Xiaomi: Facing Decline and Doubting the Future? The Tide Has Turned

05/27 2026

05/27 2026

404

404

On the evening of May 26, 2026, Beijing time, after the market closed in Hong Kong, Xiaomi Group (1810.HK) unveiled its financial report for the first quarter of 2026 (ending March 2026). Here are the key takeaways:

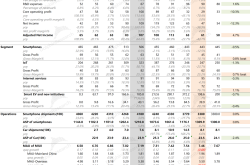

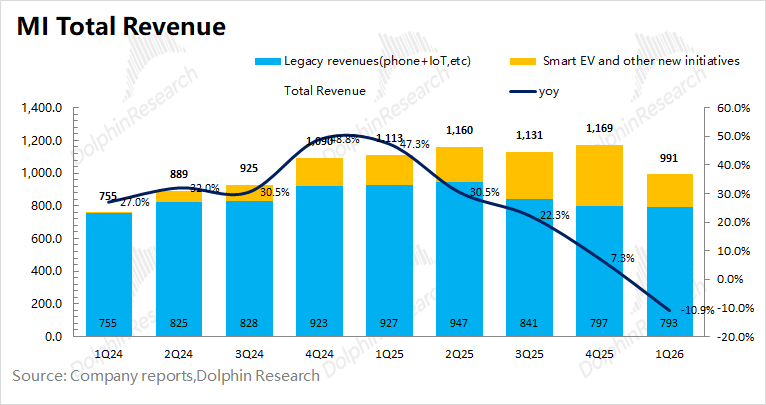

1. Overall Performance: Revenue reached RMB 99.1 billion, a year-on-year decrease of 11%. The decline in this quarter was primarily attributed to the drag from the smartphone and other business segments, with the company's traditional business (smartphones x AIoT) seeing a 14.5% year-on-year revenue drop.

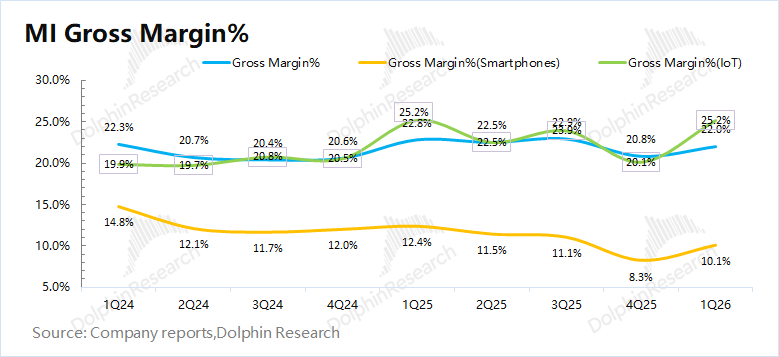

The gross profit margin for the quarter stood at 22%, down 0.8 percentage points year-on-year, mainly influenced by the year-on-year decline in gross profit margins for both the smartphone and automotive businesses.

2. Automotive Business: Revenue from automotive-related operations this quarter amounted to RMB 19.86 billion, generally meeting expectations. The company delivered 81,000 vehicles, with the average selling price (ASP) per vehicle dropping to RMB 235,000.

The decline in sales volume was influenced by factors such as the discontinuation of the old SU7 model and production capacity adjustments. The drop in ASP was attributed to the impact of purchase tax subsidies and an increased proportion of lower-ASP spot sales.

The gross profit margin for the automotive business slipped to 20.1% this quarter, close to market expectations of 20.5%, primarily affected by the decline in ASP. This included the impact of Xiaomi's subsidies for purchase taxes and the sale of a portion of lower-priced spot vehicles. Due to the further decline in gross profit margin, Dolphin Research estimates that Xiaomi's core operating profit from the automotive business fell into a loss of RMB 3.1 billion this quarter.

Impact of Purchase Tax Subsidies: Xiaomi previously announced that orders locked before 24:00 on November 30, 2025, with vehicle invoicing and delivery in 2026 due to production or transportation reasons, would receive subsidies for the difference through reductions in the final vehicle payment. For instance, the impact of purchase tax subsidies on the ASP of a single YU7 unit is approximately RMB 12,000.

