From the 'Japanese Era' to the 'Chinese Moment': A Century-Old Reshuffle in the Global Auto Market

03/23 2026

03/23 2026

633

633

The unprecedented upheaval in the auto market over the past century is just beginning.

Japanese automakers no longer 'dominate' the global market.

In March 2026, data from Nihon Keizai Shimbun showed that in 2025, Chinese automakers achieved cumulative global sales of nearly 27 million vehicles, up about 10% year-on-year, surpassing Japanese automakers' 25 million vehicles to claim the top spot in global sales for the first time.

This historic breakthrough ended the 25-year 'dominance' of Japanese automakers since 2000, once again focusing the global automotive industry's attention on the rising automotive powerhouse in the East.

Behind these figures lies the miracle of Chinese automakers' 'lane-changing overtaking' in the new energy sector. From power batteries to intelligent connected vehicles, from technological R&D to market applications, Chinese automakers have swiftly seized the commanding heights of the new energy era. In contrast, Japanese automakers are stumbling in the wave of transformation, from hesitancy in technological routes to sluggish market responses, from the gradual loss of traditional advantages to a continuous decline in innovation capabilities.

This reshuffle in the global auto market has not only changed the competitive landscape of the automotive industry but also reshaped the power structure of the global industrial system.

The alternate (alternation) of old and new in the global market

In stark contrast to the rapid advancement of Chinese automakers, Japanese automakers faced overall pressure in 2025. Except for Toyota and Suzuki, other major manufacturers experienced sales declines, reflecting their hesitation and passivity in the new energy transition.

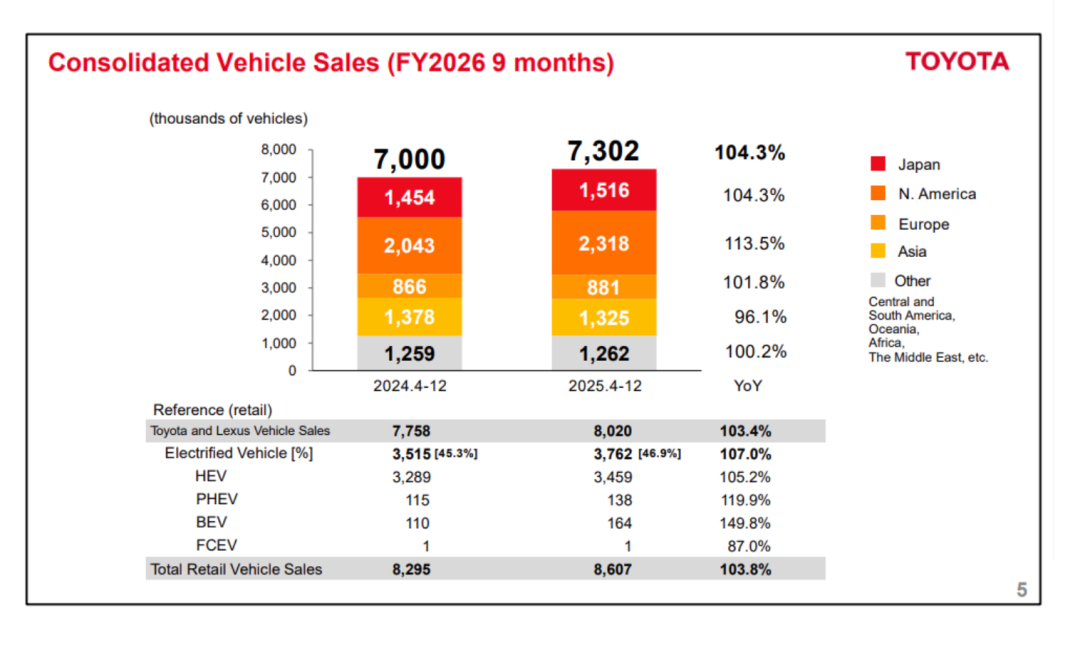

Toyota remained the world's top-selling automaker for the sixth consecutive year with 11.32 million vehicles sold, but this achievement relied heavily on its market foundation in traditional fuel vehicles and hybrid models.

In the pure electric vehicle sector, Toyota's progress has been slow. In 2025, pure electric models accounted for less than 5% of its sales, far below the average level of Chinese automakers. Toyota's 'conservatism' stems from its path dependence on hybrid technology and misjudgment of the pure electric market, causing it to gradually fall behind in the global new energy wave.

Honda and Nissan experienced more pronounced declines.

Honda's sales fell by 8% to 3.52 million vehicles in 2025, dropping to ninth place. Its sales in the Chinese market plummeted by 24%, becoming the main reason for its performance slump. Honda was slow to transition to new energy, with its seven pure electric models performing poorly in the market. Eventually, it had to cut 30% of its electric vehicle R&D budget and delegate more authority to its Chinese R&D team.

