In the First Half of the Year, Three New Car Models Were Introduced Daily—But Were 95% of Them Just Filling the Ranks?

07/02 2026

07/02 2026

461

461

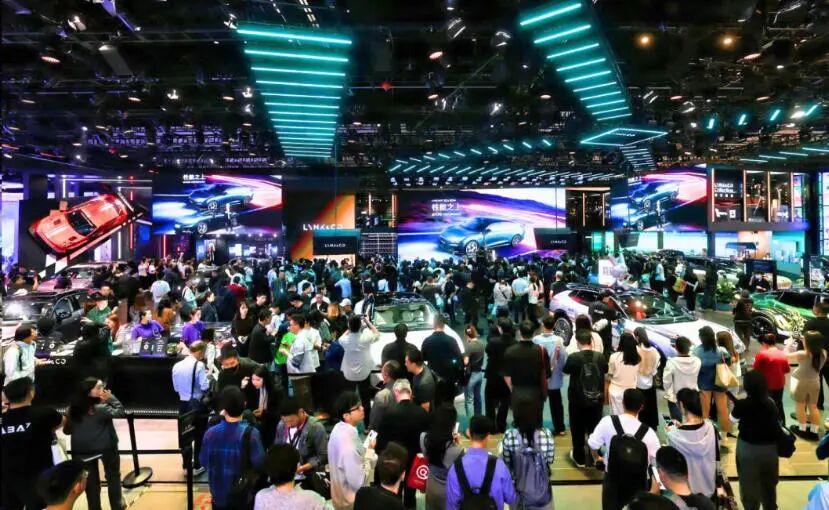

The automotive market in the first half of 2026 delivered a set of results marked by a jarring sense of disconnection. Comprehensive statistical analysis from the Dongchedi new car launch database reveals that approximately 630 new car models were launched domestically during this period. Spread over more than 180 days, this translates to an average of over three new models entering the market each day. A flurry of press conferences, press releases, and livestreams created a bustling atmosphere reminiscent of a market fair.

However, when we look beyond the surface excitement, data from the China Passenger Car Association (CPCA) on retail sales from January to May reveals a stark contrast: only around 30 new models consistently achieved monthly sales exceeding 10,000 units. This represents just 5.5% of the 550 new models launched during the same period. On one hand, there is an oversupply of new cars leading to consumer fatigue; on the other, only a handful of truly competitive flagship products exist. Automakers are frantically launching new models to maintain market presence, yet CPCA data shows a 20% year-on-year decline in cumulative retail sales of passenger vehicles in the first half of the year, with the industry's sales profit margin dropping to a five-year low of 3.4% for the same period. Everyone is asking: Has the Chinese automotive market fallen into a vicious cycle of increased production without revenue growth?

Supply-Side Frenzy Fuels False Prosperity

What many fail to point out is that the figure of 630 models contains far more "water" (a term meaning exaggeration or inflation) than imagined. This comprehensive statistic covers all models announced as "launched," including those on entirely new platforms, vertical replacements, annual facelifts, minor configuration adjustments, models with slightly extended range, new color options, and even limited editions—all can be labeled as "new car launches."

If we count only truly new models built on entirely new architectures or vertical replacements, according to statistics from industry research firm Yilanzhongche, there were only 107 such models from January to May, accounting for less than 20%. By this measure, the number of genuinely new products in the first half of the year would be around 120.

In other words, for every five "new cars" on the market, four are merely old wine in new bottles, with over 80% being minor derivatives of existing models. Annual updates with only infotainment system upgrades, exclusive editions with new exterior colors, and range-extended versions with adjusted battery capacities are essentially just repackaged attempts to regain attention. The core objective has never been to upgrade product competitiveness but rather to grab traffic, boost wholesale volumes, and scoop a little more from the existing market pool. This frantic pace of new launches is driven half by competition and half by auto shows.

In a market characterized by inventory competition, no automaker dares to halt new model launches. If you don't refresh your lineup within six months, competitors will seize your customers with "brand-new 2026 models," even if their only upgrade is wireless charging. The April Beijing Auto Show added fuel to the fire, with the official organizing committee revealing that 181 models made their global debuts at the single event, a more than 50% increase from the previous edition, directly pushing new car numbers to their peak in the first half of the year.

Moreover, with rapid iteration in new energy technologies, the traditional five-to-seven-year replacement cycle of the fuel-powered vehicle (internal combustion engine vehicle) era is obsolete. Today, minor updates every six months and major updates annually are nearly industry standards. Many models are already classified as "old" by the market before they fully ramp up production and refine their supply chains.

Cooling Demand Dilutes Individual Model Sales

As new models flood the market without a corresponding expansion of the overall market, the most direct consequence is the infinite dilution of individual model sales. With an average of three new models launched daily, only 30 truly broke into the "10,000 monthly sales club" in the first half of the year. Among the 550 new models launched from January to May (based on a broad statistical caliber), only 5.5% achieved monthly sales exceeding 10,000 units. Within the broader context of 630 new models launched in the first half of the year, this proportion would be even lower. The vast majority of new models generate buzz only on their launch day, with press releases dominating screens before fading faster than a receding tide, disappearing into the sea of newer offerings within two months without leaving a ripple.

