Has Seres Reached Its Bottom?

05/12 2026

05/12 2026

347

347

Seres' stock price has been declining for a long time. Since its H-share listing in November 2025, the stock has almost unilaterally trended downward, falling from HK$131.5 to around HK$70. The A-share price has nearly halved from its September 2025 peak.

It is a fact that the entire new energy vehicle (NEV) sector is under pressure. Since September 2025, Li Auto, XPeng, and Leapmotor have all seen poor stock performance. Industry-wide challenges such as peak penetration rates, price wars, and slowing growth rates affect all players equally.

However, Seres' stock price has been even weaker and has fallen further. This cannot be explained solely by the 'macro environment.'

So, why is a high-end NEV manufacturer with annual revenue of 165 billion yuan and a gross margin of nearly 29% underperforming its peers in stock price? Why are sales and average selling price (ASP) rising, yet profits fail to drive market capitalization? This article attempts to answer these questions from three perspectives: fundamentals, business model, and valuation pricing logic.

I. Has Profitability Really Declined?

A gross margin of nearly 29% is an impressive figure among vehicle manufacturers.

In 2025, Seres' NEV gross margin reached 28.76%, up 2.55 percentage points from the previous year. Including fuel vehicles and other businesses, the overall gross margin was 26.88%.

Horizontally, focusing on automotive sales, Xiaomi Auto's gross margin was 24.3% during the same period, BYD's was around 20%, Li Auto's was about 18%, and Tesla's and NIO's were both around 14%.

It can be said that Seres' gross margin is in a league of its own.

However, the market is more concerned with the fact that Seres' high gross margin has not organically translated into net profit growth.

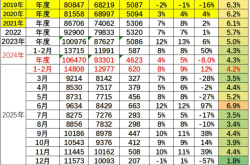

In 2025, amid a 10.1% increase in Aito sales and a 3.7% rise in per-unit ASP, Seres' revenue reached 165.054 billion yuan, up 13.69% year-on-year.

Net profit, however, remained almost stagnant, with attributable net profit at 5.957 billion yuan, up just 0.18% year-on-year, while non-recurring net profit fell by 7.8%. Government subsidies had the largest impact on non-recurring items.

In other words, despite a 13.69% revenue increase and rising gross margins, Seres' core business earnings declined.

Coupled with sales, administrative, and R&D expenses growing at a faster rate than revenue, significantly consuming the gains from margin improvements, the conclusion that profitability has deteriorated seems inevitable.

But this conclusion is somewhat unfair to Seres, or at least not objective enough for its 2025 performance.

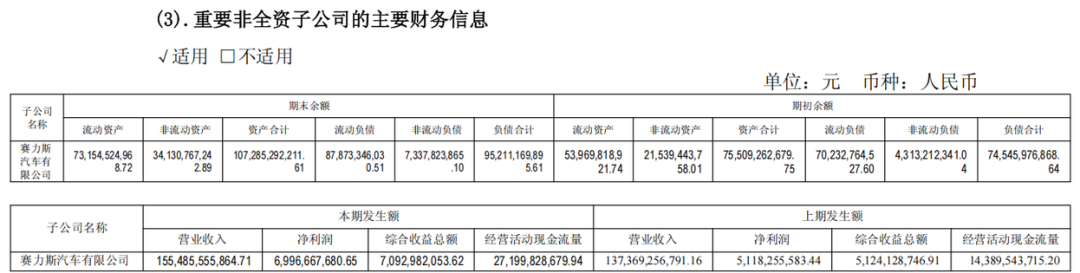

Under the net profit metric, Seres (the listed company) reported 4.74 billion yuan and 6.15 billion yuan in 2024 and 2025, respectively, with net profit margins of 3.27% and 3.72%.

Its most important subsidiary, Seres Automotive Co., Ltd., accounted for about 94% of total revenue, with net profits of 5.12 billion yuan and 6.997 billion yuan in 2024 and 2025, respectively, and net profit margins of 3.72% and 4.5%. Non-recurring net profit in 2025 was 6.25 billion yuan, up 24.69% year-on-year, with the non-recurring net profit margin also improving.

