Over 60 New Car Models Launched in March, Are Automakers Panicking?

04/28 2026

04/28 2026

609

609

'Life-and-Death Race'

Before the first major auto show of 2026 even began, a 'battle' had already erupted among automakers. According to incomplete statistics, in March 2026, there were nearly 80 automotive-related press conferences, covering technology, new cars, brands, strategies, etc., with over 60 new car models launched.

BYD released its second-generation Blade Battery, HiMode launched 10 new models simultaneously, FAW-Volkswagen introduced 5 new models, Chery and Jaguar Land Rover unveiled a new brand, Expedition, the new-generation Mercedes-Maybach S-Class made its global debut, and Chery introduced the all-new QQ3...

Such a spectacle shocked industry insiders and consumers alike. Previously, there had never been such a dense (dense) concentration of press conferences before the large-scale auto show in April.

Li Xueyong, Executive Vice President of Chery, bluntly stated that the accelerated pace of model iteration and configuration stacking have become the primary means for many automakers to attract consumers. In March, the entire industry held over 80 press conferences, creating a situation where 'you can't win by competing, but you can't afford to lie flat either.' Li Bin, Chairman and CEO of NIO, also complained that the exponential acceleration of product iteration has even led to a widespread 'new car effect death valley' among automakers, where models peak at launch and become outdated as soon as they start climbing in popularity. Li Bin said, 'It's hard for any new model to remain a bestseller for a year,' and 'no flower blooms forever' has become the norm.

As automakers push out new models at an increasingly rapid pace, industry anxiety is evident. Adopting an offensive strategy seems to be the only way to alleviate the immediate 'life-and-death race.' Price wars, intense competition for market share, overcapacity... In 2026, automakers will still face numerous challenges.

Dense Launches

The beginning of 2026 has not been smooth.

According to data released by the China Association of Automobile Manufacturers (CAAM), in March, passenger car production and sales reached 2.446 million and 2.412 million units, respectively, up 74.8% and 57.1% month-on-month but down 5% and 2.3% year-on-year. From January to March, passenger car production and sales totaled 5.909 million and 5.934 million units, down 9.3% and 7.6% year-on-year, respectively.

Against the backdrop of sustained pressure in the auto market, automakers chose to 'play their cards' intensively in March.

The Leapmotor A10 offered technical configurations far exceeding those of its competitors in the same price range, attempting to break the existing price system with a 'step-up' logic. HiMode refreshed multiple models, including the Luxeed R7, Luxeed S7, Enjoy S9, Aito M7, and Aito M8, achieving a comprehensive upgrade in intelligent configurations. By leveraging a unified technical foundation and differentiated product positioning, they aimed to gain market attention through product density.

BYD was particularly active. From the launch of flagship models like the Yangwang U7, Yangwang U8, and the Yangwang U8L Dingshi Edition at the beginning of the month, to the official delivery of the Fangchengbao Titan 3 Flash Charge Edition, and the simultaneous launch of the Haishi 06 EV and Haibao 07 EV, culminating with the Song Ultra EV, new models were introduced almost every week. Meanwhile, BYD also released its second-generation Blade Battery and flash charging technology, giving its new products a generational advantage over competitors in terms of range and charging efficiency.

Xiaomi's new-generation SU7 was also a major release. In the highly competitive 200,000-300,000 yuan ($27,500-$41,300) segment, the new-generation Xiaomi SU7 saw a price increase of 4,000 yuan ($550) across the board.

Additionally, from the Zhiji LS8 to the XPeng MONA M03, the Dongfeng Nissan NX8 to the Zeekr 8X, the Qijing GT7, Expedition, the all-new QQ3, the Geely Starry L Longfeng Series, and the Geely Galaxy M7, new car launches were almost 'non-stop' throughout March.

Meanwhile, technology-themed press conferences from companies like GAC, XPeng, Chery, FAW-Audi, and Avatr also held their own, attempting to shift industry attention from the 'new car launch' arena to the new battlefield of 'technology.'

In April, the peak of new car launches intensified further. The Beijing Auto Show in April, serving as a wind vane (bellwether) for the year, saw the debut of hundreds of new models, severely diluting user attention. Many brands chose to 'jump the gun': the Wuling Huajing S made its debut on April 7, the Changan Avatr 12 launched on April 8, the Leapmotor D19, a large flagship SUV, launched on April 16, the Dongfeng Nissan NX8 launched on April 8, the Zhiji LS8 launched on April 16, and NIO held a technical press conference for the ES9 on April 9. Multinational automakers like GM, Nissan, Hyundai, and Volkswagen also concentrate (concentrated) released their new energy strategies and major new models.

