XPENG: Can the 'Eastern Tesla' Sustain Its Narrative Amid Hype Without Profit?

03/23 2026

03/23 2026

573

573

XPENG released its Q4 2025 financial results after the Hong Kong market close and before the U.S. market open on March 20, 2026 (Beijing Time). While the headline figures appear strong, the guidance for actual vehicle manufacturing performance reveals considerable pressure. Key takeaways include:

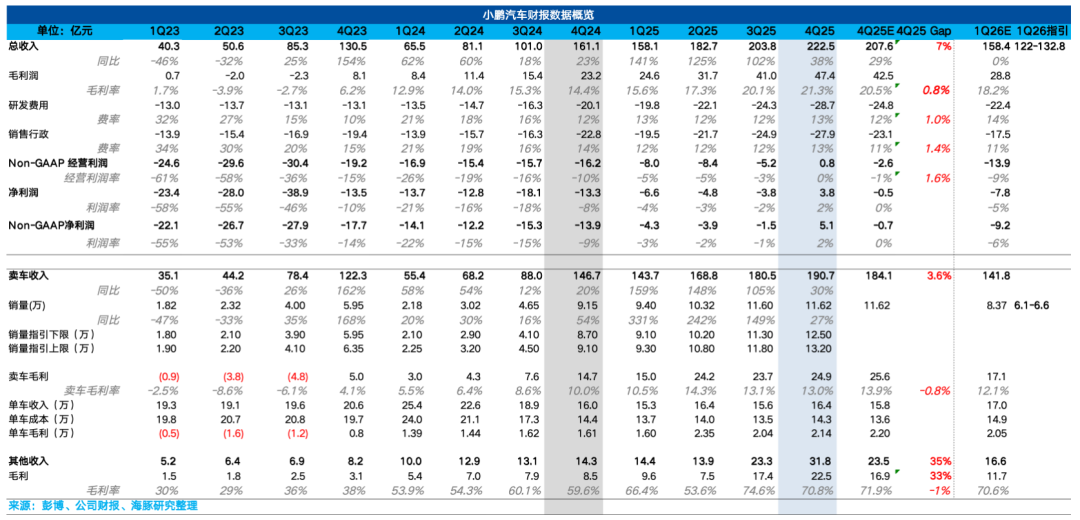

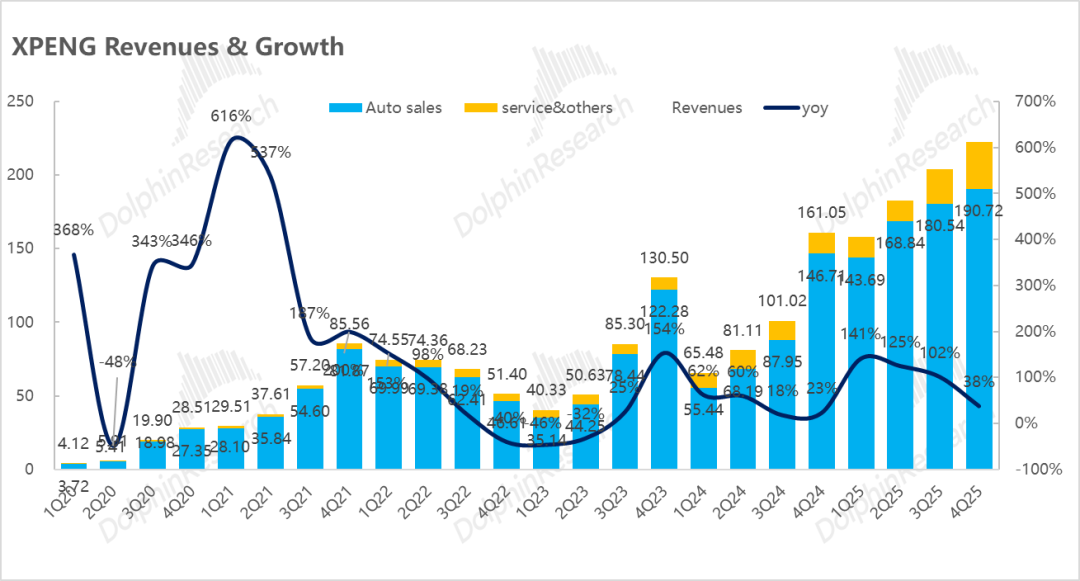

1) Revenue exceeded expectations, primarily due to a significant increase in services and other revenue: Total revenue reached RMB 22.3 billion, up 38% YoY, surpassing market expectations of RMB 20.8 billion.

