Huolala's Seventh Bid for a Hong Kong IPO: How Will It Leverage New Energy and Driverless Delivery After Achieving $2.1 Billion in Annual Revenue?

05/27 2026

05/27 2026

509

509

Source: Zhiche Technology, Public Information

In late April, Huolala (listed entity Lala Technology), a same-city freight platform, once again submitted its prospectus to the Hong Kong Stock Exchange. This marks its seventh attempt to go public on the Hong Kong Stock Exchange over the past three years.

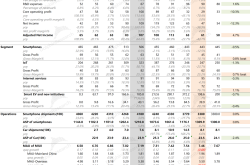

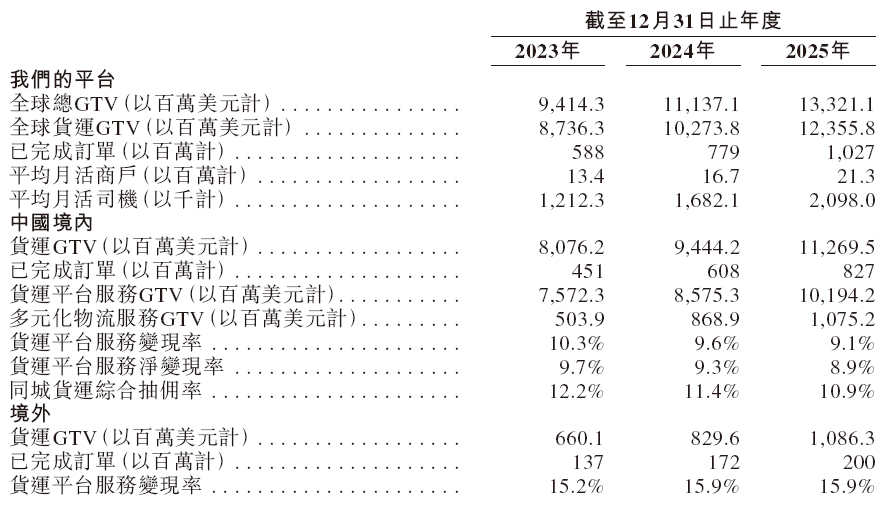

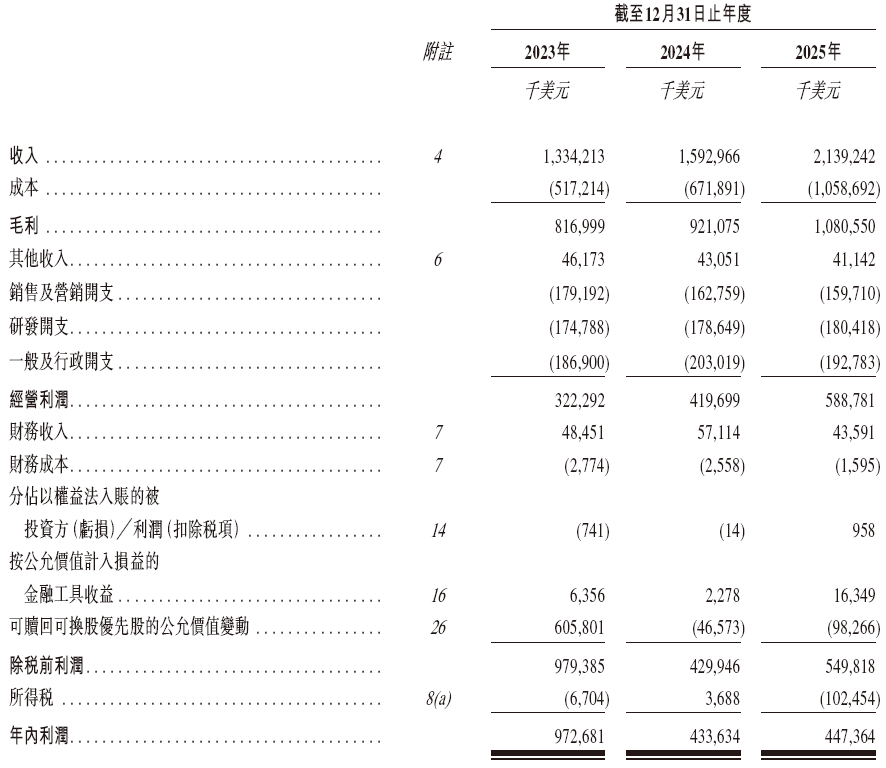

As competition intensifies and several rivals exit the market, Huolala, which initially operated as an asset-light platform, has now firmly established itself as an industry leader. In 2025, Huolala's global Gross Transaction Value (GTV) reached $13.32 billion, up 19.6% year-on-year. Annual revenue hit $2.139 billion, a 34.3% increase. Total orders surpassed 1 billion, with an average of 21.3 million monthly active merchants and around 2.1 million monthly active drivers.

