The domestic auto sales have declined so much that dealers who can't hold on have started closing stores en masse

06/08 2026

06/08 2026

452

452

Lead

Introduction

This year's dealer ecosystem is destined (doomed) to be a tumultuous one.

Last week, a rumor that "a dealer group had a physical altercation with an automaker, resulting in the manufacturer's leader being hospitalized" continued to ferment within the automotive circle. Despite the automaker brand in question promptly issuing a denial, the dealer remained silent, sparking speculation both within and outside the industry.

Where there's smoke, there's fire. In fact, this controversy serves as a magnifying glass, fully exposing the current tense state of the automotive dealer ecosystem. Amidst profound adjustments in the domestic auto market, accelerating retail declines, and persistently low consumer sentiment, conflicts between automakers and dealers are no longer isolated cases. In particular, inventory pressure has become a concentrated reflection of industry-wide supply-demand imbalances, collapsing profitability, and deteriorating manufacturer-dealer relations.

Nowadays, when most companies release their monthly sales reports, they generally provide impressive production and sales figures. However, behind these eye-catching (eye-catching) data lies reliance on overseas exports as a "fig leaf," with significant declines in domestic retail sales becoming a widespread phenomenon. Coupled with the aggressive targets set by major brands over the past two years, which led to frenzied channel expansion, the market pie is shrinking while the number of stores vying for a slice is increasing.

Furthermore, multiple pressures such as price inversion, high inventory levels, tightening regulations, and imbalanced business policies have collectively plunged domestic dealer groups into a survival winter. According to a survey by the Automobile Circulation Association, over 70% of dealers have explicitly expressed their demands, hoping that automakers will lower unreasonable sales targets, simplify evaluation rules, shorten rebate cycles, and increase subsidies. The core demands of dealers have shifted from the past focus on "boosting sales and capturing market share" to a complete focus on "ensuring survival and weathering difficulties."

The automotive circulation track in 2026 is destined (doomed) to be an even more brutal elimination race, with a large number of stores teetering on the brink of profitability and loss, and a massive wave of store closures already on the horizon.

