Behind Horizon's Shift from Profit to Loss: R&D Investment Surges Past 5 Billion, Yu Kai Targets Over 60% Growth | Mirror Pro

03/24 2026

03/24 2026

683

683

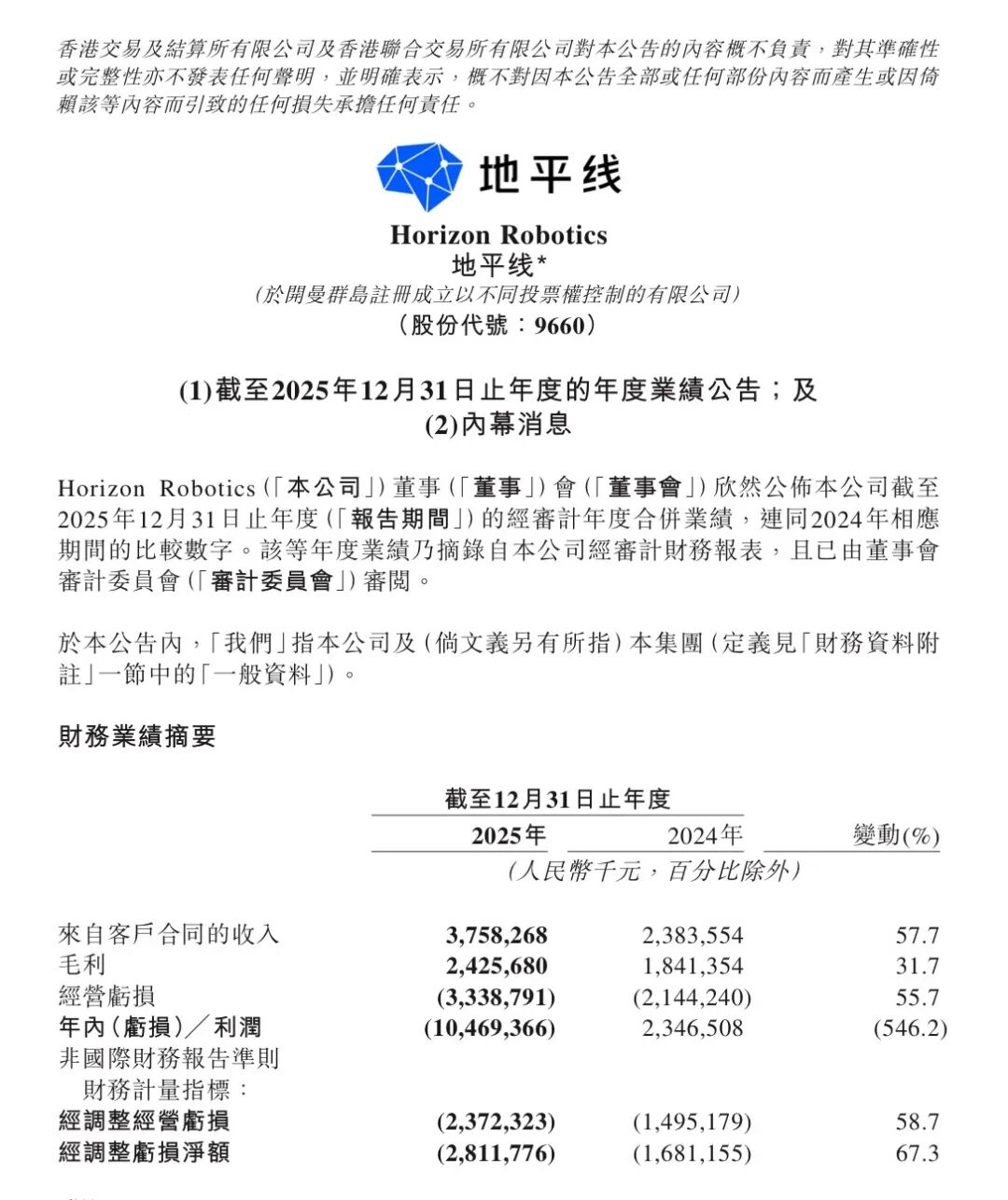

On March 19, Horizon Robotics, a core player in the intelligent driving chip sector, released its 2025 financial report, showcasing distinct characteristics of "high growth and high investment": annual revenue reached 3.758 billion yuan, a significant year-on-year increase of 57.7%, while R&D expenditure rose by 63.3% year-on-year to 5.1537 billion yuan.

The financial report shows that the automotive business remains Horizon's primary segment, accounting for 94.6%, with product solutions contributing 43.2% and licensing and services contributing 51.4%. The non-automotive business, which provides processing hardware and robot developer kits for numerous non-automotive clients and developers, accounts for only 5.4%. Over the past year, each segment has achieved varying degrees of structural breakthroughs, reflecting the critical transition of the intelligent driving industry from "basic popularization" to "high-tier upgrades."

