Xiaopeng Motors Reaches a Turning Point Through Technology Export

03/25 2026

03/25 2026

604

604

By Yang Xuejian

Source / Node AI

"Xiaopeng Motors is at a historic turning point in the application of physical AI," said He Xiaopeng, Chairman and CEO of Xiaopeng Motors. On the evening of March 20, 2026, Xiaopeng Motors (09868.HK/XPEV.US) officially released its full-year 2025 financial data, marking this report as a crucial answer to its transformation milestone.

Multiple Indicators Grow, but Net Profit Remains in the Red for the Full Year

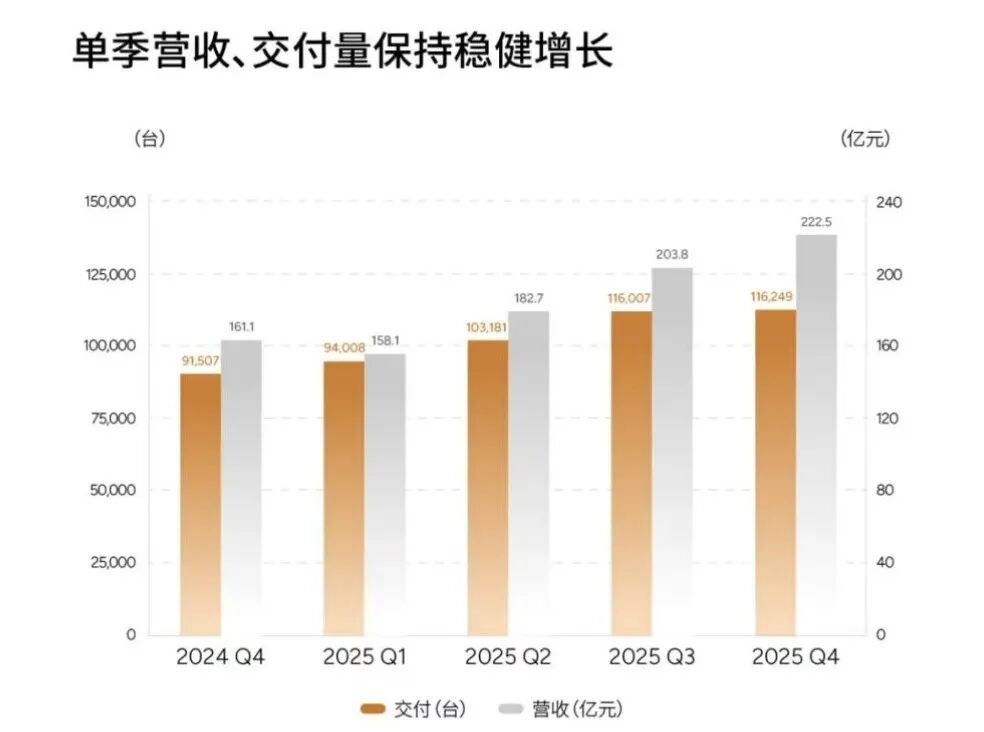

Data shows that Xiaopeng Motors delivered a total of 429,445 vehicles in 2025, up 125.9% year-on-year. Full-year revenue reached RMB 76.72 billion, an 87.7% increase year-on-year (2024 revenue: RMB 40.87 billion). The company's gross profit margin for 2025 was 18.9%, up 4.6 percentage points year-on-year, reaching a record high.

However, despite achieving a net profit of RMB 380 million in the fourth quarter of 2025 for single-quarter profitability, Xiaopeng Motors still posted a full-year loss of RMB 1.14 billion.

In terms of R&D expenses, Xiaopeng Motors spent RMB 9.49 billion in 2025, a 47.0% increase year-on-year (2024: RMB 6.457 billion). He Xiaopeng further pointed out during the conference call that nearly half of Xiaopeng's 2025 R&D investment was allocated to AI-related initiatives.

Additionally, Xiaopeng's marketing expenses reached RMB 9.40 billion in 2025, a 36.8% increase year-on-year from RMB 6.871 billion in 2024.

