What are the growth areas in the storage sector in 2026?

01/19 2026

01/19 2026

713

713

In 2026, the global storage industry is set to experience unprecedented transformation and opportunities. Strategic adjustments by industry giants are reshaping market supply and demand dynamics, AI technological advancements are driving new storage requirements, and the commercial space boom is opening up a new frontier in space storage. These three growth areas are interconnected, propelling the storage industry into a new era of development. From consumer markets to AI data centers, and from Earth's surface to outer space orbits, the application boundaries of storage technology continue to expand, becoming a core pillar for the development of the digital economy and cutting-edge technologies.

01

Domestic DRAM Expansion: Global Breakthrough Amidst Giant Withdrawals

Currently, storage chip manufacturers are focusing on producing third-generation high-bandwidth memory (HBM3E), an ultra-high-speed memory used in GPUs and AI accelerators for AI inference and training. This has put pressure on server DRAM production capacity. Companies like Google and Microsoft are also expanding their AI service businesses based on inference, further driving demand for server DRAM.

Against this backdrop, the global storage market is undergoing profound restructuring. Micron has even shut down its 29-year-old consumer brand, Crucial. This trend reflects the inevitable shift by storage giants toward high-value-added sectors but has unexpectedly opened a breakthrough for Chinese storage companies in the global market.

Simultaneously, the AI-driven supply-demand imbalance has directly triggered memory price fluctuations. Samsung and SK Hynix plan to raise server DRAM prices by 60%-70% in the first quarter of 2026 compared to the fourth quarter of 2025, with PC and smartphone DRAM prices also set to increase. Traditional DRAM contract prices are expected to rise by 55% to 60% month-on-month.

This has also impacted the supply of core components for OEM manufacturers like Dell and numerous third-party memory/SSD brands. A supply disruption could lead to a severe "shortage" crisis in the global consumer storage market, with Samsung becoming the world's largest supplier of storage and NAND, further consolidating market concentration.

Under the dual pressures of rising prices and supply shortages, global OEM manufacturers are actively diversifying their supply chains. HP has initiated qualification reviews for Chinese memory suppliers. While a large-scale shift to small and medium-sized suppliers is unlikely in the short term, completing "qualification certification" marks Chinese storage companies' official entry into the candidate list for international mainstream supply chains. The commodity nature of memory chips provides a natural advantage for this transition—strong interchangeability between brands and models, with end consumers focusing more on performance stability and price reasonableness than the identity of the chip supplier. This means Chinese storage companies can gain "replenishment" market share with cost-effective products alongside giants like Samsung and Micron, gradually solidifying their global market position. Industry experts predict that the market supply-demand imbalance will persist until at least 2028.

Chinese memory expansion overseas is both inevitable and the future norm.

02

AI Inference Drives Explosive Growth in NAND Demand

When DRAM falls short, NAND steps in. Amid tight DRAM supply, NAND storage has emerged as a core beneficiary in the AI era, particularly with the explosive growth of AI inference scenarios, which are reshaping NAND market demand. AI large models' requirements for long-context processing and massive parameter storage are driving NAND upgrades from traditional storage applications to core AI infrastructure.

NVIDIA's technological innovation has become a key engine for demand growth. Its BlueField-4 DPU provides an additional 16TB of NAND context space per GPU, effectively addressing memory loss and HBM capacity shortages during AI operations. In the new-generation Rubin NVL72 architecture AI servers, four BlueField-4 chips manage memory uniformly, with each GPU equipped with 16TB of NAND dedicated to storing AI "memory." Based on 100,000 racks, this architecture alone will create 115.2EB of additional NAND demand, accounting for 12% of global supply in 2025, significantly boosting NAND market demand.

DeepSeek's open-source Engram technology further expands NAND's application boundaries. This "conditional memory" mechanism peel off (translates to "separates") the rote memorization part of large models from neural network computations, delegating it to terabyte-scale static memory tables, forming a new "MoE computation + Engram static memory" architecture. Static memory tables are highly likely to adopt a tiered storage solution (DRAM + SSD hot/cold tiering). DeepSeek Engram shifts the storage battleground for AI large models from expensive HBM memory to more cost-effective DDR5 + NVMe systems, significantly reducing AI model deployment costs while further driving NAND storage demand.

