Leapmotor's Stock Price Tumbles 10% as Chairman Warns of 'Survival Mode': Last Year's Profit Per Vehicle Was a Mere 1,810 Yuan...

04/21 2026

04/21 2026

400

400

Source: Shenlan Finance

Since the dawn of 2026, the automotive sector has witnessed an unprecedented surge in competition, surpassing even the intensity of the previous year.

How fierce is the competition? Media reports reveal that on April 16 alone, the automotive landscape was shaken by the launch or pre-sale announcement of six new models, including the Leapmotor D19, IM LS8, Volkswagen Anhui Genesys 08, Geely Galaxy Star Glory 7, and Aion N60.

In China's burgeoning new energy vehicle (NEV) market, no automaker dares to lag. Those who do risk immediate obsolescence. Leapmotor's Chairman, Zhu Jiangming, recently sparked debate by asserting, 'The industry's shakeout is far from over.' He stressed that survival hinges on avoiding losses and achieving scale.

For Leapmotor, which just unveiled the large SUV D19 and reported robust Q1 sales, why did its H-share price plummet 10% on April 20?

What is fueling market concerns?

1

Sacrificing Margins for Survival

Data indicates that in March of this year, retail sales of passenger vehicles in China reached 1.648 million units, a 15.0% year-on-year decline. Year-to-date retail sales stood at 4.226 million units, down 17.4%.

In a contracting market, profitability often takes a backseat to survival.

On April 16, Zhu Jiangming, Leapmotor's founder, chairman, and CEO, told the media, 'The industry's shakeout is far from over. We anticipate fierce competition to persist for the next two to three years.'

Hence, Leapmotor's foremost priority is to 'scale up, surpassing profitability goals.'

This strategy is evident in the pricing of Leapmotor's new flagship SUV, the D19, which once again adopted a 'price-cutting' approach.

On April 16, Leapmotor unveiled the D19, the culmination of a decade of innovation. Boasting a length of 5,252mm, it comes equipped with CATL batteries, an 800V high-voltage platform, and a pure electric range of at least 400km for the extended-range version. Air suspension is standard across all trims, and it's endorsed by celebrity Fei Xiang, all at an astonishingly low price.

Prior to the price reveal, the market had anticipated a range of 250,000-300,000 yuan. However, the starting price was announced at just 219,800 yuan, far below expectations.

Many netizens expressed concern that Leapmotor is 'selling at a loss to grab attention.' However, the company maintains that the vehicle remains profitable.

The capital market remained unimpressed, with some investors viewing this as a sign of escalating competition and downgrading Leapmotor's profitability forecasts for the year. Consequently, on April 20, Leapmotor's stock price plummeted 10%. However, other investors confidently bought in, causing the stock to rebound amid sharp divergence between bulls and bears.

Zhu Jiangming has even acknowledged on multiple occasions that many do not favor Leapmotor.

(Source: Screenshot from Leapmotor's Zhu Jiangming video)

2

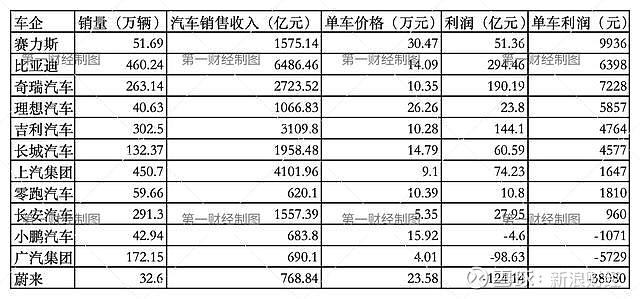

Sold 590,000 Vehicles Last Year, With an Average Profit of Just 1,810 Yuan Per Vehicle

How does Leapmotor manage to stay profitable despite its low vehicle prices?

The answer lies in its 2025 financial results: In 2025, Leapmotor's revenue soared to 64.73 billion yuan, up 101.3% year-on-year. Deliveries totaled 596,555 units, a 103.1% increase. Net profit stood at 540 million yuan, with adjusted net profit reaching 1.08 billion yuan, marking a turnaround from losses to profits.

Leapmotor's core profitability strategy revolves around in-house R&D of all critical components, avoiding external procurement. Its battery electric system, intelligent cockpit, seats, and key ADAS technologies are all developed and produced in-house. This minimizes the impact of upstream component price fluctuations on overall vehicle costs, granting Leapmotor far superior cost control compared to its peers.

Behind this lies a straightforward principle—higher scale leads to lower unit costs.