Data shows that as of December 31, 2025, Xiaopeng Motors had a total of 721 stores covering 255 cities. Its self-operated charging station network expanded to 3,159 stations, including 2,108 Xiaopeng super-fast charging stations.

Looking ahead, He Xiaopeng pointed out that overseas markets will be a major growth driver. "Based on the enhanced capabilities of our overseas product technology and supply chain services, Xiaopeng Motors' international expansion will significantly accelerate in 2027-2028, with overseas revenue becoming one of the core drivers of the company's profitability," He said.

He also stated that Xiaopeng Motors aims to double its overseas sales volume year-on-year by 2026, with overseas revenue accounting for over 20% of total revenue. To achieve this, Xiaopeng is considering charging opportunities for its intelligent driving software overseas to drive technological commercialization.

Single-Quarter Profitability Driven by 'Selling Code and Technology'

Undoubtedly, the single-quarter profitability in Q4 was the biggest highlight of Xiaopeng Motors' financial report.

"In Q4, Xiaopeng Motors achieved quarterly profitability for the first time, with a net profit exceeding RMB 380 million. We believe that by leveraging technology leadership to drive new business models, Xiaopeng Motors will achieve a profit path completely different from traditional automakers in the future," He Xiaopeng stated directly during the conference call.

What He Xiaopeng referred to as "leveraging technology leadership to drive new business models" can be seen as the core of Xiaopeng Motors' future sustainable profitability.

In the view of Node Finance, unlike the single-car-selling model of traditional automakers, Xiaopeng's new business model can be understood as exporting mature self-developed technologies externally, engaging in technology cooperation (such as its collaboration model with Volkswagen Group), or simply selling technological solutions.

Judging from Q4's performance, Xiaopeng Motors has already begun to taste the sweetness of high-profit returns from technology exports through its collaboration with Volkswagen.

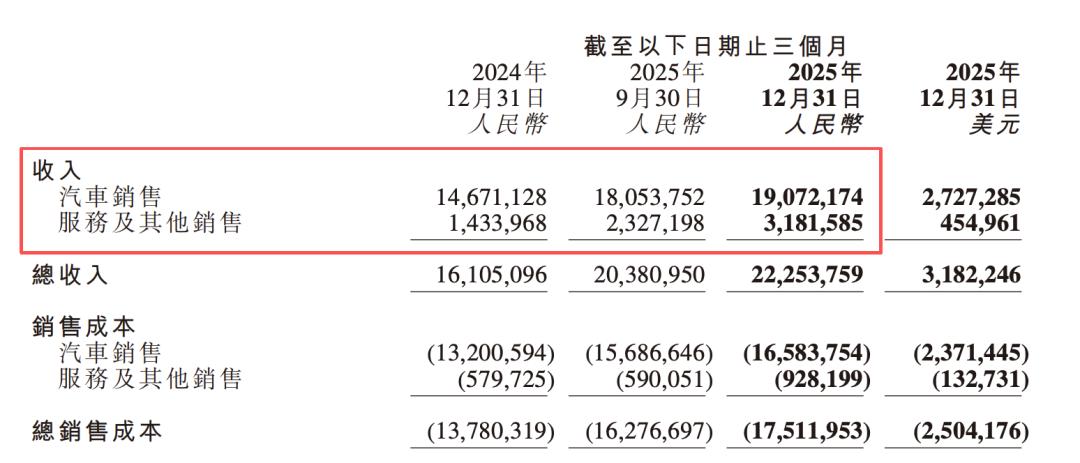

Breaking down the data, Xiaopeng Motors' total revenue in Q4 2025 was RMB 22.25 billion, a 38.2% increase year-on-year. Among this, automotive sales revenue was RMB 19.07 billion, up 30% year-on-year, remaining the foundation. However, service and other revenue surged to RMB 3.18 billion, a 121.9% increase year-on-year and a 36.7% increase quarter-on-quarter, far outpacing vehicle sales growth.

Comparing this to Xiaopeng's full-year 2025 data, automotive sales revenue was RMB 68.38 billion (up 90.8% year-on-year), while service and other revenue increased by RMB 8.34 billion (up 65.6% year-on-year). This highlights the importance of service and other revenue in Q4.