01 Exports Prop Up Appearances, Domestic Sales Hide Winter Chills

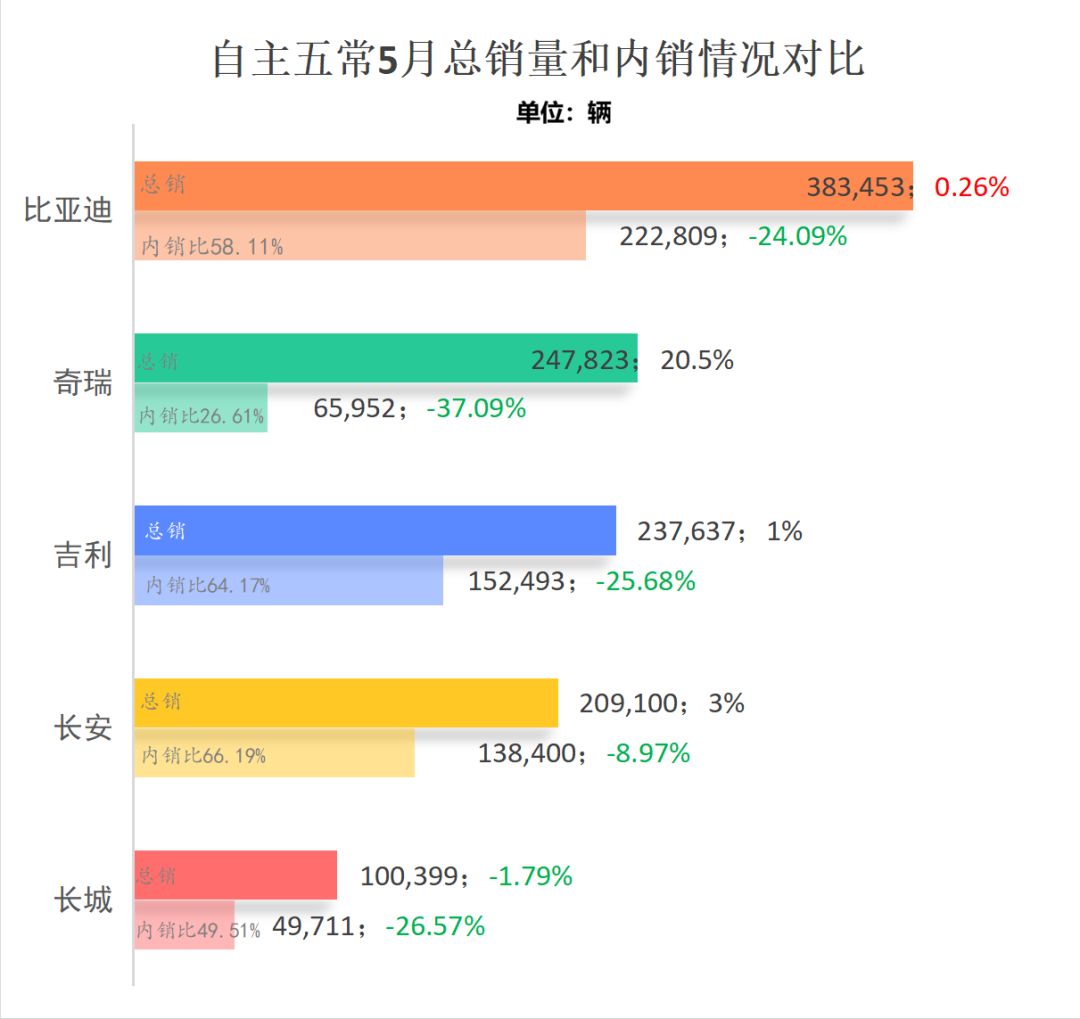

Leading brands best reflect market trends and situations. Looking at the major players—BYD, Chery, Geely, Changan, and Great Wall—in May 2026, their overall volumes remain stable, with some automakers even achieving year-on-year growth. However, breaking down the domestic and export sales structures reveals the truth: the impressive overall data is highly dependent on overseas market performance, while the domestic terminal market has already turned icy.

Specifically, BYD's overall sales in May were robust, but domestic sales were only 220,000 units, down 24% year-on-year; Chery's domestic sales were 65,000 units, with a year-on-year decline of 37%; Geely's domestic sales were 150,000 units, down 25% year-on-year; and Great Wall's domestic sales were 49,000 units, down 26% year-on-year.

Combining this with overall market data, domestic passenger vehicle sales are down about 20% year-on-year this year, indicating a general weakening in market demand. For automakers, sustained growth in overseas exports has effectively offset the downturn in the domestic market, allowing them to maintain a respectable production and sales report. However, for dealers rooted in the domestic market and largely dependent on domestic customer traffic for survival, without the buffer of overseas markets, they can only face the reality of plummeting orders and customer traffic.

All the ill effects are the result of actions taken over the past two years. At that time, major leading brands, in a bid to achieve sales targets and vie for industry rankings, planned a frenzied network expansion.

According to cross-verified data from multiple sources, BYD, aiming to hit an annual sales target of 5 million units, has deployed over 4,000 dealerships nationwide; Geely's Galaxy brand, which sold 2 million new energy vehicles in 37 months, has leveraged this trend to help Geely aim for a return to the top spot among domestic automakers, with Geely Automobile Group's four brands deploying over 2,000 dealerships; Chery has deep cultivation (delved deep into) the entire market, with Chery, Jetour, Exeed, and iCAR stores exceeding 3,000 in scale; although Great Wall's sales lag behind these leading companies, its offline network is maintained at around 2,000 stores.

On one hand, the domestic market has shrunk by 20% overall, with leading brands' domestic sales generally declining by 20-30%. On the other hand, the number of channels has increased significantly over the past two years, with multiple stores in the same city and dense regional networks becoming the norm. With a fixed or even shrinking market capacity and a sustained growth (continuously growing) number of stores, the sales volume per store is being continuously diluted.