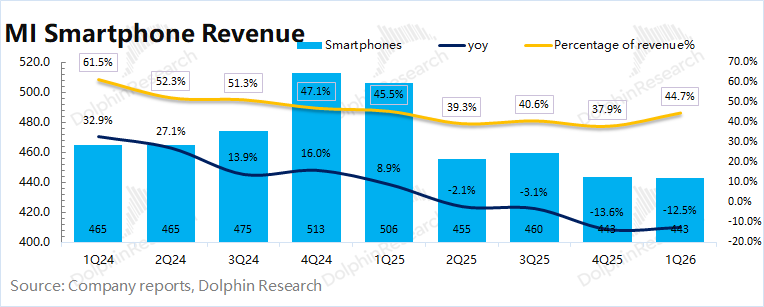

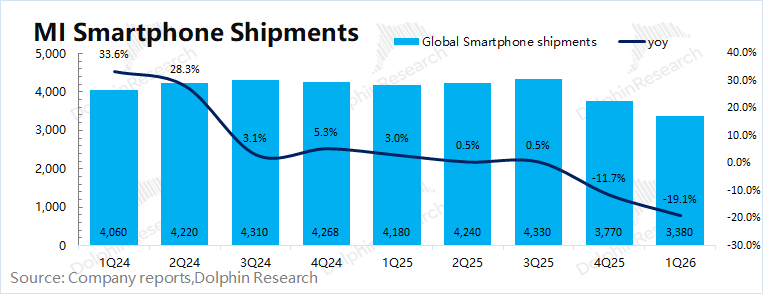

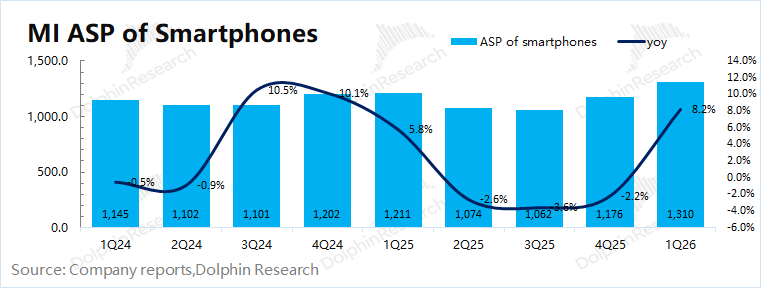

3. Smartphones: Revenue was RMB 44.3 billion, a year-on-year decrease of 12.5%, in line with market expectations of RMB 44.5 billion. Xiaomi's smartphone shipments this quarter were down 19% year-on-year, while the ASP per smartphone increased by 8% year-on-year.

By Market: Xiaomi's smartphone shipments in the domestic market were down 34.6% year-on-year, while shipments in overseas markets decreased by 12% year-on-year. The storage shortage directly impacted smartphone shipments. Considering the sequential rebound in the company's smartphone gross profit margin, Dolphin Research believes that Xiaomi prioritized allocating storage to higher-priced models, driving up the ASP.

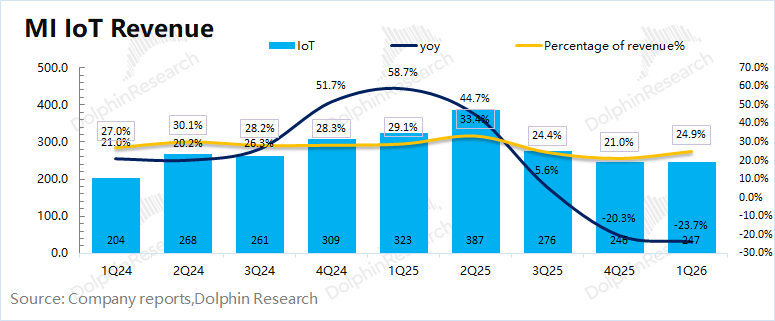

4. IoT: Revenue was RMB 24.7 billion, a year-on-year decrease of 24%, close to market expectations of RMB 25 billion, mainly affected by the reduction in national subsidies and storage issues, especially the greater impact on the company's major appliance business due to national subsidy policies (some product subsidies may have reached RMB 1,000-2,000).

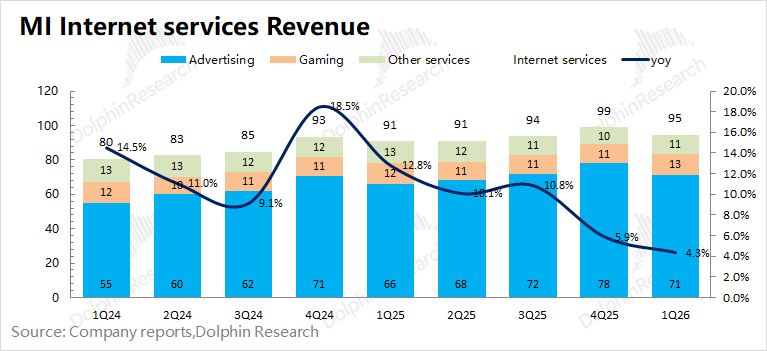

5. Internet Services: Revenue was RMB 9.5 billion, up 4% year-on-year, in line with market expectations of RMB 9.5 billion, with growth mainly driven by the advertising business. The number of MIUI users increased by 4% year-on-year, while the ARPU value increased slightly by 0.5% year-on-year.

