Where is the Way Out for the Chinese Auto Market Amid Industry-Wide Losses?

07/17 2026

07/17 2026

547

547

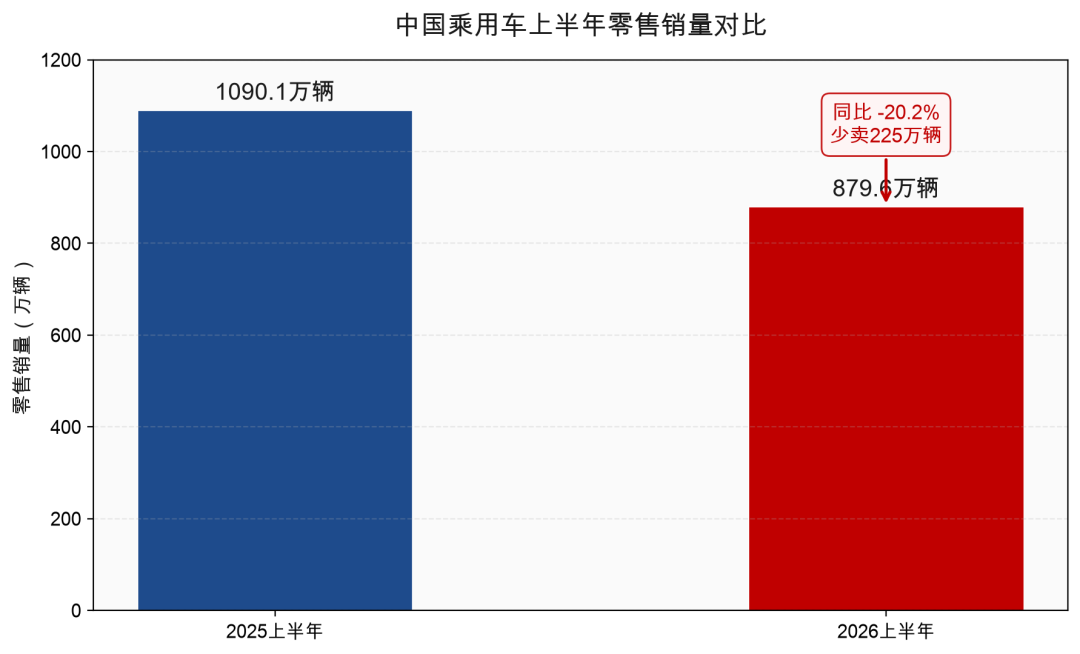

In the first half of 2026, many professionals in the automotive industry likely felt the chill. China's broad passenger vehicle sales reached only 8.796 million units, 2.25 million fewer than the same period last year, equivalent to 12,000 fewer vehicles sold per day across the industry.

Data from the China Passenger Car Association (CPCA) poured cold water on the situation. In June, industry-wide retail sales were only 1.602 million units, a 23.2% year-on-year decline; the cumulative decline for the first half of the year was 20.2%. This marks the ugliest Interim Report (half-year report) for China's auto market in a decade.

Faced with this reality, capital markets responded decisively. The A-share automotive sector lost nearly 900 billion in market capitalization over the half a year (half-year), while Hong Kong's new energy sector plummeted by over 20%. From BYD to Xiaomi, from Great Wall to Li Auto, market values shrank collectively without exception.

In the first half of this year, China's auto market had no winners—the entire industry was losing money. So, where is the way out?

01 The "Three Mountains" Crushing the Industry

The automotive industry is a typical large-scale industry where falling volumes naturally lead to declining profits. However, the decline in sales is just the surface; the real pressure comes from three insurmountable challenges.

The first mountain is the diminishing marginal effect of price wars. Since 2023, China's auto market has been mired in a "price-for-volume" battle for three full years. By the first quarter of 2026, new energy vehicle (NEV) models had an average price cut of 38,000 yuan, while fuel vehicles saw an average reduction of 37,000 yuan.