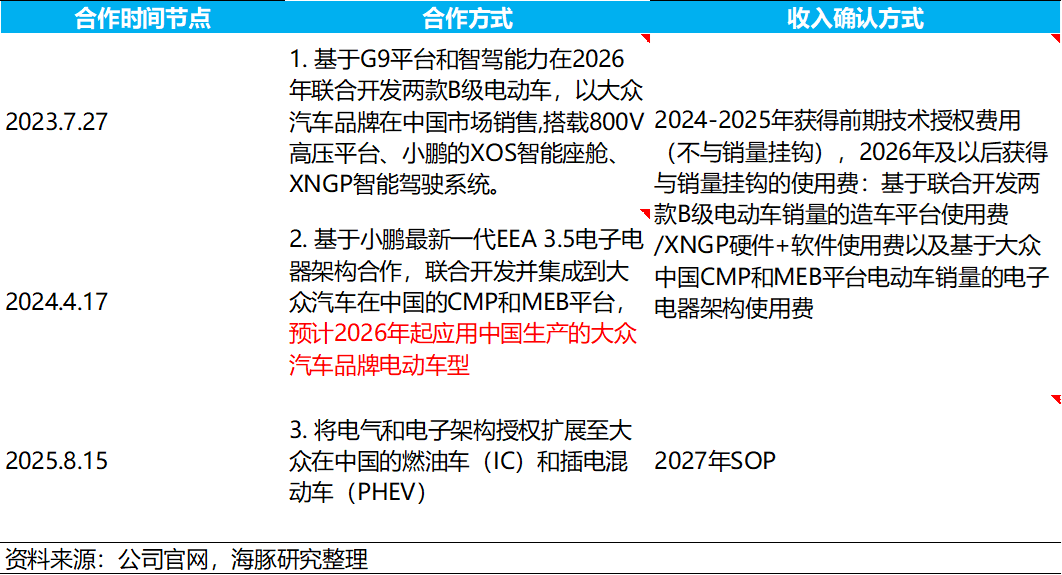

However, the largest revenue increase came from 'services and other revenue,' which surged by RMB 850 million QoQ to RMB 3.2 billion, far exceeding market expectations of RMB 2.35 billion. This was mainly driven by increased technology R&D revenue from the collaboration with Volkswagen (milestone achieved) and additional carbon credit revenue from growing overseas sales.

2) Automotive revenue growth was primarily due to improved model mix: Automotive sales revenue for the quarter was RMB 19.1 billion (up 30% YoY, exceeding market expectations of RMB 18.4 billion), benefiting from the higher proportion of the high-priced X9 model and the pull from high-ASP overseas business.

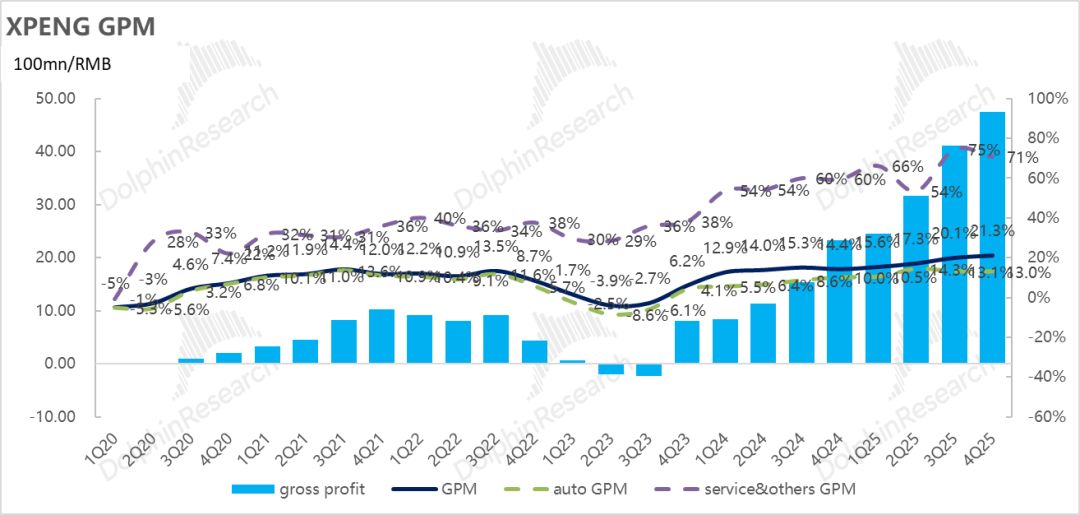

3) Automotive gross margin showed 'revenue growth without profit increase': The core automotive gross margin for the quarter was only 13%, flat QoQ and below market expectations of 13.9%. Despite the increased proportion of the higher-margin X9 model, automotive gross margin failed to meet expectations, as rising per-unit costs (primarily due to unreleased scale effects and increased supply chain and production ramp-up costs) erased the benefits of product mix optimization.

4) Overall gross margin exceeded expectations, heavily reliant on the structural pull from high-margin 'services and other revenue': XPENG's overall Q4 gross margin was 21.3%, exceeding expectations of 20.5%, primarily due to the naturally high-margin nature of technology licensing and carbon credits. The 'services and other' business had a gross margin of 70.8%, directly contributing RMB 2.25 billion in gross profit (accounting for only 14% of non-automotive revenue but nearly half of the company's total gross profit), significantly surpassing market expectations of RMB 1.7 billion.