The National Dealer Conference that concluded at the end of last month, along with a series of survey data released by the China Automobile Dealers Association, paints a complete picture of the current difficult situation for channels. Over 80% of dealers report low consumer car purchase (car-buying) willingness and a strong wait-and-see attitude, with both store customer traffic and leads sharply declining. Amidst multiple intersecting issues, dealers have long bid farewell to the era of meager profits, with widespread losses becoming the industry's main theme.

High inventory levels are the first challenge faced by all stores. In April, the domestic auto dealer inventory alert index reached 62.1%, remaining above the threshold line, with 17 mainstream brands having an inventory depth exceeding two months. Persistently high inventory not only occupies a large amount of space but also generates substantial capital interest, continuously eroding profits.

More fatal than inventory is the normalization of new car price inversion. Data shows that 82% of dealers currently experience price inversion to varying degrees, with 51.6% experiencing an inversion amplitude (margin) exceeding 15%. This means that dealers' vehicle acquisition costs are higher than the terminal selling price, resulting in losses from the moment a new car enters the store. Even first-tier luxury brands like BBA are experiencing bicycle (per-vehicle) losses of 20,000-30,000 yuan.

This has created a bizarre vicious cycle in the industry: not making an effort to sell cars leads to inventory backlogs and rising capital costs, resulting in expanding losses; yet, selling cars aggressively results in direct losses on each vehicle, with higher sales volumes leading to greater overall losses. In 2026, the total revenue of China's top 100 auto dealers was 1,721.227 billion yuan, down 8.82% year-on-year; total sales volume was 7.8832 million units, a slight decline of 1.7%. The industry is experiencing a typical double hit to revenue and gross profit.

For most dealers, the new car business has completely transformed from a traditional profit center to a loss-incurring tool for driving customer traffic, forcing dealers to rely on after-sales and additional services to barely make up for losses. Meanwhile, the zero-kilometer used car business, which helped many dealers meet KPIs and supplement profits in the past two years, has been regulated this year and become a formal export business for manufacturers, eliminating this "profit cow" and further exacerbating the difficulties for already struggling stores.

Additionally, many automakers, under pressure from sales KPIs, have imposed unreasonable business policies, further intensifying opposition between manufacturers and dealers. In 2025, dealer overall satisfaction with automakers was only 60.8 points, a historical low. Dealers generally report that current rebate rules are vague, accounting standards are opaque, and rebate fulfillment cycles are as long as two to three months, tying up a significant amount of working capital for extended periods.

When visiting a large leading brand dealer in the west earlier this year, the author truly felt the industry's seismic changes. At its peak, this single store could sell 6,000 vehicles annually, achieving stable profitability through new car gross profit, after-sales maintenance, and accident business; now, following the automaker's channel planning, it has been split into six stores, with the combined sales volume of the six stores failing to reach 6,000 units, resulting in a significant decline in single-store efficiency. Currently, the store's new car business operates at break-even or even at a loss, traditional after-sales revenue has sharply declined, and profits are highly dependent on insurance rebates, creating an extremely singular profit structure and making the store's risk resistance capacity highly fragile.

02 Wave of Store Closures: Is the Dealer Model Failing?

Elon Musk once said that partnering with dealers would not end well. However, in the context of China's vast and regionally dispersed market, dealers remain an indispensable model for auto manufacturers. Even though many new energy vehicle startups initially followed Tesla's lead and adopted a direct sales model, they have gradually or partially reverted to the dealer model and ecosystem, with no exceptions from Xpeng to HiPhi.

However, the dismal conditions in this year's auto market, with sustained losses and intense internal competition, are bound to intensify the wave of store closures. Data shows that in the second half of last year, the average loss-making rate among auto dealers nationwide exceeded 50%, with the 4S dealership network shrinking by about 500 stores net for the year, marking a second consecutive year of negative growth.