However, despite these impressive revenue figures, Huolala has failed to provide sufficient certainty to capital markets, particularly to Hong Kong stock regulators who place significant emphasis on business predictability.

According to the prospectus, Huolala's overall gross margin stood at just 50.5% in 2025, a significant drop of over 10 percentage points from the 61.2% high in 2023.

After years of capital endurance, Huolala's path seems to be narrowing: its scale is expanding, but profits are thinning; commitments are increasing, while regulatory compliance thresholds are lowering.

More importantly, the platform company, which once profited handsomely from "commissions + membership fees," now has to lower its stance to engage in heavy-duty enterprise logistics, less-than-truckload (LTL) freight, and even custom new energy trucks, as well as launch driverless delivery fleets. This shift from "light" to "heavy" is a path no one willingly takes, but Huolala has no choice.

"Three Consecutive Declines" in Commission Rates and Shrinking Core Profit Pools

Huolala's core business model, which once relied on "information matching" and platform commissions as an asset-light route, is now under pressure.

As a digital platform connecting merchants and drivers, Huolala previously did not own large numbers of vehicles or fleets. Its consistently high gross margins, exceeding 60%, coupled with mature monetization paths through membership fees and commissions, once attracted significant capital investment. However, the benefits of this approach are now being eroded.

On one hand, regulatory shifts and public pressure are to blame. Between 2021 and 2025, Huolala was repeatedly summoned by regulators at all levels, with concerns evolving from initially "high commissions" to "algorithm-driven price suppression" and "driver rights." By 2025, Huolala's comprehensive commission rate for same-city freight in China had fallen for two consecutive years to 10.9% from 12.2% in 2023. The platform's overall monetization rate also dropped for three consecutive years to 9.1%.

On the other hand, the competitive landscape is changing. The same-city freight sector not only faces sustained pressure from established rivals like Didi Delivery and Kuaigou Taxi but also welcomes cross-border entrants—Manbang Group's Yunmanman made a major push into same-city freight by acquiring Shengsheng Huiche. After securing about $1.7 billion in financing, Manbang fully entered Huolala's core market under the Yunmanman brand. Additionally, new players like Halo Delivery and JD Logistics are also eyeing opportunities, focusing on niche scenarios or innovating with models like "zero commissions + social security" to challenge Huolala's market base.

Under dual pressure, Huolala was forced to make strategic choices in 2024 and 2025: it lowered comprehensive rates and platform commissions to stabilize its driver base.

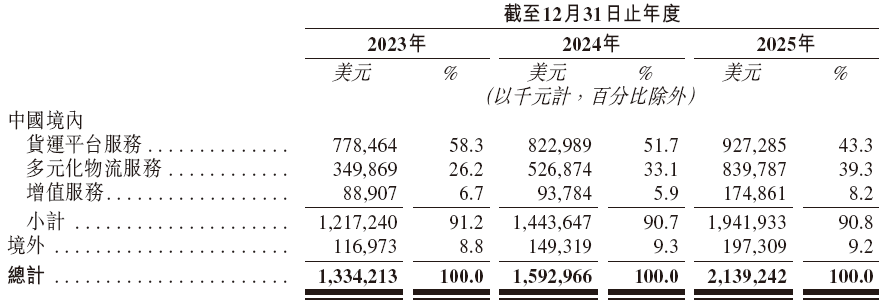

But this adjustment had direct consequences. Although the gross margin of Huolala's core profit driver—freight platform services—remained high at around 81%, its monetization rate continued to decline. Meanwhile, its share of total revenue dropped from 58.3% in 2023 to 43.3%.

Huolala is not unaware of these issues. Clinging to the commission model would only weaken its business foundation—especially as capital exit paths become increasingly uncertain.

This reflects a core contradiction in business logic: sacrificing per-order commissions for higher market share and industry standing, yet struggling to avoid the reality of increased volume without proportional revenue growth—a key profitability metric valued by capital markets.

The Cost of Diversification: From High to Medium-Low Margins

In response to capital market skepticism, Huolala's narrative to investors revolves around two main directions: overseas markets and diversified businesses.

Financial data supports this focus. In 2025, Huolala's freight platform service monetization rate in overseas markets reached 15.9%, nearly 7 percentage points higher than in China. Overseas freight GTV hit $1.09 billion, up 31% year-on-year, accounting for 8.2% of total GTV.

However, overseas markets still account for less than 10% of the total. Rapidly navigating multi-country regulations, driver recruitment, and transportation capacity expansion is no easy feat.

