The Midfield Battle of China's New Energy Vehicles Has Begun—How to Define the Path for the 2.0 Era?

03/23 2026

03/23 2026

497

497

At the 2026 CheBaiHui Research Institute Expert Media Exchange Conference, Ouyang Minggao, an academician of the Chinese Academy of Sciences, delivered a speech with a clear judgment: China's NEVs are standing at a midfield crossroads, and the ultimate outcome of this industrial revolution has been anchored in pure electric drive from the very beginning.

▍From 1.0 to 2.0: Model Reconstruction Leads Industrial Competition

The market generally views the 2025 milestone—when domestic NEV penetration exceeds 50%—as the conclusion of the first half of the industry's electrification era. Ouyang Minggao, however, defines this stage as the NEV 1.0 era, characterized by explosive electrification growth, nurturing intelligence, and the initial steps toward decarbonization.

In 2010, China established its 'pure electric drive' strategy and launched NEV subsidy pilots, kicking off the industry's marketization. By 2018, domestic NEV annual sales surpassed 1 million units, marking a critical step in marketization. In 2021, breakthroughs in passenger vehicle lithium iron phosphate battery systems propelled the industry into an era of explosive electrification, with full-year sales reaching 3.52 million units. By 2025, domestic NEV production and sales reached 16.626 million and 16.49 million units, respectively, up 29% and 28.2% year-on-year, completing a transformation from 'follower' to 'leader.'

Currently, the industry is in a critical transitional phase from the 1.0 to the 2.0 era. Ouyang Minggao states that the NEV 2.0 era—the era of intelligent electric vehicles—will be defined by explosive intelligence growth, optimized electrification, and accelerated decarbonization. The core of industrial competition will shift from the 1.0 era's binary question of 'whether EVs can be built' to the 2.0 era's hierarchical competition over 'whether intelligent EVs with core competitiveness can be built.'

China's rise as the global hub for NEVs is inseparable from industrial model innovation and reconstruction. Five distinct industrial models with clear development paths have emerged domestically, reshaping the global automotive industry's rules. These five models—each with unique strengths—will compete, converge, and iterate, becoming the core of 2.0-era competition.

The first model is the electrification-led vertical integration model represented by BYD. BYD's extreme cost-control capabilities stem from its full-chain vertical integration, covering everything from battery systems to automotive-grade chips, semiconductors, and vehicle manufacturing. This self-sufficiency in core components, combined with economies of scale, has built a formidable cost moat.

The second model is the intelligence-led horizontal integration model represented by Huawei's ecosystem. Breaking free from traditional automakers' closed loops, Huawei builds cross-brand alliances centered on intelligence capabilities. Through its 'HiCar' mode, it deeply collaborates with multiple automakers like Seres and Chery, creating a market-wide brand matrix. Its core competitiveness lies in localized capabilities for HarmonyOS smart cockpits and ADS high-level intelligent driving.

The third model is the new-force internet-based automaking model represented by NIO, XPeng, Li Auto, and Xiaomi. Centered on internet thinking, these companies leverage smart terminal marketing and user ecosystem operations, using electrification as an entry point for intelligence. They break away from traditional vehicle sales profit models, building brand ecosystems and user loyalty through deep user engagement, forming unique core advantages in intelligence.

The fourth model is the dual-drive model of independent brands represented by Geely, Chery, and Great Wall. These companies, with deep roots in the gasoline vehicle era, adopt a 'gasoline + electric' dual-drive strategy and a 'domestic + international' dual-market layout. Their future hinges on balancing trends: gasoline vehicles evolving toward large-battery HEVs and NEVs advancing toward pure electric.

The fifth model is the state-owned enterprise (SOE) self-reliance + joint venture reform model, led by central automotive SOEs and local state-owned enterprises. Leveraging state-owned resources for integration and industrial chain synergy, this model fuses strengths from other approaches, unlocking vitality through institutional reforms and combining the 'ballast' role of state assets with the innovative capabilities of entrepreneurial teams.

Ouyang Minggao emphasizes that these five development models represent viable paths explored by Chinese automakers amid industrial transformation, with no absolute superiority. The competition in the NEV 2.0 era will essentially be a clash, convergence, and iteration of these five models. Whoever can first refine and execute their model will seize the initiative in the next decade of industrial competition.

▍Why Must the Ultimate Outcome Be Pure Electric?

In recent years, industry debates over NEV technical routes have persisted: some argue that hybrid vehicles, with no range anxiety, are the optimal solution for the domestic market; others claim hydrogen fuel is the true zero-emission path, viewing pure electric as merely transitional; some even suggest e-fuels could extend the lifecycle of gasoline vehicles, deeming it premature to declare pure electric as the endgame.

Addressing this core industry controversy, Ouyang Minggao provided a definitive conclusion in his speech: the industrial endgame for NEVs must be pure electric drive. The future industry landscape will feature a energy-transportation convergence system centered on pure electric vehicles (EVs) with widespread vehicle-grid interaction (VGI).

