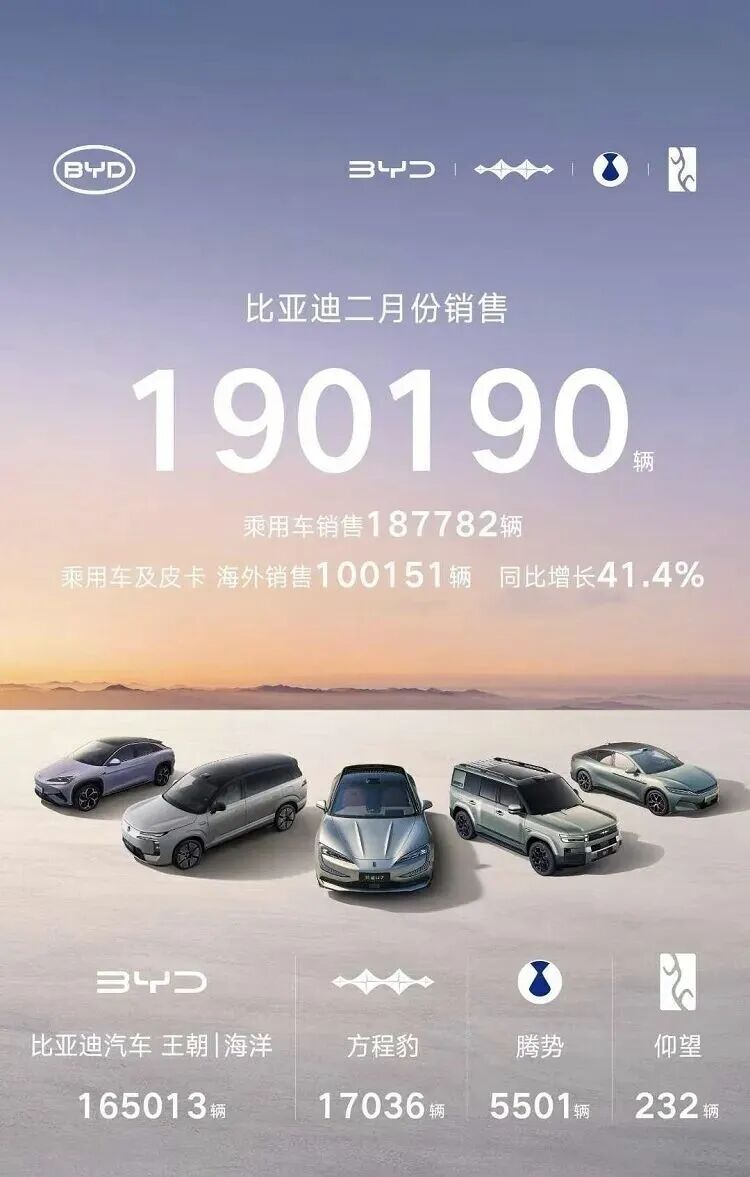

According to data released by the China Association of Automobile Manufacturers, BYD, the sales champion in 2025, sold only 190,000 units in February this year, with a cumulative sales volume of just 400,000 units from January to February, down 35.80% year-over-year.

It's important to note that BYD's annual sales in 2025 exceeded 4.6 million units. If sales continue at the January-February pace, the annual total would only reach 2.4 million units, effectively halving compared to 2025.

Geely and SAIC, which overtook BYD in February 2026, aren't faring much better.

Geely Auto sold 206,000 units in February, up a mere 0.6% year-over-year, with a cumulative sales volume of 476,000 units from January to February, up 1% year-over-year. While this surpasses BYD, Geely's 2026 sales are barely holding steady compared to 2025, partly due to deliveries shifted from last year to 2026.

SAIC's performance is similar to Geely's. The group sold 269,000 units in February, down 8.64% year-over-year, with a cumulative sales volume of 597,000 units from January to February, up 6.8% year-over-year. It's hard to call 2026 a year of growth for SAIC.

