XPENG Finally Makes a Profit, But Not from Selling Cars

03/24 2026

03/24 2026

592

592

XPENG has reached a critical turning point.

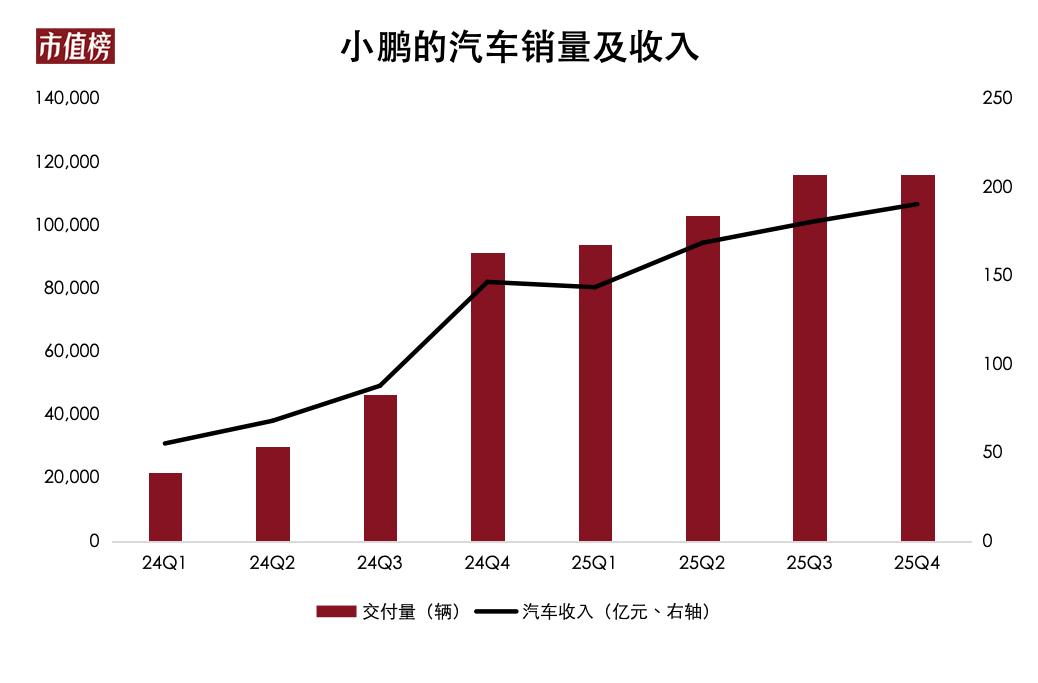

Financials released on March 20 show XPENG's annual revenue hit RMB 76.72 billion, up 87.7% YoY, a record high; 429,000 vehicles were delivered throughout the year , up 125.9% YoY.

More importantly, a net profit of RMB 380 million was achieved in Q4, marking XPENG's first profitable quarter.

For a new energy vehicle (NEV) player founded over a decade ago with cumulative losses in the billions, this is undoubtedly a milestone.

But can this mark a new starting point for XPENG? In other words, how was this first profit achieved, and is it sustainable? With NEV penetration exceeding 60%, how is XPENG positioning its automotive business and physical AI?

I. The True Value of First Quarterly Profit

The conclusion is that XPENG's profitability has indeed improved, but it is far from the point where 'Q4 marks the transition from losses to profits.' Sustained profitability remains uncertain.

In Q4 2025, XPENG's other income reached RMB 840 million, exceeding quarterly net profit and more than tripling YoY, mainly due to increased government subsidies.

Of course, as mentioned earlier, XPENG's performance has significantly improved.

Excluding subsidies, taxes, and interest—factors less related to core operations—profitability is measured by 'gross profit minus three major expenses (sales, R&D, and administrative costs).' Under this metric, 'losses' in Q4 2025 more than halved YoY, with the 'loss rate' dropping from 12.2% to 4.2%.

