The Logic Behind Car Price Hikes Has Been Shattered by Xiaomi

03/23 2026

03/23 2026

509

509

In just one month, Lei Jun has confused the outside world at least three times.

First, he initially announced an expected April launch, only to suddenly bring it forward to March 19th.

Next, a system-wide price increase of 4,000 yuan broke through many people's expectations of a modest 1,000-2,000 yuan hike and was significantly lower than the price increases by other automakers in the industry.

Then, during the launch event, on the slide comparing other models, all were competitors except for the Model 3, which was prominently displayed. Each of these three points alone warrants in-depth investigation and would certainly yield interesting conclusions.

Overall, the product competitiveness and pricing strategy of the new-generation Xiaomi SU7 continue to follow Lei's approach and are expected to achieve strong sales in the market. However, there are more issues troubling us, potential buyers holding onto their cash, and even the entire automotive industry.

Regarding price hikes and the potential wave of increases, as well as the ongoing "Schrödinger's Cat" scenario within it.

The painful reality is that even though we have identified the general reasons for the price hikes, we simply cannot provide specific figures or even accurate ranges for the increases.

This Early-Announced Price Hike Lacks a Unified Pattern

From the growth market to the mature market, automakers previously focused on how to lower car prices, but this approach is no longer valid in 2026.

The tradition of not raising prices has been broken, with Lei Jun even revealing his cards in advance, acknowledging that the new generation of SU7 would have to increase in price.

There are countless ways to raise prices, but the reasons are generally the same: rising raw material costs. Li Bin issued a warning about this at the beginning of the year.

A careful comparison of the four automakers that have currently signaled price increases reveals different logics.

First, Chery's Exeed ET5 increased the suggested retail price of its high-end version by 5,000 yuan this year, effectively firing the first shot of the year. Specifically, Exeed adjusted the previously "free" high-level intelligent driving benefits to a 5,000 yuan package. Although this was a direct price adjustment on existing models, it gave consumers the choice through optional upgrades.

Shortly thereafter, Huawei released its latest 896-line LiDAR, and the new models of Seres M9 and Zenith S800 equipped with this hardware saw synchronized price increases: the starting price of the M9 rose by 10,000 yuan, and the S800 by 20,000 yuan. This is a typical example of "premium pricing for added features," using price to raise the technological bar.

Also equipped with Huawei's latest technology, Hyper Hyper actively abandoned premium pricing. The Hyper Hyper A800, unveiled on the same night, still kept the price of its high-end version, equipped with Huawei's triple motors and the latest LiDAR solution, below 300,000 yuan after superposition (stacked) trade-in subsidies. This demonstrates that "new technology = price increase" is not an ironclad rule and depends more on brand strategy.

Then, there were rumors that the Zeekr 007 GT would soon increase in price, with subsequent speculation suggesting an expected increase of 5,000-8,000 yuan. Interestingly, Zeekr's response was not a denial but rather that it was "not yet determined."

From automakers' actions, a 5,000 yuan price increase has become the new norm in this year's auto market, with 8,000 yuan and 10,000 yuan increases being the exception. Why did the price war reach a turning point in 2026? Two macro events can explain this: the global increase in memory/chip prices and the recovery of raw material costs for power batteries.

First, let's talk about computing power and memory. Entering 2026, DRAM has been "snapped up" by AI servers. A authority (authoritative) institution predicts that the contract price of DRAM will rise from 55-60% to 90-95% in the first quarter. Storage is prioritized for server-side supply, leading to across-the-board price increases for conventional DRAM, with downstream sectors like mobile phones and automobiles having to passively absorb the cost changes.

The situation is even more challenging for automobiles because automotive-grade memory/SoCs are mostly board-level finalized. A temporary (temporary) change in materials would mean a complete redesign review, which is not worth the risk or time, and no one dares to make such a decision lightly.

Now, let's discuss batteries. Battery-grade lithium carbonate bottomed out in the second half of 2025 and rebounded sharply, with Chinese spot prices once returning to 150,000 yuan/ton in early 2026. This year, the domestic spot average price rose from 119,000 yuan to 152,500 yuan/ton in January, a monthly increase of over 28%. Additionally, the cost of cathode materials is also rising, making it impossible for automakers to bear the cost increases indefinitely.

A comparison with the mobile phone industry makes this even clearer: it's increasingly difficult to find phones priced below 1,000 yuan this year. Many institutions/media outlets are saying that smartphones have entered a period of widespread price increases, with average selling prices rising by double digits, driven by continuous price hikes in memory chips. The logic of "storage with computing power" is interconnected between cars and phones.

The Next Wave of Price Increases Will Be Justified by Added Features

However, knowing the reasons for the price increases without more details is anxiety-inducing.

In the final assembly plants of many automakers, workers who complete the final assembly of vehicles know that costs have recently increased but have no idea how much the prices of batteries, intelligent driving systems, or cabins have risen.

This would have been difficult to happen in the era of traditional fuel vehicles. In the internet age, secrets are hard to keep, but now they seem possible.

The deepest reason lies in the fact that the extent of the price increase for new cars does not directly equate to the increase in raw material costs.

Instead, it is determined during the final pricing session by executives and bosses 24-48 hours before the market launch.

Options include "sacrificing profits for sales volume" or "sacrificing some features to maintain pricing," with countless possibilities.

As the price war continues into 2026, on the surface, everyone seems to be maintaining stable prices, but a closer look reveals that the rhythm is changing. There may be more and more new cars slightly raising their official suggested retail prices under the banner of "comprehensive feature upgrades."

