High Oil Prices Constrain Gasoline Vehicle Market, Electric Vehicles Reap the Benefits

04/10 2026

04/10 2026

422

422

Lead | Introduction

Since the beginning of this year, the swift escalation of international oil prices and periodic shortages of refined oil products have not only kept the market on edge but have also quietly transformed cost structures across various industries, shaping their developmental paths. From the transportation sector to the automotive industry and extending into the broader macroeconomic landscape, the ripple effects of oil price fluctuations are spreading rapidly.

Produced by | Heyan Yueche Studio

Written by | Zhang Dachuan

Edited by | Hezi

Full text: 3,116 characters

Reading time: 5 minutes

Over the past month, the global rise in oil prices and periodic shortages of refined oil products have captured widespread attention. The surge in oil prices has led consumers to shift their preferences, accelerating the transition of domestic automotive consumption towards new energy vehicles. According to data from the China Passenger Car Association, retail sales of domestically produced narrowly defined passenger cars reached approximately 1.7 million units in March, with new energy vehicle (NEV) retail sales hitting 900,000 units, marking the first time the penetration rate exceeded 52.9%.

△This round of oil price hikes is transforming from localized cost disruptions into systemic impacts on the automotive industry.

Gasoline Vehicles Struggle as Electric Vehicles Thrive

The sustained rise in oil prices is essentially reshaping the profit landscape of the automotive industry—gasoline vehicle users are passively shouldering increased costs, while new energy vehicles are accelerating their market gains.

The most immediate impact is felt at the consumer level. Rising oil prices have significantly increased the cost of using gasoline vehicles, making the scenario of “affordable to buy but unaffordable to use” increasingly common. For an average family car with a fuel consumption of 8 liters per 100 kilometers and an annual mileage of 20,000 kilometers, the annual fuel costs will rise by approximately 2,400 to 2,560 yuan. Ride-hailing drivers will see their monthly fuel costs increase by 500 to 1,000 yuan. This persistent, essential expenditure pressure will continuously erode consumer tolerance for gasoline vehicles.