By Region: Overseas internet revenue was RMB 2.97 billion this quarter, while domestic internet revenue was approximately RMB 6.5 billion. The number of MIUI users in China continued to grow this quarter, while the number of overseas MIUI users declined slightly.

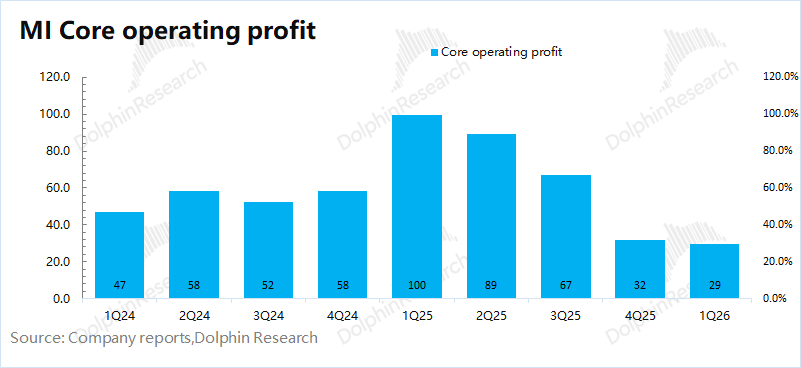

6. Profitability: Core profit was RMB 2.9 billion, with adjusted net profit at RMB 6.1 billion. The core profit from Xiaomi's traditional business was approximately RMB 6 billion, while the automotive business incurred a loss of RMB 3.1 billion this quarter.

Given the storage shortage, the company prioritized allocating storage to models with higher ASPs, leading to a sequential rebound in gross profit margin and core profit from traditional businesses. The automotive business returned to a loss this quarter due to the impact of purchase tax subsidies and declining sales volume.

Dolphin Research's Overall View: Stock Price Halved, but Fundamentals Not as Dire as Imagined

Xiaomi's financial report for this quarter generally aligns with market expectations. The year-on-year decline in the company's revenue this quarter mainly stems from the drag of the smartphone and IoT businesses within the traditional business segment.

From the data performance this quarter, Xiaomi still faces significant operational pressure. For example, smartphones and IoT continue to experience double-digit year-on-year declines, while the growth rate and gross profit margin of the automotive business have also significantly decreased.

Xiaomi's stock price has declined from HK$60 to around HK$30, reflecting the adverse impacts of storage shortages, sluggish smartphone sales, and the "cooling off" of Xiaomi's automotive business. For the stock price to rebound, the company needs to demonstrate improvements in its operations, with a focus on the progress of its automotive, smartphone, and IoT businesses:

1) Automotive Business: Annual Target of 550,000 Vehicles

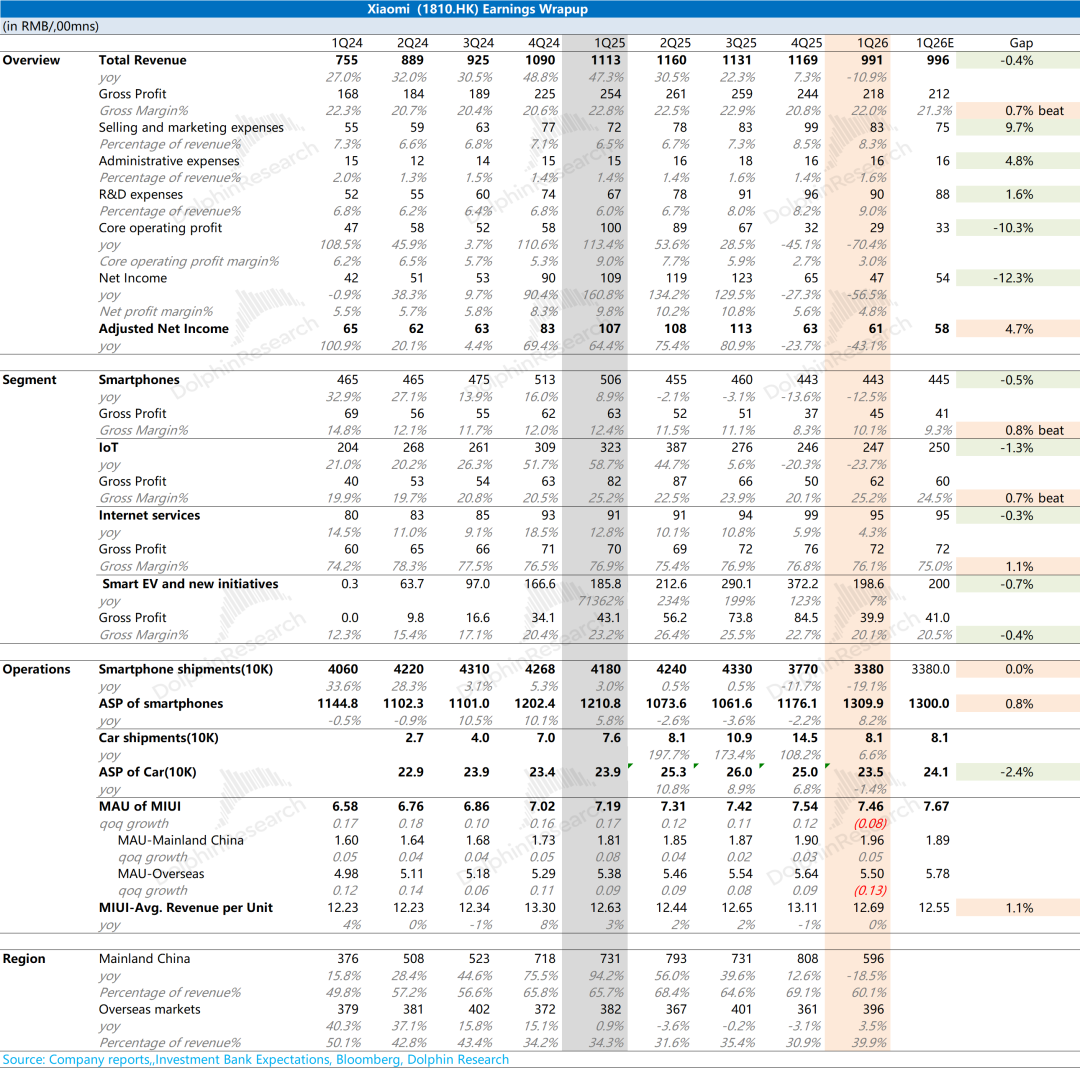

Xiaomi's automotive business shipped 81,000 vehicles in the first quarter of 2026, a significant sequential decline of 44%. The discontinuation of the old SU7 model and the launch of the new SU7 during the quarter affected production capacity to some extent. Driven by the new SU7, the company's sales volume returned to over 30,000 vehicles in April.

Although Xiaomi's automotive monthly sales volume rebounded after the launch of the new SU7 model, the change in the company's "delivery cycle" suggests that this is just a "transitional product" and not as "hot" as the previous YU7.

The current YU7 delivery cycle has decreased to less than 10 weeks, indicating that the backlog of orders has largely been cleared. The delivery cycle for the new SU7 has lengthened slightly after the "May Day holiday," but the current delivery cycle of around 3 months is still relatively normal.

The company's management previously set an annual sales target of 550,000 vehicles for the automotive business. With only 81,000 vehicles sold in the first quarter, this means sales in the remaining three quarters must reach 470,000 vehicles (i.e., over 155,000 vehicles per quarter), which is challenging. After the digestion of the YU7 "order pool," Xiaomi's automotive business has shifted from "supply-constrained" to "demand-driven," with sales volume directly affected by "order demand."

b) Traditional Business (Smartphones x AIoT): Storage Pressure Persists, Gross Profit Margin Stabilizes at Low Levels.

① Smartphone and IoT Businesses: Both businesses still experienced significant declines this quarter, mainly affected by factors such as rising storage prices and tightening national subsidies.

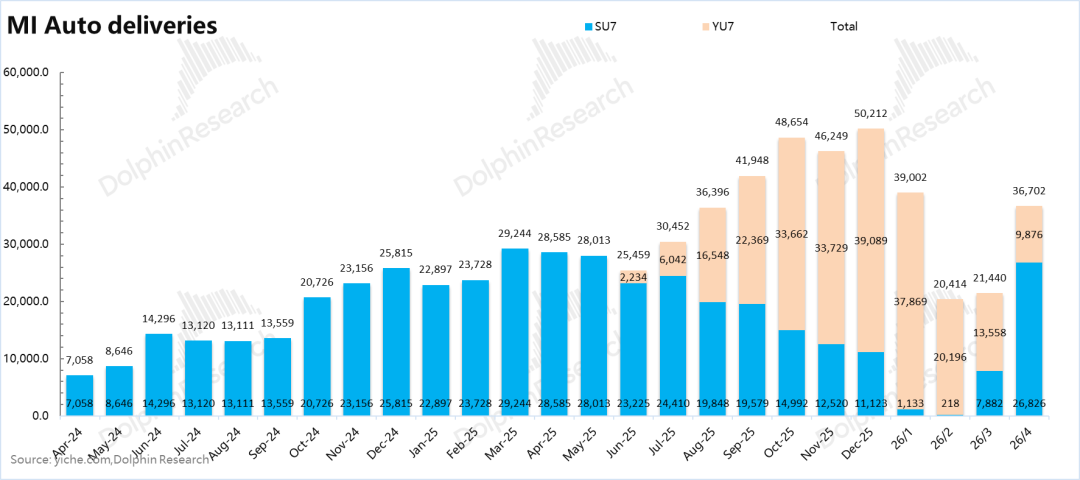

Xiaomi's smartphone shipments in the Chinese market declined significantly by 34% this quarter, mainly due to adverse factors such as Apple's "more for less" strategy with the iPhone 17 series and storage shortages. During the same period, Apple's smartphone shipments in the Chinese market increased by 34% year-on-year (while the overall market declined by 3.6% year-on-year).

