From 'Skill Showcases' to Number Crunching: The Beijing Auto Show's Shift to Cost, Efficiency, and Integration

04/27 2026

04/27 2026

428

428

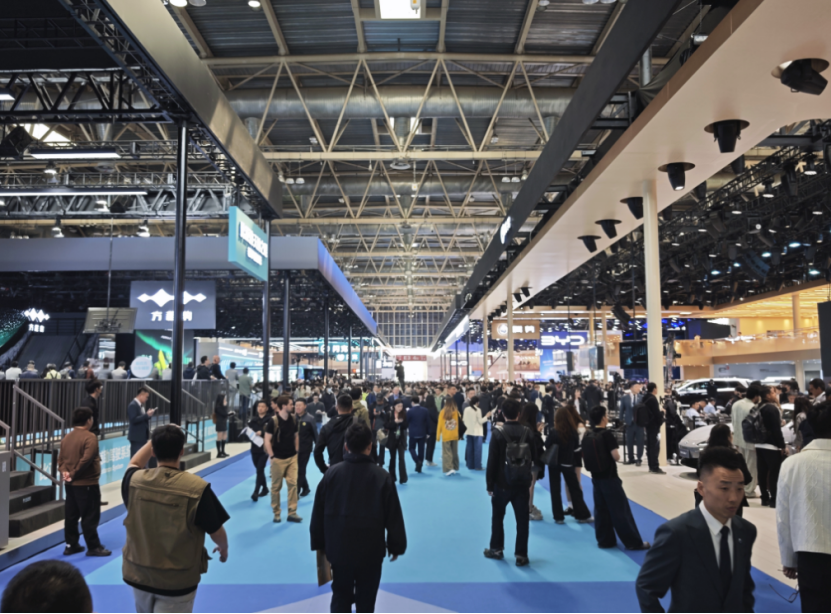

On April 24, 2026, the 19th Beijing International Automotive Exhibition opened its doors. Once a stage for flaunting "disruptive innovation" concepts, it now serves as a litmus test for "refined operations" prowess. Cost, efficiency, and integration—terms once relegated to the manufacturing back office—are now front and center, becoming key metrics for determining automakers' viability. The conversation has shifted from "skill showcases" to number crunching.

Inside and outside the exhibition halls, this focus on number crunching is taking tangible form. Chinese automakers are no longer fixated on breakthroughs in individual parameters but are systematically reducing platform R&D costs, with a more pronounced upward trajectory. Joint-venture brands' localization strategies reflect an extreme compression of supply chain responsiveness. Component suppliers, once hidden behind the scenes, are stepping into the spotlight, forging deep ties with automakers. Multiple automaker leaders are publicly signaling increasing urgency—a final battle for survival is underway.

▍The End of the 'Wild West' Era: From 'Surviving' to 'Breaking In'

If past auto shows revolved around "who built the cooler car," the core question at this year's event has become "who can keep building cars."

At the global strategy conference held on the eve of the auto show, Zhu Huaerong, Chairman of Changan Automobile, stated bluntly: "By 2030, the starting threshold for an auto group to survive will be 3 million units. Between 3 and 5 million units means just surviving, 5 to 8 million units allows for a comfortable existence, but to become a globally leading enterprise, annual sales must reach 8 to 10 million units or more." His judgment is not unfounded—the top 15 to 20 global auto groups already account for 70-80% of the market share, and the Matthew effect is accelerating. Zhu Jiangming, founder of Leapmotor, expressed a similar viewpoint: "The top ten global automakers must achieve at least 3.5 to 4 million units. To be an automaker, you must go global."

Global sales data also supports this judgment: According to the 2025 global automaker sales rankings, Toyota led with approximately 11.32 million units, followed by Volkswagen Group with 8.984 million units. Among Chinese automakers, BYD ranked sixth with 4.602 million units, SAIC Group seventh with 4.508 million units, and Geely Holding ninth with 4.116 million units. The "entry ticket" for the global top ten is around 3.5 million units, with the top five all exceeding 5 million units—3 million units is merely the threshold.

Currently, automaker profits are at rock bottom, with the norm being that the more you sell, the less you earn. More concerning than scale pressure is the profit dilemma. In 2025, the profit margin for China's auto industry was just 4.1%, a historical low. By 2026, the situation became even more severe—according to data from the China Passenger Car Association, the industry's profit margin further narrowed to 2.9% in January-February 2026, with profits of 43.5 billion yuan, a 30% year-on-year decline. For comparison, the profit margin in the non-ferrous metals industry was as high as 39.4%, and in the oil industry, it was around 30%.

Automaker financials are even more telling: among 12 mainstream listed automakers, none had a profit per vehicle exceeding 10,000 yuan. Changan Automobile, with a profit per vehicle of just 960 yuan, had the "thinnest" profit margins. New energy brands like Shenlan and Avatr are still in their investment phase, dragging down overall profitability. GAC Group swung from profit to loss, with a net loss of 8.784 billion yuan for the year. The entire industry is trapped in a dilemma of "increasing revenue without increasing profits." As industry insiders point out, expansion at the cost of "losing money on every vehicle sold" is ultimately unsustainable in business logic, no matter how strategically necessary.

As the domestic market is squeezed by weak demand and high costs, going global has become the essential pivot point. In the first quarter of 2026, China's total auto exports reached 2.226 million units, a 56.7% year-on-year increase, with new energy vehicle exports at 954,000 units, a staggering 120% year-on-year rise.

Chen Shihua, Deputy Secretary-General of the China Association of Automobile Manufacturers, commented that exports continue to grow rapidly, exceeding earlier expectations. However, no mainstream automaker at this year's show views simple trade exports as a long-term solution. "Local for local" has become the most frequently mentioned phrase in globalization narratives.

