New Energy Vehicles Dominate: Penetration Rate Soars Past 60%, Fuel Vehicles Vanish from Top 10; Mid-Year Report Reveals Zero for New Energy in Some Metrics

06/12 2026

06/12 2026

540

540

In a mere six months, new energy vehicles have conquered the entire mainstream household automotive market.

As 2026 reaches its midpoint, China's automotive market has unfolded its 'mid-year report card' with striking clarity for the industry. Despite a persistently sluggish overall market, structural divisions have reached unprecedented levels.

New energy vehicle penetration has skyrocketed past 60% in one fell swoop, leaving traditional fuel vehicles struggling even to make the top 10 list. Exports have emerged as the 'lifeline' for several major domestic automakers to maintain their performance. With the brand elimination race well underway, the gap between frontrunners and laggards is widening faster than anticipated. This is not a fleeting market fluctuation but a definitive milestone marking the industry's deep dive into transformation.

In essence, the new landscape of China's auto market has largely been shaped based on the first half's market performance.

Breaking the 'Oil-Electric Equilibrium'

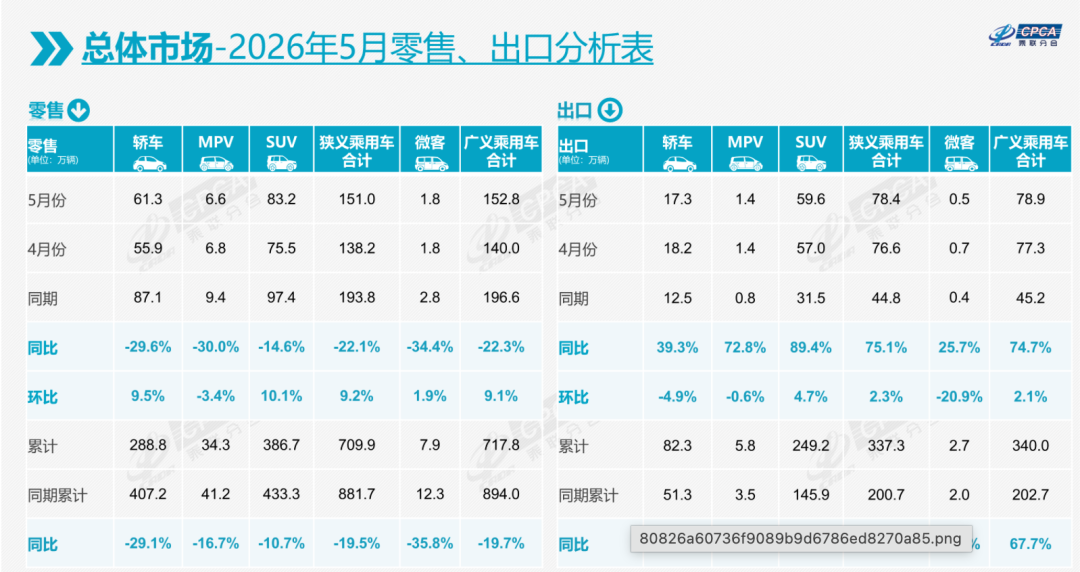

The automotive market in the first half of 2026 faced greater pressures than initially anticipated at the year's outset. Data from the China Passenger Car Association (CPCA) reveals that 7.15 million passenger cars were sold nationwide in the first five months, marking a 19% year-on-year decline. In May alone, sales of 1.545 million units represented a 20% year-on-year drop, marking the second consecutive month of declines exceeding 20%.

This downturn can be attributed to two primary factors: short-term 'anticipatory spending' and a broader 'cooling effect' in the economic environment.

At the end of last year, the impending expiration of new energy vehicle purchase tax exemptions prompted many potential buyers to rush their purchases, effectively 'pre-spending' demand for the first half of this year. Additionally, subsidies in the first quarter of last year inflated the sales base, naturally amplifying this year's year-on-year decline.

On the other hand, consumer confidence is gradually recovering, leading to more cautious spending habits. Data from the National Bureau of Statistics confirms this trend, showing a 10.6% year-on-year decline in automotive consumption in the first four months, significantly lagging behind overall retail sales growth.

However, there are signs of a rebound. Retail sales in May increased by 12% from April, and while the dealer inventory warning index has not yet fallen below the threshold, it has declined for two consecutive months, indicating a gradual thawing of the market from the first quarter's deep freeze. Coupled with the upcoming implementation of trade-in policies in the second half of the year, the industry's expectation of a 'decline followed by a rise' is gradually being validated. Short-term fluctuations cannot derail the overall trajectory of industry transformation.