Xiaopeng Motors also explicitly stated that the growth in service and other business revenue in Q4 was primarily due to increased revenue from providing technology R&D services to other automakers and growth in sales of spare parts and carbon credit business revenue.

Among these, providing technology R&D services to other automakers clearly refers to the collaboration with Volkswagen. In other words, Xiaopeng's ability to turn a profit in Q4 2025 was driven by high-margin technology revenue from its collaboration with Volkswagen.

Specifically, Xiaopeng and Volkswagen achieved two major technological delivery milestones in Q4: the completion of key development and mass production-level delivery of the Electronic Electrical Architecture (CEA); and the official technical authorization and implementation of the high-level intelligent driving system (XNGP). Additionally, Volkswagen has become the first external customer for Xiaopeng's Turing chip and second-generation VLA large model.

Not limited to Volkswagen, Xiaopeng will open its Turing chip and intelligent overall solutions to more automakers, embodied intelligence enterprises, and Tier 1 suppliers in the future.

On one hand, collaboration with Volkswagen continues to expand; on the other hand, signals of cooperation with other automakers are being released. It is not hard to understand that what He Xiaopeng refers to as "a profit path completely different from traditional automakers" may not be limited to competing on new car sales volume but rather on "selling code and technology."

What Other Challenges Remain?

Relying on technology authorization with Volkswagen to achieve single-quarter profitability has opened up new growth potential for Xiaopeng, but the future remains uncertain. With intensifying competition in the automotive market, every contender in the knockout stage is, as He Xiaopeng once said, "climbing out of a pile of 'casualties'."

After delivering a confidence-boosting full-year and quarterly financial report, the challenges Xiaopeng Motors currently faces are laid bare.

First, sales volume structure relies on low-priced, high-volume models.

Breaking down Xiaopeng's 2025 sales structure, the MONA M03, priced at RMB 119,800, sold 175,300 units throughout the year, accounting for over 40% of total sales and becoming the sales pillar. In contrast, high-end models like the G9 and X9, priced around RMB 300,000, sold approximately 40,000 units cumulatively throughout the year, accounting for less than 10%. The two new 200,000-RMB-level models launched in the second half of 2025 on a new platform, the Xiaopeng G7 and the all-new Xiaopeng P7, also saw sales performance start high but end low. Taking the all-new Xiaopeng P7 as an example, it was launched in August 2025, with sales exceeding 8,000 units in September but dropping to just 2,300 units in December (data from the China Passenger Car Association).

The issues arising from reliance on low-priced, high-volume models are evident. On one hand, low-priced models have low gross margins and contribute little to improving profitability in the vehicle business. On the other hand, and more importantly, the entry-level model market is fiercely competitive, with BYD's lineup ahead and "new force leader" Leapmotor and others vying in the RMB 100,000 price range. Xiaopeng Motors' MONA M03, fighting alone, could significantly impact Xiaopeng's overall sales if its sales weaken.

Second, the performance of the Z08 determines how far "the great roc (Xiaopeng)" can go.

Technology collaboration with Volkswagen was a key factor in Xiaopeng's Q4 profitability. The first model jointly developed by both parties, the mid-to-large-sized all-electric SUV Z08, rolled off the production line on March 13 of this year. Unlike the typical 36-to-48-month development cycle for joint-venture brand models, the Z08 took only 24 months.

During the development of the Z08, Volkswagen led product design definition, technical verification and approval, quality standards, and driving control tuning, while Xiaopeng provided technical support such as the VLA all-scenario intelligent driving assistance system.

The price range and detailed specifications of the Z08 have not yet been disclosed, but outside predictions suggest it may be priced around RMB 250,000.

The Z08 competes in the highly competitive large five-seater new energy SUV segment, which includes the Tesla Model Y, Xiaomi YU7, Li Auto i6/L6, and NIO ES6, among others.

For the Z08 to compete with Tesla and domestic brands, its pricing strategy will determine how far it can go in the market. Its performance not only affects Volkswagen's new energy prospects in China but also Xiaopeng Motors' confidence in its role as a technology supplier and its bargaining power in future collaborations.