The 'crazy' pace of new launches left netizens exclaiming, 'Smart electric vehicles are iterating so fast it's ridiculous; I can't keep up.'

Doubled Anxiety

Behind the dense (dense) launches lies the undeniable anxiety of automakers. More new models are being introduced, yet the market is not heating up accordingly.

During the prolonged dense (dense) exposure of new models in March and April, multiple new car-related contents emerged almost daily, making it difficult for any single model to maintain sustained attention. The 'window period' for publicity is also easily drowned out in the sea of information.

A relevant executive from Dongfeng Nissan bluntly stated, 'Nowadays, we need to break through the circle. If we can't even attract media attention, who will pay attention to us?'

In reality, the exposure gained from new car launches is hard to sustain. Li Bin said, 'The entire industry's smart electric products are iterating too fast. Previously, mechanical and gasoline vehicles iterated every 5 or 7 years, but now it's hard for a new model to remain a bestseller for a year.' In his view, with the iteration of intelligent chips, vehicles must also iterate, and advancements in battery technology also necessitate iteration. Without iteration, a vehicle feels 'old.' The 'window period' for the 'new car effect' is being compressed shorter and shorter.

The direct impact of this disconnect between industry iteration rhythm and product lifecycle is that new models peak in popularity at launch, and demand falls as production ramps up, making it difficult for automakers to balance supply and demand, leading to violent (severe) fluctuations in the supply chain. Wasting hundreds of millions of yuan on a single model has become commonplace, ultimately benefiting neither the manufacturer, the supply chain, nor the user.

Moreover, if product iteration is too rapid, the market lifecycle of new products is correspondingly shortened, bringing numerous derivative issues: On the one hand, simultaneous development of multiple generations of products leads to higher upfront R&D investment; on the other hand, the shortened amortization period for equipment investment also increases these costs. Additionally, the profit period is significantly shortened, often to less than half of the previous duration, inevitably leading to further cost increases and profit declines.

Public data shows that the profit margins of the automotive industry continue to decline, dropping to 4.1% in 2025, the lowest level on record. From January to February 2026, industry profits fell 30% year-on-year, with the profit margin further declining to 2.9%. Among automakers, 'cost reduction and efficiency improvement' has become a major topic in recent years.

However, despite the enormous costs, automakers still dare not halt their 'new product' launches. Consumer expectations for intelligence and autonomous driving are reshaping the competitive rules of the market. The current state of industry anxiety shows no signs of easing.

Chen Shihua, Deputy Secretary-General of the China Association of Automobile Manufacturers (CAAM), stated that looking ahead to the second quarter, the policy effects of 'two new initiatives' will continue to be released, and the Beijing Auto Show will kick off a dense (dense) period of new product launches, helping to boost market enthusiasm and stimulate automotive consumption. However, it should also be noted that the current external environment is complex and volatile, with rising risks of geopolitical conflicts, high volatility in raw material and key component prices, further increasing operational pressures on enterprises. The domestic market momentum remains weak, and the industry still faces significant pressure.

This article is original content from China Automotive News. Feel free to share it with your peers. For media reprints, please credit the author and source at the beginning of the article. Any media or self-media creating video or audio scripts based on this article's content will be held legally responsible for violations.

-

Hao Jida, Apple Supply Chain Coil Supplier, Switches Brokerage and Revives IPO Amidst Customer Dependency and Compliance Challenges

-

![]()

Annual Advertising Expenditure of VOYAH with Yudeshui: A Deep Dive

-

![]()

Can Computers, Despite Daily Price Hikes, Still Be a Viable Purchase?

-

![]()

January-June Auto Stocks' 'Resilience Ranking': Geely Alone Posts Gains, Six Plummet Over 40%, One Tumbles 54.5% | Mirror Pro

-

![]()

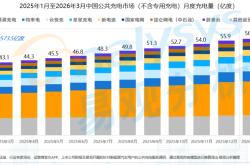

China’s Public Charging Market: Didi Charging, Teld, and Yunkuai Take the Lead

-

![]()

The First Year of AI-Native Mid-Year Shopping Festival: Technology Reconstructs Human-Product Matching for 618

-

![]()

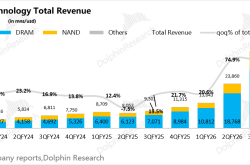

Micron has released its financial report, showing revenues of $41.5 billion, a 74% increase quarter-over-quarter, with a gross margin of 84.6%. The company provided both short-term and long-term guida

-

![]()

Expert Interpretation of New Policy Combination: Activating the Trillion-Dollar Automotive Aftermarket