Changan Automobile officially released its "Global Reach Plan 2.0," planning to invest 100 billion yuan over five years to build a full-chain system of R&D, manufacturing, and services across 22 overseas bases, aiming for 1.5 million overseas sales by 2030. Unlike the first version, which focused on vehicle exports, this edition emphasizes exporting technology, standards, and industrial ecosystems, attempting to become a long-term global corporate citizen.

Leapmotor has chosen a different asset-light path, leveraging "Leapmotor International," a joint venture with Stellantis, to build on over 800 European outlets. It plans to launch CKD production in Spain in the fourth quarter of this year, advancing local manufacturing and procurement. Geely Automobile also announced its 2030 overseas strategy, planning to introduce over 10 new energy models to overseas markets, with overseas sales accounting for more than one-third of the total. While their paths differ, the direction is highly consistent—from "going out" to "breaking in" and then "rising up," Chinese automakers' globalization is being redefined.

▍The Second Half of Intelligence: From "Stacking Hardware" to "AI Integration"

If scale and integration are the "substance" of the auto show, then the dazzling array of intelligent technologies on display is the most direct "face" of this event. The most significant technological signal at this year's show is that the inaugural year of large-scale commercialization for L3 autonomous driving has truly arrived. The battleground for high-level intelligent driving is no longer limited to a few flagship models but has expanded across the mainstream price range of 200,000 to 500,000 yuan.

Huawei's ADS 3.0 intelligent driving system is making significant inroads into the mainstream market, while major new energy vehicle (NEV) players are universally pre-installing L4-capable hardware. Li Auto's flagship model, the all-new L9 Livis, made its global debut, equipped with four high-performance LiDAR sensors and two self-developed 5nm "Mach 100" chips, delivering a total computing power of 2560 TOPS. It also features the world's first "fully integrated" full-wire-controlled chassis, combining wire-controlled steering, four-wheel steering, and fully electric mechanical braking into one system.

NIO's ES9 also debuted with a 5nm intelligent driving chip and a 900V ultra-fast charging and battery-swapping architecture, enhancing the combination of premium intelligent driving and energy replenishment experiences. Meanwhile, traditional automakers and joint-venture brands are showing unprecedented urgency. Volkswagen's ID.ERA 9X features Momenta's intelligent driving solution, developed under Chinese leadership, and CATL batteries. Audi's A6L (C9) is deeply integrated with Huawei's ADS 3.0. This shift in R&D leadership from foreign to Chinese players reflects the most pragmatic localization breakthrough by joint-venture brands under survival pressure.

The evolution of smart cockpits has also reached a critical juncture, with the auto show almost declaring the full arrival of the AI era for cockpits.

Unlike the incremental upgrades of "bigger screens and more voice commands" in previous years, the cockpit systems on display this year are transitioning from passive response to proactive, predictive services. AI agents, multimodal interactions, and full-scenario ecological integration have become core features showcased by major automakers. The key differentiator in experience is no longer the simple accumulation of features but the upgrade of underlying computing power and the depth of localized ecological integration, particularly evident among leading new energy vehicle players.

Complementing intelligent driving and cockpits is the large-scale implementation of underlying technologies. The wire-controlled chassis has truly entered mass production, with flagship models universally equipped with wire-controlled chassis systems. 800V and even 1000V high-voltage platforms are being rapidly adopted, with 10-minute charging for over 400 kilometers of range becoming a mainstream configuration. Meanwhile, self-developed chips have become a new battleground for automakers, with 5nm process chips moving from concept to flagship standard, pushing the computing power race to a near-fever pitch.

Behind all these changes, a larger industrial ecosystem is taking shape: the auto show is no longer a solo performance by automakers but a concentrated display of full-industry-chain collaboration. At this year's show, deep ties between automakers and tech companies like Huawei, Momenta, and Horizon Robotics, as well as battery giants like CATL, have become the norm. Supply chain enterprises are moving from behind the scenes to the forefront, sharing exhibition space with automakers, reflecting a reallocation of discourse power in the automotive supply chain.

The cross-border integration of automobiles with AI and the Internet of Things is no longer just a conceptual discussion but is accelerating toward a future mobility ecosystem where vehicles connect with everything. As a vehicle's core competitiveness increasingly depends on chips, algorithms, and ecological integration capabilities, the traditional concept of a "car" itself is being redefined.

In previous years, the Beijing Auto Show was filled with emotions of catching up and disruption, with Chinese brands cheering for every progress and joint-venture brands anxious about the impact. But this year, emotions have given way to calm calculations. The words repeatedly spoken by automaker leaders are cost, efficiency, collaboration, and long-term survival. As Zhu Huaerong put it, the competitive landscape of the automotive industry will largely take shape in the next three to five years. Perhaps it is within this consensus, no longer romantic but sufficiently sober, that China's automotive industry is truly beginning to mature.

Layout 丨 Yang Shuo

-

![]()

Expert Interpretation of New Policy Combination: Activating the Trillion-Dollar Automotive Aftermarket

-

![]()

Doubao Goes 'Professional', Volcano Rolls the Snowball

-

AI: No Sign of a Bubble!

-

![]()

NVIDIA-Backed AI Unicorn Secures $1.5 Billion Funding: Revenue Soars 2000%

-

![]()

Doubao Pro is Here: How Can Seed 2.1 Be Integrated into Real Processes?

-

"PCB Juice" Sees Four Consecutive Declines: Even Computing Power Material Suppliers Can't Lift This "Old Stock"

-

![]()

Potential 'Seismic Shift' in the U.S. TV Industry: Competition Shifts from Hardware Sales to Traffic Entry Points

-

![]()

Audi A6L's Defense in the Luxury C-Class Market: Following Huawei's Smart Driving Integration, Is Large-Battery HEV the Next Move?