Qualcomm's management mentioned in exchanges that "channel inventory clearance will ease, the Chinese Android smartphone market will bottom out in the next quarter, and return to sequential growth in the second half of the year."

Current demand in the smartphone market has not yet rebounded, but the impact of storage shortages has already been reflected in the company's declining stock price and fully digested by the market. Combined with the gross profit margins of smartphones and IoT, even with current storage price increases, the gross profit margins of the company's traditional hardware have stabilized and stopped declining, making it difficult for operational conditions to worsen further.

Overall, Xiaomi still faces significant pressure in its traditional segments (smartphones and IoT), with gross profit margins remaining at relatively low levels. However, the positive aspect is that hardware gross profit margins rebounded sequentially this quarter. As for the automotive business, the company has set an annual guidance of 550,000 vehicles, which is currently the main focus. Attention should be paid to the performance of the company's subsequent new vehicle launches.

Under the impact of multiple pressures, Xiaomi's stock price has "halved" from its relative high of HK$60.

Under a relatively pessimistic scenario (Xiaomi's smartphone revenue declines by 9%, IoT experiences a slight year-on-year decline), traditional businesses will see a single-digit year-on-year decline, while the automotive business will meet the company's target of 550,000 vehicles but experience declines in ASP and gross profit margin. It is estimated that Xiaomi's core operating profit after tax from traditional businesses in 2026 will be approximately RMB 20 billion, down 16% year-on-year; revenue from the automotive business will be approximately RMB 140 billion, up 32% year-on-year.

Under the above scenario, the key is to achieve the company management's guidance of 550,000 vehicles in the automotive business. If the guidance is difficult to meet or is revised downward subsequently, it may further depress the company's stock price. As for the traditional segments, a relatively pessimistic scenario has largely been factored into the stock price, and subsequent demand recovery could drive performance upward.

The following is a detailed analysis:

I. Overall Performance: Revenue Declines Again, Gross Profit Margin Stabilizes

With the addition of the automotive business, Xiaomi's financial reports now include two new categories in addition to the previous "Smartphones x AIoT": "Automotive and Innovation Businesses."

Xiaomi's decision to disclose the "Automotive and Innovation Businesses" separately reflects the company's emphasis on the automotive business. The company's market capitalization previously broke the trillion-dollar ceiling, mainly due to expectations surrounding the automotive business.

1.1 Revenue

Xiaomi Group reported total revenue of RMB 99.1 billion in the first quarter of 2026, down 11% year-on-year, generally in line with market expectations of RMB 99.6 billion. The decline this quarter was mainly due to the drag from the smartphone and IoT businesses.

1) Original Business - Smartphones x AIoT (Traditional Business): Revenue was RMB 79.3 billion, down 14.5% year-on-year. Hardware business performance remained "poor," with smartphone revenue down 12.5% year-on-year and IoT revenue down 24% year-on-year.

2) New Businesses - Xiaomi's smart automotive and other new businesses generated revenue of RMB 19.86 billion this quarter, up 7% year-on-year, mainly affected by the delivery of the YU7, discontinuation of the old SU7 model, and the preparation period for the new SU7.

1.2 Gross Profit Margin

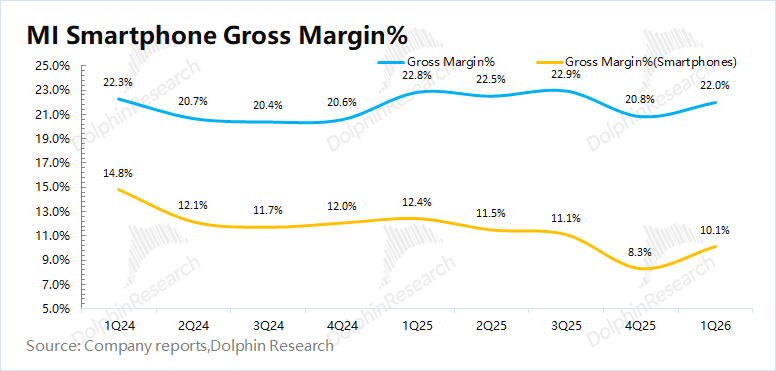

Xiaomi Group reported a gross profit margin of 22% in the first quarter of 2026, better than market expectations of 21.3%. The gross profit margins for smartphones and IoT businesses declined sequentially this quarter, while the gross profit margin for the automotive business continued to decrease.