In 2025, for instance, Leapmotor's gross margin improved by 6.1 percentage points year-on-year to 14.5%. With both scale and margins on the rise, profitability followed suit. Based on an adjusted net profit of 1.08 billion yuan and deliveries of 596,000 units in 2025 (ranking first among new NEV brands), Leapmotor's net profit per vehicle last year was just around 1,810 yuan—equivalent to the profit from selling a single smartphone.

According to data from Yicai, Leapmotor's per-vehicle profit ranks in the lower-middle tier of the industry. While it lags behind BYD, Chery, and Li Auto in profitability, it outperforms traditional automakers like SAIC and Changan, as well as loss-making new NEV brands like XPeng and NIO.

Leapmotor has also excelled in exports. Leveraging its partnership with Stellantis, its joint venture, Leapmotor International, achieved annual profitability in its second year. In 2025, total exports reached 67,052 units, surpassing the annual sales of many new NEV brands.

Export growth remains robust this year, with 24,300 units exported in January-February alone. Western Securities projects total exports could reach 150,000-200,000 units this year, with export margins significantly higher than domestic markets.

Additionally, Leapmotor has repeatedly reiterated its 2026 target of 1 million units, roughly 400,000 more than last year. Achieving this will be no easy feat, especially amid a general decline in the domestic market in Q1.

However, Leapmotor's extreme 'cost-effectiveness' has also branded it as a 'low-end' player.

3

Capital Market Divided

Frankly, automaking is not a highly profitable industry. Last year, CATL's profits surpassed the combined profits of over a dozen A-share automakers.

As of April 20, the combined market cap of 23 A-share automakers (including BYD, SAIC, Seres, GAC, Great Wall, Changan, and JMC) stood at just 2.08 trillion yuan, while CATL alone boasted a market cap of 1.97 trillion yuan, nearing 2 trillion.

Automakers face pressure from both powerful upstream suppliers and intense downstream price competition, making it difficult to improve valuations.

For Leapmotor, many were initially skeptical, believing its 'low-price strategy' was unsustainable. When the D19 was priced low again, some investors felt Leapmotor was 'too honest' and 'disappointing,' even suspecting it was 'selling at a loss.' Their logic was that Leapmotor should pursue a 'brand-up' strategy. However, Zhu Jiangming views the current market as 'increasingly competitive with limited capacity,' making survival the top priority.

This divergence is also reflected at the institutional level.

On April 16, JPMorgan raised its 2026/27 profit forecasts for Leapmotor by 10%-17% and its target price to HK$90, seeing 65% upside potential after the stock surged ~27% in the past month. JPMorgan's rationale is that Leapmotor is expected to see Q2-Q4 deliveries surge 90%-100% MoM due to rising international oil prices, maintaining an 'Overweight' rating.

However, on March 18, Haitong International updated its research report, projecting Leapmotor's 2026 revenue to exceed 100 billion yuan with EBIT reaching 3.88 billion yuan. Yet, it lowered Leapmotor's 2026 target price from HK$73.51 to HK$61.44, primarily due to a reduction in the price-to-sales (PS) ratio from 1x to 0.75x.

Faced with a challenging automotive market this year, whether Leapmotor can sustain its 'dark horse' momentum and forge a new path as a 'budget' new NEV brand remains to be seen.

Shenlan Finance New Media Cluster, originating from the Shenlan Finance Journalist Community, has a 15-year history as a leading domestic finance new media outlet. Its accounts focus on China's most valuable companies, cutting-edge industries, and emerging regional economies, providing valuable content for investors, corporate executives, and the middle class. Welcome to follow.

-

![]()

Jitian Xingzhou: A Pioneer in Optical Payloads Secures Hundreds of Millions in Series B Funding!

-

![]()

Orders Secured Through to the Second Half of the Year! The Rationale Behind the 'Surge' in Demand for This Company’s Optical-Grade Base Films

-

![]()

Beyond Patents: The Retail Rivalry of Insta360 and DJI Unfolds

-

![]()

180 Billion Market Cap Vanished! How Did Seres Fall So Far?

-

![]()

Blockbuster! Domestic storage takes the global double crown for the first time, from an AI company

-

![]()

China Spearheads Formulation! World's Pioneering Global Technical Regulation for Automated Driving Systems Greenlit and Unveiled

-

![]()

Farewell to Pulsed Support Policies: Three Major Auto Policy Directions from Multiple Departments Take Effect on the Same Day

-

![]()

Embercore AI’s Accelerated Funding: The Robot Industry’s Shift Toward ‘Learning Systems’