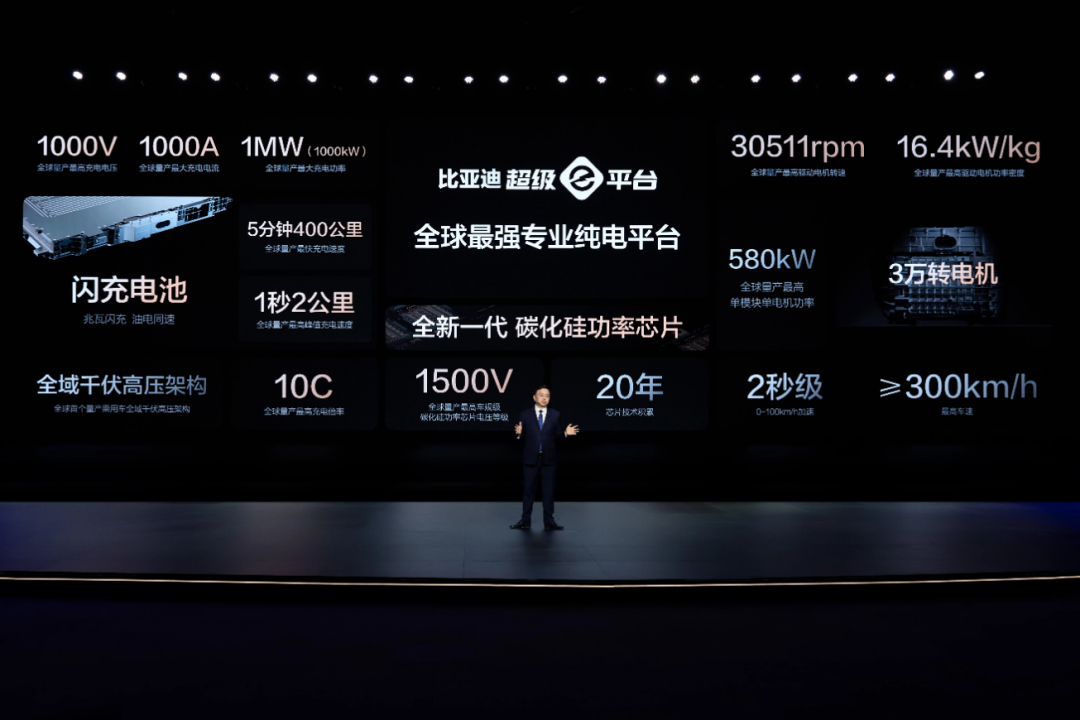

From the perspective of automaker sales performance, most domestic new energy vehicle (NEV)-focused companies have achieved year-on-year and month-on-month growth, with few exceptions. Notably, BYD, leveraging its comprehensive strength in the new energy sector, surpassed Geely Auto to top domestic sales charts for the first time in March this year. This shift reflects not only BYD's dual breakthroughs in pure electric and hybrid technology routes but also the market contraction of Geely's gasoline vehicle segment due to oil price fluctuations. The trend of consumers migrating towards new energy models under high oil price conditions has significantly suppressed traditional gasoline vehicle sales, indirectly boosting the market expansion of new energy leaders. Even in the United States, there are calls to ease tariff restrictions on cost-effective Chinese electric vehicles—not due to policy shifts but as a spontaneous market choice under high oil price pressure.

In reality, the deeper impacts of rising oil prices are unfolding at the industrial level. Rising oil prices are not merely a fuel pricing issue but a classic cost shock: logistics costs surge, supply chain operational expenses rise, and crucially, core materials like plastics and synthetic rubber, which are inherently tied to the oil-pricing system, become more expensive. In other words, oil price hikes will ripple outward, transmitting layer by layer from the energy sector to the vehicle manufacturing end, comprehensively raising the cost base of the automotive industry. If prolonged blockades of the Strait of Hormuz disrupt shipping, the global automotive supply chain could even face periodic “disruptions.”

△Prolonged blockades of the Strait of Hormuz could disrupt shipping, potentially causing periodic “disruptions” in the global automotive supply chain.

Window of Opportunity for Chinese Electric Vehicles in the Era of High Oil Prices

Currently, the trajectory of the U.S.-Israel-Iran conflict remains uncertain, and structural instability in the Middle East may persist long-term. Scenarios where Iran repeatedly threatens to block the Strait of Hormuz could recur, continuously disrupting global oil supply and normalizing high oil prices.

For Chinese automakers, which already hold a first-mover advantage in the new energy vehicle sector, this presents an extremely rare strategic window of opportunity. Extending the perspective reveals a familiar scenario. During the two oil crises of the 1970s, U.S. automakers, long reliant on large-displacement models, suffered severe setbacks, while fuel-efficient Japanese automakers rose to prominence, breaking into European and U.S. markets. Subsequently, Japanese vehicles established significant advantages in both fuel economy and quality control systems, exemplified by Toyota's lean manufacturing, gradually solidifying their global position. To this day, General Motors, Ford, and Stellantis have yet to fully surpass Japanese brands in fuel efficiency and reliability.

△Japanese automakers leveraged the two oil crises to rapidly grow into global players and maintain their position to this day.

Today, a similar industrial script is unfolding. The difference is that this time, Chinese automakers hold the “technological dividends.” New energy vehicles and intelligence form two critical assets: on one hand, rising oil prices are rapidly widening the usage cost gap between gasoline and electric vehicles, compelling both ordinary consumers and B-end operators to reevaluate their purchasing decisions; on the other hand, China has established global leadership in vehicle electrification engineering capabilities and the power battery sector. Battery enterprises like CATL and BYD not only face overwhelming global demand but have also become key suppliers for international automakers such as Tesla.

More critically, once overseas users switch to Chinese new energy vehicles due to rigid factors like “usage costs,” they will encounter not only lower energy consumption costs but also leapfrogged experiences in intelligent cockpits and autonomous driving. This shift from “passive choice” to “active endorsement” is the true determinant of long-term brand competitiveness. As reputation accumulates globally, Chinese automakers like BYD, Geely, and Chery have a genuine opportunity to replicate the rise of Toyota, Honda, and Nissan, even establishing deeper competitive moats in the electrification era.

△Rising oil prices may usher in new development opportunities for Chinese electric vehicles.

Profit Margins Bottom Out, Accelerating the Automotive Industry’s “Elimination Race”

A new round of deep reshuffling in the domestic automotive industry is almost inevitable. Intense competition in recent years has left most automakers battered, with continuously weakening profitability. Data shows that the profit margin of the domestic automotive industry was merely 4.1% in 2025, and by January-February 2026, it further declined to 2.9%, nearing the “survival line” of the manufacturing sector. Against this backdrop, oil price fluctuations are not just external shocks but act as a “fuse,” accelerating industry consolidation, with some automakers exiting the stage—a matter of time.