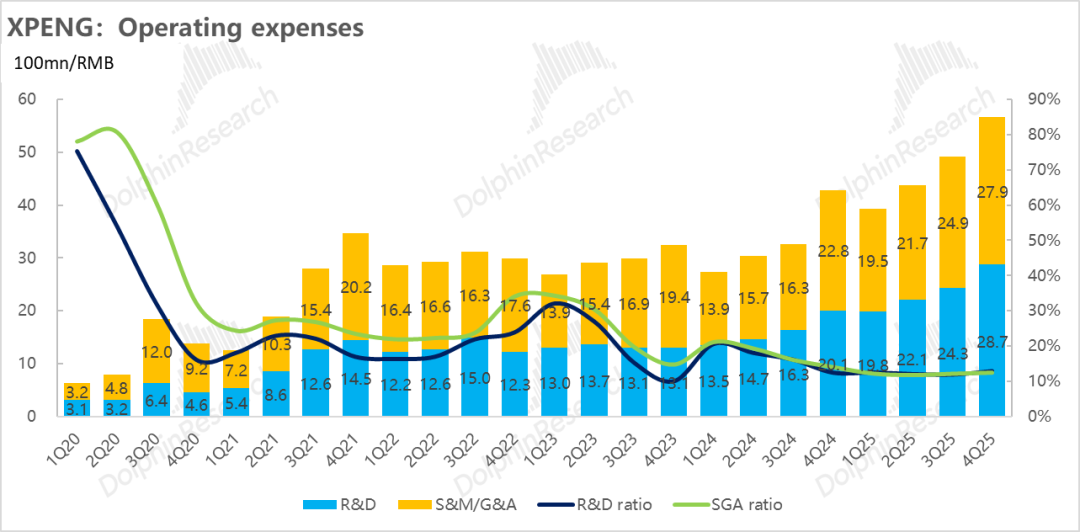

5) Operating expenses surged QoQ, preparing for the 'dual-energy vehicle strategy' and AI: In Q4, XPENG made strategic upfront investments for the 'product-heavy' 2026 and AI direction, leading to significant overperformance in R&D and SG&A expenses.

R&D expenses reached RMB 2.87 billion, well above market expectations of RMB 2.48 billion, primarily due to upfront investments in a dense new product cycle, intelligent driving, and humanoid robots. Sales expenses also reached RMB 2.79 billion, far exceeding market expectations of RMB 2.3 billion, mainly due to upfront expansion in terminal marketing and channels, preparing for the 'dual-energy vehicle strategy.'

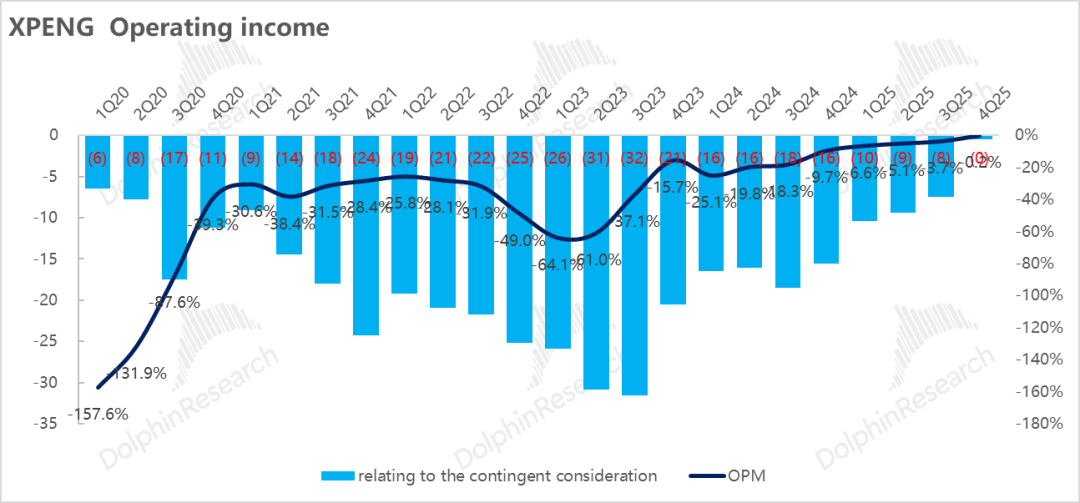

6) Net profit turnaround lacks substance; core operations remain bleeding: Although the quarter recorded RMB 380 million in net profit, marking the first turnaround since listing, this was highly dependent on RMB 840 million in one-time 'other income' from government subsidies, with actual operations still in a loss position after exclusion.

Looking at core operating profit (gross profit - core three expenses), which better reflects the main business's profitability, Q4 showed a loss of RMB 920 million, worsening by RMB 100 million QoQ from Q3's RMB 820 million loss. This means that despite overall gross profit growth, it was entirely offset by surging R&D and SG&A expenses, with the company's core business still bleeding.

Dolphin Research's View:

Overall, XPENG's Q4 headline performance was quite strong, with revenue, gross margin, and profit all exceeding market expectations, and net profit successfully turning positive for the first time since listing.

However, stripping away this 'glossy' exterior, high-margin technology service revenue and substantial government subsidies have 'polished' the true profitability, with the core vehicle manufacturing business showing 'revenue growth without profit increase' in Q4. The market is more concerned about XPENG's weak guidance for 2026 and hopes for future breakthroughs.

① Key Q1 2026 Guidance:

Guidance under the 'dual-energy vehicle' new product cycle fell short of expectations, with XPENG providing notably weak Q1 performance guidance, reflecting significant sales pressure:

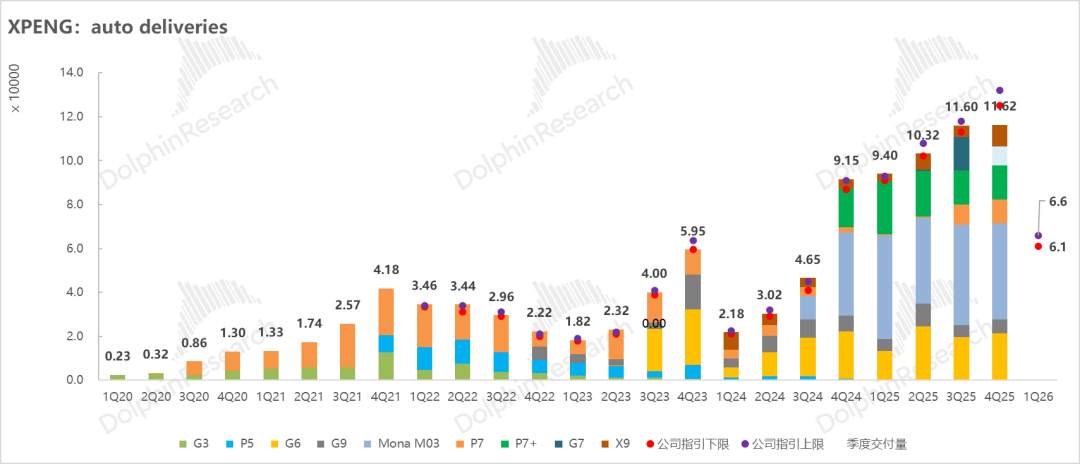

a. Weak sales guidance fails to deliver on new vehicle potential: Q1 sales guidance is only 61,000-66,000 units (down 30%-35% YoY, well below market expectations of 84,000 units). Combined with known data for January-February, this implies March sales of only 26,000-31,000 units, showing some recovery but insufficient momentum.

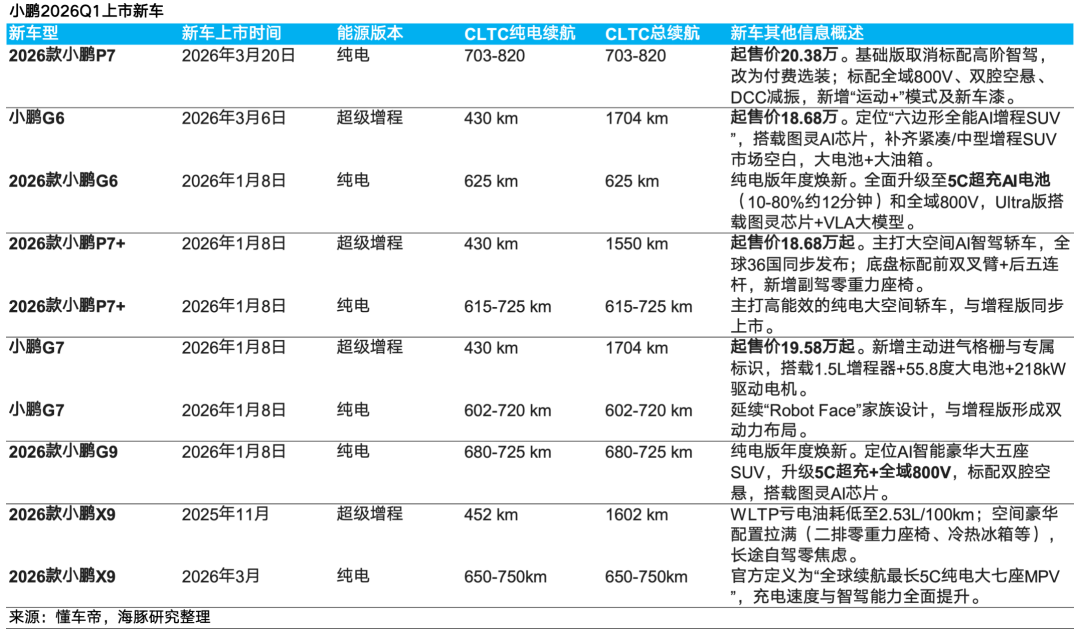

Despite facing dual pressures from the traditional off-season and purchase tax incentive phase-out in Q1, XPENG simultaneously launched a 'BEV + super range-extended' combo of G7/P7+/G6/G9 models. Under the aggressive strategy of 'same price for range-extended and BEV, upgraded specs without price hikes,' these high-range new vehicles (BEV 430km/combined over 1550km), which began delivery in late January, failed to boost terminal demand as expected, raising market doubts about XPENG's new product cycle potency centered around 'dual-energy vehicles.'

b. Revenue guidance implies ASP decline, with automotive gross margin expected to remain under pressure:

Q1 revenue guidance is RMB 12.2-13.28 billion. After excluding services and other revenue, the implied average selling price (ASP) is around RMB 155,000-165,000, with the upper limit only flat QoQ and below market expectations of RMB 170,000.

With the X9 model's sales proportion expected to continue rising, the overall ASP still fell short of expectations, mainly due to XPENG's increased terminal promotions and price cuts, indicating 'visibly high' sales pressure.

While terminal concessions pressure ASP, XPENG's automotive gross margin will also face two cost headwinds in Q1, with sales gross margin expected to remain under pressure:

1) Diminished scale effects: A significant QoQ decline in sales volume leads to soaring per-unit fixed costs such as depreciation and amortization.

2) Rising upstream costs: Recent sustained increases in core raw material prices such as power batteries, memory chips, and bulk aluminum.

