February’s Sluggish Sales: Not All Gloom—Is This the Best Time for Car Buyers?

03/23 2026

03/23 2026

468

468

February’s lackluster sales figures came as no surprise, but should we still keep a close eye on March for signs of recovery in the auto market?

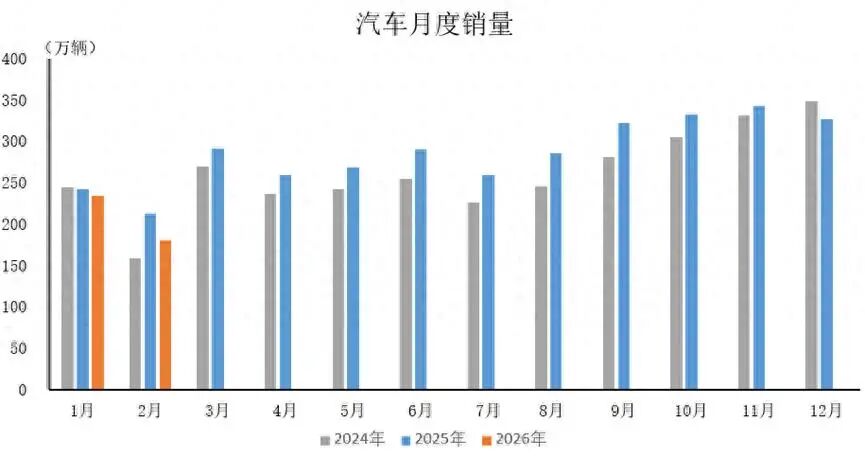

While the industry was mentally prepared, there was a collective gasp when the China Association of Automobile Manufacturers (CAAM) released last month’s data. In February 2026, automobile production and sales stood at 1.672 million and 1.805 million units, respectively, marking double-digit declines both month-on-month and year-on-year.

These dismal figures were somewhat anticipated—after all, February had only 16 effective working days. Coupled with the policy stimulus at the end of the previous year, which pre-emptively consumed much of the purchasing power, a market cooldown was almost inevitable. However, this cannot be solely attributed to the “holiday effect,” as January’s auto market also faced challenges. The entire first quarter has presented automakers with a less-than-impressive performance. Hence, major brands, holding their breath, are likely gearing up to make a significant push in March.

New Technologies, High Discounts—Automakers Must Step Up Their Game

With sales pressure mounting, automakers are not sitting idly by. The hottest topic in the auto circle recently has been BYD’s “Flash Charge China” launch event. The debut of the second-generation Blade Battery has excited many tech enthusiasts. Charging from 10% to 97% in just 9 minutes—this speed is nearly comparable to filling a gas tank. During a highway trip, a restroom break and a coffee purchase would be enough time to nearly fully charge the vehicle, gradually alleviating the last bit of range anxiety for pure electric vehicles.

Of course, it takes time for new technologies to transition from launch to widespread adoption. BYD plans to construct 20,000 flash charging stations nationwide by the end of the year, an undoubtedly massive undertaking. However, for consumers on the fence, such technological breakthroughs serve as a morale booster, intensifying the psychological tug-of-war between “waiting a bit longer” and “buying now.”

Meanwhile, another more direct incentive is unfolding intensively in March. Step into any car showroom in a mall, and you’ll frequently hear sales advisors mention “7-year ultra-low interest” plans. Whether it’s BYD’s Ocean Network, NIO, or Leapmotor, all are offering extended financial installment plans.

The appeal of such financial promotions lies in their ability to lower the purchasing threshold without directly slashing prices and harming the brand. Daily payments as low as a few dozen yuan carry significant appeal for young families mindful of cash flow planning. It is foreseeable that in the coming month, as automakers strive to meet first-quarter targets, similar “price endurance” preferential policies will only increase, not decrease. After all, for most ordinary families, beyond the future promises brought by new technologies, the pressure of monthly loan repayments is the most tangible consideration at present.

Overseas Sales Outpace Domestic, but Geopolitics Loom Large

In stark contrast to the domestic market’s chill, the export sector is thriving. In February, automobile exports reached 672,000 units, up over 52% year-on-year. More surprisingly, several automakers’ overseas sales surpassed their domestic figures. For instance, BYD’s overseas sales reportedly accounted for over half of its total, while Chery’s February exports made up more than 70% of its sales volume. Such a scenario was hard to imagine before—what used to be seen as mere “exploratory trips” overseas has now evolved into establishing a solid presence and reaping rewards.