The most striking change in the first half of this year is the much faster-than-expected penetration of new energy vehicles, completely disrupting the previous 'oil-electric equilibrium'.

In May, the retail penetration rate of new energy vehicles surged to 62.9%, a new all-time high. In other words, more than six out of every ten new vehicles sold are now new energy models. Looking at the top 10 sales list, which best reflects market strength, seven spots were occupied by fuel vehicles in January, reduced to just one by April, and by early June, the last fuel vehicle had been squeezed out.

New energy vehicles have captured the entire mainstream household market in just half a year.

The performance of different players reveals even more pronounced divergences. In the first half of this year, the growth logic of traditional domestic automakers has fundamentally shifted, with exports becoming the core driver of overall sales, while the domestic market generally faces downward pressure.

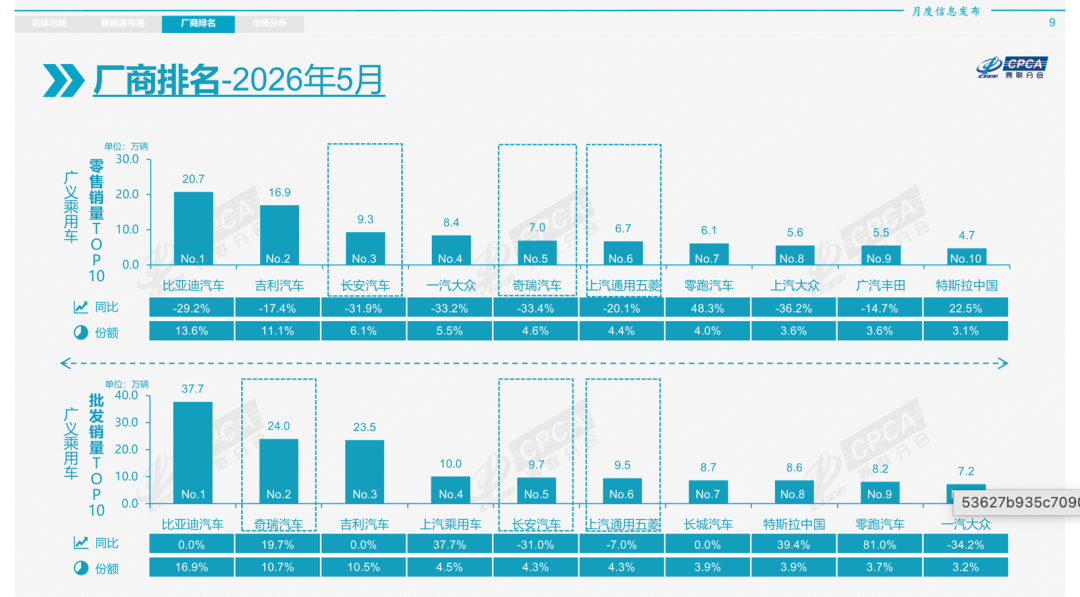

BYD's May sales increased by just 0.26% year-on-year, with nearly all growth coming from exports. That month, it exported 160,600 units, an 80.7% year-on-year surge, accounting for 42% of total sales, while domestic sales fell 24% year-on-year. Chery exported 181,900 units in May, accounting for 73.4% of total sales, effectively transforming into an international automaker reliant on overseas markets. Geely exported 85,000 units in May, an 184% year-on-year increase, with exports rising from less than 13% of total sales last year to 36%.

Data shows that China's auto exports indeed surged in the first half, with cumulative exports exceeding 4.25 million units in the first five months, a year-on-year increase of over 50%. Full-year exports are expected to challenge the 10 million-unit mark. The average export price per vehicle has also risen from 100,000 yuan five years ago to the 300,000-yuan level. Chinese automakers are upgrading from low-price, high-volume exports to supplying mid-to-high-end products globally, marking a major breakthrough for China's automotive industry.

However, we cannot overlook the challenges. The domestic market generally declined by 18% to 40%, and relying solely on exports for growth requires addressing domestic market weaknesses.

Transformation Pains Do Not Dampen Long-Term Optimism

In the premium new energy vehicle market, competition intensified sharply in the first half of this year. 'Selling 30,000 units per month' has become the new benchmark for new forces to establish themselves at the top, while the former '10,000-unit club' has become a life-and-death threshold. The market landscape is rapidly reshaping.

