Six Years in the Red: Excluding Non-Recurring Items, OFILM’s Net Profit Struggles Despite 22.1 Billion Yuan Revenue

04/02 2026

04/02 2026

465

465

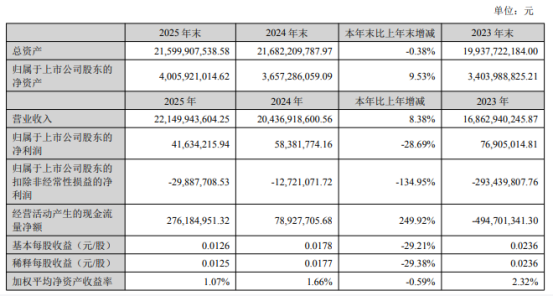

On the evening of April 1, OFILM unveiled its 2025 annual report, revealing a revenue of 22.15 billion yuan, marking an 8.38% year-on-year increase. Given the incomplete recovery of consumer electronics end-market demand and fierce industry inventory competition, this growth is commendable.

However, the profit picture is less rosy. Net profit attributable to shareholders stood at 41.6342 million yuan, a 28.69% decline year-on-year. Excluding non-recurring gains and losses, the net profit was -29.8877 million yuan, with losses widening by 134.95% year-on-year. This marks the sixth consecutive year that OFILM has reported a negative net profit when excluding non-recurring items.

For this former industry leader, which once shone brightly during the heyday of consumer electronics, these financial results paint a complex picture: revenue growth coexists with a decline in profits, while the main business's ability to generate cash has been under pressure for six straight years.

In the optics industry, net profit excluding non-recurring items is a key indicator for assessing the true competitiveness of a module or component manufacturer. Six consecutive years of losses reveal that while OFILM has managed to restore its revenue scale through new ventures like smart cars and VR/AR after cutting ties with Apple's supply chain, the value of its businesses has yet to fill the massive gross profit gap left by its traditional consumer electronics operations.

OFILM's annual report underscores the persistent severity of the "bottom of the smile curve" dilemma in the module manufacturing sector. OFILM began with camera modules, a field that once symbolized the rise of domestic optics. However, with technological democratization and overcapacity, the gross margins of pure module packaging and assembly have long lingered near break-even levels.

Despite OFILM's recent efforts to venture into high-end lenses, 3D sensing, and automotive ADAS lenses in a bid to ascend to high-value-added links in the upstream supply chain, financial data indicates that the "friction costs" of this transformation remain significant. As the industry transitions from supply shortages to intense internal competition, scale alone is no longer a safeguard—cash flow and gross margins have become the true lifelines for enterprises.

This is why outside observers naturally focus on OFILM's highly anticipated "second curve"—the perception systems in the smart car sector. Undeniably, with the rapid advancement of automotive intelligence, demand for optical components such as in-car cameras and LiDAR is soaring, offering OFILM vast growth potential.

However, current data shows that the scale of the automotive business is still insufficient to fully counterbalance the downturn risks in consumer electronics. Moreover, the automotive supply chain is characterized by long certification cycles, extended payment terms, and fierce competition, with established players like Sunny Optical and Lianchuang Electronics already making significant inroads. For OFILM, the key to escaping its current predicament of "revenue growth without profit growth" lies in transforming automotive business "revenue growth" into "profit growth." This challenge is not unique to OFILM but is a common issue faced by all consumer electronics supply chain companies venturing into automotive optics.

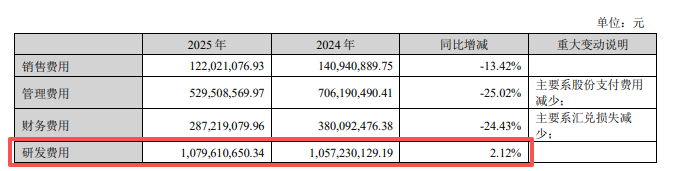

Meanwhile, the balance between asset write-downs and R&D investment has become increasingly precarious. The optics industry is both technology-intensive and capital-intensive. Reflecting on OFILM's past financial volatility, asset write-downs—particularly inventory devaluation and fixed asset impairments—have often been the primary culprits eroding profits. In today's era of rapid technological iteration, with periscope lenses, glass-plastic hybrids, optical image stabilization, and other new technologies emerging endlessly, if companies cannot accurately predict technological trends, earlier heavy capital investments can quickly turn into sunk costs.

The annual report reveals that OFILM maintains a high level of R&D investment, reflecting its attempt to safeguard its technological edge. However, how to enhance the commercialization efficiency of R&D and avoid the dilemma of "research without development, development without profitability" is a critical question not just for OFILM but for the entire Chinese optics industry.

Ultimately, OFILM's 2025 financial report serves as a mirror, reflecting its struggle to rebuild its cash-generating capabilities after dramatic external changes. A net profit of 41.63 million yuan is razor-thin for a leader with annual revenue exceeding 20 billion yuan, leaving little margin for error. On a positive note, OFILM has not fallen behind; it still possesses technological positioning capabilities in automotive optics, infrared sensing, and newly deployed VR/AR optical solutions.

The future optics race will hinge on refined cost control, a healthy customer structure, and the ability to "monetize" technologies in emerging application scenarios. Whether OFILM can achieve a "turnaround" in net profit excluding non-recurring gains and losses in 2026 will not only mark a turning point for its capital market valuation but also serve as an important indicator of whether China's optics supply chain has truly achieved high-quality development after industry consolidation.

-

![]()

Market Share Dilemma: DJI vs. Insta360—Is It '40-40' or '60-30'?

-

![]()

Market Share Dilemma: DJI vs. Insta360 – A '40-40 Split' or '60-30 Split'?

-

![]()

It's Kunlunxin's Turn to Play

-

![]()

Is the New Performance Peak Just the Starting Point? What Will Be Crystal-Optech's Next Destination?

-

![]()

Goertek Pours 69 Million Yuan into Elite Precision: Ramping Up Optical Precision Manufacturing and R&D Capabilities

-

![]()

Avatr Attempts HKEX Listing Again, With 20,000 Vehicles Sold in First Five Months

-

![]()

NVIDIA Announces 10-Fold Production Capacity Increase in 2 Years, Disrupting the Energy Storage Industry

-

![]()

AI Enters the Second Half: Models Are No Longer Scarce, What’s Truly Scarce Are Computing Power, Scenarios, and Trust