The issue lies in the equity structure. In 2024, minority shareholders absorbed nearly 1.3 billion yuan in losses, while in 2025, their share of profits turned positive at 190 million yuan.

This does not deny Seres' 'revenue growth without profit growth' in 2025 but rather suggests a complex situation where fundamentals have not worsened, but the equity structure has been diluted.

Of course, this refers only to 2025.

In the first quarter of 2026, Seres' profitability did see a material decline.

Q1 2026 revenue was 25.75 billion yuan, up 34.5% year-on-year—a significant increase. Total sales reached 88,400 units, up 29.4% year-on-year, including 78,500 NEVs, up 43.9% year-on-year.

However, profit performance was poor across all metrics. Net profit fell 17.6%, attributable net profit was 754 million yuan, up less than 1% year-on-year, and non-recurring net profit dropped 73.87% year-on-year to 103 million yuan.

Gross margin, a key indicator of profitability, declined by 2.4 percentage points quarter-on-quarter and 1.4 percentage points year-on-year. This was due to a shift in sales mix toward lower-margin models, Aito absorbing purchase tax for some orders, and rising raw material costs.

Operating expense ratios rose 2.6 percentage points compared to Q1 2025, combining with margin declines to pressure net profits. The largest change was in R&D expenses, detailed below.

Beyond the income statement, the cash flow statement also raised concerns.

In Q1 2026, Seres' net cash flow from operating activities was -20.95 billion yuan, compared to -7.63 billion yuan a year earlier, with net outflows more than doubling. The company attributed this to increased inventory, channel financing, and growing accounts receivable.

II. Huawei Partnership: Dividends Received and Costs Paid

Seres' collaboration with Huawei is a turnaround story worthy of a business school case study in any industry.

In 2020, Seres (then known as Sokon) had annual revenue of just 14.3 billion yuan and a net loss exceeding 1.7 billion yuan, struggling as a third-tier automaker in the fuel vehicle sector.

With Huawei's comprehensive support, Seres achieved a miraculous brand transformation: The Aito brand rapidly gained traction after launch, with per-unit pricing stabilizing above 300,000 yuan. The M9 model topped luxury car sales above 500,000 yuan for multiple months, with monthly sales once exceeding 18,000 units. Total revenue reached 165 billion yuan in 2025, a tenfold increase in five years.

Huawei provided Seres with brand premium, product definition capabilities, advanced intelligent driving technology, and a high-quality nationwide sales network. The market consensus is clear: Without Huawei, there would be no Seres today.

But every coin has two sides.

Every resource Huawei invested in Seres came with a price.