From the demand side, the downward trend in the gasoline vehicle market is irreversible. Even if oil prices retreat temporarily, consumers will incorporate oil price volatility into long-term cost considerations during purchasing decisions, and this “reshaped expectation” will continuously suppress demand for gasoline vehicles. For traditional automakers reliant on gasoline vehicle businesses for financial support, particularly joint ventures, this is a fatal blow. Over the past few years, while these automakers have launched new energy models, they remain stuck at the “single-point breakthrough” stage, failing to achieve scale effects or build systemic competitiveness. Once gasoline vehicle sales decline persistently, their cash flow foundations—critical for survival—will be rapidly eroded.

△Traditional joint-venture automakers heavily reliant on gasoline vehicle businesses face immense challenges.

Is transformation still possible? The reality is not optimistic. The barriers to competition in the new energy vehicle sector have been significantly raised in a short time: pure electric range for hybrid models now generally exceeds 200 kilometers, urban NOA (Navigation on Autopilot) is becoming standard, and ultra-fast charging technology imposes higher requirements on batteries, electric drives, and electronic control systems (the “three electric” systems). Building these capabilities entails not only massive R&D investment but also relies on long-term technological accumulation and systemic capabilities. For automakers with tight finances and insufficient technological reserves, there is virtually no time window to “catch up.”

△A full transition to new energy vehicle businesses poses increasing challenges for joint-venture automakers.

From the supply side, pressures are also intensifying. Rising oil prices have driven up raw material prices across the upstream sector, further eroding already thin profit margins. Given severe overcapacity in the domestic automotive market, vehicle manufacturers lack the capacity to significantly pass on costs to end consumers. Any price hikes would rapidly trigger demand loss. More critically, leading enterprises like BYD, Geely, and Chery, armed with scale advantages and cost control capabilities, possess stronger “pressure thresholds.” In this landscape, the first to succumb to cost pressures and raise prices may be the first to be eliminated by the market.

This means competition is shifting from “growth-focused” to “survival-focused.” In the coming period, the Chinese automotive market will no longer be a simple battle for market share but a brutal endurance race: competing on cash flow, technological systems, and cost control capabilities. The survivors will not be those shouting the loudest about transformation but those truly completing systemic restructuring and establishing scale advantages in the new energy and intelligence sectors. The rest will gradually exit in this accelerating elimination race.

Commentary

The shock triggered by oil prices appears superficial as a cost issue but is, in essence, a reallocation of industrial power: the advantages of the gasoline vehicle era are being rapidly eroded, while a new wave of electrification offensives may arrive sooner than expected. High oil prices are not merely a cyclical disruption but act as a continuously pressed “accelerator”—compressing the last space of the gasoline vehicle era while amplifying the global substitution process of new energy vehicles. This time, China’s automotive industry likely stands at the forefront of the wave. Meanwhile, a deeper but equally critical shift is underway: industry consolidation and integration, once hoped to be achieved through market mechanisms, may now be significantly accelerated by this round of external shocks. In other words, this is not just an industrial upheaval triggered by energy prices but a potential catalyst driving structural restructuring in China’s automotive industry.

(This article is original to Heyan Yueche and may not be reproduced without authorization.)

-

![]()

Domestic Pioneer: Changjin Photonics, First Listed Company Focused on Special Optical Fibers, Soars Over 15-Fold on STAR Market Debut

-

![]()

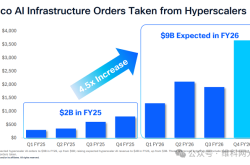

Single-Quarter Orders Break $1 Billion Barrier! Cisco’s Acacia Surfs the AI Boom

-

![]()

Consistently Propelling Technological Progress: Qualcomm’s Xu Hao Elucidates How 6G Trial Frequencies Can Optimize the Balance Between Coverage and Bandwidth

-

![]()

Liushenyu Mine Disaster Drives Industrial Innovation: Pioneering a New Era of Intelligent Mine Safety with Integrated Air-Ground Systems

-

![]()

Ant Group CEO Han Xinyi's Latest Speech: The Emergence of 'Trust Logic' in the AI Era

-

![]()

Demystifying the Rankings: Do High Scores in Robotics Competitions Equate to Real-world Implementation Strength?

-

![]()

Europe's Q1 Smartphone Market Shipments Revealed: Samsung Holds Firm at First Place, Honor Surges Over 60%

-

![]()

Mixed Fortunes: The Ongoing Transformation of the Automotive Industry's Value Landscape