Charging Pile Operators Are 'Hanging on by a Thread'

05/08 2026

05/08 2026

484

484

The Charging Pile Industry Can No Longer 'Keep Pace'

Behind the plummeting charging service fees, numerous charging pile operators are 'hanging on by a thread'.

The burgeoning new energy vehicle (NEV) sector once transformed the charging pile industry into a lucrative investment opportunity. Nowadays, the market is saturated, and competition is fierce.

Several years ago, it was common to hear about hour-long waits for charging at highway rest stops and tourist spots during holidays. However, with the widespread deployment of charging infrastructure, the industry has expanded rapidly, significantly alleviating the 'charging difficulty'.

However, this rapid expansion has also plunged the industry into a cutthroat competitive environment. According to CCTV's Economic Half-Hour, leading companies' charging stations now earn a net profit of just 4 cents per kWh, with over 60% of public charging stations either operating at a loss or with minimal profit, making it extremely challenging for small and medium-sized operators to survive.

From 'riding the wave' to 'fighting for survival,' is this once-profitable sector still appealing?

Profitability Challenges Amid Rapid Expansion

Data from the National Charging Infrastructure Monitoring Service Platform reveals that by the end of February 2026, China's total electric vehicle charging infrastructure surpassed 21.01 million units, marking a 47.8% year-on-year increase. This includes 4.834 million public charging units (+28.8% YoY, with a total rated power of 229 million kW) and 16.176 million private charging units (+54.6% YoY).

Charging station at a highway service area (Photo/Liu Shanshan)

In 2026, charging volumes during holidays soared year-on-year, with significantly reduced wait times. 'Charge-on-arrival' has become the norm, thanks to policy support. The 'Three-Year Doubling of EV Charging Infrastructure Service Capacity' Action Plan (2025–2027) aims to construct 28 million charging units by the end of 2027 to meet the charging needs of 80 million electric vehicles.

The industry has transitioned from a shortage of charging piles to an oversupply, resolving a key bottleneck for NEV adoption. However, the larger scale has also brought about wider losses, posing another urgent challenge for the charging sector.

According to CCTV News, a small public charging pile operator in Qingdao, Shandong, generated 500,000 yuan in annual revenue when its station was established in 2020. By 2023, annual revenue had plummeted to 80,000 yuan, with profits now hovering around 60,000 yuan after accounting for labor and maintenance costs. A 16-unit station built by a leading company for 1.2 million yuan earns a net profit of just 4 cents per kWh after deducting equipment depreciation, rent, labor, and power losses.

Several factors are making it increasingly difficult for public charging pile operators to achieve profitability.

Firstly, automakers and battery giants are reshaping the competitive landscape. Companies like BYD, NIO, and CATL view their charging and battery swap networks as supporting services for vehicle sales, aiming to enhance user experience and boost sales rather than relying on charging for profit. The widespread rollout of such facilities has enriched supply but also diverted core customers from third-party operators, squeezing their survival space. At the ES9 product launch, NIO founder, chairman, and CEO William Li announced that as of April 8, 2026, NIO had invested over 20 billion yuan in charging and battery swap infrastructure, operating 8,751 stations with over 10.72 million battery swaps and 85.55 million charging sessions.

Meanwhile, rapid technological advancements are exacerbating profitability pressures. Charging pile technology cycles are significantly shorter than those of traditional infrastructure. Before 2020, 60–120 kW air-cooled piles were mainstream but are now obsolete. Fast-charging piles (180–240 kW) that gained popularity in 2023 will soon require upgrades to 360 kW or higher. From 2026 onwards, 250 kW+ ultra-fast charging is becoming the standard, with 600 kW liquid-cooled technology gaining traction.

Cui Dongshu, secretary-general of the China Passenger Car Association, noted that the ratio of pure EVs to charging units was approximately 0.82:1 in 2025, nearing a 1:1 supply-demand balance. With a surge in public charging pile installations, the vehicle-to-pile ratio has become more favorable, entering a phase of 'more piles than vehicles.' This has intensified operational differentiation, with older, low-power charging piles experiencing declining utilization.

These upgrades are driven by both policy and market forces. Policies mandate high-power pile configuration ratios and efficiency standards, phasing out 30% of old, inefficient piles. Tong Zongqi, deputy secretary-general of the China Electric Vehicle Charging Infrastructure Promotion Alliance, stated that high-power charging facilities refer to DC piles with single-gun output exceeding 250 kW. 'For EV owners, future travel will offer richer, more convenient charging options tailored to diverse scenarios,' he added.