03

Space Storage: A Specialized Storage Blue Ocean Driven by Commercial Space

The explosive growth of commercial space is opening up a new frontier for the storage industry beyond Earth. Global satellite deployment has entered a boom phase: data from the U.S. Satellite Industry Association shows that the number of in-orbit satellites increased from 958 in 2010 to 3,371 in 2020, with projections exceeding 100,000 by 2030. China filed for 203,000 satellite frequency and orbit resources with the ITU in late 2025, covering 14 satellite constellations—a record for China's largest international frequency and orbit application. Among them, the CTC-1 and CTC-2 constellations, applied for by the Radio Spectrum Development and Technological Innovation Research Institute, each request 96,714 satellites, totaling 193,428, accounting for over 95% of the total application. Other applicants include China StarNet, China Mobile, and Galaxy Space.

Soochow Securities points out that looking ahead to 2026, the commercial space industry will see multiple catalysts, particularly the Intensive maiden flight ( dense maiden flights) of multiple reusable/large-capacity commercial rockets, which will significantly enhance rocket payload capacity and address previous bottlenecks in satellite communication development. China's low-orbit satellite internet entered bulk launch construction in the second half of 2025, with larger-scale launches expected in 2026, further accelerating industry development.

Meanwhile, the U.S. Federal Communications Commission approved SpaceX's next-generation satellite constellation plan, authorizing the deployment of 7,500 second-generation Starlink satellites in addition to the existing 8,000, bringing the total number of globally approved in-orbit second-generation satellites to over 15,000.

With the exponential growth of satellites, the commercial space boom is directly driving demand for space-grade specialized storage chips. These chips must pass stringent space certification to ensure long-term stable operation in extreme space environments.

The massive deployment of satellites has transcended their traditional role as "signal relays," evolving into intelligent platforms that integrate data collection and processing. Earth observation satellites generate vast amounts of remote sensing data daily, communication satellites must handle increasing high-throughput traffic, and new-generation satellites are equipped with onboard AI processing capabilities. So, how can space data be securely stored?

Space represents the "ultimate test" for storage devices. High-energy particle radiation, extreme temperature swings from -55°C to 125°C, heat dissipation challenges in microgravity, and severe vibration during spacecraft launch and docking pose Deadly Test (fatal challenges) to storage chips. Ordinary consumer-grade storage chips are prone to data corruption, component failure, or complete breakdown in such environments. Only space-grade certified specialized storage chips can shoulder the responsibility of space data storage.

Storage devices on space stations face even harsher challenges, requiring not only tolerance to extreme environments but also high reliability for long-term on-orbit operation. High-energy particles can penetrate device packaging, directly damaging chip transistor structures and causing data loss or logical errors. Extreme temperature differentials lead to material thermal expansion and contraction, reducing electronic component lifespans. Microgravity diminishes heat dissipation efficiency, while frequent vibrations impose stringent standards on device mechanical stability. The cumulative effects of these challenges make ordinary storage products unsuitable for space station environments.

To overcome these technical hurdles, chip manufacturers must break through three core technological barriers:

First, radiation-hardened technology. By employing specialized material packaging, redundant circuit design, and SOI (Silicon-on-Insulator) radiation-resistant processes, radiation-induced error rates can be reduced to aerospace-grade standards. For example, a "triple modular redundancy" architecture runs three independent circuits simultaneously, allowing the system to recover correct data through redundancy checks even if one circuit is damaged.

Second, wide-temperature adaptability optimization. Specialized packaging materials resistant to high and low temperatures are selected, with integrated temperature sensors and dynamic adjustment circuits inside the chip to enable adaptive stable operation under extreme temperatures. Some high-end products even incorporate micro thermal pipe active cooling systems for precise temperature regulation.

Third, mechanical structure reinforcement. Metal-reinforced casings and shock-absorbing brackets, paired with anti-loosening locking structures, resist severe vibrations during launch and docking. Internal component layouts are optimized to place core components like controller chips in low-vibration areas and secure them with potting compounds to prevent displacement in microgravity.

A qualified space-grade storage device must undergo rigorous "full-dimensional extreme testing." Radiation testing: Simulating space radiation environments in particle accelerators for continuous irradiation lasting hours to days to verify chip resistance to single-event upsets and single-event latches. Temperature cycling testing: Repeatedly switching between -55°C and 125°C for hours per cycle to simulate extreme space temperature variations and test material and component tolerance. Vibration and shock testing: Replicating the mechanical environment of spacecraft launch and docking on vibration tables to verify device structural robustness. Lifespan testing: Conducting continuous read/write tests for months or even years to ensure performance does not degrade during long-term on-orbit operation.

Only products that pass all tests can earn their "ticket" to space.