As the core business, the automotive segment achieved revenue of 3.557 billion yuan in 2025, a year-on-year increase of 53.9%, with a gross margin maintained at a high level of 67.2%, demonstrating strong business resilience. Revenue from product solutions surged by 144.2% year-on-year to 1.622 billion yuan, with its contribution to total revenue jumping from 27.9% in 2024 to 43.2%, becoming the core engine driving growth. Behind this growth is the explosive shipment of mid-to-high-tier intelligent driving hardware. In 2025, total shipments of Horizon's Journey series processing hardware reached 4.01 million units, a year-on-year increase of 38.8%, with hardware supporting mid-to-high-tier intelligent driving functions shipping 4.8 times more than in 2024, directly boosting the average value per vehicle by over 75% and forming a virtuous cycle of "increasing volume and value."

The licensing and services business continued to act as a "ballast stone," achieving revenue of 1.935 billion yuan in 2025, a year-on-year increase of 17.4%, with a gross margin as high as 94.5%. The steady growth of this segment benefits from the high recognition of Horizon's algorithms and software stack in the industry, not only deepening cooperation with long-term partners such as CARIAD under the Volkswagen Group but also attracting one of Japan's largest automotive parts groups to become a top-five customer, validating the commercial value of its technological foundation.

Although the non-automotive solutions segment accounts for a relatively small proportion, its growth is rapid, with revenue reaching 201 million yuan in 2025, a year-on-year increase of 179.9%. The rapid growth of this segment opens up diversified growth opportunities for Horizon beyond the automotive sector, aligning with its long-term strategy of "empowering multiple industries with a foundational AI platform."

01 Technological Breakthroughs and Ecosystem Expansion Build Competitive Barriers

Horizon's business performance is highly aligned with the development pace of China's intelligent vehicle industry. In 2025, the penetration rate of intelligent driver-assistance systems in China's passenger vehicle market reached 67.6%, with the penetration rate of mid-to-high-tier intelligent driving (NOA) doubling from 21.6% in 2024 to 42.6%. The adoption rate of mid-to-high-tier intelligent driving in domestic brands reached as high as 61.8%, significantly outpacing the 13.1% of joint-venture brands. Horizon's 44.2% market share in the mainstream market below 200,000 yuan, 47.7% share in the basic ADAS market, and 14.4% share in the mid-to-high-tier intelligent driving market solidify its position in the industry's first tier, making it a core driver of the trend toward "democratizing high-tier intelligent driving."

Horizon's key breakthroughs in 2025 are concentrated in two dimensions: technological productization and ecosystem globalization, building deep barriers for it in the fierce market competition. The mass production of the full-scenario urban assistant driving solution HSD became the biggest highlight of the year. As China's first intelligent driving large model based on one-stage end-to-end technology, HSD officially entered mass production in November last year, first deployed in mainstream models priced around 150,000 yuan, with over 22,000 units delivered in just over a month after launch. More notably, although models equipped with HSD are priced higher, they account for 83% of total sales of related models, and during the Spring Festival this year, user intelligent driving mileage accounted for 41%, significantly outperforming the industry mainstream, proving that high-tier intelligent driving has shifted from a "gimmick" to a "key factor in Car purchase decision (vehicle purchase decisions)." As of the end of 2025, HSD has secured design wins from over 10 OEM brands for more than 20 models, demonstrating strong commercial conversion capabilities.

The globalization and diversification of ecosystem layout (layout) have also shown remarkable results. In the domestic market, Horizon has deep ties with domestic and joint-venture brands, securing design wins for over 110 new models; in overseas markets, it has won design wins for over 40 export models from 11 automakers, with cumulative lifecycle export design wins reaching 2 million units, while securing design wins for overseas models from three international automakers through international Tier 1 suppliers, with lifecycle shipments reaching 10 million units. In particular, the first model from Coolridge, a joint venture with the Volkswagen Group, has recently entered mass production, with six additional new models expected to launch in 2026, marking Horizon's cooperation with international automakers transitioning from the R&D stage to scaling (large-scale) delivery.

02 Strategic Choices Behind High Investments

The most notable aspect of the financial report is undoubtedly Horizon's shift from profitability to a significant loss over the past year. In 2025, Horizon reported an annual loss of 10.469 billion yuan, a sharp fluctuation from the profit of 2.347 billion yuan in 2024, with an adjusted net loss of 2.812 billion yuan, a year-on-year expansion of 67.3%. However, this change is not due to a deterioration in business fundamentals but rather the result of multiple overlapping factors.

The majority of the loss came from "fair value changes in preferred shares and other financial liabilities," which resulted in a book loss of 6.664 billion yuan, primarily due to the increase in the fair value measurement of related liabilities caused by the company's rising market value. This is a non-cash accounting treatment and does not directly reflect operating conditions. After excluding the impact of the aforementioned financial instruments and non-cash items such as share-based payments, Horizon's adjusted net loss was 2.812 billion yuan, mainly due to high R&D investments.