Leapmotor emerged as the biggest dark horse in the first half, precisely targeting the mainstream family market priced between 100,000 and 200,000 yuan. In May, it delivered over 80,000 units, an 81% year-on-year increase, carving out a niche in fierce competition through a volume-driven strategy. NIO achieved growth through a multi-brand layout, delivering 37,700 units in May, with three brands working synergistically to prove the feasibility of transitioning from a single premium brand to a multi-brand strategy. HiPhi relied on the strong sales of the M6 model, delivering 46,000 units in May, a 41% month-on-month increase, rejoining the top tier. Li Auto, XPeng, and Xiaomi stabilized around the 30,000-unit mark, holding their top positions, but the ranking competition has become fiercely competitive.

Meanwhile, the survival space for smaller players continues to shrink. Many newly launched models that previously claimed 'explosive orders' have seen their popularity fade far faster than expected, with 'launch as a hit, delivery as obsolete' becoming the new norm. The industry elimination race is accelerating.

As Zhu Jiangming of Leapmotor said, the Chinese market cannot sustain more than a dozen mainstream new forces. The pace of brand consolidation will further accelerate in the next two to three years, with the top players likely consolidating into single digits.

In stark contrast to domestic and new forces, joint venture brands continue to decline. In the first quarter of this year, their overall market share fell to a historical low of 38.5%. In April, retail sales of mainstream joint venture brands plummeted by 37% year-on-year, far exceeding the market average decline.

The predicament of joint venture brands essentially stems from their slow electrification transition. In the most mainstream household price range of 100,000 to 200,000 yuan, domestic plug-in hybrid and pure electric models now offer configurations and experiences far surpassing those of joint venture brands. With a 150,000-yuan budget, domestic models offer larger spaces, more comprehensive intelligent configurations, and lower usage costs. Consumer choices, reflected in their purchasing decisions, have led to a continuous loss of users for joint venture fuel vehicles.

Although some joint venture brands have begun launching electrified products, both their product positioning and consumer perception lag behind market trends, making it difficult to reverse the overall downward trajectory in the short term. The first half's market performance further confirms that joint venture brands can no longer delay their transformation.

Beyond sales divergences, the automotive industry has also witnessed several noteworthy technological trends in the first half of this year, pointing the way for development in the second half and beyond.

According to an industry insight released this year by the China Society of Automotive Engineers, automotive technological innovation has entered a new phase of 'multiple legs racing simultaneously'.

HEV is no longer a neglected transitional technology but has become a long-term stabilizing force within the fuel vehicle ecosystem. Commercial vehicle electrification is no longer fixated on a single path, with fuel cells recognized as a viable option for medium-to-long-distance heavy-duty transport. L3 autonomous driving has become a necessary threshold for large-scale deployment of autonomous vehicles. AI Agents are transforming intelligent cockpits from 'functional features' into 'intuitive assistants'. Even automotive chips are seeing the best window of opportunity for domestic substitution.

These breakthroughs all point to one conclusion: competition in China's automotive industry has shifted from volume to technological prowess. The second half of the race will hinge on core technological strength, providing solid confidence for the industry's long-term upward trajectory.

Overall, the first half of 2026 marks a turning point as China's automotive market dives deeper into transformation. Market pressure is a normal part of this transition period, but the comprehensive breakthrough in electrification, rapid export growth, and multi-faceted technological innovations all prove that China's automotive industry maintains strong development momentum.

However, we must also recognize that the elimination race has entered its most intense phase. With hundreds of new energy vehicle brands still competing in the domestic market, a significant number will gradually exit in the next two to three years, leaving only a few players to survive and thrive.

For the industry, the first half's trends have provided clear answers. Adapting to electrification trends, focusing on core technologies, and expanding globally are essential to securing a position in the new market landscape.

Note: Images sourced from the internet. Please contact us for removal if any infringement occurs. -END-

-

![]()

Annual Revenue Soars to 24 Billion! Large-Scale AI Models Ignite Edge AI Demand, Quectel Sets Sights on AI-Powered IoT

-

![]()

Left-Hand AIVA, Right-Hand Jiayue! Volcano Engine’s Back-to-Back Moves: Can ByteDance Replicate ‘Hongmeng Zhixing’ Success?

-

![]()

The 'Double-Edged Sword' of Roborock's Operations: Soaring Scale Amid Profit Dilemma Under Heavy Marketing Spend

-

![]()

Agent's 'Anti-Consensus' Strategy in the Second Half: SaaS Companies Carve Out a New Ecological Niche

-

![]()

AI Large Models Compete for the Business of 'Zhang Xuefengs'

-

Chinese Brands Face the 'Twilight of the Gods' and 'Battle of the Gods' at the World Cup

-

![]()

Exclusive | DingTalk's Leadership Change: Next Steps Include Integrating MuleRun

-

![]()

Exclusive | DingTalk's Leadership Change: Next Steps Include Integrating MuleRun