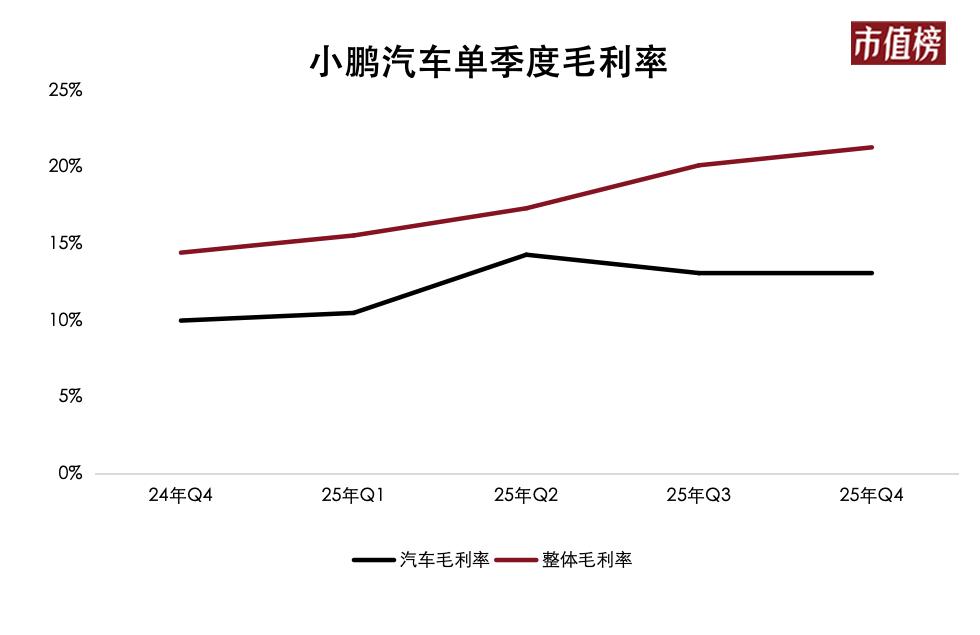

XPENG's Q4 financials were impressive: revenue of RMB 22.25 billion, up 38.2% YoY; deliveries of 116,000 vehicles, a record high; and a gross margin of 21.3%, also a record.

A 20% gross margin is considered a key threshold for NEV makers' profitability and technological moat. XPENG's margin even surpassed Tesla's and BYD's.

So, how did the 21.3% gross margin come about?

Mainly through lighter-asset businesses, i.e., providing R&D services to partner automakers.

In Q4, service and other revenues, including technical service income, had a gross margin exceeding 70%, contributing 48% of gross profit with just 14% of revenue.

Benefiting from this, XPENG's overall gross margin kept hitting new highs. Collaboration with Volkswagen in intelligent driving, chips, and electronic architecture helped XPENG break free from the traditional 'selling cars for profit' model.

However, XPENG's performance in selling cars was far less impressive than 'selling technology.'

In Q4, automotive revenue was RMB 19.07 billion, up 30% YoY, with a vehicle gross margin of 13%, up 3 percentage points YoY but down 0.1 percentage points QoQ and 1.3 percentage points from Q2.

A 13% vehicle gross margin is unremarkable among NEV makers. To sustain profitability, vehicle margins need further improvement, and economies of scale must continue to take effect.

This explains why XPENG's Q1 guidance raised concerns in the market.

In January and February, XPENG delivered 20,000 and 15,000 vehicles, respectively, totaling just 35,000. While in line with industry trends, this performance was relatively weak. XPENG's Q1 guidance was even lower at 61,000–66,000 units, down ~30–35% YoY, below market expectations; revenue was projected at RMB 12.2–13.28 billion, down 16–22.8% YoY.

Of course, Q1 is traditionally a slow season for car sales, especially this year with greater pressure from purchase tax phase-out. The issue is that XPENG's product offensive in Q1 was not weak.

In January, the P7+ and G7 extended-range and BEV versions were launched, along with BEV versions of the G6 and G9; in March, the G6 extended-range version followed. The P7+ and G7 extended-range models feature a 1.5T range extender, CLTC pure electric range of 430 km, and combined range of 1,550–1,704 km, with an aggressive pricing strategy: the P7+ and G7 extended-range models are priced the same as their BEV counterparts, while the G6 extended-range version is RMB 10,000 more expensive than the BEV version. The new models offer increased features without price hikes, aiming to capture market share at the start of 2026.