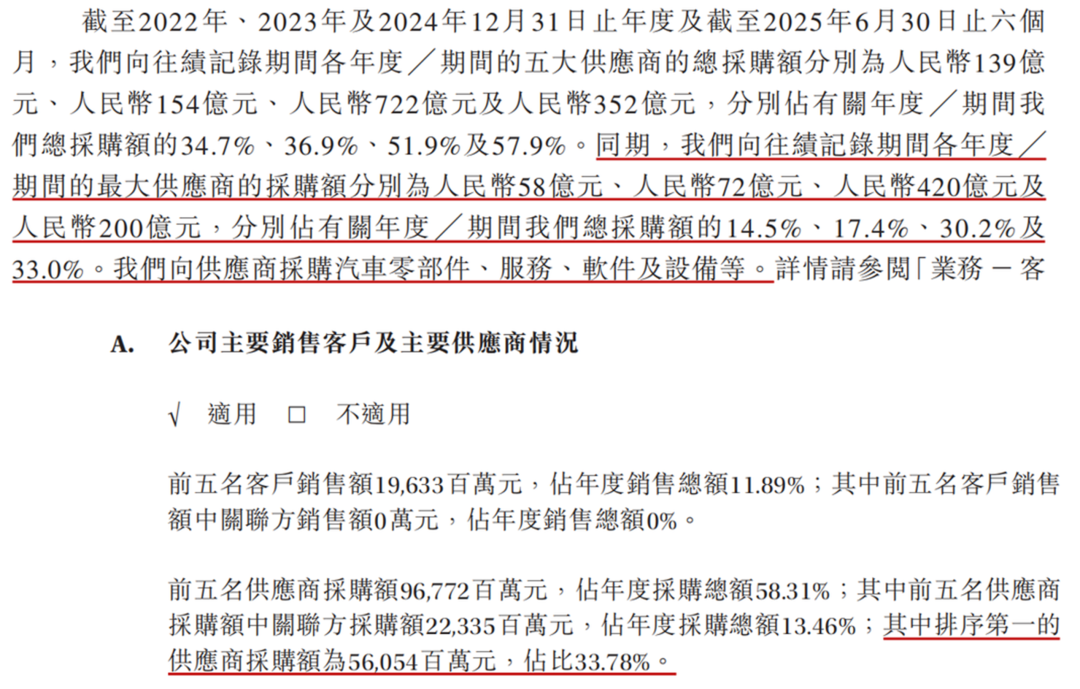

According to Seres' Hong Kong IPO prospectus, from 2022 to 2025, payments to its largest supplier amounted to 5.8 billion yuan, 7.2 billion yuan, 42 billion yuan, and 56 billion yuan, accounting for 14.5%, 17.4%, 30.2%, and 33.78% of total procurement, respectively.

This largest supplier is widely believed to be Huawei.

The cumulative 111 billion yuan paid over four years purchased hardware and software such as intelligent cockpits and autonomous driving assistance systems, as well as Huawei's nationwide store channel services and brand marketing support. Seres bought not just hardware but also 'the ability to sell cars.'

Although this differs from the common perception of 'profit sharing,' Huawei, as a supplier and channel service provider, has indeed taken a significant slice of Seres' revenue.

This cooperation model, especially in sales, is reflected in the income statement.

In 2025, Seres' selling expenses reached 24.19 billion yuan, with advertising, flagship store construction, and service fees accounting for 22.95 billion yuan. Much of this went toward Aito exhibit traffic generation, store sales promotion, and brand marketing services within Huawei's channel system.

Both selling expense ratios and cost structures differ significantly between Seres and other NEV manufacturers.

Since Hong Kong-listed peers like Li Auto and XPeng combine selling and administrative expenses, their totals are used to assess Huawei's impact.

In terms of selling and administrative expense ratios, Seres, NIO, Li Auto, and XPeng stood at 17.6%, 18.4%, 9.5%, and 12.3%, respectively, in 2025.

On a per-unit basis, selling plus administrative expenses were 56,000 yuan, 49,000 yuan, 26,000 yuan, and 22,000 yuan per vehicle, respectively.

In other words, even with Aito achieving industry-leading gross margins, high channel costs significantly eroded profit margins, leaving limited gains at the net profit level.

This is a classic trade-off of sovereignty for efficiency.

The story does not end here. More impactful for Seres is the fundamental shift in market expectations.

For Sokon, which faced annual losses and survival struggles, merely surviving was a victory. But for Seres, a high-end NEV benchmark with 165 billion yuan in annual revenue and far higher margins than peers, the bar for external scrutiny is much, much higher.

The question used to be: 'Can Huawei save Seres?' Now it is: 'Can Seres derive more independent value from its heavy reliance on Huawei?'

Investors deeply worry about how much autonomy Seres retains in product definition, pricing, and channel control amid deep Huawei cooperation. This makes the company's profits seem more like 'residual claims' after Huawei's technological and channel enablement, rather than native (native) profitability from an independent automaker.

Some investors directly asked on interactive platforms: 'Is the company considering negotiating with Huawei to reduce the so-called 'Huawei tax?''

