AI Chip Price War Impacts Auto Industry, BYD and Changan Reluctantly Hike Prices

05/06 2026

05/06 2026

521

521

Since 2026, the global semiconductor industry has been swept by a fresh wave of price increases, with memory chips seeing the most dramatic spike. This industry upheaval, sparked by the explosive growth in AI computing power, has sent ripples downstream, ultimately reaching the automotive sector.

In the midst of this cost upheaval, BYD's move to raise prices first has emerged as an industry "barometer," hinting at the immense cost pressures automakers are grappling with.

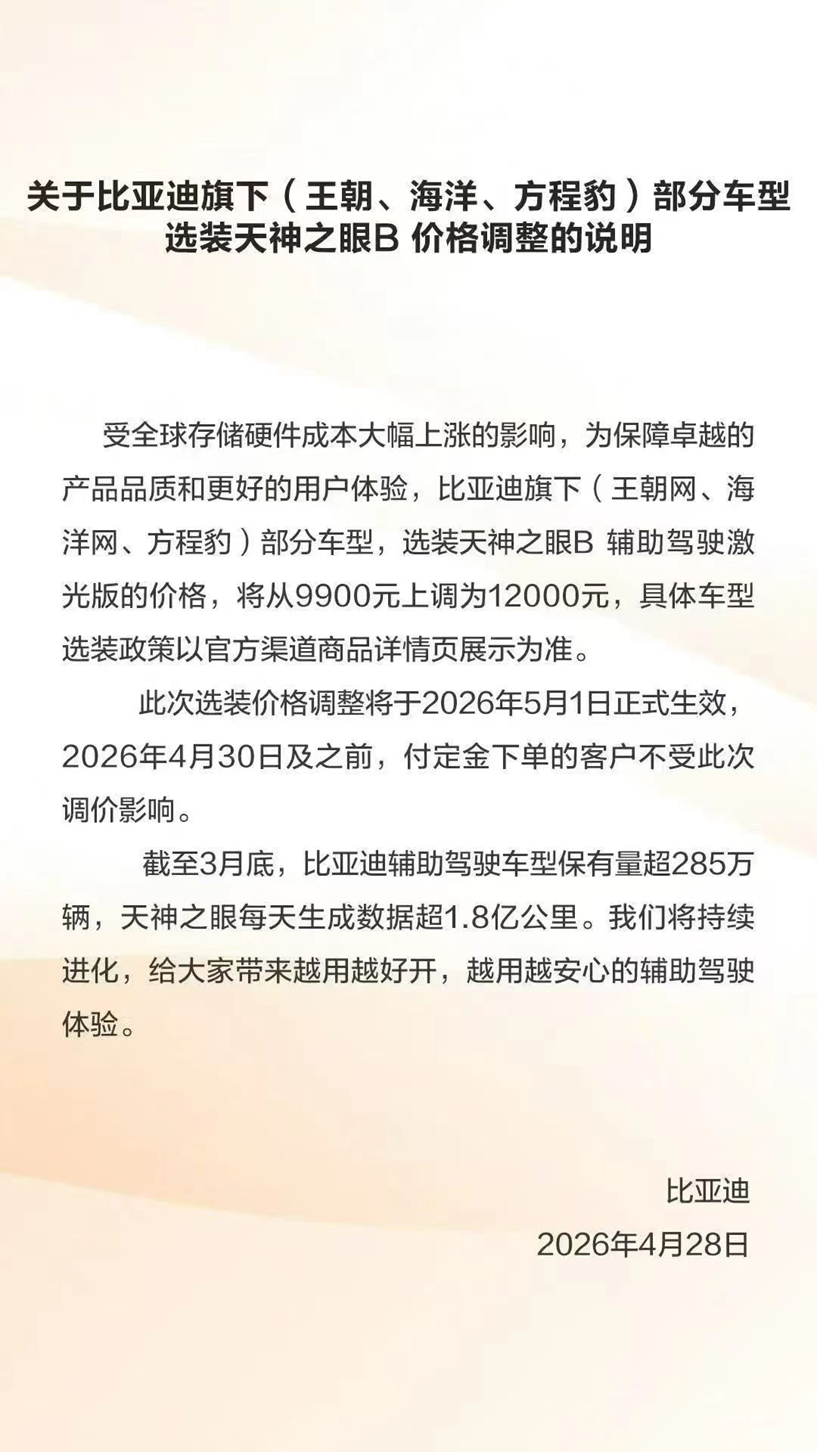

On April 28, BYD officially announced that the optional price for the 'Divine Eye B' assisted driving laser version of certain models under its Dynasty, Ocean, and Fangchengbao networks would rise from 9,900 yuan to 12,000 yuan, marking an increase of 2,100 yuan. The reason cited for this price adjustment is a "significant hike in global memory hardware costs." As a leading domestic new energy vehicle company, BYD's price adjustment is no hasty decision—the 'Divine Eye B' version is outfitted with NVIDIA's OrinX chip and boasts DRAM capacities ranging from at least 16GB to a maximum of 64GB. The surge in memory chip prices directly inflates the material costs associated with intelligent driving configurations.