If traditional automotive giants can barely maintain their footing with their massive fuel and hybrid vehicle portfolios, then for "new automotive forces" that rely solely on new energy vehicles, their performance in February 2026 completely exposes their true survival state after the reduction of subsidies and new purchase tax policies.

To mask weak monthly data, many new-force automakers resort to wordplay in their posters, such as "consolidated financial statements." However, a closer look at the data reveals a chilling reality:

For example, HiPhi delivered 28,212 units in February, up 31% year-over-year, seemingly an impressive performance. However, compared to its January figure of 57,915 units, sales plummeted by nearly 30,000 units month-over-month, effectively halving.

Notably, the AITO brand even avoided releasing a monthly sales report, opting instead to announce "cumulative deliveries of over 58,000 units from January to February." Subtracting the 40,016 units announced in January, AITO's actual February deliveries were only 17,984 units.

Meanwhile, Seres, in the same camp, sold only 945 units in February, a staggering 90.6% year-over-year decline, according to Chery's data.

Looking at other leading new-force automakers represented by NIO, XPeng, and Li Auto, their situations are equally dire.

Li Auto delivered 26,421 units in February, nearly flat compared to January. In the dismal landscape of 2026, this might seem like a rare "straight-A student" performance.

However, Li Auto's sales in 2025, while declining, still exceeded 400,000 units, averaging around 38,000 units per month. The average sales of 26,000 units in the first two months of 2026 hardly support dreams of a "counterattack."

Beyond sales, even Li Auto, known as the "automotive product manager" that best understands users, seems powerless to boost sales. The once-iconic "fridge, TV, sofa" and spacious family-oriented designs are now standard across new energy vehicles. When unique selling points become commonplace, it will be tough for the Li L series to continue "coasting" in 2026.

NIO delivered 20,797 units in February, down over 6,000 units month-over-month. The high-margin ES8 orders that helped NIO achieve profitability in the fourth quarter of 2025 are now flagging. The volume-focused ET5 and ES6 still rely on older platform architectures. With competitors aggressively upgrading specifications this year, it's nearly impossible for NIO to achieve growth with its existing lineup.

XPeng's situation is even worse, with only 15,256 units delivered in February, continuing its decline. While it saw a temporary rebound with the affordable MONA M03, its high-end models (like the G9) remain uncompetitive in pricing. Worse still, competitors are now offering 800V high-voltage systems and advanced autonomous driving at price points between 100,000 and 150,000 yuan, rapidly eroding the MONA M03's cost-performance advantage.

Leapmotor's data, meanwhile, borders on the surreal.

With 28,067 units delivered in February, the performance seems steady. However, Leapmotor set an astonishing annual KPI of 1.05 million units for 2026. Having completed just over 50,000 units in the first two months, it would need to sell nearly 100,000 units per month for the remaining 10 months to meet its target—a nearly impossible feat in today's hyper-competitive market. Even Leapmotor itself must find this target hard to swallow.

Among new forces, Zeekr appears to be faring the best. It delivered 23,867 units in February, up a staggering 70% year-over-year, and even saw a slight month-over-month increase of a dozen units compared to January. However, to meet its annual target of 300,000 units, it still needs to sell 25,000 units per month for the remaining 10 months—a challenging but not impossible goal.

After reviewing all these figures, two words sum up the entire automotive market: anxiety.

Looking back at Xiaomi SU7's 1-to-5-week delivery cycle, when even Xiaomi, with its inherent star power, has entered a state of "ready cars waiting for customers," the plight of other players at the table becomes all too apparent.

02

When Buying a Car Becomes Cheaper Than Coffee

If the cliff-like sales curves serve as the industry's weather forecast, then in the terminal market, the desperation of automakers' sales teams to acquire customers has become painfully obvious.

First, there's the "extreme" home test drive service.

Test drives are no longer about going to a dealership; instead, cars are lining up to come to you. A simple consultation request on an app can lead to sales calls arriving faster than food delivery. To snag the few remaining potential customers, "home test drives" have become standard across all brands.