But did such dramatic price cuts actually boost sales? The answer is no. As seen at the beginning of this article, passenger vehicle sales in the first half of the year fell by 20% year-on-year. Price cuts, once a panacea, have now become a placebo—increasingly ineffective, yet painful to stop.

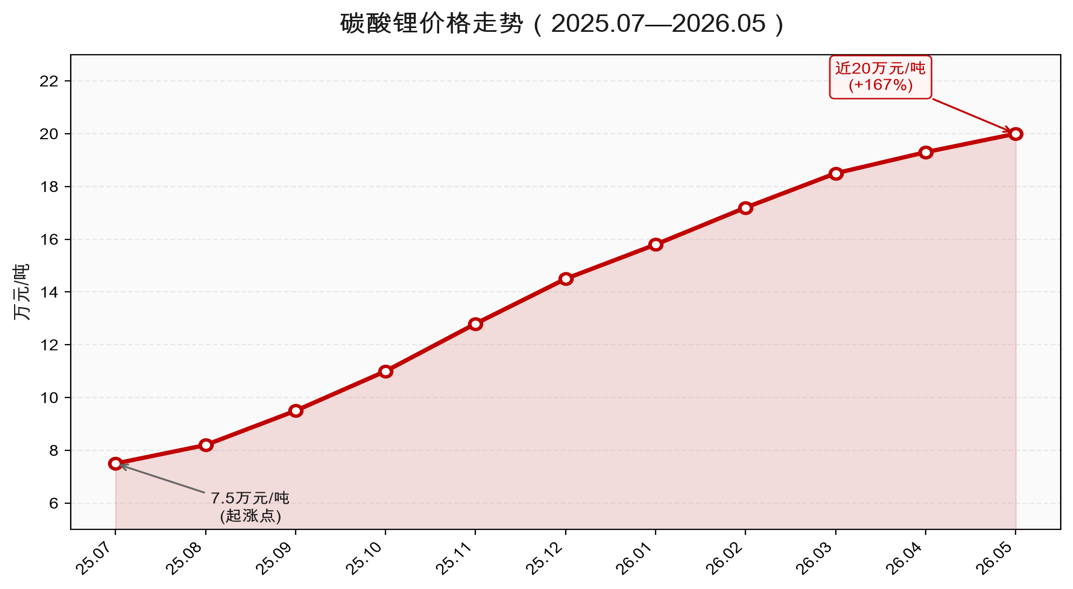

The second mountain is the skyrocketing costs of raw materials and manufacturing. Consider lithium carbonate, the most critical material for batteries: its price surged from 75,000 yuan per ton in July 2025 to nearly 200,000 yuan per ton in May 2026, a 167% increase. Given that battery costs account for 30-50% of a vehicle's total cost, every 100,000 yuan increase in lithium prices adds 3,000-5,000 yuan to the cost of a 50-kWh electric vehicle.

Chips have also seen exaggerated price hikes, with AI and large language models monopolizing advanced production capacity from memory giants. Automotive-grade DRAM prices surged by 180% in three months, adding thousands more to the hardware storage costs per vehicle. Combined with copper prices exceeding 100,000 yuan per ton, aluminum prices breaking 25,000 yuan per ton, and logistics costs rising 12-15% year-on-year, manufacturing costs per vehicle have increased by 15,000-20,000 yuan.

The third mountain is overcapacity and high inventory levels. The contradiction between channel inventory pressure and weak terminal demand is widespread, with dealer inventory warning indices remaining persistently high. Low capacity utilization means higher fixed costs per vehicle, while inventory backlogs tie up significant working capital. This creates a vicious cycle: vehicles aren't selling, but factories keep producing; more production leads to higher inventory; higher inventory strains cash flow. Once trapped in this cycle, escaping is difficult unless demand suddenly surges.

