Fully Electric Vehicles Finally Commanding High Prices

05/12 2026

05/12 2026

419

419

Lead

Introduction

The Fully Electric Era Accelerates

April's domestic automotive sales data revealed an industry split: while the overall market faced pressure, fully electric models gained strength, with sales of models like the Li Auto i6 and NIO ES8 continuing to rise.

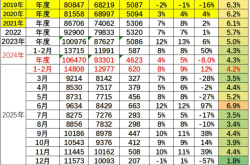

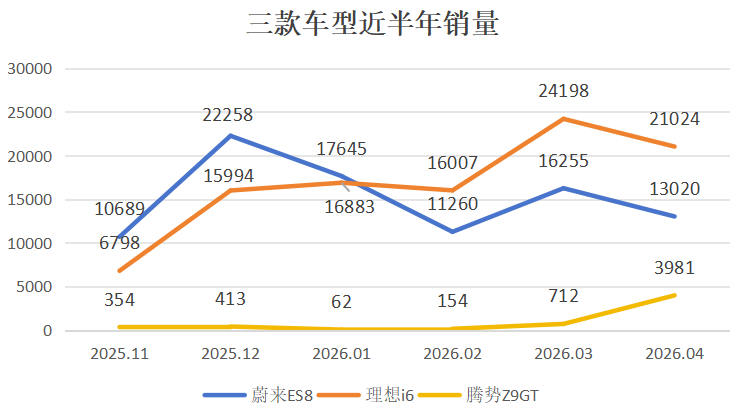

Although Li Auto's overall sales dipped below 40,000 units, the i6's monthly sales exceeded 20,000 units, firmly establishing itself in the mainstream fully electric market. The newly upgraded Denza Z9GT, leveraging second-generation blade batteries and flash-charging technology, reversed its sales trend, climbing to 3,900 units in April. Another high-end benchmark, the NIO ES8, achieved 13,000 monthly deliveries, with cumulative sales exceeding 100,000 units since launch, continuing to lead the 400,000-yuan fully electric SUV market.

In the past, while penetration rates for fully electric and new energy vehicles climbed, they were largely concentrated in the low-end market below 150,000 yuan. The mid-to-high-end market above 250,000 yuan saw limited fully electric penetration, with most sales coming from hybrid models like plug-in hybrids and extended-range EVs.

The simultaneous popularity of mid-to-high-end models like the Li Auto i6, Denza Z9GT, and NIO ES8—including the 500,000-yuan NIO ES9, which secured nearly 10,000 pre-orders in its first month—signals not just individual product successes but the irresistible advance of the fully electric era. This is backed by strong product capabilities and a robust charging ecosystem, reflecting profound industry shifts.

01 Li Auto, NIO, and Denza Break Open the Mid-to-High-End Fully Electric Market

'Why are the Li Auto i6, Denza Z9GT, and NIO ES8 selling so well?' This has been one of the hottest topics in the industry recently.

Take the Li Auto i6: as an all-around 'bucket' vehicle, it has few weaknesses in terms of product strength. Its self-developed VLA large model, dual-gun magic carpet suspension, 720km fully electric range, and comfortable, intelligent cabin experience ensure high standards in core areas like intelligent driving, handling, and ride comfort. Priced precisely at 250,000 yuan, it targets the mainstream consumer segment, offering a premium fully electric experience.

But beyond product strength, Li Auto's deep insight into the fully electric market is even more critical. Beyond brand, price, and product capabilities, the core factor influencing fully electric purchasing decisions is charging convenience. As one of the most consumer-aware automakers, Li Auto's supercharger station rollout has yielded visible results.

Long before the i8's launch, Li Auto accelerated its national supercharger station network. By 2025, it aims to have 4,000 supercharger stations. By December 2025, with 20,000 Li Auto supercharging piles in place, it will become the automaker with the most supercharging piles nationwide.

For a brand newly transitioning to fully electric on a large scale, this rollout speed is remarkable. After launch, the i6's deliveries were initially limited by production capacity. Only after ramping up output at its Changzhou plant did it truly take off, surpassing 20,000 monthly sales.

Now consider the NIO ES8: after a comprehensive product upgrade, its starting price dropped to 400,000 yuan, further reduced to 300,000 yuan under NIO's Battery-as-a-Service (BaaS) rental scheme. While monthly rental fees apply, this model lowers the entry barrier, making the high-end fully electric SUV accessible to more users. Meanwhile, NIO's long-accumulated battery-swapping network has matured, reducing range anxiety.