Furthermore, it should be noted that Volkswagen Group's collaborations in intelligent driving and intelligent cockpit technologies in China have always been multi-pronged and not solely focused on Xiaopeng Motors. For example, in the high-level intelligent driving sector, it partnered with Horizon Robotics to establish a joint venture, while for intelligent cockpits, it has deep cooperation with Thundersoft. Some Audi models even use Huawei's ADS intelligent driving solution.

Finally, competition in the "technology export" track (competitive arena) is equally fierce.

Xiaopeng Motors attempts to break free from the single revenue and profit model of "selling cars and hardware" by "selling code and technology," but it faces strong competitors in the intelligent driving field it excels in.

Currently, Huawei and Horizon Robotics dominate the first tier of domestic intelligent driving and brand market share. Huawei leads in reputation for its full-stack self-developed + extreme hardware redundancy approach, with its ADS system praised for safety, stability, and multi-scenario adaptability, securing fixed point contracts for high-end models under the Harmony Intelligent Mobility Alliance. Horizon Robotics, meanwhile, rapidly expands through its software-hardware integrated layout, securing over 20 model fixed point (design win) contracts for its Horizon Smart Drive (HSD) by the end of 2025.

In comparison, any automaker focusing on full-stack self-development, including Xiaopeng Motors, currently cannot match Huawei or Horizon Robotics in terms of hardware redundancy and large-scale mass production capabilities. If Xiaopeng hopes to expand its client base beyond Volkswagen, it faces entirely new challenges in terms of software and hardware capabilities.

More importantly, Xiaopeng must compete with other intelligent driving suppliers on technological leadership, requiring sustained high R&D investment, faster iteration of its intelligent driving system, and optimization of the Turing chip's computing power. Any slowdown in pace could allow competitors to overtake it within just a few months.

Therefore, in the view of Node Finance, Xiaopeng Motors currently especially needs to do the following three things:

First, increase sales volume and profitability of its high-end products. Strengthening one's own capabilities remains crucial. Despite the significant growth brought by technology exports, the foundation still lies in vehicle sales.

We believe that Xiaopeng Motors must remain committed to its high-end strategy, focusing resources on creating another blockbuster model beyond the MONA M03 and improving its gross margin structure by providing intelligent driving service experiences through its self-developed intelligent driving capabilities.

Second, expand to second-tier automakers and create cost-effective technology solutions. While leveraging the buzz generated by the Z08's launch and sales, Xiaopeng should accelerate the export of more cost-effective mature intelligent driving solutions to second-tier automakers, reducing reliance on a single client and finding a reasonable breakthrough strategy given that first-tier brands are largely occupied by Huawei and Horizon Robotics.

Third, enhance resilience against overseas uncertainties. As mentioned at the beginning of this article, Xiaopeng Motors has set higher targets for overseas sales volume and revenue in 2026, such as doubling sales volume and increasing revenue contribution to 20%. However, with rapidly changing international situations, not only Xiaopeng but all Chinese automakers seeking overseas expansion face significant uncertainties.

Overall, increasing sales volume and profitability of Xiaopeng's own high-end models remains the key factor in ensuring its long-term stable development.

-

![]()

The Unstoppable Rise of 'Optical Progress and Copper Decline': Sunny Optical’s Strategic Vision for the Next Decade

-

![]()

AI + Going Global in the Second Half: No Intermission for Robot Vacuum Cleaners

-

![]()

The Suffering Endured in E-commerce, Walmart Doesn't Want to Repeat in AI

-

![]()

What Does the Doubling of New Energy Vehicle Exports Mean?

-

![]()

Ghosn: 'Only I Can Save Nissan'

-

![]()

Volkswagen Lays Off 100,000 Employees, The Elephant Sits Down

-

![]()

Expanding Production Capacity! Yutong Optics Acquires Approximately 1.5 Hectares of Industrial Land in Chang'an, Dongguan

-

![]()

Why Is Nokia Making a Comeback in the AI Era?