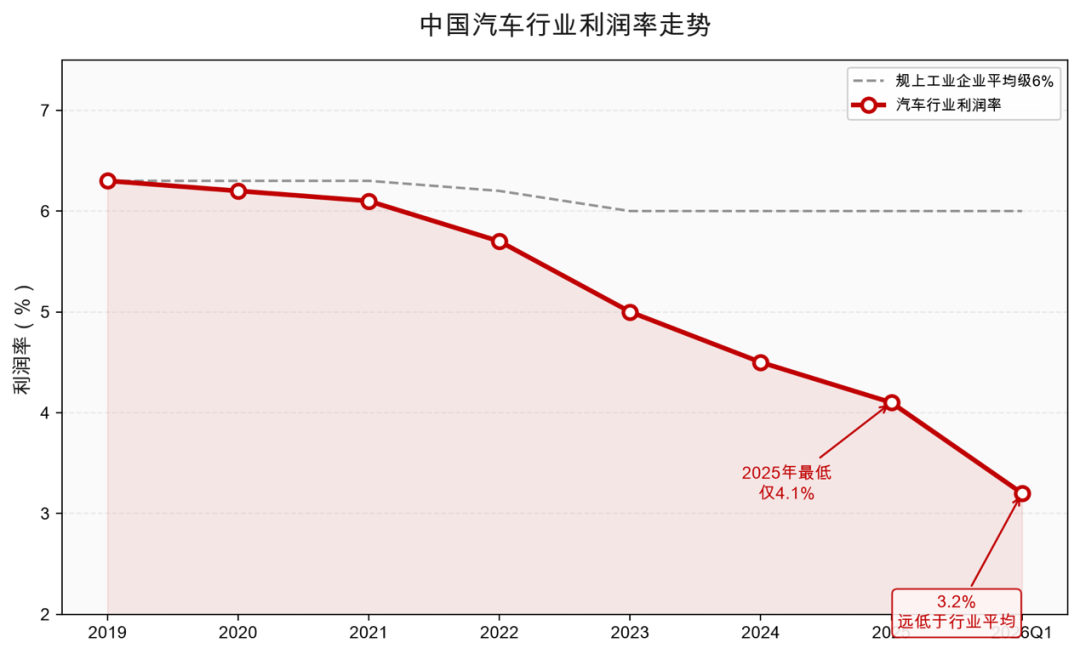

The combined weight of these three mountains is evident. The automotive industry's profit margin fell to 4.1% in 2025, the lowest since 2015; it dropped further to 3.2% in the first quarter of 2026, well below the national average of 6% for industrial enterprises above a certain scale. Capital markets have reclassified automotive stocks from growth to cyclical manufacturing, fundamentally altering valuation logic. The entire industry is trapped in a "higher output without higher efficiency, higher revenue without higher profits" deadlock.

02 No One Can Escape the Cold Winter

A review of financial reports reveals that "losses" dominate the industry.

Consider Xpeng and Li Auto, representatives of new forces. In Q1 2026, Xpeng reported revenue of 13.03 billion yuan, a 17.6% year-on-year decline, with net losses reaching 1.78 billion yuan, up 168.7% from 660 million yuan in the same period last year. Deliveries totaled 62,682 units in Q1, a sharp 33.3% drop year-on-year.

Li Auto, once the fastest new force to achieve profitability, has returned to losses. Q1 revenue was 23 billion yuan, down 11.4% year-on-year, with net losses of 2.3 billion yuan compared to a 647 million yuan profit the previous year. More concerning is Li Auto's plummeting gross margin, which crashed from 20.5% to 7.9%, with vehicle margins falling to 6.1%.

Xiaomi, last year's sales dark horse, is also struggling. Its automotive business reported a 3.1 billion yuan loss in Q1, with its stock price falling nearly 60% from a historic high of 61.45 HKD to 25.86 HKD as of July 15, making it one of the worst-performing new forces this year.

Traditional automaker GAC Motor is bleeding continuously. Earnings previews show GAC's non-recurring net loss for H1 2026 reached 4.8-5.6 billion yuan, marking eight consecutive quarters of losses. Once a cash cow through joint ventures, it has now become a financial burden.