Recently, a consumer named Xiao Yang, who was considering buying a car, mentioned that he had just left a comment in a livestream for a certain new energy vehicle brand on Douyin. Within half an hour, a local salesperson added him on WeChat. After a brief conversation, the salesperson quickly brought the car to Xiao Yang's doorstep.

Such a submissive approach to customer acquisition would have been unimaginable just two years ago.

Second, there's the undeniable "bare-knuckle fighting" on the sales frontlines.

A veteran salesperson with nearly a decade of experience in the automotive industry told Hyper Focus, "The biggest problem now is that we've lost all our 'trump cards.' Previously, when we talked about 800V high-voltage systems, LiDAR, 8295 chips, or NVIDIA Orin-X processors, customers would be impressed. Now, look at vehicles in the 200,000-yuan range—every brand has these features."

"We used to rely on information asymmetry to sell cars, but now customers know more than we do. As soon as we quote a price, they pull out their phones and say, 'Look, the XPeng G7 and IM LS6 in the same class not only cost over 10,000 yuan less but also come with an extra 5,000 points and a camping gear set.' Product capabilities have completely leveled up across the board, leaving us with nothing but brute-force sales tactics."

This reality of "fully equipped, no weaknesses" means every sale comes at the cost of salespeople's hoarse voices and brands' profit margins.

Beyond the sales experience, to offset rising costs from purchase tax policy adjustments, the automotive market unleashed unprecedented financial "nuclear weapons" at the start of 2026.

Previously, three-year financing was standard, with five years being the limit. However, since February this year, over 20 brands, including Tesla, Xiaomi, BYD, and Li Auto, have started offering seven-year ultra-long low-interest loans. Given China's average vehicle replacement cycle of around five years, this is tantamount to "still paying off the loan after selling the car."

For example, some BYD Ocean Network models now have daily payments starting at an astonishing 29 yuan—less than the cost of two cups of coffee. Tesla's seven-year ultra-low-interest plan reduces monthly payments for the Model 3 to just 1,918 yuan, with an annualized interest rate of around 1%. Xiaomi has also joined the fray, offering financing plans with down payments as low as 15% and terms extending up to 84 months.

It's important to understand that this isn't just about extending payment terms; essentially, automakers are digging into their own pockets to subsidize users. While current financing costs are relatively low, these low-interest or even interest-free offers represent significant real-money subsidies from automakers.

However, given the dismal sales figures, this "self-help competition" among automakers has only just begun.

With everyone already maxing out on specifications, slashing prices, and perfecting services, traditional competitive tactics are nearing their limits. This industry-wide collective anxiety will only drive automakers to continue resorting to even more aggressive moves and deeper price cuts in the coming days.

Xiaomi SU7's production capacity "overflow" has merely torn open a small corner of the brutal reality of the 2026 automotive market.

The magic of hype is fading, and the subsidy crutch is gone, leaving only a bare-knuckled fight for survival. The new energy vehicle war of 2026 has only just begun, and the coming chapters promise to be even more brutal than any before.

- END -

-

![]()

The Unstoppable Rise of 'Optical Progress and Copper Decline': Sunny Optical’s Strategic Vision for the Next Decade

-

![]()

AI + Going Global in the Second Half: No Intermission for Robot Vacuum Cleaners

-

![]()

The Suffering Endured in E-commerce, Walmart Doesn't Want to Repeat in AI

-

![]()

What Does the Doubling of New Energy Vehicle Exports Mean?

-

![]()

Ghosn: 'Only I Can Save Nissan'

-

![]()

Volkswagen Lays Off 100,000 Employees, The Elephant Sits Down

-

![]()

Expanding Production Capacity! Yutong Optics Acquires Approximately 1.5 Hectares of Industrial Land in Chang'an, Dongguan

-

![]()

Why Is Nokia Making a Comeback in the AI Era?