Among them, the contraction of fuel vehicle networks for joint ventures and luxury brands has been most pronounced, with a 5.7%-5.8% reduction in related 4S store locations in 2025. The negative impacts of large-scale store closures are chain-like, not only disrupting automakers' channel layouts but also undermining consumer trust in brands.

The industry is saying that it needs to actively embrace new energy vehicles, but the many uncertainties surrounding new energy have also put many authorized dealers in a dilemma. Currently, new energy brands adopt a mix of direct sales and authorized models. In automakers' direct sales systems, sales profits are unrelated to authorized stores; under pure authorized models, the sales service fees for new energy models are already meager, and stores face stringent evaluation metrics while after-sales profitability continues to weaken. This has led many investors to adopt a wait-and-see attitude towards the new energy authorization model.

Looking at the entire industry, the dealer group has clearly polarized. Profit-making groups that can maintain operations and achieve positive returns have generally completed business reconstruction. They mostly rely on mature customer operation systems, full-chain used car businesses, new energy transition capabilities, and refined management to create diversified profit models, no longer solely dependent on new car sales volume. On the other hand, dealers mired in losses mostly adhere to traditional business approaches, highly dependent on the new car business, and step by step fall into systemic losses amidst the price inversion environment.

Therefore, the current dilemma faced by dealers is no longer an individual issue of poor single-store operation or backward management but rather a concentrated eruption of industry-wide problems such as severe market supply-demand imbalances, outdated channel models, and unfair business rules. To emerge from the winter, both automakers and dealers need a revolution.

Automakers must first abandon illusions and discard the "sales volume and market share only" mindset, facing up to the real trends and capacity of the domestic market. On one hand, they should optimize channel layouts, close inefficient stores in the same city, and curb disorderly expansion and vicious price wars; on the other hand, they should adjust business policies, eliminate vague and bundled rebate rules, directly link rebates to wholesale sales, and shorten payment cycles.

For dealers, with domestic sales plummeting and revenue and profits shrinking, the primary task is to "stop the bleeding and survive." The Automobile Circulation Association suggests that dealers need to prioritize asset streamlining, leverage digital tools to reduce costs and increase efficiency, and improve cash flow conditions. Simultaneously, they should actively reconstruct their profit models, break free from dependence on new car sales, and focus on new businesses such as used cars, customized services, and car owner community operations, transitioning from mere "car sales stores" to comprehensive mobility service providers.

The author believes that automakers and dealers are inherently interdependent, with channels representing the last mile for brands to reach users. The survival state of dealers directly determines the vitality of the entire industry. Nowadays, issues such as declining domestic auto market sales, price inversion, high inventory levels, and channel overcapacity are intertwined, making short-term pain unavoidable.

In the coming period, industry reshuffling will continue to intensify. Small and medium-sized dealers lacking funds, without diversified business support, and adhering to traditional models will be the first to be cleared out by the market, leading to mergers and reorganizations among dealer stores and small groups. Meanwhile, leading dealer groups that actively transform, operate with refinement, and possess comprehensive service capabilities will gradually gain a foothold.

From another perspective, this winter, while impacting the domestic dealer industry, is also an opportunity to stimulate their upgrade and make them stronger.

Editor-in-Chief: Cao Jiadong Editor: Chen Xinnan

THE END

-

![]()

"3D Vision Pioneer" Grapples with Internal Strife: $120 Million in Share Reductions Offset by $147 Million Private Placement

-

![]()

The domestic auto sales have declined so much that dealers who can't hold on have started closing stores en masse

-

![]()

Five Brands Team Up with Huawei: Will Dongfeng Still Pursue Independent R&D?

-

![]()

The Large Six-Seater SUV Market: Overhyped and Overrated

-

![]()

The Smart Driving Blue Light: Urgent Need for Rectification

-

![]()

Would OpenAI Be Fascinated by Anthropic’s Concepts?

-

![]()

Tencent: Few Great Queries, Yet Possessing the Ultimate One

-

Does DingTalk Need Revolutionaries or Reformers?