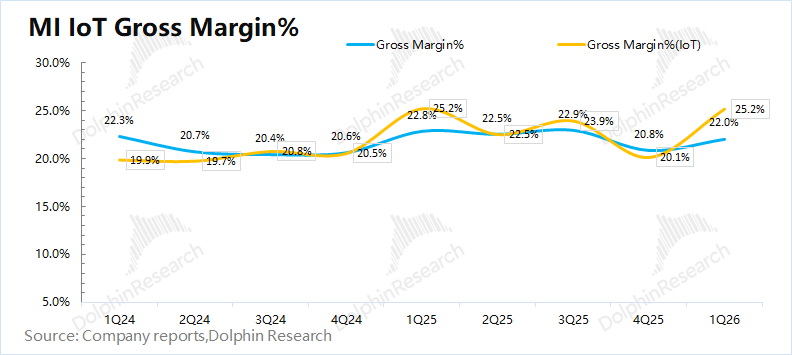

a) The gross profit margin for Xiaomi's old businesses was 22.5%, up 2.5 percentage points sequentially, mainly due to the company prioritizing the allocation of storage to products with higher ASPs. The smartphone business's gross profit margin rebounded sequentially to 10.1% this quarter, while the IoT gross profit margin rebounded to 25.2%.

The company's other businesses within the traditional business segment continued to incur a gross loss of RMB 80 million this quarter, including services such as air conditioner installation. If this gross loss is included in the IoT business, the true gross profit margin of the IoT business should be around 24.9%.

2) The gross profit margin for new businesses such as automotive was 20.1%, close to market expectations of 20.5%. The sequential decline in the automotive business's gross profit margin this quarter was mainly due to Xiaomi's subsidies for purchase taxes and the sale of a portion of lower-priced spot vehicles.

Impact of Purchase Tax Subsidies: Xiaomi previously announced that orders locked before 24:00 on November 30, 2025, with vehicle invoicing and delivery in 2026 due to production or transportation reasons, would receive subsidies for the difference through reductions in the final vehicle payment. Taking the YU7 as an example, the impact of purchase tax subsidies on the ASP of a single YU7 unit is approximately RMB 12,000.

II. Automotive Business: Annual Target of 550,000 Vehicles

The automotive business generated RMB 19 billion in revenue, which, combined with revenue from peripheral automotive businesses, totaled RMB 19.86 billion, generally in line with market expectations of RMB 20 billion.

With 81,000 vehicles sold, the ASP per vehicle this quarter was RMB 235,000, down RMB 15,000 sequentially, mainly due to factors such as Xiaomi's purchase tax subsidies and the sale of some lower-priced spot vehicles. Dolphin Research estimates that the purchase

III. Mobile Phone Segment: Prioritizing Price Protection Over Sales Volume

In the first quarter of 2026, Xiaomi's smartphone division reported revenue of RMB 44.3 billion, marking a 12.5% year-over-year decline. This downturn was primarily attributed to storage component shortages and intensified market competition.

Dolphin Research provides a detailed analysis of Xiaomi's smartphone business, focusing on sales volume and pricing:

Sales Volume: In this quarter, Xiaomi shipped 33.8 million smartphones, representing a 19% decrease from the previous year. The Chinese market witnessed a particularly sharp decline of 34.6%.

Market Breakdown: (1) In China, Xiaomi's smartphone market share fell to 12.6%, an 8% year-over-year decrease, primarily due to storage shortages and heightened competition. (2) Overseas, Xiaomi's smartphone shipments declined by 12% year-over-year, with its market share decreasing by 0.8%.

Pricing: The average selling price (ASP) for smartphones in this quarter reached RMB 1,310, an 8% increase from the previous year. Dolphin Research notes that the ASP recovery was not driven by robust demand (as sales volumes dropped significantly) but rather by the company's strategy of allocating storage to higher-priced models.

Gross Profit Margin: The smartphone division's gross profit margin stood at 10.1%, up 1.8 percentage points sequentially. This improvement was primarily due to the ASP recovery. Despite sluggish downstream demand, Xiaomi prioritized "ASP > gross profit margin > sales volume" amid storage shortages.

IV. IoT Segment: Impact of Reduced Government Subsidies

In the first quarter of 2026, Xiaomi's IoT division generated revenue of RMB 24.7 billion, a 23.7% year-over-year decrease. This decline was primarily due to reduced government subsidies and storage issues, with the company's major appliance business being particularly affected by subsidy cuts (some product subsidies reached RMB 1,000-2,000).