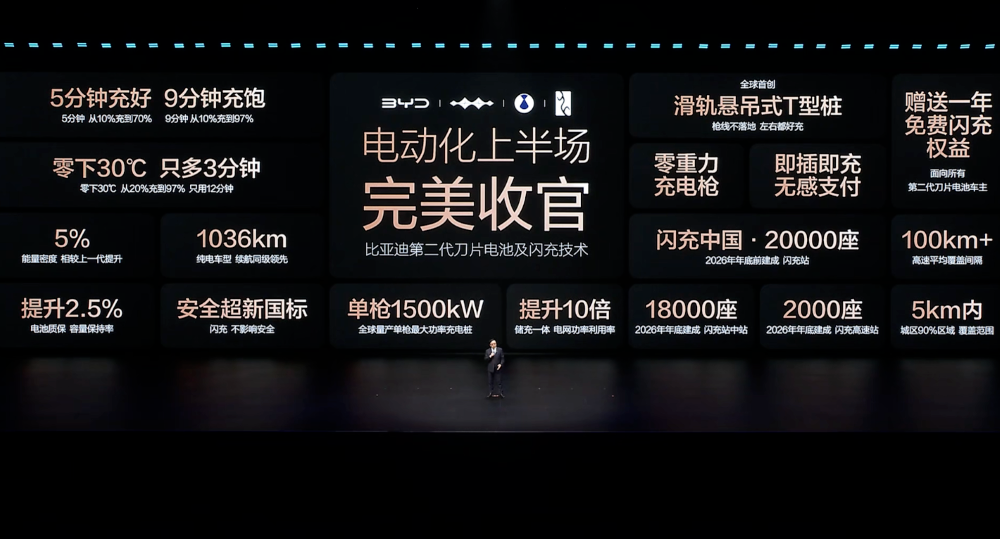

Unlike new forces, industry giant BYD leveraged technological innovations like second-generation blade batteries and flash-charging technology, along with cost-effectiveness, to address charging and range anxiety, successfully entering the mid-to-high-end fully electric market.

Before its March refresh, the Denza Z9GT's monthly sales languished. Equipped with second-generation blade batteries, its range exceeded 1,000 kilometers, and with flash-charging support, pure electric orders surpassed plug-in hybrid versions, nearing 80% initially—a stark contrast to the first-generation model's hybrid dominance. In April, the Z9GT's sales surged to 3,981 units, with daily production reaching 260 vehicles.

Beyond the Z9GT, the Fangchengbao Titan 7 EV flash-charging version is also poised for launch. Market feedback shows that since its late-April debut, pre-orders have exceeded expectations, with a delivery peak expected in May, shifting Fangchengbao's sales mix away from hybrids.

Unlike new forces, BYD, an early entrant, has cultivated a loyal customer base now entering a new replacement cycle. Faced with significant breakthroughs in brand batteries and charging technology, they are more likely to switch to fully electric models. Not to mention, compared to hybrids' dual systems, fully electric vehicles offer cheaper maintenance.

Not just BYD and the aforementioned companies, several recently launched multi-powertrain models have shown a overwhelming dominance of pure electric orders. According to Dongfeng Nissan, the Nissan NX8, launched in April, had a pure electric-to-extended-range order ratio of 2:1 initially. In March, the pure electric versions of the Seres M8 and M9 outsold their extended-range counterparts, reaching a 6:4 ratio. Earlier, the all-new Leapmotor C11 saw 80% pure electric pre-orders, with extended-range models accounting for just 20%.

02 The Fully Electric Era Accelerates: Large Five-Seaters Succeed Large Six-Seaters

More noteworthy than these individual models is the market trend they reflect. The simultaneous popularity of multiple mid-to-high-end fully electric models is not an isolated event but a microcosm of the irresistible advance of the fully electric era.

The acceleration of the fully electric era is now unstoppable.

CPCA data shows that in April, China's passenger vehicle retail sales reached 1.4 million units, a significant decline from March. Against this backdrop, fully electric models demonstrated strong resilience, with 579,000 units sold—unchanged from March—but their penetration rate surged to 41%, a sharp increase from March.

The accelerated transition to fully electric vehicles is driven by multiple factors.

On one hand, sustained high fuel prices are prompting consumers to reevaluate ownership costs. In January and February, influenced by purchase tax adjustments, the Spring Festival holiday, and price changes, the growth pace of new energy vehicle penetration slowed. Following multiple fuel price hikes in March, penetration rates for fully electric and new energy vehicles rose accordingly.

Although charging pile electricity prices have adjusted this year, most fast-charging piles cost no more than 2 yuan per kWh, with even lower prices in lower-tier cities, where charging costs consistently remain below 0.6 yuan. While service fees are higher in first-tier cities like Shanghai, the overall cost advantage of charging for daily travel remains solid.

The number of charging piles is also growing rapidly. Automakers and charging pile operators are accelerating station construction. By late March this year, China had 21.48 million electric vehicle charging piles, up 46.9% year-on-year. BYD, which just launched its second-generation blade batteries, plans to build 20,000 flash-charging stations this year, ensuring average distances of 3 kilometers in first- and second-tier cities, 5 kilometers in third- and fourth-tier cities, and 6 kilometers in fifth- and sixth-tier cities between stations.