② Looking at 2026 as a whole:

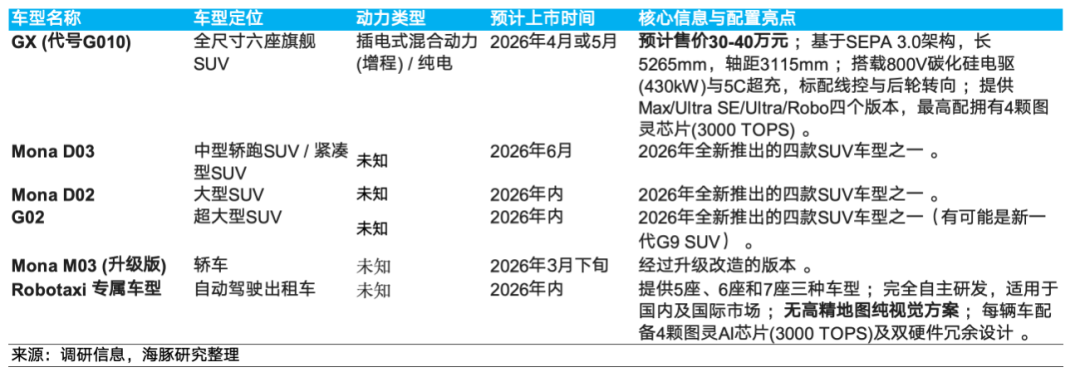

Despite the unfavorable Q1 start and XPENG not yet providing a 2026 delivery target (focus on earnings call guidance), the market still expects XPENG to reach 520,000 deliveries in 2026 (up 21% YoY). This growth will be primarily driven by super range-extended models and four new SUV models planned for launch in 2026 (including Mona D02, Mona D03, GX, and G02/G01).

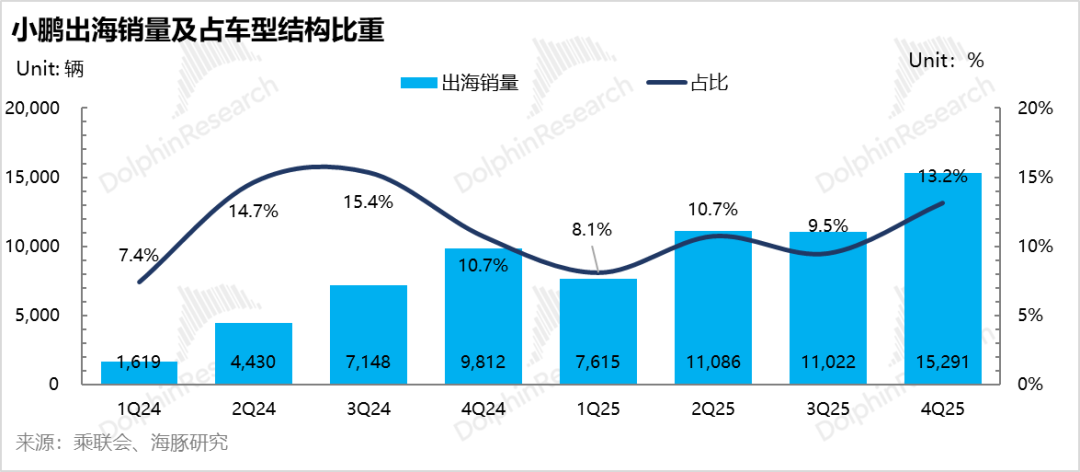

Overseas sales as a core growth engine: XPENG previously planned to double overseas sales to 90,000 units in 2026 (45,006 units in 2025).

The company will focus on expanding into five overseas markets: Israel, Germany, Norway, Thailand, and France, planning to launch at least four new models out of six global core models. To support this, XPENG plans to expand its channel network to 680 stores, covering over 60 countries and regions. The company's longer-term goal is to exceed 1 million overseas sales by 2030, contributing over 70% of total profit.

Currently, overseas sales reached nearly 7,000 units in January-February (annualized 42,000 units). Dolphin Research believes the achievability of this aggressive overseas sales target remains to be seen.

Domestic base supported by 'major new product cycle':

If the overseas target of 90,000 units is met, the expected 520,000 total sales imply 430,000 units need to be completed domestically (up 12% YoY). Dolphin Research believes this target has a relatively high probability of being achieved, supported by the launch of two high-volume Mona platform new SUVs in Q2 and H2 2026.

AI Progress: XPENG is accelerating the commercialization of AI capabilities from R&D to market:

a. Intelligent driving foundation upgraded again: On the hardware side, the 'Turring' chip with 750 TOPS of computing power has entered mass production with new vehicles. On the software side, XPENG officially launched the second-generation vision-language-action model 'XPENG VLA 2.0' in March 2026. This model adopts an innovative 'vision + language-to-action' architecture, eliminating intermediate conversion steps and enabling direct translation of visual signals into action commands. To accelerate integration, XPENG established a new 'General Intelligence Center,' combining autonomous driving and smart cockpit R&D teams.

b. Robotaxi acceleration: XPENG plans to launch three models (5-seater, 6-seater, 7-seater) designed specifically for Robotaxi services in 2026. These models will not require high-definition maps and will operate solely on vision technology. Each vehicle will be equipped with 4 Turring chips (3,000 TOPS) and dual hardware redundancy. Robotaxi operations will begin pilot testing in 2026, with plans to license software development kits to third parties.

c. Humanoid robot sprint: The new-generation 'Iron Man' humanoid robot, equipped with solid-state batteries and 3 Turring chips (2,250 TOPS), incorporates technologies such as VLT, VLA, and VLM. XPENG plans to achieve mass production by the end of 2026, initially for applications such as guided tours and shopping assistance.

A more detailed value analysis has been published in the Longbridge App's 'Updates - In-Depth (Research)' section under an article with the same title.

Below is a detailed analysis:

I. Automotive Gross Margin Falls Short of Expectations

With XPENG's Q4 sales volume already announced, investors are primarily concerned with automotive revenue and gross margin performance in this earnings report.

Q4 automotive delivery volume remained largely flat QoQ, with market expectations originally anticipating a slight increase in automotive gross margin from Q3's 13.1% to 13.9% driven by product mix optimization.