Gross Profit Margin: The IoT division's gross profit margin reached 25.2%, up 5.1 percentage points sequentially. This improvement was driven by higher gross profit margins for certain consumer lifestyle products in overseas markets and the recovery of gross profit margins for smart major appliances and tablets in mainland China.

V. Internet Services: Growth Slows Due to Smartphone Shipment Decline

In the first quarter of 2026, Xiaomi's internet services division reported revenue of RMB 9.5 billion, a 4% year-over-year increase. The primary growth driver was advertising:

a) Advertising Services: Revenue reached RMB 7.1 billion, a 7% year-over-year increase. However, the growth rate slowed significantly compared to previous double-digit increases.

This slowdown is because Xiaomi's core advertising scenarios—app distribution and pre-installed apps—act as distribution fees that most major app developers must pay. Advertising for pre-installed apps, in particular, is nearly guaranteed profit. Since pre-installation revenue is directly tied to smartphone shipments, the significant decline in shipments directly impacted pre-installed app revenue.

b) Value-Added Services: This category includes game distribution, Xiaomi's e-commerce platform Youpin, and Xiaomi Finance. Revenue remained roughly flat year-over-year at approximately RMB 2.4 billion, indicating stability.

Overall, the long-term revenue logic for internet services still depends on hardware shipments. In Xiaomi's reclassified revenue model, this segment is generally categorized under Legacy business. Only by integrating software and hardware can Xiaomi, as a smartphone manufacturer, sustain its internet monetization strategy. Given the current decline in smartphone shipments, pressure on the growth rate of this business is expected.

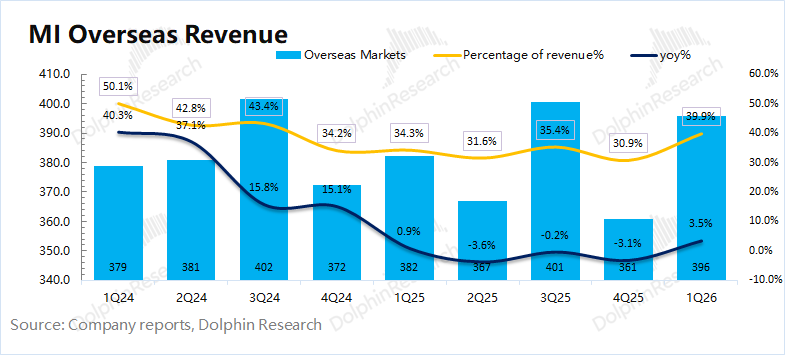

VI. Overseas Markets: Growth in Hardware and Software

In the first quarter of 2026, Xiaomi's overseas revenue reached RMB 39.6 billion, a 3.5% year-over-year increase. Amid a sluggish domestic market, the proportion of overseas revenue rebounded to around 40%.

Further Breakdown: Xiaomi's overseas internet services business grew by 10% this quarter, reaching RMB 3 billion. Meanwhile, overseas hardware revenue increased by 3% year-over-year, returning to growth and reflecting a recovery in demand for overseas IoT and related markets.