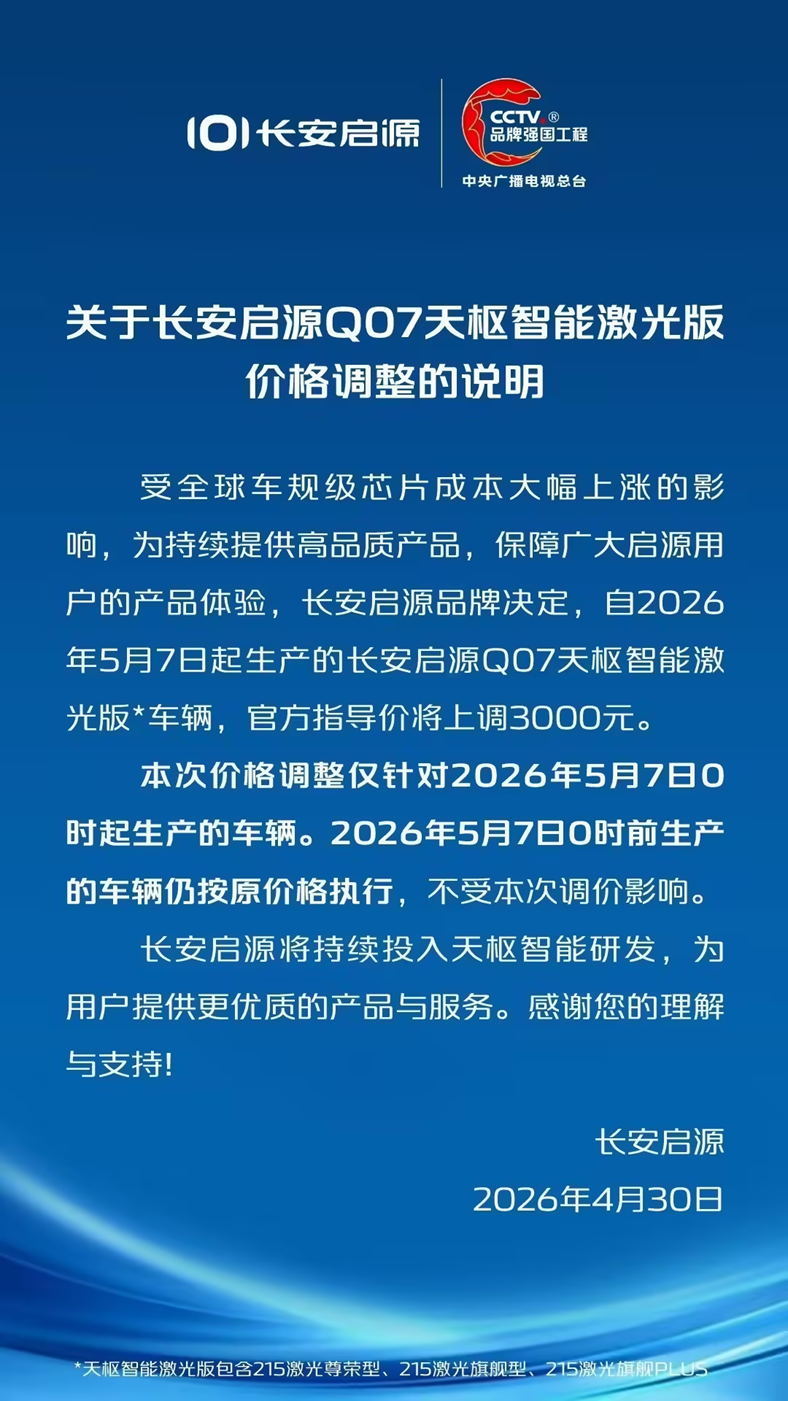

BYD's price adjustment, acting as the first domino, swiftly set off a chain reaction across the industry. On April 30, Changan Automobile's Qiyuan brand issued a price adjustment notice, stating that due to substantial increases in global automotive-grade chip costs, the official suggested price (recommended retail price) of the Changan Qiyuan Q07 Shuyu Intelligent Laser Version produced from May 7, 2026, would go up by 3,000 yuan. As another prominent domestic automaker, Changan's follow-up move further underscores the widespread impact of chip price hikes on automakers.

In reality, apart from BYD and Changan, since 2026, over 15 new energy vehicle companies, including Chery, Zeekr, and Xiaomi, have announced price hikes or reductions in terminal discounts, with increases spanning from 2,000 to 10,000 yuan. Behind these collective actions by automakers lies an insurmountable cost burden.