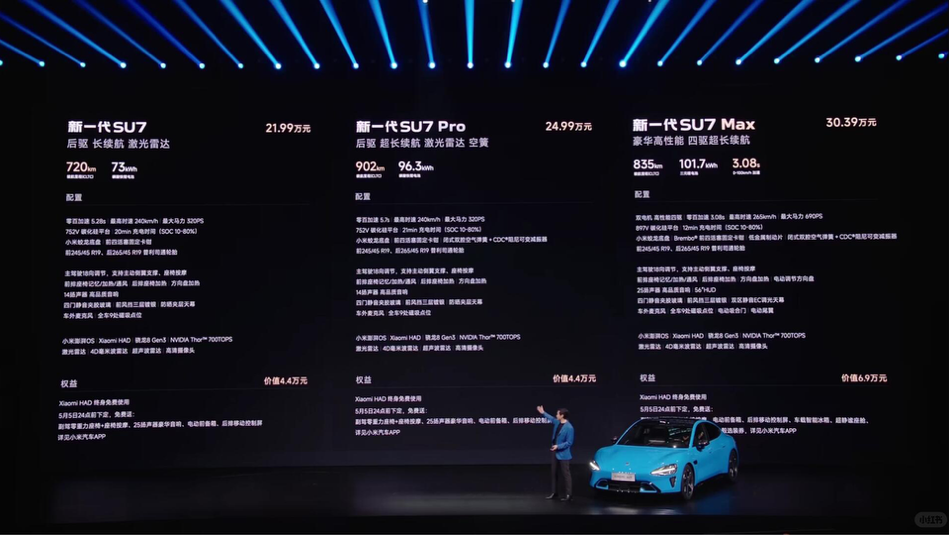

The strategy of the new-generation Xiaomi SU7 is straightforward: "piling on" hardware in terms of safety, intelligent driving, powertrain, and chassis, then only "slightly" raising the price. The entire lineup is equipped with LiDAR and NVIDIA Thor chips, with the standard/Pro versions pulling the high-voltage platform up to 752V and the Max version directly to 897V. The Pro and Max versions also upgrade the suspension to dual-chamber air suspension + CDC. In this context, not raising prices would be a surprise, and a price increase is reasonable... Lei Jun has once again managed consumer expectations perfectly. This type of price increase, justified by added features, makes consumers feel that their money is well spent.

Zeekr's approach is also clear. Lin Jie, Senior Vice President of Geely Automobile Group and General Manager of Zeekr Brand Sales Company, made it clear in an interview after the Zeekr 8X technology launch event: first, do their best to absorb the increased costs of raw materials within the system; second, respond through a combination of "adjusting features and pricing"; moreover, the 007/007 GT and 009 will soon be updated, focusing on fully rolling out capabilities like 900V high-voltage architecture and Thor chips, then "comprehensively considering costs and pricing." The underlying message is that price increases are not ruled out, but consumers will be made to recognize the value of the increases. This strategy aligns with that of the new-generation SU7.

Why does the Xiaomi SU7 have the qualification to "set the pace"? Because the first-generation Xiaomi SU7 had already stabilized the market for 200,000-300,000 yuan pure electric sedans before being discontinued. In the 2025 retail rankings for pure electric sedans priced above 200,000 yuan, the SU7 sold approximately 258,000 units, leading the Model 3's 200,000 units and becoming the annual sales champion in this price segment. This means it has established pricing authority within the same niche.

When the leader announces an upgrade accompanied by a price increase, it often provides a reference point for brands in the same price range. Once the anchor is set, subsequent new products are more likely to compete within a similar price band—you can be cheaper, but you'll have to explain "what's missing"; you can also be more expensive, but you'll need to justify "why"... This is a long-standing rule in the automotive market.

In the past few years, automakers have tried every tactic in the price war: direct reductions in suggested retail prices, cash subsidies, limited-time benefits, low-interest financing, trade-in subsidies... However, as cost curves rise and promotional effects on consumers weaken, the automotive market also needs such a shift.

From a consumer psychology perspective, this shifts "premium pricing" from brand narratives to verifiable evidence of "parameters and scenarios." In other words, it's no longer just about being "high-end" but telling you "how much charge can be added in 9-15 minutes of fast charging, whether urban NOA can be used, or how many kilometers per hour the moose test was passed at." When data and experiences are presented, "a slight increase" is easier to understand.

However, the complexity of the Chinese automotive market lies in the fact that there is no one-size-fits-all principle: brands that are turning around or desperately need a reputation reversal may even "sell at a loss" in the short term, using fully loaded features + large subsidies to regain their reputation. These "abnormal prices" will also coexist this year.

As a result, there will be cases where some manufacturers add features and raise prices, while others pile on benefits to the max. This is not a contradiction but a stratification: different brands have adopted different solutions.

In conclusion, it can be predicted that future price increases for new cars will increasingly occur under the guise of "added features." Therefore, faced with cost pressures, consumers planning to buy a car in 2026 will find it increasingly difficult to have it all.

-

![]()

The Unstoppable Rise of 'Optical Progress and Copper Decline': Sunny Optical’s Strategic Vision for the Next Decade

-

![]()

AI + Going Global in the Second Half: No Intermission for Robot Vacuum Cleaners

-

![]()

The Suffering Endured in E-commerce, Walmart Doesn't Want to Repeat in AI

-

![]()

What Does the Doubling of New Energy Vehicle Exports Mean?

-

![]()

Ghosn: 'Only I Can Save Nissan'

-

![]()

Volkswagen Lays Off 100,000 Employees, The Elephant Sits Down

-

![]()

Expanding Production Capacity! Yutong Optics Acquires Approximately 1.5 Hectares of Industrial Land in Chang'an, Dongguan

-

![]()

Why Is Nokia Making a Comeback in the AI Era?