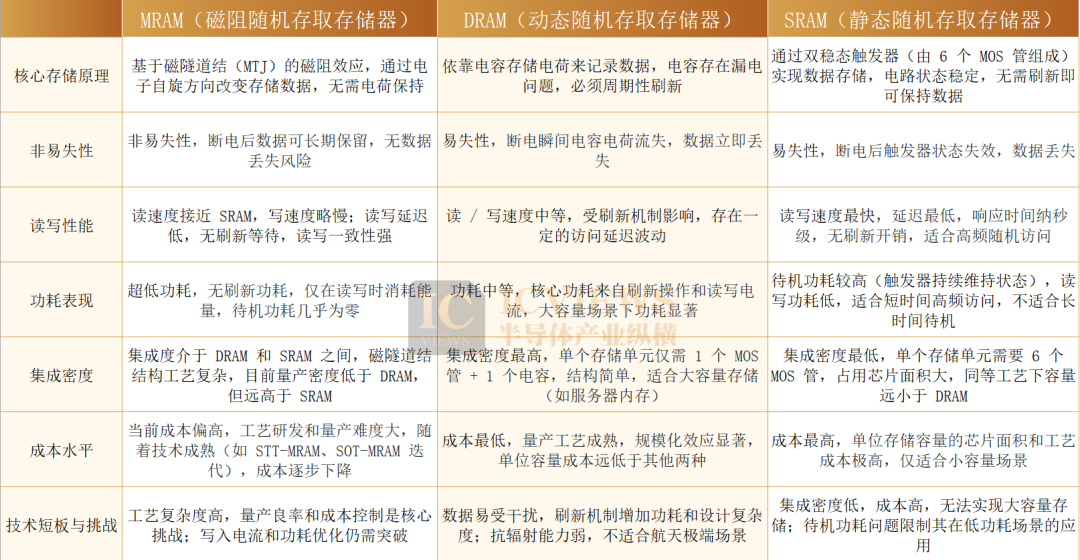

Among numerous candidate technologies, Magnetoresistive Random Access Memory (MRAM) stands out with its exceptional performance, emerging as a promising star in space storage. MRAM is inherently immune to single-event upsets caused by space radiation and offers a nearly permanent lifespan. It combines symmetric read/write speeds with ultra-low operational power consumption, achieving a "faster speed, lower power" dual breakthrough compared to same-density Dynamic Random Access Memory (DRAM), perfectly aligning with the energy constraints of long-distance space travel. In scenarios where spacecraft are far from the Sun and solar power is limited, MRAM's low power consumption advantage becomes particularly pronounced, enabling it to handle more onboard data processing tasks while reducing system energy consumption, significantly lowering the risk of space mission failures. Japan's Earth observation satellite, SpriteSat, upgraded its magnetometer subsystem's memory to MRAM, validating the technology's space application value.

Additionally, storage chip giant Micron Technology launched its first space-grade verified, radiation-resistant Single-Level Cell (SLC) NAND flash memory last year, marking the starting point for its space storage product line. The company is also establishing a space engineering laboratory to target the space product market. Micron's space-grade NAND flash memory features a single-chip capacity of 256Gb, the highest density for space-use NAND products currently available. It has passed critical verification tests required by NASA and U.S. military standards, including temperature aging, Total Ionizing Dose (TID), and Single-Event Effects (SEE), confirming its long-term stable operation in high-radiation and extreme environments, meeting the high reliability standards for space missions.

The storage industry in 2026 will face both opportunities and challenges. Domestic DRAM companies will seek breakthroughs amid global supply chain restructuring, NAND storage will achieve value upgrades with the AI inference boom, and space storage will open up new frontiers in the commercial space wave. These three growth areas will not only reshape the storage industry's market landscape but also support the development of cutting-edge fields such as the digital economy, artificial intelligence, and aerospace. With continuous technological innovation and expanding application scenarios, the storage industry is entering a new golden era of development. Companies that can accurately grasp these growth areas and breakthrough core technologies will ultimately dominate the global market competition.

-

![]()

Jitian Xingzhou: A Pioneer in Optical Payloads Secures Hundreds of Millions in Series B Funding!

-

![]()

Orders Secured Through to the Second Half of the Year! The Rationale Behind the 'Surge' in Demand for This Company’s Optical-Grade Base Films

-

![]()

Beyond Patents: The Retail Rivalry of Insta360 and DJI Unfolds

-

![]()

180 Billion Market Cap Vanished! How Did Seres Fall So Far?

-

![]()

Blockbuster! Domestic storage takes the global double crown for the first time, from an AI company

-

![]()

China Spearheads Formulation! World's Pioneering Global Technical Regulation for Automated Driving Systems Greenlit and Unveiled

-

![]()

Farewell to Pulsed Support Policies: Three Major Auto Policy Directions from Multiple Departments Take Effect on the Same Day

-

![]()

Embercore AI’s Accelerated Funding: The Robot Industry’s Shift Toward ‘Learning Systems’