Take our office building as an example: when new energy vehicles first emerged years ago, there were no charging facilities. Now, multiple charging stations from brands like Didi and Haohan have moved in, along with numerous slow-charging piles, significantly improving charging convenience and reducing range anxiety. Once drivers experience the ease of charging, they rarely return to traditional vehicles.

The rapid improvement of infrastructure has cleared the biggest obstacle to fully electric vehicle adoption, directly reflecting changes in market dynamics. Brands that accurately grasp consumer needs are now reaping the rewards.

As one of the most market-savvy automakers, Li Auto's founder, Li Xiang, has consistently demonstrated accurate predictions about industry trends and the ability to create hit models. The launch of the Li Auto L9 kicked off the trend for large six-seaters and extended-range vehicles. Initially, the industry was skeptical about extended-range routes, but Li Auto's success prompted more brands to explore this segment. Large six-seaters became wildly popular, covering price ranges from 150,000 to 500,000 yuan, with brands like Galaxy, Leitao, NIO, Seres, and Zeekr all launching bestsellers.

In recent months alone, the NIO ES9, SAIC Volkswagen ID.ERA 9X, Wuling Huajing S, IM LS8, Wey V9X, Yijing X9, XPeng GX, and Li Auto L9 Livis have all launched or started pre-sales, with large six-seaters ubiquitous at the Beijing Auto Show, nearly every brand featuring a similarly specced model at their booth's center. While manufacturers are enthusiastic, consumer attitudes are shifting.

In March this year, only two large six-seater models—the NIO ES8 and Zeekr 9X—sold over 10,000 units, with many others falling short of 1,000 monthly sales. Coupled with demographic changes, consumers are growing tired of homogeneous three-row large six-seaters, which are now seen as impractical. The heyday of large six-seaters is ending rapidly.

Taking their place are fully electric large five-seaters, exemplified by the Li Auto i6.

In the sub-200,000-yuan market, fully electric penetration is already high, with models like the Geely Xingyuan and BYD Dolphin selling well. The economy fully electric model is well-established in this segment. However, above 250,000 yuan, there has been a lack of a true mass-market hit fully electric model.

With the accelerated arrival of the fully electric era and changing consumer perceptions, flagship models like the Li Auto i6 are validating the market potential of this price band. Meticulously refined product strength, combined with the sustained release of fully electric era dividends, is prying open a critical gap in the mid-to-high-end fully electric market.

Compared to the large six-seater market, the fully electric large five-seater segment is far broader. With a market capacity exceeding one million units, it can accommodate multiple leading players coexisting and thriving, rather than rapidly descending into homogeneous competition like large six-seaters.

Of course, competition is intensifying, and the fully electric large five-seater landscape is not yet set. The market newly warmed by the Li Auto i6 will soon see strong entrants. The Fangchengbao Titan 7 EV flash-charging version has launched to high enthusiasm, and the Leitao L80 is set to debut, with its lower BaaS pricing posing a direct threat to the i6. Whether the i6 can hold its market position will depend on its production ramp-up speed, brand loyalty, and the continued expansion of its supercharging network.

Now consider NIO. The success of the NIO ES8 is the result of William Li's years of commitment to fully electric and battery-swapping technologies. From achieving profitability in Q4 last year to the current dual-model strategy with the ES8 and ES9, NIO has finally embraced the fully electric era.

Despite the popularity of extended-range vehicles and widespread skepticism, NIO persisted with its battery-swapping layout and high-end fully electric positioning—a challenging path. But with the accelerated pace of the fully electric era, NIO's accumulated battery-swapping network, brand positioning, and user community are now translating into tangible market advantages.

From the Li Auto i6 to the NIO ES8, from the Denza Z9GT to the Fangchengbao Titan 7, fully electric models are flourishing across the 200,000–400,000-yuan mid-to-high-end market. The fully electric market is achieving breakthroughs across all price bands, with technological iteration, cost advantages, policy support, and a maturing charging ecosystem jointly fueling the accelerated advance of the fully electric era.

In April, amid overall market pressure, fully electric penetration rose instead of fell, signaling the irreversible trend of fully electric vehicles replacing fuel-powered ones.

Editor-in-Charge: Du Yuxin Editor: He Zengrong

THE END

-

![]()

Qianwen Revolutionizes Taobao: Alibaba's Bold Self-Transformation

-

![]()

What’s the Real Story? China Leads in 5G Patents but Pays More in Royalties!

-

![]()

8 Auto Companies Unanimously Deny 'Summons for Talks' Rumors, but OTA Battery Locking is Real

-

![]()

China’s Premier AI Infrastructure Provider Launches IPO, with Zhipu AI and SenseTime as Key Backers

-

![]()

Have car prices gone up?

-

![]()

Samsung Withdraws, Joint Venture Automakers Brace for Battle

-

![]()

Nvidia Starts Adding Soap to the Bubble

-

![]()

Can Car Companies Not Generate Profits Solely from Vehicle Sales? What Challenges Do They Face?