Finally, industry leader BYD reported a 4.085 billion yuan net profit attributable to shareholders in Q1 2026, a 55.38% year-on-year decline. As the absolute leader, this profit halving signals more than any analysis report.

Seres' situation is even more dramatic. Earnings previews released on July 12 indicate an expected loss of 1.5-1.8 billion yuan for H1 2026, compared to a 2.941 billion yuan profit the previous year—a swing from profit to loss. Despite the flagship SUV Aito M9 selling over 10,000 units in June and reclaiming the sales crown in the 500,000-yuan price segment, Aito Automobile still lost 1.05-1.3 billion yuan in H1. This illustrates that even popular brands cannot escape unscathed amid overall market contraction.

The list of profit declines continues: Leapmotor's losses widened by 200%, BAIC's by 189%... What was once a joke about new forces "losing money on every vehicle sold" now applies to the entire industry.

03 How to Survive the Industry Winter?

The winter is indeed cold, but the industry won't stay frozen forever. The more pertinent question is: What paths can lead automakers back to spring?

Earlier, we mentioned overcapacity as one of the industry's pressing challenges. However, China's automotive production capacity is far from saturated when viewed globally. "Going overseas" has become the core pillar for offsetting domestic retail declines. According to CPCA data, national passenger vehicle exports reached 877,000 units in June, an 82.3% year-on-year increase; NEV exports surged by 152.7% to 499,000 units, accounting for 56.9% of total passenger vehicle exports. In other words, more than one in two Chinese vehicles exported overseas is an NEV.

BYD, the industry leader, is accelerating its export drive. In June, BYD's overseas exports reached 174,897 units, a 95% year-on-year increase. For the first half of the year, BYD exported a cumulative 7,878,9367 units, accounting for 43.6% of the group's total sales. At this pace, BYD's export ratio will approach 50% this year, with overseas operations carrying even greater weight.

Similarly, Chery, a pioneer in overseas expansion, exported over 940,000 units in H1 2026, continuously breaking Chinese brand export records. One in every two Chery vehicles sold in Europe is an NEV. SAIC Motor sold 735,000 units overseas in H1, a 48.7% year-on-year surge, with its MG brand ranking sixth in UK brand sales in May. Benefiting from higher average selling prices and gross margins overseas, going global has become a crucial support for more Chinese automakers seeking high-quality growth.

Besides exports, high-end transformation is another key to escaping the industry winter. After all, to generate profits, automakers cannot rely solely on volume; they must raise prices. Hongmeng Intelligent Mobility (HIM) achieved an average transaction price of 391,000 yuan in May, ranking first among Chinese brands and even surpassing some best-selling models from Mercedes-Benz, BMW, and Audi. The Aito brand alone has an average transaction price of 409,000 yuan. In the premium market above 300,000 yuan, Chinese brands now have true dual benchmarks for "price + volume."