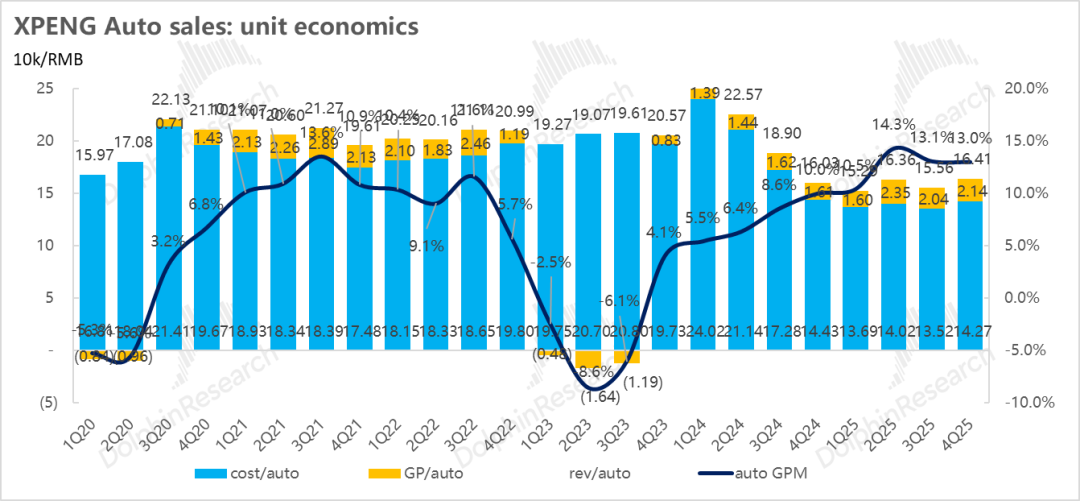

However, the actual Q4 automotive gross margin was only 13%, showing nearly zero QoQ growth and unexpectedly falling short. Although model mix improvements pushed up ASP, simultaneous significant increases in per-unit costs entirely offset the benefits of product mix optimization.

Breaking down per-unit economics:

a) ASP: High-priced models and overseas expansion drive ASP higher than expected

XPENG's Q4 ASP reached RMB 164,000, up RMB 8,000 QoQ from RMB 156,000, not only exceeding market expectations of RMB 158,000 but also surpassing the company's previous guidance implying RMB 155,000. ASP growth was primarily driven by two factors:

① Increased proportion of flagship X9 model: In Q4, the high-priced X9's sales proportion rose 4 percentage points QoQ to 9%; meanwhile, the low-priced MONA M03, targeting the mass market, saw its proportion slip 2 percentage points QoQ to 38%. This shift clearly tilted the domestic sales mix toward higher price segments.

② Sustained growth in high-margin overseas business: Q4 overseas sales reached 15,300 units, with its proportion in total sales rising 3.7 percentage points QoQ to 13.2%. Due to higher pricing in overseas markets, this increased proportion directly raised the overall ASP.

③ Limited overall discounting:

In Q4, XPENG offered RMB 5,000/5,000/15,000 cash discounts for its G6, G9, and X9 BEV models, along with continuing 3-year zero-interest/5-year low-interest financing plans for some models. Overall discounting remained relatively controlled in Q4, with limited negative impact on ASP.

b) Per-unit cost: Lack of scale effects and soaring costs drag down gross margin

XPENG's Q4 per-unit cost was approximately RMB 143,000, up about RMB 7,000 QoQ from RMB 136,000. This cost increase was the direct 'culprit' pressuring gross margin growth. Key drivers of cost increases include:

① Inherent cost increases for high-priced models: While the increased proportion of X9 models raised ASP, as a large MPV, its per-unit BOM (bill of materials) cost is inherently high.

② Hindered scale effect release: Q4 total deliveries were only 116,000 units, largely flat QoQ and below the original guidance of 125,000-132,000 units. Stagnant sales mean factory depreciation, amortization, and other fixed costs cannot be further diluted.

The sales shortfall was primarily due to the phase-out of national/local 'trade-in' subsidies at the end of Q4 2025, which led to significant pre-emption of mid-to-low-end purchasing demand in Q3, severely impacting volume-dependent models like MONA M03.

Meanwhile, volume-oriented models G7 and new P7 averaged only around 2,000 monthly sales in November-December, failing to step up.

③ Early production ramp-up and supply chain volatility: Early-stage production ramp-up losses for new models (especially those first introducing super range-extended versions), combined with short-term fluctuations in procurement costs for some core components (such as batteries), further pushed up per-unit manufacturing costs.

c) Per-unit gross profit: Revenue growth without profit increase, gross margin stagnant

XPENG's Q4 per-unit gross profit was only RMB 21,000, up a slight RMB 1,000 QoQ and below market expectations of RMB 22,000. This ultimately resulted in an actual Q4 automotive gross margin of only 13%, flat QoQ and below the consensus expectation of 13.9%.

II. Guidance Falls Short of Expectations Amid New Vehicle Cycle of 'Dual Capability in One Vehicle'

Compared to the mixed results in Q4, XPENG's guidance for Q1 appears notably weaker:

a) Weak sales guidance fails to reflect new vehicle potential:

Sales guidance for Q1 stands at just 61,000-66,000 units, representing a YoY decline of 30%-35% and falling well short of market expectations of 84,000 units. Combining known data from January (~20,000 units) and February (~15,000 units), implied March sales would range between 26,000-31,000 units, showing early signs of recovery from February's lows.