Nissan's sales fell by 4% to 3.2 million vehicles, falling out of the global top ten for the first time since 2004 and being surpassed by Suzuki. Its sales in the Chinese market have declined for seven consecutive years, and global sales of its electric model, the Leaf, fell by 12%. Insufficient new energy technology reserves and sluggish market responses have become fatal weaknesses for Nissan's development.

The collective predicament (predicament) of Japanese automakers is essentially the failure of their 'successful experiences in the fuel vehicle era' in the new energy era. For a long time, Japanese automakers have dominated the global market with their technological advantages in fuel vehicles and refined management. However, under the wave of electrification and intelligence, their technological iteration speed has slowed, and product innovation has been insufficient, making it difficult to meet global consumers' demand for new energy vehicles.

At the same time, the weak performance of the Japanese domestic market, with sales down 15% year-on-year in 2025, further exacerbated their performance pressure.

In contrast, the global sales leadership this time is backed by the systemic breakthroughs of Chinese automakers centered on new energy. Among them, BYD and Geely have become the 'dual engines' driving the rise of Chinese automakers.

BYD achieved sales of 4.6 million vehicles in 2025, up 8% year-on-year, surpassing Ford to rank sixth globally and defeating Tesla with an absolute advantage in the pure electric vehicle sector to become the global pure electric sales champion. Its overseas sales exceeded 1 million vehicles for the first time, accounting for 20% of its total sales.

Industry analysts believe that BYD's success stems from its vertically integrated capabilities across the entire industrial chain, from power batteries and IGBT chips to vehicle manufacturing, building a self-controlled new energy vehicle ecosystem. BYD also accurately grasped global market demand, launching targeted products in Southeast Asia, Europe, South America, and other regions. For example, it established a production base in Brazil, achieving production in just 15 months, demonstrating the deep integration of 'Chinese speed' and localized operations.

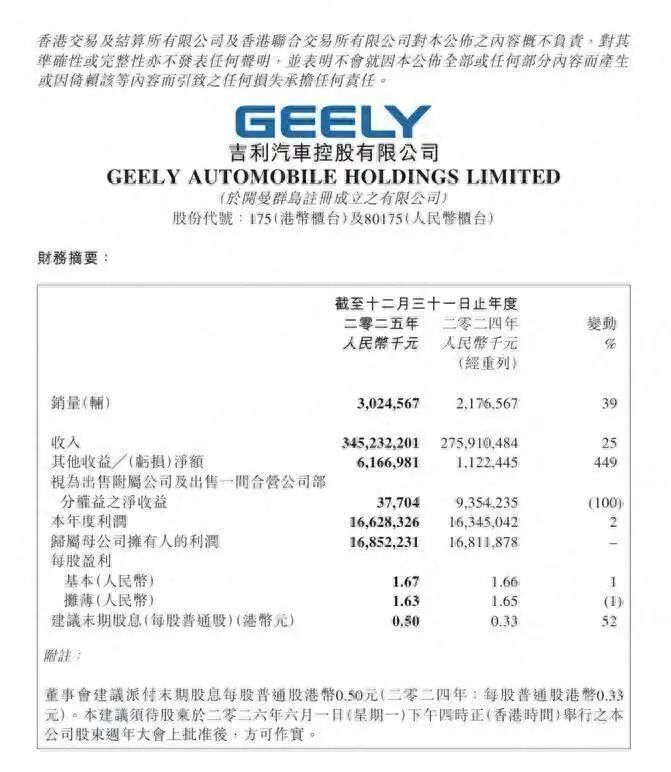

Geely Auto pushed its sales up to 4.11 million vehicles with a 23% growth rate, rising to eighth place globally.

Geely's rise is attributed to its 'multi-brand matrix + global R&D' strategy. The Zeekr brand targets the high-end market, the Galaxy brand focuses on the mainstream new energy sector, and the Geometry brand deep cultivation (cultivates) the entry-level market. At the same time, Geely has established a global '1+7+N' R&D center network, developing localized products for different regional markets, achieving an upgrade from price advantages to technological advantages.

In addition to BYD and Geely, six other Chinese automakers, including Chery, Changan, SAIC, and Great Wall, ranked among the top 20 in global sales, surpassing Japan's five companies. Chery's overseas sales reached 1.2944 million vehicles in 2025, up 33.2% year-on-year, accounting for 49.2% of its total sales, ranking first among Chinese brand passenger vehicle exports for 23 consecutive years. SAIC Group broke through 300,000 vehicles in the European market with its MG brand, with hybrid model sales surging 300% year-on-year, showcasing the diversified advantages of Chinese automakers in the new energy technology sector.

Opportunities and challenges coexist

Chinese automakers' claim to the top spot in global sales this time is not accidental but the inevitable result of China's automotive industry's 'lane-changing overtaking' in the new energy sector.