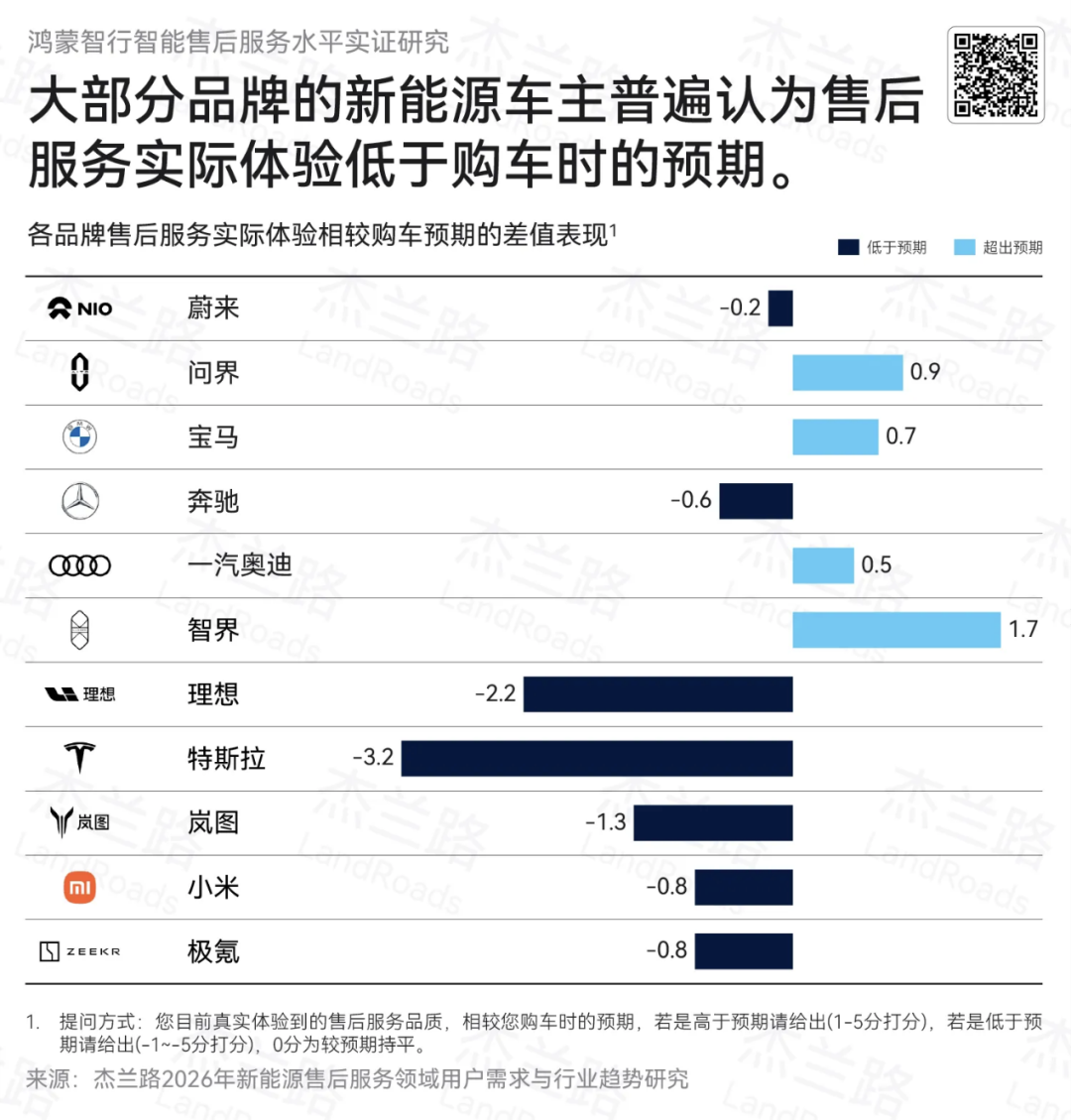

High-end transformation brings not only profit margins but also brand moats. The Aito M9 topped both the plug-in hybrid and pure electric residual value rankings for H1 2026, while the Aito M8 and M5 ranked in the top three of their respective segments. In Jelanyu's 2026 after-sales service survey, Aito's after-sales experience exceeded user expectations by 0.9 points, surpassing traditional luxury brands, with Smart Vision exceeding expectations by 1.7 points—the highest in the survey. "Investors look at market cap, consumers look at experience." When a brand's after-sales experience surpasses traditional luxury rivals and its residual value leads the industry, it signifies a completed high-end transformation in consumer perception.