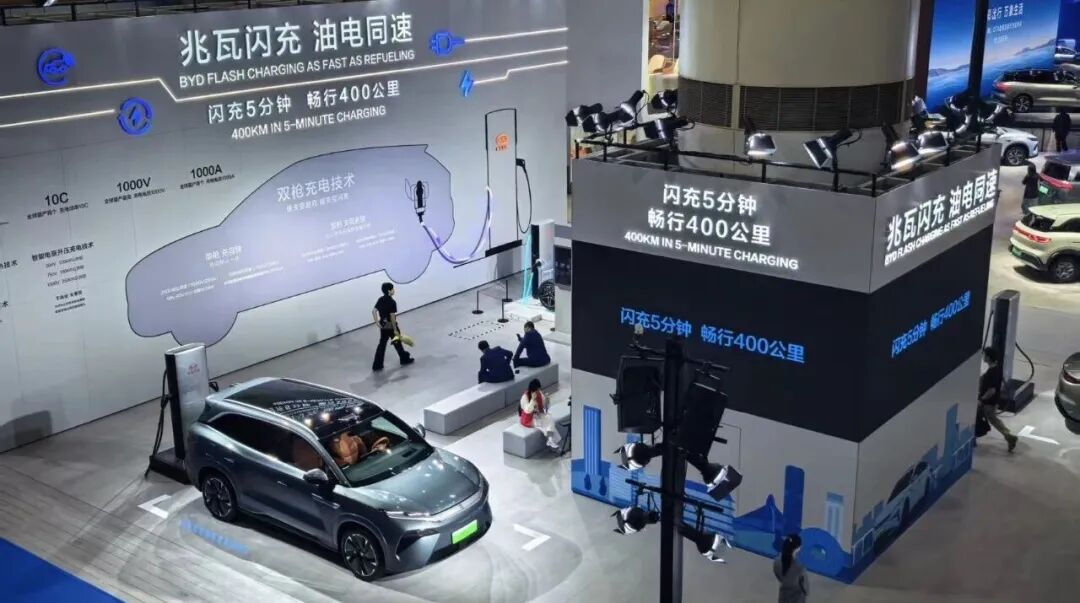

BYD's megawatt flash-charging tech demo zone at the 2025 Guangzhou Auto Show (Photo/Liu Shanshan)

With the widespread adoption of 800V high-voltage platform vehicles and megawatt-level ultra-fast charging piles, vehicles can recharge 400 km of range in just 5–10 minutes, significantly diverting traffic from low-power piles.

Early 60 kW piles cost 50,000 yuan each and took 1.5 hours to fully charge a 70 kWh battery, with a planned payback period of 5–8 years. Today, with NEV ranges universally exceeding 600 km, these piles become 'low-efficiency' after just 3–4 years, with utilization rates below 10%, facing elimination before recouping costs.

Additionally, falling costs have disrupted the pricing equilibrium. Standardized mass production has reduced the price of 60 kW charging piles from 50,000 yuan to under 20,000 yuan. New entrants, leveraging cost advantages, have undercut prices, forcing incumbents to follow suit.

Will Charging Fees Increase?

Charging fees consist of two parts: electricity costs and service fees.

Electricity costs, which constitute the larger share, are set by the State Grid and remain stable, with no adjustment authority for charging firms. The floating service fee is the key determinant of operators' profitability and survival pressure.

Charging service fees cover costs such as site rent, equipment depreciation, maintenance, labor, and power losses. In recent years, rents in prime urban areas have risen, fast-charging equipment investments have increased, and maintenance and power upgrade costs have climbed. Meanwhile, charging subsidies are being phased out, making long-term low-price operations unsustainable.

However, most charging pile operators dare not raise service fees lightly.

EV owners' primary demands are 'available piles, fast charging, and reasonable prices,' with no strong preference for specific brands. Since charging is largely self-service—from unplugging to payment—consumers are highly price-sensitive and unlikely to pay extra for brands or services. In dense charging areas, the market is buyer-driven, with owners comparing real-time electricity prices via apps and choosing the cheapest option. Any operator raising fees first risks rapid user loss. This 'price-focused, brand-agnostic, low-engagement' mindset makes it hard for operators to profit from brand premiums or differentiated services, trapping them in price wars.

Tong Zongqi believes that as charging networks expand, the early phase of subsidy-fueled price wars will end. Different stations have varying service levels, construction costs, and losses, justifying differentiated pricing. 'We need to guide operators to use tiered pricing to influence owner choices,' he said.

Escaping low-profit or loss-making traps is now a priority for the charging pile industry. Rather than blind expansion, operators must carefully consider site selection, improve station environments, APP experiences, and equipment reliability to retain users. More efficient charging gear, smart maintenance to cut labor and power losses, and revenue diversification through energy storage and peak-shaving arbitrage are essential to move beyond reliance on service fees.

Operators can also explore diverse profit models, such as integrating retail, advertising, and vehicle maintenance at charging stations or partnering with automakers and financial platforms for bundled deals, transforming charging points into comprehensive service hubs. New models like battery swapping and leasing can complement traditional charging, offering fresh growth avenues.

Clear policy guidance and regulation are also vital for the industry to escape cutthroat competition. Unified service standards, transparent pricing rules, and curbs on predatory price wars—alongside shifting subsidies from 'per-pile counts' to 'operational performance'—will encourage firms to focus on service quality and station excellence, fostering a market ecosystem of 'quality-driven pricing' and healthy competition.

As the 'capillaries' of the NEV industry, the healthy development of charging piles is crucial for the sector's steady progress. After industry consolidation, with refined operational models, upgraded charging technologies, and more regulated competition, the sector will overcome low-price traps and move toward a new phase of high-quality development.

-

![]()

Total Investment Hits Nearly 3.28 Billion! Goertek Launches Mass Production of 12-Inch Transparent Substrate Wafer for AR Glasses’ Micro-Nano Optical Components

-

![]()

Why Is This Precision Optical Film Leader Worth Reevaluating with a Tens of Millions Procurement?

-

![]()

AI Costs Plummet by 90% Over Nine Years: Key Insights from Davos You Shouldn’t Miss

-

Doubao, Your Late-Night AI Companion, Now Eyes Profitability

-

![]()

SRC Empowers SEER Intelligence to Reach a Market Cap of Tens of Billions, Yet Fails to Sustain Profitability

-

![]()

China’s Embodied AI Industry Faces Fierce Domestic Competition, Making Overseas Expansion Essential for Survival

-

![]()

32.8 Billion Yuan Investment! Goertek’s 12-Inch AR Glasses Optical Wafer Base in Lingang Begins Operations

-

![]()

How Far is the All-New Li Auto L8 from Being the Best Five-Seat SUV with In-House Full-Stack Development?