Continuous investment in technological R&D is the fundamental guarantee of competitiveness. In 2025, Horizon's R&D expenditure accounted for 137.1% of revenue, primarily used for the iteration of core products such as the HSD solution and Journey 6 series hardware, as well as technological investments in cloud services and tape-outs. Although high R&D investment has expanded losses in the short term, it has also laid a technological leadership foundation for Horizon. The launch of the new-generation computing architecture BPU "Riemann Architecture" and the planning of the Journey 7 processing hardware will further enhance computing power and support the onboard deployment of larger-scale AI models.

Horizon's founder and CEO, Yu Kai, also emphasized during the earnings call that he is not afraid of high R&D investments, believing that HSD is not only a core product for winning in urban intelligent driving but also a technological foundation for advancing toward L4-level autonomous driving and even the broader robotics industry. This strategy of converting current profits into future technological moats is not uncommon in the high-growth tech sector.

As a capital-intensive and technology-intensive industry, intelligent driving requires long-term R&D investments to breakthrough core technologies such as algorithms and chips, while technological commercialization requires deep collaboration with automakers, undergoing lengthy cycles of R&D, testing, and mass production. Horizon's choice to increase investments during the industry's outbreak period (boom phase) to capture market share and consolidate technological barriers is essentially a pursuit of long-term value rather than a compromise on short-term profitability.

Moreover, financial report data shows that Horizon's operating cash flow and cash reserves remain healthy. Cash and cash equivalents reached 20.2 billion yuan at the end of 2025, a year-on-year increase of 31.3%, providing sufficient ammunition for sustained R&D investments. Meanwhile, the company's asset-liability ratio was 58.7%, within a reasonable range, with no pledged assets or significant contingent liabilities, indicating an overall robust (stable) financial structure.

03 Future Outlook: Technological Iteration and Scenario Expansion Open Growth Ceilings

Horizon has clearly outlined its development direction for 2026 and beyond in the financial report. At the product level, it will launch a new-generation cockpit-driving fusion full-vehicle intelligent agent chip (Agentic CAR SoC) and operating system (Agentic CAR OS), reducing system costs while enhancing user experience through software-hardware collaborative optimization (collaborative optimization), expected to become standard in next-generation intelligent vehicles. Meanwhile, the urban NOA solution based on the single Journey 6M hardware has entered mass production, bringing high-tier intelligent driving to the 100,000-yuan-level market and further driving technological popularization.

In terms of technological deployment, Horizon plans to launch Robotaxi trial operations in designated domestic cities in the third quarter of this year, accumulating real-world road data for L4-level autonomous driving to lay the foundation for technological iteration and commercial deployment. This move marks its advancement from an "intelligent driving solution provider" to an "L4-level technology mass production enabler," potentially seizing the initiative in the future driverless mobility market.

In terms of ecosystem cooperation, in addition to deepening collaboration with existing automakers, Horizon will continue to advance its global layout , especially capitalizing on the wave of overseas brand intelligence transformation to compete for market share with its technological cost-effectiveness advantages. The adjustment of transitioning D-Robotics (Digua Robotics) from a subsidiary to an associate company not only helps focus resources on the core automotive business but also allows it to continue sharing in the growth dividends of the robotics industry through ecological cooperation, optimizing overall financial performance.

Regarding this year's performance, Yu Kai predicts steeper growth in automotive revenue, with confidence in further accelerating to around 60% growth in 2026, far exceeding the 54% in 2025. From an industry trend perspective, the intelligent driving industry is transitioning from "feature competition" to "experience competition," with users' demand for full-scenario intelligent driving in urban and highway settings becoming increasingly strong. Chip computing power, algorithm precision, and data accumulation have become core competitive elements. Leveraging its technological accumulation in automotive-grade chips, a vast network of ecological partners, and market validation of products like HSD, Horizon is well-positioned to further consolidate its advantages amid the increasing industry concentration.

However, it also faces fierce competition from domestic and foreign tech companies and traditional chip giants, as well as challenges such as high raw material costs and accelerated technological iteration. For Horizon, 2026 will be a critical "landing year": the launch of cockpit-driving fusion products, Robotaxi trial operations, and mass production of more cooperative models will directly determine the pace of its market share and profitability improvements.

-

![]()

The Unstoppable Rise of 'Optical Progress and Copper Decline': Sunny Optical’s Strategic Vision for the Next Decade

-

![]()

AI + Going Global in the Second Half: No Intermission for Robot Vacuum Cleaners

-

![]()

The Suffering Endured in E-commerce, Walmart Doesn't Want to Repeat in AI

-

![]()

What Does the Doubling of New Energy Vehicle Exports Mean?

-

![]()

Ghosn: 'Only I Can Save Nissan'

-

![]()

Volkswagen Lays Off 100,000 Employees, The Elephant Sits Down

-

![]()

Expanding Production Capacity! Yutong Optics Acquires Approximately 1.5 Hectares of Industrial Land in Chang'an, Dongguan

-

![]()

Why Is Nokia Making a Comeback in the AI Era?