From product exports to industrial exports, Chinese automakers are deepening their global layout . For example, BYD has established production bases in Brazil and Thailand, Geely plans to acquire Nissan's Mexican factory, and Chery has globally deployed R&D centers and service networks. Chinese automakers are shifting from simple product exports to localized production, technology exports, and brand operations.

According to data, China exported over 7 million vehicles in 2025, up 21.1% year-on-year, with new energy vehicle exports accounting for over 40%, showcasing strong market competitiveness. At the same time, Chinese power battery companies such as CATL and SVOLT are accelerating their overseas layout (presence), with businesses covering Europe, South America, Southeast Asia, and other regions, providing industrial chain support for Chinese automakers' globalization.

On the other hand, from price advantages to technological advantages, the core competitiveness of Chinese automakers is also upgrading.

In the electrification sector, Chinese automakers have mastered core technologies such as power batteries, motors, and electronic controls. BYD's Blade Battery and CATL's Qilin Battery are at the global leading level. In the intelligence sector, Chinese automakers have achieved breakthroughs in autonomous driving and in-vehicle systems. The deep participation of tech companies such as Huawei and Xiaomi has further enhanced the intelligence level of Chinese automobiles.

These technological advantages are being converted into market advantages, driving the continuous improvement of Chinese automotive brand value.

Obviously, in the face of the rise of Chinese automakers, global automotive industry competition will become more intense, and Chinese automakers will also face more challenges, including the rise of global trade protectionism, such as the EU imposing tariffs on Chinese pure electric vehicles and the U.S. introducing the Inflation Reduction Act, which bring pressure to Chinese automakers' overseas expansion.

Taking the Inflation Reduction Act as an example, according to its provisions, starting from 2024, vehicles containing any battery components manufactured or assembled by foreign sensitive entities will lose eligibility for tax credits. By 2025, this provision will extend to key minerals such as lithium, cobalt, and nickel required for battery manufacturing. This means that Chinese electric vehicles exported directly to the U.S. will hardly be eligible for the $7,500 tax credit, severely weakening their market competitiveness.

Although China and the EU reached a consensus in January 2026 to replace the current tariffs with a 'minimum import price' mechanism, this alternative scheme is still a de facto market access restriction.

On the other hand, as competition in the global new energy vehicle market intensifies, European, American, Japanese, and Korean automakers are accelerating their transitions, forming an encirclement against Chinese automakers. Brand premiumization (upscaling) remains a long road ahead, with Chinese automakers still having a low share in the global high-end market, requiring continuous technological investment and brand building.

However, the opportunities are also enormous. The global new energy vehicle market is still in a period of rapid growth. According to the International Energy Agency, global new energy vehicle sales are expected to reach 40 million vehicles by 2030, offering vast market space. The technological advantages of Chinese automakers in electrification and intelligence will become their core weapons in global competition. With the export of Chinese automotive industry standards, Chinese automakers will have more say in the global industrial system.

Overall, the unprecedented upheaval in the auto market over the past century is just beginning. The 25-year 'dominance' of Japanese automakers has ended, and Chinese automakers have claimed the top spot in global sales for the first time. This is not only a ranking alternation between two automotive powers but also a landmark event in the century-old upheaval of the global automotive industry.

For Japanese automakers, this is not the end but an alarm bell compelling them to completely break free from path dependence and accelerate their transformation. For Chinese automakers, claiming the top spot is just a new starting point. Trade protectionist barriers, the encirclement of global automakers, and shortcomings in the high-end market are all real challenges on the road ahead.

We should also see that the huge increment (growth) in the global new energy market, China's technological accumulation in electrification and intelligence, and the in-depth layout (presence) of industrial exports are all the confidence to navigate through cycles.

From 'following' to 'keeping pace' and then to 'leading,' the Chinese automotive industry has completed in a few decades the journey that the West took a century to achieve. However, the real test has never been a momentary sales lead but whether it can continuously innovate amid technological iterations, build an irreplaceable industrial ecosystem in global competition, and win long-term recognition from global consumers in brand building.

Note: Some images are sourced from the internet. If there is any infringement, please contact us for deletion.

-END-

-

![]()

The Unstoppable Rise of 'Optical Progress and Copper Decline': Sunny Optical’s Strategic Vision for the Next Decade

-

![]()

AI + Going Global in the Second Half: No Intermission for Robot Vacuum Cleaners

-

![]()

The Suffering Endured in E-commerce, Walmart Doesn't Want to Repeat in AI

-

![]()

What Does the Doubling of New Energy Vehicle Exports Mean?

-

![]()

Ghosn: 'Only I Can Save Nissan'

-

![]()

Volkswagen Lays Off 100,000 Employees, The Elephant Sits Down

-

![]()

Expanding Production Capacity! Yutong Optics Acquires Approximately 1.5 Hectares of Industrial Land in Chang'an, Dongguan

-

![]()

Why Is Nokia Making a Comeback in the AI Era?