VII. Profitability: Traditional Businesses Recover, Auto Business Posts Losses

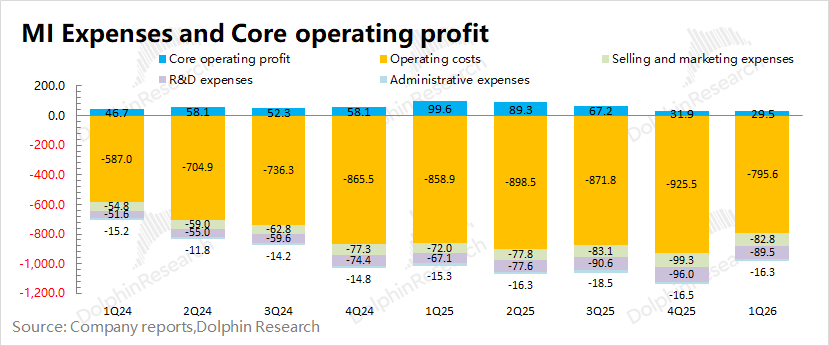

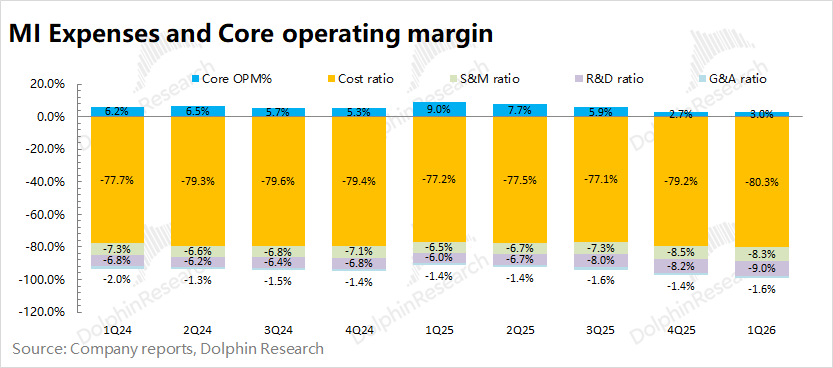

In the first quarter of 2026, Xiaomi's total operating expenses across three categories amounted to RMB 18.9 billion, with the expense ratio increasing to 19%. Expenses for innovative businesses, such as automotive and AI, reached RMB 7.1 billion, remaining around RMB 7 billion.

Excluding the automotive business, traditional businesses' operating expenses were approximately RMB 11.76 billion, a 10.5% year-over-year increase. The operating expense ratio for traditional businesses declined to 14.8%, primarily due to increased R&D spending. Xiaomi currently employs 26,000 R&D personnel, with growth over eight consecutive quarters.

Adjusted net profit for the first quarter of 2026 was RMB 6.1 billion. However, Dolphin Research disagrees with Xiaomi's method of adjusting net profit, as it does not exclude financial income or dividend incomes from invested companies. Even if sustainable, these do not represent the company's core business and fail to reflect long-term profitability.

Overall, Dolphin Research focuses more on core operating profit (revenue - cost - three expenses), as it more accurately reflects the company's ability to sustain profitability in its core business operations.

The company's actual core operating profit this quarter was RMB 2.9 billion, with a core operating profit margin of 3%. The decline in core profit was primarily due to reduced revenue, while the sequential increase in core profit margin was driven by the recovery in hardware gross profit margins.

Further Breakdown: The core operating profit for traditional businesses this quarter was approximately RMB 6.05 billion (an increase of RMB 3.9 billion sequentially), while the core operating profit loss for the automotive business was RMB 3.1 billion (a decrease of RMB 4.1 billion sequentially).

- END -

// Reprint Authorization

This article is an original piece by Dolphin Research. Reproduction requires authorization.

// Disclaimer and General Disclosure

This report is intended for general comprehensive data purposes, designed for general reading and data reference by users of Dolphin Research and its affiliated institutions. It does not consider the specific investment objectives, investment product preferences, risk tolerance, financial status, or special needs of any individual receiving this report. Investors must consult with independent professional advisors before making investment decisions based on this report. Any person making investment decisions using or referring to the content or information in this report assumes all risks. Dolphin Research shall not be liable for any direct or indirect responsibilities or losses that may arise from the use of the data contained in this report. The information and data in this report are based on publicly available sources and are for reference purposes only. Dolphin Research strives to ensure, but does not guarantee, the reliability, accuracy, and completeness of the information and data.

The information or viewpoints mentioned in this report shall not, under any jurisdiction, be regarded or construed as an offer to sell securities or an invitation to buy or sell securities, nor shall they constitute recommendations, inquiries, or endorsements of relevant securities or related financial instruments. The information, tools, and data in this report are not intended for distribution to or use by individuals or residents in jurisdictions where such distribution, publication, provision, or use contradicts applicable laws or regulations or subjects Dolphin Research and/or its subsidiaries or affiliated companies to registration or licensing requirements in those jurisdictions.

This report only reflects the personal viewpoints, insights, and analytical methods of the relevant creators and does not represent the stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, and the copyright is solely owned by Dolphin Research. No institution or individual may, without the prior written consent of Dolphin Research, (i) produce, copy, duplicate, reproduce, forward, or create any form of copies or reproductions in any manner, and/or (ii) directly or indirectly redistribute or transfer them to other unauthorized persons. Dolphin Research reserves all related rights.

-

![]()

Is the Ultra-Luxury Electric Vehicle a Misguided Concept?

-

![]()

Xiaomi: Facing Decline and Doubting the Future? The Tide Has Turned

-

![]()

European Cars, Made in China

-

![]()

"My Parents Have Been Driving Their Gasoline Car for Over a Decade, Yet My Electric Vehicle Needs Replacing After Just 4 Years"

-

![]()

Qwen: A Driving Force Behind Alibaba Cloud’s Evolution

-

![]()

SAIC’s Milestone of 100 Million Vehicles: A Testament to SAIC Volkswagen’s Contribution!

-

![]()

New Energy Online Taxis: A Smooth Ride, Except for the Non-Stop Vomiting

-

![]()

Alipay Unveils the Globe’s Pioneering Token-Based Payment Service: Will the AI Era Revolutionize How We Pay?