Can Car Companies Not Generate Profits Solely from Vehicle Sales? What Challenges Do They Face?

05/12 2026

05/12 2026

435

435

In recent years, new energy vehicles have unquestionably emerged as the focal point of market attention. However, despite being widely regarded as a promising sector, a recent statement by Zhao Fei, General Manager of Changan Automobile, has ignited a heated debate. Zhao Fei claimed that automakers are currently struggling to turn a profit solely from selling cars. What is the underlying reality? What are the challenges confronting car companies?

I. Can Car Companies Not Generate Profits Solely from Vehicle Sales?

According to a report by Haibao News, "Currently, car companies are finding it increasingly difficult to profit solely from selling cars." This sentiment was echoed by Zhao Fei, General Manager of China Changan Automobile, at the recent High-Level Forum on the Development of Intelligent Electric Vehicles (2026).

Zhao Fei's remarks are not alarmist but rather a candid reflection of the current state of the automotive industry.

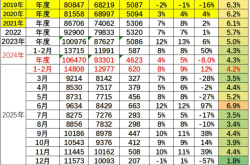

"From January to February this year, the automotive industry's profit margin stood at a mere 2.9%, indicating significant downward pressure," bluntly stated Cui Dongshu, Secretary-General of the China Passenger Car Association (CPCA), at the aforementioned forum. "The automobile manufacturing industry is facing profit pressures from both upstream and downstream sectors."

From leading companies to small and medium-sized brands, and from new energy vehicles to traditional fuel-powered cars, the entire industry seems to be trapped in a vicious cycle of "increasing sales without corresponding revenue growth, and rising revenue without improved profitability." Sales volumes continue to climb, yet profits are dwindling. Many companies are even operating at a loss for extended periods, relying on financing and shareholder investments to sustain their operations.

According to Cui Dongshu, in January-February 2026, the profit margin of the non-ferrous metal industry reached 39.4%, compared to just 9% in 2017. The oil industry's profit margin soared from 5% to approximately 30%. In stark contrast, the automotive industry's profit margin plummeted from 8% in 2017 to 2.9%. "The automotive industry has made substantial contributions to upstream sectors, but the disparity between upstream and downstream sectors is becoming increasingly pronounced. The mid- and downstream sectors, particularly the automotive industry, are under immense pressure and are currently struggling," Cui Dongshu remarked candidly.

II. What Challenges Do Car Companies Face?

Currently, many Chinese automakers find themselves in the precarious position of struggling to profit from vehicle sales. What are the deep-seated reasons behind this predicament? How can they find a way out?

Firstly, intense price wars at the market level have severely eroded automakers' profits. In recent years, led by Tesla's significant price reductions, the entire automotive market has been engulfed in fierce price competition. This price war has plunged the market into a state of continuous internal strife, serving as the direct catalyst for the steady decline in automakers' profits. This is not a healthy form of market competition in the traditional sense but rather a classic example of the "prisoner's dilemma" game. Amid intensifying competition in the existing market, automakers, in a bid to secure a limited market share, maintain capacity utilization rates, and enhance brand visibility, have resorted to price as the most direct and primitive competitive weapon.

The essence of this competitive model is a concentrated manifestation of low-level, homogeneous competition. When products struggle to differentiate themselves in terms of core technology, intelligent experience, and brand premium, price reductions become the only shortcut to attract consumer attention and stimulate short-term sales. However, this strategy of "trading price for volume" is akin to drinking poison to quench thirst. It directly compresses the profit margin per vehicle and can even lead to a situation where "selling one car results in a loss." More profoundly, it distorts the industry's value assessment system, creating sustained expectations of price reductions among consumers, further suppressing normal market demand, and trapping the entire industry in a vicious cycle of "increasing competition leading to losses, and losses leading to even fiercer competition."

It can be said that there are no winners in this price war. It not only drains resources from vehicle manufacturers but also transfers immense operational pressure to downstream dealer networks and upstream component suppliers, resulting in widespread losses among dealers, extended payment terms for suppliers, and a sharp deterioration in the ecological health of the entire supply chain.

Secondly, the phenomenon of supply-side bottlenecks is severe. In the automotive supply chain, automakers occupy a central position, but this does not imply they hold absolute bargaining power within the supply chain. In fact, Chinese automakers face numerous supply-side bottlenecks, particularly in core components such as power batteries, where they are highly dependent on upstream suppliers.

As the "heart" of new energy vehicles, power batteries account for a significant portion of the total vehicle cost. Previously, we have repeatedly highlighted that the profits of a dozen listed automakers cannot match those of a single company like CATL, which is a classic illustration of this issue. Currently, the global power battery market is characterized by oligopoly, with a few large suppliers controlling core technologies and most of the market share. This places automakers in a passive position when procuring power batteries, with weak bargaining power. Upstream suppliers can arbitrarily adjust prices and supply volumes based on market conditions and their own interests, while automakers can only accept these changes passively.