While Q1 is traditionally a slow season for auto sales, particularly under this year's reduced purchase tax incentives, XPENG's aggressive product launches in Q1—including the G7/P7+/G6/G9 lineup—fully activated its 'BEV + Range-Extended Series Hybrid' dual-capability strategy. Notably, the range-extended versions of the G7, P7+, and G6 feature a 1.5T range extender with CLTC pure electric range of 430km and combined range up to 1,550-1,704km.

Despite aggressive pricing strategies—'same price for range-extended and BEV models' and 'upgraded specs without price hikes'—these new vehicles, which began deliveries in late January, failed to stimulate strong sales as anticipated. This raises doubts about the market impact of XPENG's new vehicle cycle.

b) Revenue guidance implies ASP decline, underscoring sales pressure

Total revenue guidance for Q1 is RMB 12.2-13.28 billion. After excluding service and other revenues, the implied average selling price (ASP) ranges from RMB 155,000-165,000, barely matching Q4's upper limit and falling short of market consensus expectations of RMB 170,000.

Despite expected growth in sales of the high-end MPV X9, overall ASP remains stagnant, likely due to XPENG's intensified terminal promotions and price cuts:

① Direct cash subsidies: XPENG offers RMB 5,000 cash subsidies for the MONA M03 and G6 sedan/SUV; RMB 8,000 for the P7+, old P7, and new G7; and up to RMB 17,000 for the high-end BEV SUV G9.

② Extended financing options: The '7-year low-interest' auto financing program, covering all models, effectively lowers purchase barriers.

While terminal concessions pressure ASPs, cost pressures are also mounting, suggesting significant margin headwinds for XPENG in Q1:

① Eroding scale effects: Q1 sales volume is expected to shrink sharply QoQ, causing fixed costs per unit (e.g., depreciation) to surge.

② Rising upstream material costs: Prices for core raw materials (power batteries, memory chips, aluminum, etc.) have recently trended upward.

III. Overall Gross Margin Exceeds Expectations: 'Cosmetic' Profit Boost from VW Tech Licensing and Carbon Credits

XPENG's Q4 total revenue reached RMB 22.3 billion (beating consensus of RMB 20.8 billion), with an overall gross margin of 21.3% (exceeding consensus of 20.5%).

However, a breakdown reveals that the outperformance was driven not by the core auto business but by high-margin 'service and other revenues':

① Revenue outperformance relies heavily on non-auto segments:

Auto business: Revenue grows, but margins lag

Automotive sales revenue hit RMB 19.1 billion (+30% YoY, beating consensus of RMB 18.4 billion), driven by higher mix of the high-ASP X9 and robust overseas sales. However, as previously noted, elevated per-unit costs offset product mix improvements, resulting in a core auto gross margin of just 13%, missing expectations.

Services and other businesses: Explosive growth from tech licensing and carbon credits

The largest contributor to Q4 performance was 'services and other revenues,' which surged RMB 850 million QoQ to RMB 3.2 billion, far exceeding consensus of RMB 2.35 billion. The QoQ spike was primarily due to:

a. A milestone achievement in R&D collaboration with Volkswagen on electronic electrical architecture (EEA) tech, unlocking significant incremental licensing revenue.

b. Additional carbon credit gains from rising overseas sales.

② Skewed gross margin structure masks core profitability weakness

Benefiting from the inherently high margins of tech licensing and carbon credits, the 'services and other' segment achieved a gross margin of 70.8% in Q4 (down 4 ppts QoQ due to business mix but remaining at an elevated level). This segment contributed RMB 2.25 billion in gross profit, vastly exceeding consensus of RMB 1.7 billion.

Despite accounting for just 14% of total revenue, this non-auto segment generated nearly half of XPENG's total gross profit, artificially inflating the company's overall gross margin to 21.3%.

IV. Operating Expenses Surge to Support 'Dual Capability' and AI Ecosystem, Weighing on Core Profitability

XPENG has long positioned 'intelligence' as its core moat, necessitating sustained heavy investment in AI-driven autonomous driving and new platform development.

In Q4, these pre-emptive strategic investments for the 'product supercycle' in 2026 caused R&D and SG&A expenses to significantly exceed expectations, becoming the primary drag on core operating profit.

1) R&D expenses: RMB 2.87 billion, betting big on new models and physical AI

XPENG's Q4 R&D spending reached RMB 2.87 billion, well above consensus of RMB 2.48 billion and up RMB 450 million QoQ from RMB 2.43 billion. The QoQ increase was driven by:

① Upfront investments for dense (intensive) new product cycles: In Q4 2025, XPENG initiated its 'dual capability' transformation with the launch of the range-extended version of its flagship X9.

The company is also stockpiling resources for a full-scale 'dual capability' rollout in 2026, including range-extended variants for all existing BEV models and four new SUV launches. R&D activities related to new platform development, powertrain adaptation, and engineering validation formed the bulk of the QoQ increase.

② ADAS upgrades: At the hardware level, XPENG's self-developed high-performance 'Turring' chip (750 TOPS per chip) entered mass production with the G7 and new P7 models in Q3.

At the algorithm level, the company's VLA 2.0 (Vision-Language-Action) large model was released in March 2026. Featuring an innovative 'vision-to-action' end-to-end architecture, the model eliminates the traditional language translation layer to reduce latency and improve decision-making efficiency, serving as a unified technical foundation for vehicles, Robotaxis, robots, and flying cars.

To accelerate integration, XPENG established a new 'General Intelligence Center' to merge autonomous driving and smart cockpit R&D teams under a unified AI base model and technology framework.