But judging by January and February delivery numbers, the explosive potential of the new product cycle remains to be seen.

II. Product Matrix: MONA Leads, Extended-Range Fills Gaps

XPENG's sales mix underwent a fundamental shift in 2025.

Multiple data sources report that the low-priced MONA M03 accounted for over 40% of total 2025 sales, making it XPENG's undisputed flagship model, followed by the slightly higher-priced P7+. The other three BEV SUVs—G6, G7, and G9—performed average.

This means XPENG's sales increasingly rely on models priced below RMB 200,000.

This structure has two consequences: first, sales volume surged, with the full-year total of 429,000 units being impressive; second, the average selling price (ASP) per vehicle dropped to ~RMB 159,200 in 2025, down RMB 29,000 from 2024.

But the flip side is that brand positioning is being dragged down.

When a brand's flagship models shift from the G-series priced above RMB 200,000 to the MONA priced just above RMB 100,000, 'XPENG' in users' minds becomes increasingly associated with 'cost-effectiveness' rather than 'technology' or 'premium.'

Profit margins on vehicles priced in the tens of thousands are capped. If XPENG continues to rely on the MONA, true profitability may remain elusive.

MONA's success kept XPENG alive, but to thrive, it must establish a foothold and achieve volume in higher price segments.

In 2026, XPENG's product strategy centers on 'one model, dual capabilities,' meaning parallel development of BEV and extended-range models.

2026 is a major product year for XPENG. The January launches were just the beginning; four new models are planned for release this year.

To prepare for this 'product super year' and make strategic upfront investments in AI, XPENG's administrative and sales expenses reached RMB 2.79 billion in Q4 2025, up RMB 300 million QoQ due to terminal marketing and channel expansion. R&D expenses increased by RMB 450 million QoQ, with both expense increases outpacing revenue growth.

Doubling down on extended-range technology at this juncture will undoubtedly raise questions, such as whether XPENG is moving backward.

However, He Xiaopeng believes extended-range technology will be needed for 10–20 years. He pushed for extended-range powertrains five times before finally launching them. He also has high expectations for extended-range sales.

In January, the X9 extended-range version delivered 4,219 units in a single month, with cumulative deliveries exceeding 50,000 units. This performance validated market demand. The X9 super extended-range model gained unexpected popularity in northern and inland cities, with pre-sale orders matching those of the same period.

From a market demand perspective, Li Auto, AITO, and Leapmotor all have popular extended-range models. However, data also shows slowing growth in extended-range vehicles: 1.235 million extended-range electric vehicles (EREVs) were sold in 2025, up 6.0% YoY, lagging behind BEVs (24.4%) and plug-in hybrids (8.8%).

Additionally, the 2026 passenger vehicle market outlook is pessimistic, with the China Passenger Car Association (CPCA) projecting just 1% growth and the China Association of Automobile Manufacturers (CAAM) even more conservative at 0.5%. Whether XPENG's extended-range models can replicate the X9's success remains uncertain, given market capacity and competition.

Zooming out to the global stage, the situation looks better.

Overseas public charging stations account for about one-third of the global total, making extended-range models a necessity for overseas expansion.

In 2025, XPENG delivered 45,000 vehicles overseas, up 96% YoY, ranking first among Chinese new NEV makers in BEV export sales. To continue expanding, extended-range models are almost mandatory.

III. AI Narrative: XPENG's Next Major Battle

With NEV penetration exceeding 60%, NEV makers are seeking new narratives or second growth curves.

AI is the most consensus-driven and imaginative option.

Li Auto is betting on embodied AI, with Li Xiang stating that 2026 represents the 'last window to become a global AI leader'; NIO is laying the groundwork for autonomous driving and embodied AI with its self-developed 5nm intelligent driving chip, which Li Bin calls 'preparing for the AGI era'; Seres is anchoring its strategy in 'AI+', with Zhang Xinghai explicitly stating a push into mobile intelligent agent business.