For instance, when the prices of raw materials for power batteries rise, suppliers swiftly pass on these costs to automakers. However, automakers, fearing loss of market share, dare not easily pass on these costs to consumers and must bear them themselves, leading to severe erosion of profits. Additionally, technological bottlenecks in some core components also limit automakers' development. Due to a lack of independent research and development capabilities, automakers have to rely on imports or cooperate with foreign companies, which not only increases costs but also exposes them to risks of technological blockades and supply disruptions. The supply-side bottlenecks place Chinese automakers in a relatively weak position within the supply chain, making it difficult for them to secure sufficient profit margins.

Thirdly, there is a mismatch between high sunk costs and lengthy return periods. The automotive industry is undergoing a paradigm shift from being mechanically defined to software-defined, and from being a single mode of transportation to an intelligent mobile terminal. This shift is not as simple as changing a powertrain; it requires automakers to completely reconstruct their entire research and development system, electronic and electrical architecture, and software ecosystem. This means automakers must simultaneously make massive capital expenditures in multiple high-tech areas such as battery technology, self-developed chips, advanced autonomous driving algorithms, and intelligent cockpits.

From an economic perspective, foundational and disruptive technological innovations inevitably come with extremely high trial-and-error costs and lengthy return periods. Current investments in intelligence are more akin to "building highways"—before a sufficient user base and mature business model are established, every line of code and every road test is purely a cost burn.

However, capital markets and competitive dynamics force automakers to invest, as this relates to their future survival. Huge research and development expenditures, heavy labor costs, and infrastructure amortization directly translate into substantial financial burdens on current financial statements. The severe mismatch between inputs and outputs over time places automakers under unimaginable profit pressure during the transition period.

Fourthly, breaking out of the dilemma has become the most critical issue facing every automaker. In the long run, to overcome the current profitability dilemma, Chinese automakers must undergo a profound self-revolution, with the core being a transformation from mere hardware manufacturers to technology ecosystem enterprises with technological premiums and strong supply chain integration capabilities. This is not just a shift in profit models but a reshaping of the corporate DNA.

On one hand, automakers must quickly abandon the single-mode dependency on hardware sales and achieve product upgrades through technological innovation, tapping into new revenue sources brought about by technological premiums. Future cars will no longer be just modes of transportation but mobile intelligent terminals and digital living spaces. The core of competition will shift from horsepower and fuel consumption to computing power, algorithms, and user experience. Automakers need to build their own software ecosystems, transforming one-time hardware sales into recurring software and service revenues through OTA upgrades, autonomous driving subscription services, and intelligent cockpit app stores. This will not only significantly enhance the lifetime value of each vehicle but also establish stronger and longer-lasting connections with users, fostering powerful brand loyalty.

On the other hand, strengthening supply chain integration capabilities and gaining control over core industrial chain advantages such as the "three electric systems" (battery, motor, electric control) is the fundamental path to regaining profit dominance. Automakers can no longer be satisfied with being "assembly plants" in the supply chain but must extend their value chain upstream. This can be achieved through various means such as self-research and self-production, strategic investments, and joint development. By establishing technological barriers and cost advantages in core areas such as batteries, motors, and electric control, automakers can not only effectively resist price increase pressures from upstream suppliers but also transform these core technologies into product competitiveness, thereby achieving higher brand premiums in the end market. When an automaker can simultaneously define products, control core technologies, and operate user ecosystems, it truly possesses the ability to navigate through cycles and sustain profitability.

Therefore, the decline in automakers' profits is a special case of market competition and also an important direction for current automakers to undergo transformation and change. The current strategy is for automakers to find ways to enhance their own competitive advantages to regain their profit high ground.

END

-

![]()

Qianwen Revolutionizes Taobao: Alibaba's Bold Self-Transformation

-

![]()

What’s the Real Story? China Leads in 5G Patents but Pays More in Royalties!

-

![]()

8 Auto Companies Unanimously Deny 'Summons for Talks' Rumors, but OTA Battery Locking is Real

-

![]()

China’s Premier AI Infrastructure Provider Launches IPO, with Zhipu AI and SenseTime as Key Backers

-

![]()

Have car prices gone up?

-

![]()

Samsung Withdraws, Joint Venture Automakers Brace for Battle

-

![]()

Nvidia Starts Adding Soap to the Bubble

-

![]()

Can Car Companies Not Generate Profits Solely from Vehicle Sales? What Challenges Do They Face?