③ Proactive investments in humanoid robots: XPENG's next-gen 'Iron' humanoid robot reached a critical R&D stage. The robot features industry-first all-solid-state batteries, three 'Turring' AI chips (total 2,250 TOPS), and a multimodal large model system integrating VLT (thinking), VLA (action), and VLM (interaction).

To achieve commercial deployment in April 2026 (e.g., guiding, reception) and mass production of an advanced version by end-2026, related algorithm training, hardware iteration, and scenario testing investments likely increased QoQ.

2) SG&A expenses: RMB 2.79 billion, reflecting channel expansion for new models

Q4 sales and administrative expenses hit RMB 2.79 billion, far exceeding consensus of RMB 2.3 billion and up RMB 300 million QoQ from RMB 2.49 billion. The increase stemmed primarily from terminal marketing and channel expansion:

① Higher marketing and commission expenses: The launch of heavyweight models like the X9 range-extended version in Q4 drove up marketing spend, while sales commissions paid to franchise stores (dealers) also rose QoQ.

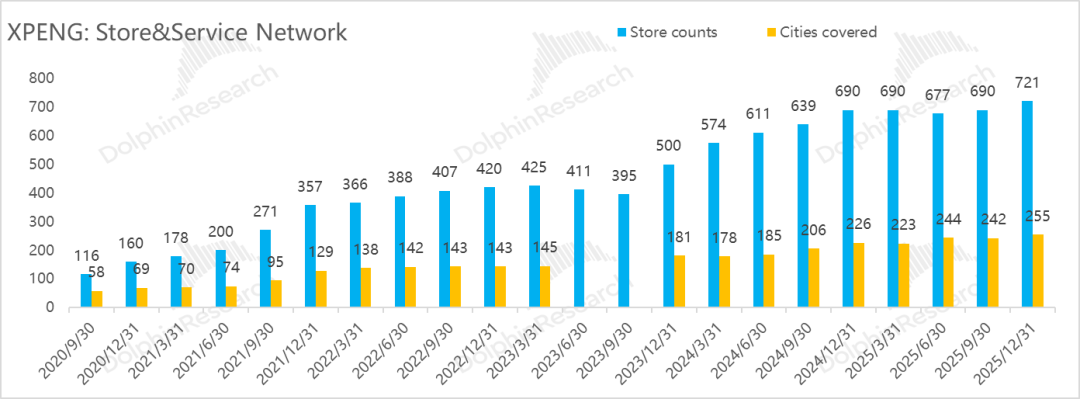

② Rapid channel expansion: To support the 2026 'dual capability' sink (market penetration) strategy and four new SUV launches, XPENG accelerated store openings in Q4, adding 31 new outlets (total 721) across 13 new cities (total 255). This rapid expansion caused rigid costs (rent, staffing) to spike.

V. Net Profit Turnaround Lacks Substance, Core Operations Still Bleeding

While Q4 net profit reached RMB 380 million—XPENG's first positive quarter since listing—this result relied heavily on RMB 840 million in 'other income' (primarily one-time government subsidies). Excluding non-recurring items, XPENG remained unprofitable in Q4.

From the perspective of core operating profit (gross profit - core operating expenses), which better reflects organic profitability, Q4 posted a RMB 920 million loss—worsening from Q3's RMB 820 million loss (an additional RMB 100 million in losses). Despite sequential gross profit growth, the sharp QoQ rise in sales, administrative, and R&D expenses dragged down profitability, indicating continued core operating losses.

- END -

// Reprint Authorization

This article is an original work by Dolphin Research. Reproduction requires authorization.

// Disclaimer and General Disclosure

This report is for general reference only, intended for users of Dolphin Research and its affiliates for general browsing and data reference. It does not consider the specific investment objectives, product preferences, risk tolerance, financial condition, or unique needs of any individual receiving this report. Investors must consult independent professional advisors before making investment decisions based on this report. Any person using or referring to the content or information in this report for investment decisions assumes all associated risks. Dolphin Research shall not be liable for any direct or indirect losses arising from the use of data contained herein. The information and data in this report are based on publicly available sources and are for reference only. While Dolphin Research strives to ensure the reliability, accuracy, and completeness of the information and data, no guarantees are made.

The views, opinions, and analytical methods expressed in this report are those of the individual authors and do not represent the stance of Dolphin Research or its affiliates.

This report is produced by Dolphin Research, with copyright reserved solely to Dolphin Research. No institution or individual may, without prior written consent from Dolphin Research: (i) reproduce, copy, duplicate, reprint, forward, or create derivatives in any form; or (ii) directly or indirectly redistribute or transfer to any unauthorized party. Dolphin Research reserves all related rights.

-

![]()

The Unstoppable Rise of 'Optical Progress and Copper Decline': Sunny Optical’s Strategic Vision for the Next Decade

-

![]()

AI + Going Global in the Second Half: No Intermission for Robot Vacuum Cleaners

-

![]()

The Suffering Endured in E-commerce, Walmart Doesn't Want to Repeat in AI

-

![]()

What Does the Doubling of New Energy Vehicle Exports Mean?

-

![]()

Ghosn: 'Only I Can Save Nissan'

-

![]()

Volkswagen Lays Off 100,000 Employees, The Elephant Sits Down

-

![]()

Expanding Production Capacity! Yutong Optics Acquires Approximately 1.5 Hectares of Industrial Land in Chang'an, Dongguan

-

![]()

Why Is Nokia Making a Comeback in the AI Era?