III. Shifting Valuation Logic

These concerns are already reflected in Seres' valuation.

Due to its deep cooperation, capital markets once equated Seres with 'Huawei's car-making' symbol.

When Aito hit one million units in September 2025, Seres was still seen as a 'tech growth stock under Huawei's HarmonyOS Intelligent Mobility concept' in A-shares, with a trailing P/E ratio once exceeding 40x.

But Huawei's HarmonyOS Intelligent Mobility 'ecosystem' expanded rapidly, with Aito evolving from a solo act to 'five brands in parallel.' Seres shifted from exclusive partner to 'one of N,' stripping away its scarcity premium layer by layer.

The A-share price nearly halved from its September 2025 peak, while the H-share price fell from HK$131.5 to around HK$70 within six months of listing, largely reflecting this valuation logic shift.

The erosion of scarcity is clearly trackable in data.

Aito's sales share within HarmonyOS Intelligent Mobility declined from about 87% in 2024 to around 72% in 2025, even dipping below 70% in Q1 2026.

Huawei's automotive BU has spun off as Inceptio Intelligence, with Seres and Changan each holding 10% stakes. This signals Huawei's shift from 'deep partner' to 'supplier open to the entire industry.'

Meanwhile, collaborations with Chery (Luxeed), BAIC (Stelato), JAC (Maestro), and SAIC (Z-Bound) are fully underway, with Huawei expected to launch multiple new models in 2026. Prime store display space, marketing resources, and technology first-mover rights are no longer exclusive to Aito.

From an industry perspective, overall NEV penetration has plateaued at high levels, with range-extended models facing particular controversy over peaking golden cycles.

Citibank explicitly warned of 'the impending end of the range-extender golden cycle' and downgraded Seres' sales forecasts. When scarcity fades and growth doubts emerge, valuation multiples compress not just due to market sentiment but a fundamental repricing.

This drives Seres to ramp up R&D investment. As mentioned earlier, R&D expenses saw the largest change among costs.

In 2025, Seres' R&D expenses were 7.954 billion yuan, up 42% year-on-year, while R&D investment grew even faster at 77.4% to 12.51 billion yuan, with its revenue share rising from 4.9% in 2024 to 7.6%.

Li Auto, XPeng, and NIO disclose only R&D expenses, but multiple sources suggest they likely expense R&D investments. If so, Seres' R&D investment scale exceeded NIO, XPeng, and Li Auto in 2025 based on available data.

In Q1 2026, Seres' R&D expenses surged over 70% year-on-year, the largest increase among period expenses, with the R&D expense ratio rising further from Q1 2025.

R&D investments focus on flagship product development, platform construction (e.g., Magic Cube Technology Platform 2.0 intelligent vehicle architecture, fifth-generation 2.0T super range-extender technology), AI transformation, and innovative businesses.

On one hand, Seres uses AI to reshape existing product forms and integrate data flows and business processes across segments. On the other, it layout (positions) for future businesses by developing technologies for bipedal robots, wheeled robots, quadrupedal robots, and wheeled-legged composite robots.

Increased R&D spending is both an attempt to build non-Huawei moats and a search for the next pricing anchor before range-extender dividends fade.

-

![]()

Qianwen Revolutionizes Taobao: Alibaba's Bold Self-Transformation

-

![]()

What’s the Real Story? China Leads in 5G Patents but Pays More in Royalties!

-

![]()

8 Auto Companies Unanimously Deny 'Summons for Talks' Rumors, but OTA Battery Locking is Real

-

![]()

China’s Premier AI Infrastructure Provider Launches IPO, with Zhipu AI and SenseTime as Key Backers

-

![]()

Have car prices gone up?

-

![]()

Samsung Withdraws, Joint Venture Automakers Brace for Battle

-

![]()

Nvidia Starts Adding Soap to the Bubble

-

![]()

Can Car Companies Not Generate Profits Solely from Vehicle Sales? What Challenges Do They Face?