The few breakout hits that emerge mostly carry the familiar label of "cost-effectiveness," supported by publicly verifiable sales data. According to CPCA retail sales data for May, the Leapmotor A10, launched in March, surged to 22,306 deliveries in a single month. This all-electric SUV, which offers lidar and advanced autonomous driving features at a price point below 80,000 RMB, has accumulated over 50,000 sales in three months since launch. SAIC-GM-Wuling disclosed that the Wuling Binguo Pro, launched in late May and targeting the 50,000-80,000 RMB commuter market, surpassed 30,000 cumulative sales within 38 days of launch, comfortably exceeding 10,000 monthly sales. According to Seres' delivery announcement, the Aito M6, launched at the Beijing Auto Show in April, rapidly ramped up deliveries relying on Huawei's autonomous driving technology and HarmonyOS cockpit, surpassing 20,000 deliveries in its second month on the market. Similarly, CPCA data shows that the Geely Xingyuan, which underwent a mid-cycle refresh in May with upgraded independent suspension and FlymeAuto infotainment, sold 38,751 units in a single month, becoming the top-selling refreshed model in the first half of the year.

Additionally, models like BYD's third-generation Yuan PLUS, launched in May, and Li Auto's i6, launched earlier in the year, quickly joined the "10,000 monthly sales club" after their debuts. More notably, consumer sentiment has shifted. Previously, the launch of a major new model would invariably drive a wave of showroom traffic. Now, when consumers see news of a new model launch, their first reaction is often not "I need to check this out" but rather "There will be another new model next month; I'll wait."

Data from a June terminal survey by the China Automobile Dealers Association confirms this trend: the average consumer decision-making cycle for car purchases has lengthened by 12 days compared to last year, with a significant increase in wait-and-see sentiment. With more choices, consumers become more hesitant, stretching the purchase decision-making cycle. New models, originally intended to stimulate consumption, have instead become a reason for consumers to delay purchases—a counterproductive effect that clustered new launches by automakers likely did not anticipate.

Profitability Under Pressure: Trapped in a Vicious Competition Cycle

Even more concerning than sales dilution is the industry's entrapment in a vicious cycle of "increased production without revenue growth," sinking deeper with every struggle. A set of data disclosed by Cui Dongshu, Secretary-General of the CPCA, at the 2026 mid-year automotive industry operation analysis meeting is highly revealing: from January to May this year, the industry generated 4,209.6 billion RMB in revenue, a mere 1.4% year-on-year increase, while operating costs rose by 2.3%. Ultimately, total profit reached 144 billion RMB, a 20% year-on-year decline, leaving the sales profit margin at just 3.4%. Given that terminal price wars continued in June and upstream component costs rose, substantial improvement in industry-wide profitability pressure is unlikely in the first half of the year.

In essence, despite selling more, profits have shrunk, with many brands even losing more money the more they sell. According to Wind's Q1 2026 financial reports for 12 mainstream listed passenger vehicle companies, over half saw a year-on-year decline in net profit attributable to shareholders, with five directly incurring losses. Even industry leaders like BYD and Geely experienced double-digit year-on-year declines in net profit.

Wang Xia, President of the China Council for the Promotion of International Trade Automotive Committee, put it bluntly in a public speech at the 2026 China Automotive Chongqing Forum: "The simultaneous decline in sales, revenue, and profit is historically rare. Sales without profit support are merely hollow numerical games." Nio founder Li Bin also admitted candidly during the Q1 2026 earnings call: "The rapid iteration of new models has caused massive resource waste. It's not uncommon in the industry for billions to be invested in a model only to see it flop." In the end, automakers, supply chains, and consumers all lose out.

The logic of this cycle is straightforward: to maintain market presence, automakers have no choice but to push out new models at a frenetic pace, driving up costs for R&D, marketing, and production line adjustments. However, with an overwhelming number of new products, sales per model become increasingly thin, preventing economies of scale from materializing and keeping costs high. To clear inventory and boost sales, price wars ensue, further eroding profits.

With profits insufficient to support R&D, automakers rely on even more new models to grab traffic and pressure dealers with inventory, creating a self-perpetuating cycle of intensifying competition. Additionally, according to JW Insights monitoring, the average price of automotive-grade memory chips rose by over 30% year-on-year in the first half of 2026, with upstream cost pressures continuing to trickle down, squeezing automakers' profit margins to near-zero.

Ultimately, the spectacle of three new car launches daily cannot sustain a healthy industry. The glory of 30 breakout hits cannot conceal the embarrassment of nine in ten new models merely making up the numbers. Prosperity built on a pile of new models is ultimately fragile. When 80% of so-called "new cars" are merely rebadged, facelifted traffic tools, when consumers grow immune to a barrage of launch events, and when the entire industry bleeds real money on ineffective competition, this extensive (rough, unsustainable) approach is unlikely to endure.

Fortunately, some automakers have begun to hit the brakes, slowing down iteration cycles, consolidating product lines, and concentrating resources on core products. For the industry as a whole, the key challenge ahead is no longer "how many new models can be launched in a year" but rather "how long a single model can sustain market relevance and generate profit." Shifting from quantity competition to quality competition, from traffic grabbing to value creation, is likely the only viable path to escape this vicious cycle.

-

![]()

Preparing for the 6G Era: US Completely Shuts Down 2G Networks, China Unicom Initiates Gradual Decommissioning of WCDMA 3G Networks

-

![]()

Mid-year 2026 Sales Review: Auto Market Shifts from Scale Expansion to Systemic Capabilities for Long-term Positioning

-

![]()

From the ARD Protocol, the Turning Point for the Agent Industry Has Arrived

-

Pinduoduo's Strategic Leap in Xiong'an: Beyond Investment, a Pledge to Flourish

-

Liang Wenfeng Has No Desire to Become Another Sam Altman

-

![]()

Revenue Soars, Losses Mount in Billions, Sales Stumble: Avatr's Hong Kong IPO Bid Amid Breakthroughs and Anxieties

-

![]()

Breaking Industry Records in Financing Speed, the Dark Horse of Embodied AI Rides the Wave of Enthusiasm | Gechao

-

![]()

Pix Exclusive | Mercedes-Benz China Establishes GTM Department to Avoid Repeating CLA's Mistakes