XPENG has upgraded its positioning to 'a pioneer in mobility within the physical AI world and a global embodied AI company.'

In 2025, XPENG's R&D spending reached RMB 9.49 billion, up 47.0% YoY, with AI-related investments accounting for RMB 4.5 billion. In 2026, this figure will rise further to RMB 7 billion.

Intelligent driving is the starting point for physical AI.

XPENG's intelligent assisted driving was once in the top tier, but this strength was gradually caught up or even surpassed by latecomers. It wasn't until the second-generation VLA (Vision-Language-Action) model that XPENG regained its leading position in intelligent driving.

To explore the VLA technical route, the company has invested 30,000 GPU cards in computing power since 2024, burning over RMB 2 billion in training costs. For a long time, discussions were held multiple times about whether to abandon VLA due to a lack of visible progress. In Q2 2025, VLA 2.0 achieved a major breakthrough, advancing XPENG's autonomous driving technology upgrade by 'nearly two years.'

In Q1 2026, the second-generation VLA model began rolling out to Ultra models. This model is applicable not only to vehicles but also to four types of embodied AI terminals: Robotaxi, humanoid robots, and flying cars.

The Turing chip is another ace for XPENG. The Turing chip has been selected by Volkswagen for global use, becoming the first Chinese self-developed intelligent driving chip supplied to an international automaker. The first co-developed model, the 'Zoy 08,' began mass production in March.

In robotics, the mass production (mass-produced) version of the humanoid robot IRON has completed testing, with a target of achieving mass production by the end of 2026. He Xiaopeng set a more specific goal at the earnings call: monthly production capacity exceeding 1,000 units by year-end.

The Robotaxi business is also advancing. On March 23, XPENG officially announced the establishment of a Robotaxi business unit, planning to launch three Robotaxi models in 2026. These will be equipped with four Turing chips, delivering 3,000 TOPS of onboard computing power, and will begin safety-operator-assisted passenger tests in the second half of the year.

However, uncertainties surrounding technology commercialization warrant attention.

In technology licensing, XPENG aims to replicate Huawei's 'external supply' model for intelligent driving. The key lies in maintaining technological leadership amid competition from giants. Huawei has already deployed its technology across brands like AITO, Avatr, and Arcfox; XPENG still needs to gain recognition from more clients beyond Volkswagen.

For humanoid robots, IRON is priced at RMB 200,000–300,000, targeting the high-end commercial market—significantly more expensive than competing products from Unitree at the same stage.

Unitree's prospectus shows that humanoid robots have relatively high gross margins, but their applications are primarily in research, with low penetration in consumer and industrial markets. This means IRON must deliver tangible, quantifiable scenario value to attract B-end customers, rather than just being 'usable.'

More importantly, if the rollout of L3/L4 autonomous driving policies falls short of expectations, it could delay the mass production and commercialization of C-end intelligent features and Robotaxi operations.

With simultaneous progress on the Turing chip, VLA model, humanoid robots, and Robotaxi, XPENG must make strategic choices in management and resource allocation.

In the capital markets, XPENG's valuation (based on PS multiples) is higher than other NEV makers, reflecting market recognition of its technical route and AI transformation. However, this also places pressure on the company: investors are willing to pay for the 'physical AI' prospect, but only if this technological edge can translate into sustainable profit growth.

-

![]()

The Unstoppable Rise of 'Optical Progress and Copper Decline': Sunny Optical’s Strategic Vision for the Next Decade

-

![]()

AI + Going Global in the Second Half: No Intermission for Robot Vacuum Cleaners

-

![]()

The Suffering Endured in E-commerce, Walmart Doesn't Want to Repeat in AI

-

![]()

What Does the Doubling of New Energy Vehicle Exports Mean?

-

![]()

Ghosn: 'Only I Can Save Nissan'

-

![]()

Volkswagen Lays Off 100,000 Employees, The Elephant Sits Down

-

![]()

Expanding Production Capacity! Yutong Optics Acquires Approximately 1.5 Hectares of Industrial Land in Chang'an, Dongguan

-

![]()

Why Is Nokia Making a Comeback in the AI Era?