This wave of chip price hikes is not merely a traditional shortage phase but a structural crisis triggered by a mismatch between soaring demand and production capacity, with an intensity and duration that far surpass market expectations.

In the first quarter of 2026, global memory chip contract prices skyrocketed, with DRAM (memory) contract prices surging 90%-95% quarter-on-quarter and NAND Flash (storage) prices jumping 55%-60%. The price increases for automotive-grade chips were even more staggering, with DDR4 prices rising 337% annually, DDR5 prices surging over 300%, and spot prices for high-end automotive-grade DDR5 skyrocketing by 300%. The primary driver of this price surge is the "chip war" between the AI and automotive industries—a single AI server requires eight times the DRAM of a traditional server. Cloud giants like Microsoft and Google have pre-locked most chip production capacity for 2026 and even 2029, while the three major memory giants—Samsung, SK Hynix, and Micron—have shifted 18%-28% of their DRAM production capacity to HBM (high-bandwidth memory) for AI, significantly curtailing production of automotive-grade mature process chips.

The contraction on the supply side, coupled with surging demand driven by the automotive industry's shift towards intelligent transformation, has left automakers ensnared in "chip anxiety."

Today's smart vehicles have essentially transformed into "computers on four wheels," with a high-end intelligent model requiring 3,000-4,000 chips, several times that of traditional fuel vehicles. Memory chips are a core necessity—smart cockpits need to run large operating systems, and autonomous driving requires real-time processing of LiDAR point cloud data, both of which demand high-capacity, high-speed memory chips. The memory chip usage in a smart vehicle has surged from dozens of GB in traditional fuel vehicles to hundreds of GB or even terabyte-level. More critically, chip capacity expansion cycles are lengthy, with an advanced-process wafer fab taking 18-24 months from construction to production, meaning new capacity cannot be swiftly released. It is predicted that the memory chip supply satisfaction rate for the automotive industry may plummet below 50% in 2026, with this "hard shortage" expected to persist until at least the end of 2027.

For automakers, price hikes have always been a "dilemma" rather than a proactive choice.

The domestic automotive market remains fiercely competitive, with previous price wars already significantly compressing profit margins. Cui Dongshu, Secretary-General of the China Passenger Car Association, has pointed out that the automotive industry's profits are declining sharply, with upstream cost pressures continuing to mount. If automakers do not raise prices, the cost increases from chip price hikes will be fully absorbed by themselves, further squeezing profit margins and potentially impacting R&D investment and product quality. However, if they do raise prices, they risk declining terminal sales, especially amid a weak consumer market recovery and widespread hesitation among buyers. Every price adjustment carries the risk of losing some potential customers.

In Conclusion: For the entire industry, chip price hikes present both a challenge and an opportunity.

They compel automakers to reevaluate their cost structures and supply chain layouts, accelerating chip self-research and domestic substitution processes while propelling the industry towards high-quality development. Meanwhile, they encourage consumers to view vehicle price fluctuations more rationally, focusing on core product value rather than solely pursuing low prices. The successive price adjustments by BYD and Changan are a microcosm of the automotive industry amid the chip price surge. This AI-driven chip restructuring is profoundly altering the competitive logic of the automotive industry, testing the resilience and wisdom of every automaker. For automakers, only by proactively responding through technological innovation, supply chain upgrades, and product optimization can they break through the cost dilemma.

In the short term, the "wave of price hikes" among automakers may persist, with more small and medium-sized automakers likely to be forced out of the market due to insurmountable cost pressures, further concentrating the industry. It is believed that in the future, with the continuous maturation of domestic chip technology, the gradual release of production capacity, and improvements in automakers' supply chain management capabilities, chip cost pressures are expected to gradually ease.

(Image sourced from the internet; removal upon infringement claim)

-

![]()

Is Zhipu's Trillion-Yuan Market Cap, Despite No Profit, Truly 'Outrageous'?

-

![]()

XiaoPai Unveils Home AI Brain, Paving the Way for Smart Homes to First Grasp 'Home Understanding'

-

![]()

Is the Future of Extended-Range EVs Pure Electric or Li Auto’s 5C Extended-Range? A Li Auto Executive Shares Insights

-

Ant Group’s New Board of Directors: Signaling a New Era?

-

![]()

Google Initiates TPU Sales, as Industry Leaders Eye AI Chips for 'Cost-Effective Tokens'

-

![]()

Input Methods: The Rising Star in AI! WeChat, Doubao, and Qianwen Lead the Charge into the Voice Input Era

-

![]()

Struggling to Sell? Cut It Out! Toyota, Volkswagen, and Changan Lead the Charge in Streamlining, Eliminating Non-Core Products in the Blockbuster Model Era

-

![]()

Arm China and Volcano Engine Join Forces to Expedite Cloud Computing and AI Infrastructure Rollout