First, pure EVs boast the industry's highest green electricity utilization efficiency, with unmatched energy advantages over other routes. Ouyang cited key data: pure EVs utilize green electricity twice as efficiently as green hydrogen vehicles and four times as efficiently as e-fuel internal combustion engine vehicles. Under the same scale of green electricity supply, pure EVs can achieve far greater driving ranges than other technologies. Against the backdrop of global carbon neutrality strategies, energy utilization efficiency directly determines a technology's long-term viability.

Second, pure EVs are the only vehicle type capable of deep integration with the new energy system. Multiple Chinese cities have already launched VGI demonstration projects, allowing users to offset charging costs or even earn profits through peak-valley electricity pricing. Future pure EVs will function as generators, energy storage units, and consumers, fully integrating into the new energy ecosystem.

Third, pure EVs offer significant cost advantages. Most models now have per-kilometer electricity costs below 0.1 yuan, just one-fifth of comparable gasoline vehicles. As green electricity becomes more widespread and distributed photovoltaics + VGI are implemented, energy costs will decline further, potentially reaching zero or even negative costs per kilometer.

Fourth, pure EVs are naturally suited for high-level autonomous driving, making them the ideal carrier (platform) for the intelligence era. The core of high-level autonomy is millisecond-precise vehicle control, and pure EVs' motor control systems respond at millisecond speeds—far faster than gasoline vehicles' engine and transmission systems—perfectly matching the control demands of advanced autonomous driving systems. Ouyang predicted that by 2030, L4 autonomous passenger vehicles based on advanced end-to-end large models will achieve mass commercialization in the mid-to-high-end market, a goal dependent on pure electric drive and its deep integration with intelligence.

Fifth, pure EVs represent China's most globally competitive automotive category. In 2025, China's NEV exports surpassed 2.615 million units, with pure EVs accounting for approximately 62.9%—a core pillar in China's transition from an automotive giant to a powerhouse.

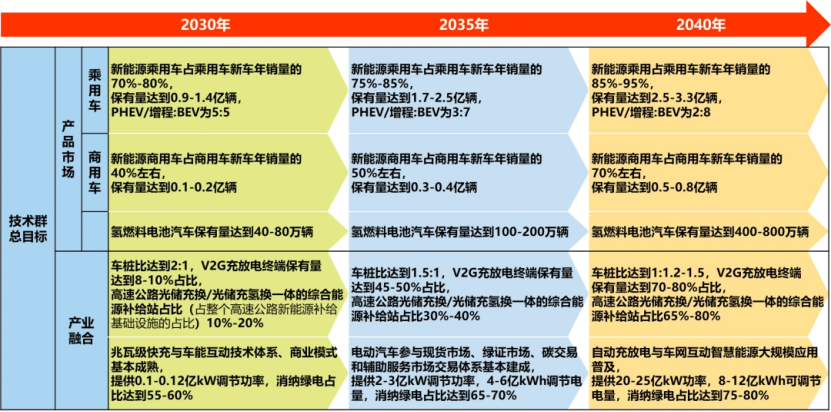

Based on his endgame judgment of pure electric drive, Ouyang also outlined a clear timeline for industrial development: By 2030, the industry will enter the NEV 3.0 era—the era of new energy intelligent electric vehicles—characterized by explosive decarbonization, optimized intelligence, and deepened electrification. By then, non-fossil fuel power generation will exceed 50% domestically, all-solid-state batteries will achieve mass production, and VGI will begin widespread adoption. By 2035, NEV penetration among domestic passenger vehicles will reach 75%-85%, with pure EVs accounting for over 70%. Green electricity will become the primary charging source, and VGI energy storage will surpass stationary battery storage in scale, with 200-300 million EVs on China's roads. By 2040, NEV penetration will further rise to 85%-95%, with the remaining market share primarily occupied by large-battery hybrid models serving remote areas and special scenarios with limited charging infrastructure.

Some market views suggest the NEV industrial competition is already settled, but in reality, after electrification barriers are fully broken, the industry is entering a broader development space. Beyond anchoring decarbonization as the ultimate goal, the key lies in promoting deep integration between NEVs and the new energy system to create a new ecosystem converging transportation and energy.

Layout 丨 Yang Shuo Image sources: CheBaiHui Research Institute, Qianku.com

-

![]()

The Unstoppable Rise of 'Optical Progress and Copper Decline': Sunny Optical’s Strategic Vision for the Next Decade

-

![]()

AI + Going Global in the Second Half: No Intermission for Robot Vacuum Cleaners

-

![]()

The Suffering Endured in E-commerce, Walmart Doesn't Want to Repeat in AI

-

![]()

What Does the Doubling of New Energy Vehicle Exports Mean?

-

![]()

Ghosn: 'Only I Can Save Nissan'

-

![]()

Volkswagen Lays Off 100,000 Employees, The Elephant Sits Down

-

![]()

Expanding Production Capacity! Yutong Optics Acquires Approximately 1.5 Hectares of Industrial Land in Chang'an, Dongguan

-

![]()

Why Is Nokia Making a Comeback in the AI Era?