Now consider the more closely watched diversified logistics segment (LTL, moving, enterprise services). In 2025, this sector's GTV in China reached $1.08 billion, up 23.7% year-on-year, accounting for 8.1% of total GTV. However, its gross margin stood at just around 15.9%, a stark contrast to the over 81% margin in freight platform services.

When low-margin diversified businesses rapidly increased their share of total revenue from 26.2% in 2023 to nearly 40%, Huolala's overall gross margin decline becomes understandable.

This raises a more fundamental question: How low a gross margin can Huolala tolerate?

In comparison, competitors like Didi Delivery and Yunmanman are also pursuing diversification, but their margins were never high to begin with, so they don't face the same transition from "high-margin platform" to "medium-low-margin logistics operator." Huolala, however, must confront capital market revaluation due to "revenue growth without profit growth."

For Huolala, diversification is indeed a necessary direction for enterprise services and supply chain extension. But if this comes at the cost of such a rapid profit margin dilution, how far this path can go ultimately depends on the attitude of the Hong Kong Stock Exchange.

Technological Transformation: From New Energy Customization to Driverless Delivery

If commissions and diversification represent Huolala's financial narrative, then new energy and autonomous driving define its future technological story. In this area, Huolala's strategic layout is more proactive than outsiders perceive—but the contradictions are equally complex.

New Energy: Bridging Platform Drivers and Automakers

New energy commercial vehicles are entering a dual window of policy and market opportunity. Industry forecasts suggest new energy logistics vehicle sales could hit 800,000 units by 2026. In early 2026, the Ministry of Transport explicitly proposed accelerating the large-scale adoption of new energy commercial vehicles, extending national subsidies for "trade-in" programs, with maximum subsidies of $19,800 for replacing National IV diesel trucks with new energy heavy trucks.

Freight platforms wield more influence in this chain than many realize.

Since 2024, Huolala has mandated increasing proportions of new energy vehicles among newly added vehicles in first-tier cities like Beijing, Shanghai, Guangzhou, and Shenzhen. The platform uses algorithms to grant operational advantages to new energy vehicles: higher order acceptance rates, priority in recommending high-quality orders, and technical service fees 10-15% lower than those for fuel vehicles. Meanwhile, Huolala's "Green Journey Initiative" has integrated numerous charging stations and poles, with annual charging volumes reaching hundreds of millions of kWh.

Huolala's platform rules directly influence what orders drivers receive and how much they earn. New energy vehicles enjoy priority in order acceptance and recommendations, with technical service fees 10-15% lower than for fuel vehicles. These mechanisms substantially guide drivers toward new energy models when selecting vehicles.

A deeper layer of strategy involves moving upstream. Huolala's wholly-owned Duola Automobile has partnered with Lingshi Automobile, a subsidiary of Guangxi Automobile Group, to jointly develop and launch new energy micro and small truck models like "Duola 3.8" and "Duola Small Cargo." These vehicles are not arbitrarily designed but are reverse-customized based on the massive daily order data from Huolala's platform.

Huolala's logic is clear: instead of letting drivers purchase "good enough" vehicles on the market, the platform should directly customize vehicles that best match its transportation capacity needs. This "scenario-driven manufacturing" model mirrors how ride-hailing platforms deeply customize dedicated vehicles. It may become one of Huolala's most compelling long-term strategies—transforming it from merely an order allocation platform to quietly reshaping demand structures in the commercial vehicle market.

Autonomous Driving: At the Crossroads of Pilot Projects and Scalability

Compared to the incremental innovation of new energy, autonomous driving represents the future of "transportation capacity."

In April 2026, Huolala and Baixiniu, an L4 autonomous driving Robovan company, officially launched large-scale commercial operations of driverless freight in Linyi, Shandong. Baixiniu RX integrated into Huolala's platform, providing instant driverless delivery services to C-end users, micro and small merchants, and wholesale trade stores. The initial fleet plans to rapidly expand to 200 units, operating 24/7. Baixiniu revealed that its transportation capacity cooperation with both Shunfeng and Huolala will exceed 10,000 units within three years.

Huolala is not alone in pushing forward. Didi Delivery has deployed over 1,200 driverless delivery vehicles in Qingdao in partnership with Neolix, while Kuaigou Taxi has teamed up with Jushi Intelligence to deploy a thousand-unit driverless delivery fleet in Xuzhou. Nearly all leading platforms are simultaneously scaling up driverless delivery.

This means that if widely adopted, driverless delivery could fundamentally alter freight platforms' cost structures—platforms would no longer rely solely on large, volatile driver pools but could own predictable, round-the-clock transportation capacity resources.