Behind this transformation lies a tangible improvement in China’s automotive product competitiveness. In the Middle Eastern market, high temperatures and sandy environments pose rigorous tests for vehicle thermal management and air conditioning systems. Chinese brands have won local consumers’ recognition through localized adaptations and rich configurations. In Southeast Asia, electric pickup trucks and SUVs, with their novel designs and smart experiences, are encroaching on the traditional turf of Japanese vehicles. Overseas market growth has indeed partially offset the decline risks during the domestic off-season.

However, after years of editing and witnessing international fluctuations, concerns linger. Geopolitical conflicts in the Middle East hang like a sword of Damocles. Huatai Securities research notes that short-term geopolitical disruptions, such as conflicts between the US, Israel, and Iran, could suppress exports, estimating the affected Middle Eastern market size at around 300,000 units. CAAM experts also admit that while exports performed well in the first two months, March’s data remains uncertain due to regional conflicts. For instance, Iran, a key export destination for Chinese automobiles, could see logistical and settlement issues escalate if the situation deteriorates.

Rising Fuel Prices—A Boon for New Energy Vehicles?

As the auto market frets over sales, domestic fuel prices hit their biggest year-to-date increase on March 10, adding over 20 yuan to fill a tank. International oil prices surged past $110 per barrel, driven by the invisible hand of geopolitical conflicts. For ordinary fuel vehicle owners, monthly fuel bills have become glaring; for prospective car buyers, this undoubtedly adds significant weight to the psychological scales in favor of new energy vehicles.

Analyzing the numbers, while this year’s purchase tax incentives for new energy vehicles have slightly diminished, the policy adjustments did pre-emptively consume demand for some A00-class microcars (like the Wuling Hongguang MINI EV), leading to a sales decline in the first two months. However, when considering the long-term impact of rising fuel prices, the calculation changes. A recent UBS report analyzes it clearly: rising fuel prices could increase annual operating costs for fuel vehicles by about 2,000 yuan, while battery costs are declining—the price of lithium iron phosphate batteries is now less than half of early 2022 levels. This dynamic enhances the full lifecycle cost advantage of electric vehicles.

This cost advantage is subtly reshaping car selection criteria. Data shows that while A00-class microcar sales have declined, B-class new energy vehicles are growing against the trend, indicating a market shift from mere “policy subsidies” to “product strength.” Especially against the backdrop of high fuel prices, models like extended-range and plug-in hybrids, which eliminate range anxiety while offering electric drive economy, have become top choices for many family users.

Conclusion

Returning to our initial question, while this year’s economic environment seems fraught with uncertainty, it’s not all bad news for auto consumption. High fuel prices will accelerate the transition from fuel vehicles to new energy vehicles, while automakers, vying for existing users, will unveil more hardcore technologies like flash charging and flexible financial policies. For consumers holding cash, the March-June period might offer a sweet spot—on one hand, waiting for revolutionary technologies like BYD’s flash charging to become widely available; on the other, negotiating relatively favorable prices in the market. As for overseas prospects, while geopolitics remains an unavoidable variable, Chinese automobiles, backed by a complete industrial chain and product competitiveness, will continue their global expansion, albeit with more flexible and diversified approaches. Though the first quarter may be cold, the auto market’s spring often sprouts amid fierce competition.

-

![]()

The Unstoppable Rise of 'Optical Progress and Copper Decline': Sunny Optical’s Strategic Vision for the Next Decade

-

![]()

AI + Going Global in the Second Half: No Intermission for Robot Vacuum Cleaners

-

![]()

The Suffering Endured in E-commerce, Walmart Doesn't Want to Repeat in AI

-

![]()

What Does the Doubling of New Energy Vehicle Exports Mean?

-

![]()

Ghosn: 'Only I Can Save Nissan'

-

![]()

Volkswagen Lays Off 100,000 Employees, The Elephant Sits Down

-

![]()

Expanding Production Capacity! Yutong Optics Acquires Approximately 1.5 Hectares of Industrial Land in Chang'an, Dongguan

-

![]()

Why Is Nokia Making a Comeback in the AI Era?