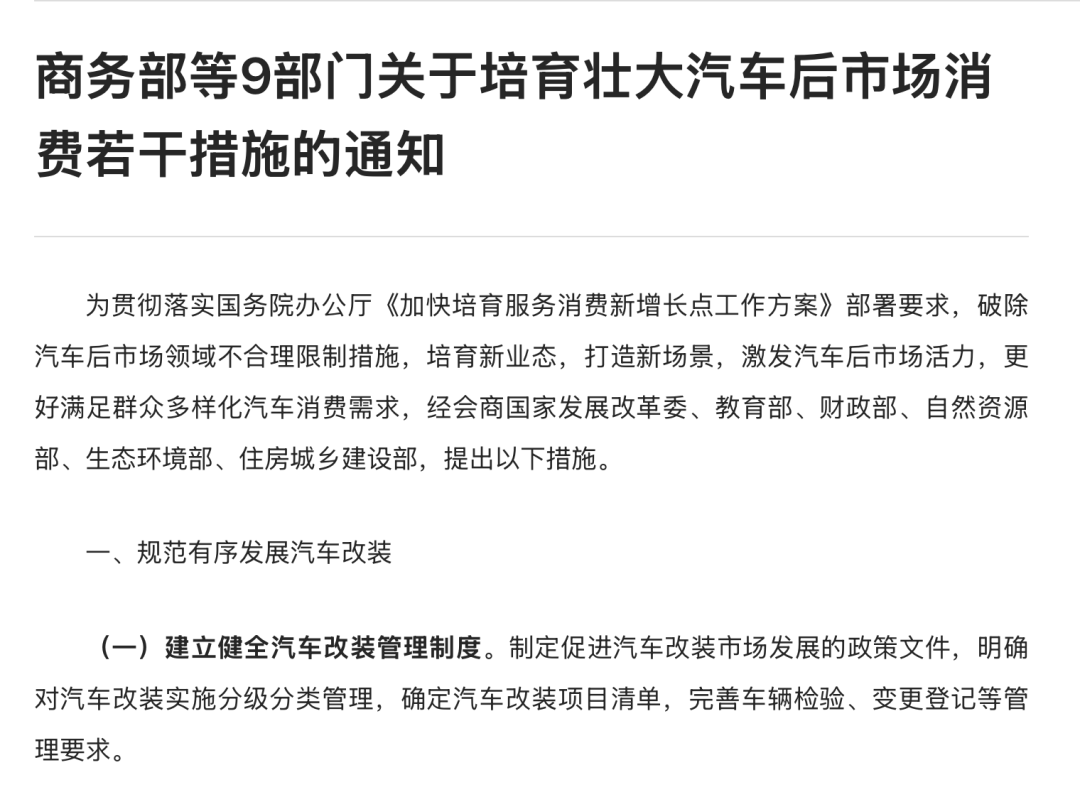

Policy has also proposed new solutions for the current industry winter. In March, nine departments including the Ministry of Commerce jointly issued the "Notice on Several Measures to Cultivate and Expand Automotive Aftermarket Consumption," explicitly urging localities to relax access restrictions in areas such as vehicle modifications, RV camping, classic cars, maintenance insurance, automotive racing, and car rentals. It's clear that aftermarket services spanning the entire automotive lifecycle will become automakers' second growth curve.

Engaging in price wars in a shrinking market leads nowhere. Only automakers that excel in product quality, high-end positioning, overseas expansion, and service penetration can emerge from this winter. While industry-wide cyclical fluctuations are inevitable, the enterprises that truly withstand cycles are always those that have built genuine barriers in product strength, brand power, and service systems.

-

The Moment to Evaluate Montage Technology Has Arrived

-

![]()

StepOn Has Solved the Monetization Challenge of Large Models with Just a Smartphone

-

![]()

Is a Camera the New AI Safety Guardian? Hikvision Introduces Active Vision Operation Monitoring Gun-Ball Camera at WAIC 2026

-

The Second Half of AI: Cost-Effectiveness Takes Center Stage

-

![]()

Location, Concentration, and Trajectory Tracking: Hikvision’s TDLAS Gas Cloud Imaging Telemetry System Debuts at WAIC 2026

-

The 'AI Study Tour' Under the Original Equipment Manufacturer Model is Set to Create a New Wave of Internet-Famous Science and Innovation Cities

-

![]()

Now, There's a 'Basis' to Curb 'Price Wars': Future Reports of Automakers Setting Low Prices Will Be Probed Under New Rules

-

![]()

WAIC 2026: Farewell to Parameter Races, Full-Chain AI Commercialization