But this is precisely where Huolala's contradictions lie.

On one hand, Huolala's business model fundamentally relies on its 2.1 million drivers. They are both transportation capacity providers and direct contributors to platform commissions. If driverless vehicles massively replace manual delivery, conflicts between driver rights and stable transportation capacity will become acute. Currently, driverless vehicles mainly operate in standardized, small-batch, short-distance delivery scenarios, while non-standard tasks like large cargo handling and home installation services are unlikely to be automated shortly. However, in high-frequency, low-price orders, driverless vehicles may increasingly encroach on drivers' order opportunities—a trend that may be hard to reverse.

On the other hand, autonomous driving is an extremely capital-intensive sector. Huolala is in the midst of an IPO sprint with tight cash flow. As of late 2025, the company had net liabilities of $1.888 billion and short-term net current liabilities as high as $2.090 billion. Whether through self-research or partnerships, large-scale investments in autonomous driving fleets will further strain its already tight cash flow.

From the perspective of autonomous driving industry progression, Huolala's current driverless delivery operations in Linyi resemble a localized stress test—accumulating data and validating business models within a limited area. The real turning point may come in three to five years: when driverless delivery costs decline further, road access policies become more open, and technology maturity reaches new heights. By then, Huolala's ability to transition from "platform matching" to "autonomous transportation capacity" will determine its final position in this sector.

RMB 33.7 Billion Valuation Adjustment Mechanism Looms, IPO Window Closes in Less Than Six Months

Dissecting Huolala's story across technology, operations, and vehicle models reveals some logics worthy of long-term strategic layout. However, capital markets care less about stories and more about certainty and exit paths.

Huolala's real challenge lies not in its commercial capabilities but in the RMB 33.7 billion valuation adjustment mechanism agreement behind its three-year, seven-attempted Hong Kong IPO failures.

As of December 31, 2025, the company's redeemable convertible preferred shares amounted to US$4.8179 billion (approximately RMB 33.7 billion). According to disclosures, if a qualified listing is not completed by November 8, 2026, the redemption rights will be reinstated.

The clock is ticking for Huolala, with less than half a year remaining on its timeline.

This is no trivial matter. As of 2025, Huolala's recorded cash reserves stood at US$1.822 billion, while its net liabilities reached US$1.888 billion—nearly matching figures. Should the earnout redemption clause be activated, the company would confront substantial cash outflow challenges.

The primary market has been instrumental in propelling this unicorn, now valued at US$12.965 billion. However, with repeated misses on potential listing windows, the patience of early investors has been severely tested by the relentless cycle of 'filing—lapsing—refiling.'

The Hong Kong Stock Exchange acknowledges Huolala's scale but casts doubt on its commercial resilience. The company's prolonged reliance on commissions and membership fees, coupled with sustained pressure on core profitability metrics, is compounded by regulatory uncertainties. Specifically, over half of its compliant transportation capacity operates within freight safety oversight gray areas.

Since last year, Huolala has taken proactive steps to reduce fees and concessions, gradually lowering the commission cap for drivers. Nevertheless, the platform's underlying profitability pressures persist unabated. This scenario raises the capital markets' primary concern: once subsidies are withdrawn or external support weakens, will Huolala's over 2 million drivers defect to rival platforms?

Seven filings, seven periods of anticipation. The question of whether Huolala can secure approval from the Hong Kong Stock Exchange before the deadline looms large, with an answer imminent.

- End -

Disclaimer:

Articles marked 'Source: XXX (non-Zhiche Technology)' in this official account are reproduced from other media sources. The purpose of reproduction is to disseminate and share information more widely and does not imply this platform's endorsement of the views expressed or assumption of responsibility for their authenticity. Copyright remains with the original authors. Please contact us for removal if any infringement is identified.

-

Computing Power Crisis: Four Major Forces Enter Token Service Market

-

![]()

Agnes AI Releases Three Core Multimodal Models: Text, Image, and Video

-

![]()

Tesla Abandoned Radar Five Years Ago; Now, China’s Market is on the Verge of Delivering Its Verdict

-

![]()

Chinese Automobile Design Steps into a New Phase of Global Aesthetic Dialogue

-

![]()

Huolala's Seventh Bid for a Hong Kong IPO: How Will It Leverage New Energy and Driverless Delivery After Achieving $2.1 Billion in Annual Revenue?

-

![]()

When It Comes to Electric Car Manufacturing, Even Ferrari Must Learn from China

-

![]()

Is the Ultra-Luxury Electric Vehicle a Misguided Concept?

-

![]()

Xiaomi: Facing Decline and Doubting the Future? The Tide Has Turned